Tax Compliance Readiness 2026: A Practical Roadmap for Growing Businesses

Prepare your business for tax compliance readiness in 2026 with our practical roadmap designed for growing companies.

Most startups fail because of cash problems, not bad ideas. Yet many founders skip basic startup financial controls, treating bookkeeping as an afterthought.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how early financial discipline separates thriving businesses from those that crash. The good news: strong financial hygiene isn’t complicated, and it’s never too early to start.

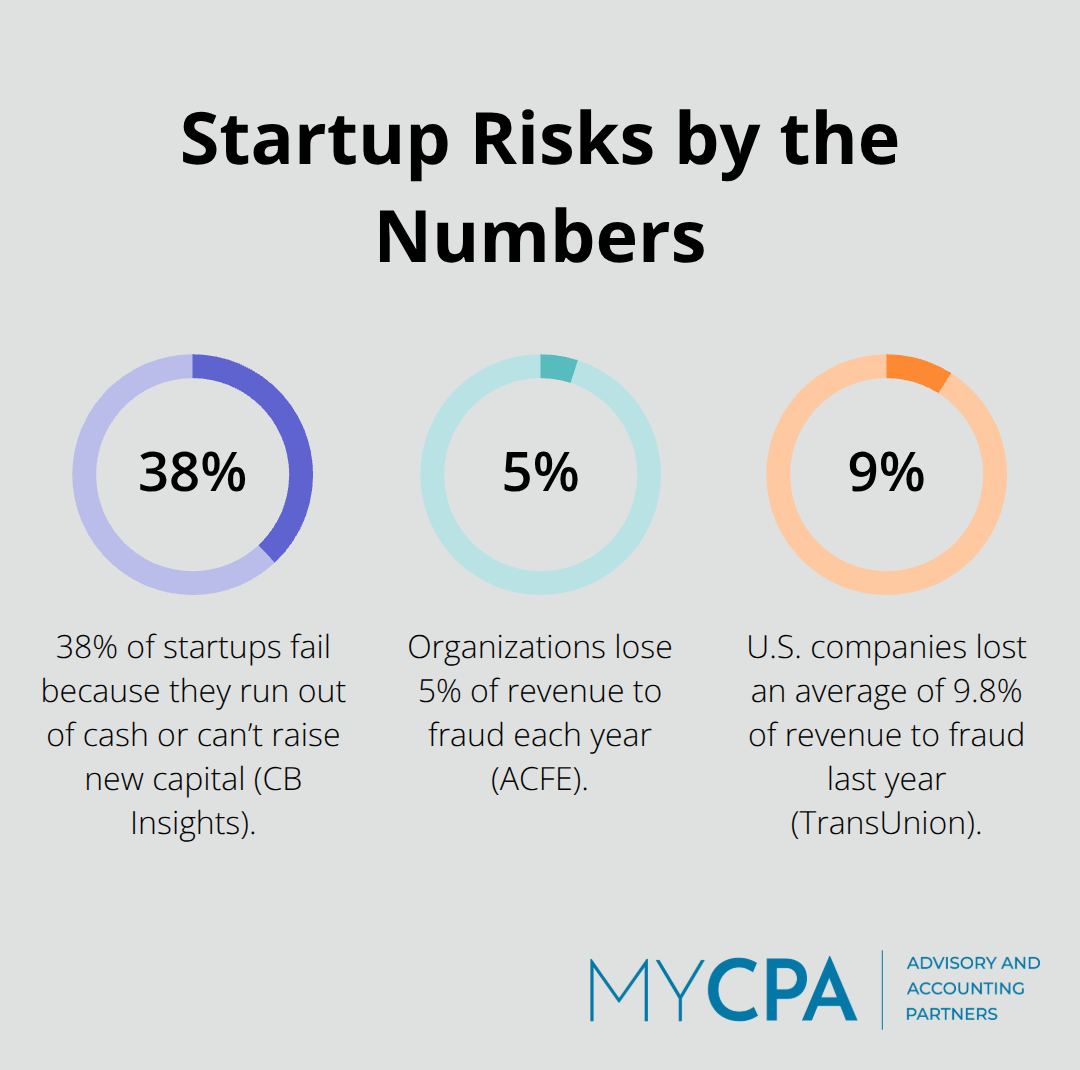

Cash flow problems kill startups faster than bad products. According to CB Insights, 38% of startups fail because they run out of cash or fail to raise new capital. The difference between startups that survive and those that collapse often comes down to one thing: whether founders caught cash problems early enough to fix them. Financial controls give you that early warning system.

Without them, you’re flying blind. You won’t know if your bank balance is dropping until it’s nearly gone. You won’t spot unauthorized spending or accounting errors until they’ve compounded into serious problems. The Association of Certified Fraud Examiners reports that organizations lose 5% of revenue to fraud each year. That’s not a theoretical risk-it’s money walking out the door while you’re distracted building your product. The moment you implement basic controls like bank reconciliation, expense approvals, and segregation of duties, you shift from reactive to proactive. You catch problems in week two instead of month six. That speed matters because cash is survival.

Financial controls transform your cash position from a mystery into a dashboard you check daily. Most founders don’t realize how quickly small leaks become fatal. If you’re spending $50,000 monthly and you don’t reconcile your accounts for three months, you could easily miss $30,000 in unauthorized corporate card charges or duplicate vendor payments. Implement monthly bank reconciliation, set up approval workflows for expenses above a certain threshold (start at $500), and require dual authorization for any payment over $1,000. These aren’t bureaucratic busy work-they’re the difference between catching a $10,000 problem in month one versus discovering a $150,000 problem during fundraising. As you scale and hire team members, controls become non-negotiable. The ACFE found that smaller firms with fewer than 100 employees incur significantly higher fraud losses per incident than large firms because weak internal controls invite mistakes and misuse. A simple rule: the same person should never initiate, approve, and record a transaction. Separate those duties across at least two people from day one.

Investors expect clean financials before you pitch. Not after you’ve secured funding-before. They want to see that you track cash, that your books make sense, and that you have basic controls in place. Most founders think financial hygiene is something you build right before fundraising. That’s backwards. If you wait until you’re raising capital to get your act together, investors will assume your financial management is sloppy everywhere else. Start now with a cloud accounting system like QuickBooks Online or Xero, establish a monthly close process, and document your approval procedures. This creates an auditable trail that lenders and investors demand. When you’re ready to raise, you’ll hand over three years of precise financial data instead of scrambled records and handwritten notes. That confidence translates directly into better terms, faster due diligence, and investor willingness to back you.

Fraud and embezzlement drain startup cash, cause lasting reputation damage, trigger costly investigations or charges, and hinder fundraising. Small businesses face disproportionate risk because founders often wear too many hats and can’t maintain proper oversight. A founder who approves all expenses, records them, and reconciles the bank account has created a perfect environment for error or theft. The ACFE data shows that asset misappropriation is the most common fraud type in small businesses. You prevent this by splitting responsibilities. One person prepares payments, another signs or approves them. One person records transactions, another reconciles accounts. These simple separations cost nothing but catch problems fast. The longer you wait to implement controls, the harder they become to introduce. Teams resist new approval processes. Founders resist losing autonomy. But controls don’t restrict growth-they enable it. With clean financials and documented procedures, you scale confidently. Without them, you scale recklessly and discover problems too late.

The foundation of financial hygiene rests on three non-negotiable controls that cost nothing to implement but save thousands in errors and fraud. Start with complete separation of business and personal finances. Open a dedicated business bank account and corporate credit card immediately, even if you’re a sole proprietor. Never pay startup expenses from your personal account and reimburse yourself later. This single step eliminates the accounting nightmare of commingling funds and protects you during tax season and audits. Use a business account with clear transaction history and separate statements.

Many founders delay this thinking it adds complexity, but the opposite is true. A business account simplifies everything because every transaction flows into one system.

Next, implement monthly bank reconciliation without exception. Reconciliation means comparing your bank statement to your accounting records to catch discrepancies. Set aside two hours each month to match every deposit and withdrawal. This catches duplicate charges, unauthorized transactions, and accounting errors before they compound. New data reveals U.S. companies lost an average of 9.8% of revenue to fraud-46% more than last year and 27% above the global average. Monthly reconciliation catches that theft in week one, not month six. Use QuickBooks Online or Xero to automate this process. Both platforms connect directly to your bank and flag transactions that don’t match your records.

Finally, establish a written approval procedure for all expenses above a threshold you define. Start at $500 for early-stage startups. Any expense below $500 goes straight to your accounting system. Any expense above $500 requires written approval from you or a designated leader before payment. For expenses above $1,000, require two approvers. Document these approvals in your accounting software or email and keep them on file. This prevents impulse spending, catches duplicate vendor payments, and creates an auditable trail investors demand.

Segregation of duties is the principle that stops fraud cold. The same person should never initiate a payment, approve it, record it, and reconcile it. Split these responsibilities across at least two people from day one. If you’re a solo founder, this seems impossible, but it’s not. One person initiates and records the expense in your accounting system. You as the founder approve and sign off on the payment. This two-step process takes five minutes but eliminates the environment where theft thrives. As you hire, assign one team member to manage accounts payable and another to reconcile the bank account monthly. This creates natural checks and balances.

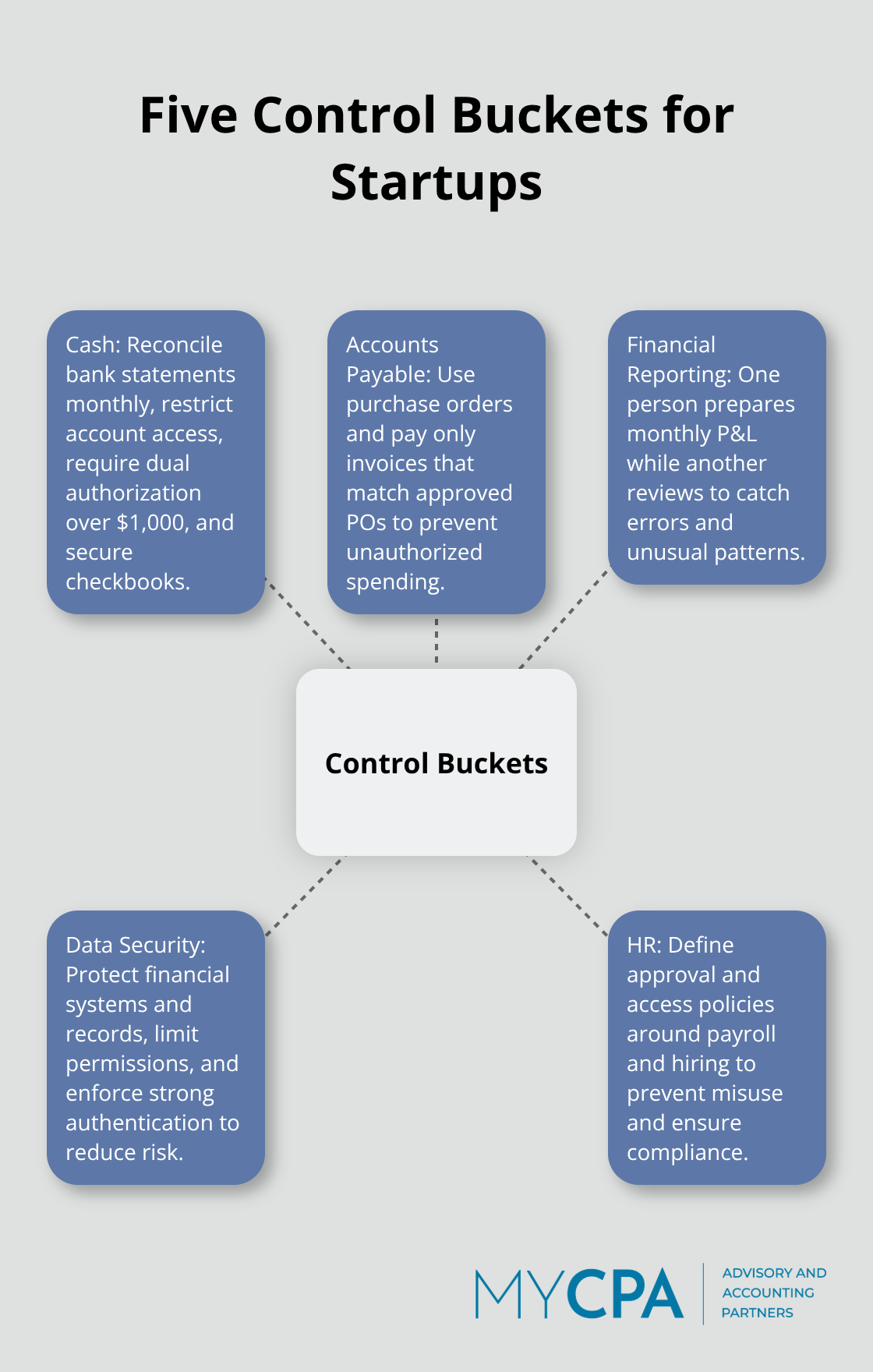

NetSuite’s framework for financial controls identifies five key buckets for startups: cash, accounts payable, financial reporting, data security, and HR. For cash specifically, implement these practices immediately. Reconcile bank statements monthly without fail. Limit who has access to your business bank account and credit cards. Require dual authorization for any disbursement over $1,000. Keep checkbooks locked and separate duties so one person writes checks and another signs them.

For accounts payable, formalize the process with a simple rule: no invoice gets paid without a matching purchase order. This prevents paying for goods or services you didn’t authorize. For financial reporting, assign one person to prepare your monthly profit and loss statement and another to review it independently. This catches calculation errors and unusual spending patterns. These controls scale with your business. Start lean with the essentials today and add sophistication as you hire. The moment you move beyond solo operations, your approval procedures and segregation of duties become the backbone that prevents costly mistakes and keeps your team accountable.

Founders repeat the same financial control mistakes, and these errors cost real money. The most common mistake is postponing bookkeeping until revenue climbs or fundraising begins. This creates a financial mess that takes weeks to untangle. You end up hiring an accountant to reconstruct months of transactions, categorize expenses incorrectly, and miss tax deductions worth thousands. Worse, when investors ask for historical financial data, you scramble to explain gaps or inconsistencies that damage credibility. Start bookkeeping on day one, not day 100. Open your business bank account and set up QuickBooks Online or Xero immediately, then spend 30 minutes each week to categorize transactions. This habit costs nothing but prevents the expensive cleanup later.

The second critical error is mixing personal and business finances. Founders pay business expenses from personal accounts, blend personal purchases with business spending, and create accounting chaos. This destroys your audit trail, makes tax season a nightmare, and invites IRS scrutiny. When you mix funds, you lose the ability to track actual business profitability, which means you cannot assess whether your startup actually works. You also lose the liability protection that separates your personal assets from business debts. Open a dedicated business bank account and corporate card on day one. Use them exclusively for business transactions. This single step clarifies your financial picture and protects you legally.

The third mistake is failing to monitor cash flow regularly. Founders obsess over revenue but ignore cash position. You can have strong sales and still run out of cash if customers pay in 60 days while you pay vendors upfront. This timing mismatch destroys startups that do not forecast cash weekly. Build a simple cash flow forecast that projects your bank balance 12 weeks forward. Include all receivables, payables, payroll, and planned expenses. Update it every Friday. This takes 20 minutes but prevents the panic of discovering you are broke with no warning.

Many founders also fail to establish approval procedures early, thinking controls limit speed. The opposite is true. Without written approval thresholds, team members spend money on unnecessary tools, duplicate services, or unauthorized vendor relationships. You discover the waste months later when reconciling. Implement a simple rule immediately: any expense over $500 requires your written approval before payment. This catches waste early and forces conversations about spending that matter. As you hire, document these procedures in writing and assign them to a finance leader.

The cost of postponing controls is exponential. Implement them now while your operation is simple, and they become automatic. Wait until you have 20 employees and a complex expense structure, and introducing controls generates resistance and takes months to enforce. Early implementation of basic controls (bank reconciliation, approval thresholds, segregation of duties) prevents the financial chaos that derails startups. The moment you delay these steps, you accumulate technical debt that becomes harder to fix as your team grows.

Financial controls separate founders who catch problems early from those who face crises unprepared. The three practices we’ve outlined-separating business and personal finances, implementing monthly bank reconciliation, and establishing written approval procedures-form the backbone of startup financial controls that protect your cash and build investor confidence. Start this week by opening a dedicated business bank account, setting up QuickBooks Online or Xero, and documenting your approval threshold in writing.

The cost of postponing these steps compounds monthly. Every month you delay, you accumulate financial debt that becomes harder to fix as your team grows. Founders who establish these practices early scale confidently, while those who wait discover problems too late to prevent serious damage.

We at My CPA Advisory and Accounting Partners help startups build the financial foundation they need to thrive. Whether you need support setting up your chart of accounts, implementing approval procedures, or preparing for investor due diligence, our accounting services and business advisory support guide you from day one. Contact us today to learn how we can help you establish accurate financial reporting and proactive financial management.

Privacy Policy | Terms & Conditions | Powered by Cajabra