Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Running a business with multiple entities, international operations, or industry-specific regulations means your accounting gets complicated fast. Most business owners we work with at My CPA Advisory and Accounting Partners struggle to manage these layers without expert guidance.

The good news: complex accounting solutions don’t have to feel overwhelming. We’ll walk you through the specific challenges you’re facing and show you practical ways to simplify them.

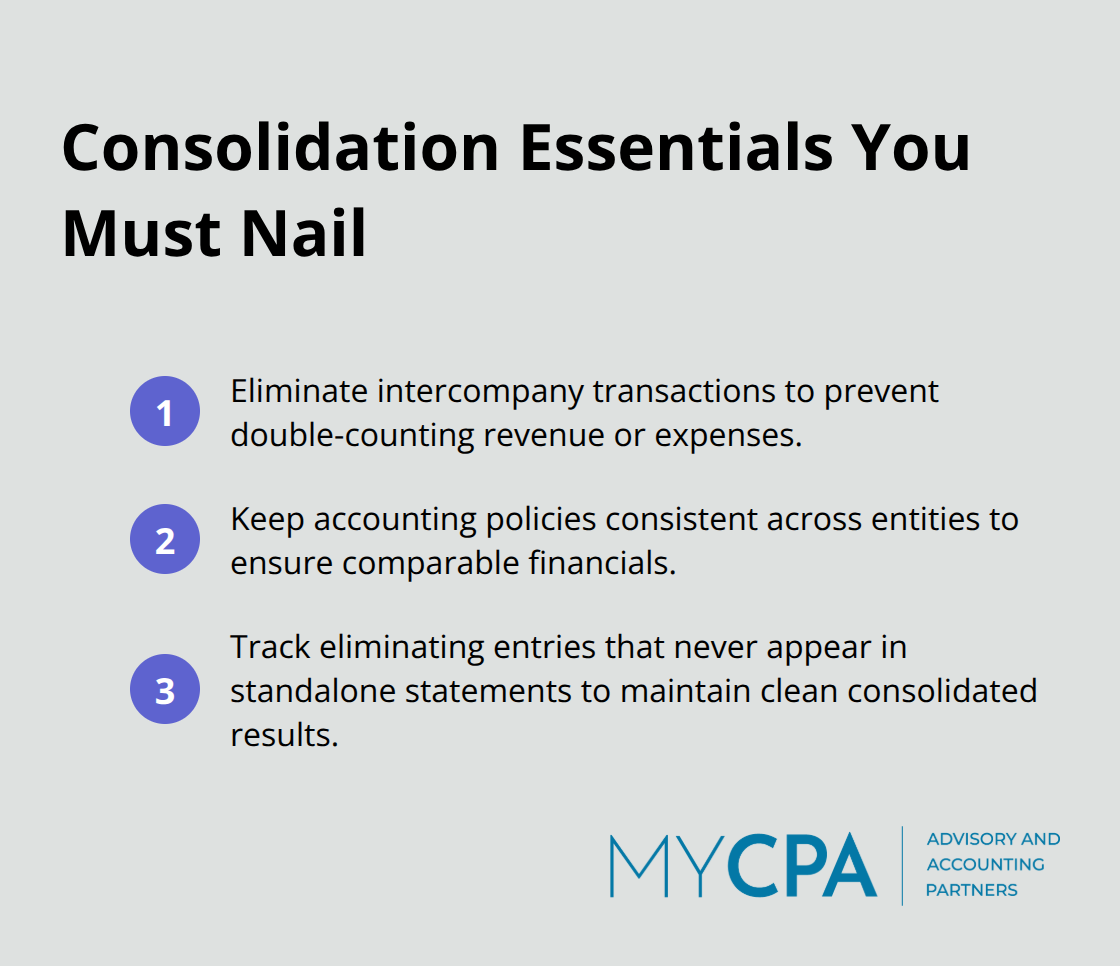

Multi-entity structures create immediate complexity that most business owners underestimate. When you operate through separate legal entities-whether for liability protection, tax efficiency, or operational separation-your accounting cannot treat them independently anymore. Consolidation requires you to eliminate intercompany transactions, maintain consistent accounting policies across entities, and track eliminating entries that do not appear in individual financial statements.

The FASB consolidation standards under ASC 810 demand that you identify the parent entity, assess control over subsidiaries, and properly account for any non-controlling interests. This is not theoretical: one missed intercompany sale or loan can distort your profit margins by thousands of dollars and create audit issues. Many business owners discover consolidation problems only during tax season or when applying for financing. The fix requires detailed documentation of ownership structures, transaction flows between entities, and clear policies on when consolidation applies.

Cross-border operations amplify this challenge significantly. International transactions involve currency fluctuations that hit your bottom line directly-a 5% swing in exchange rates can swing profitability by hundreds of thousands depending on your transaction volume. Revenue recognition across borders demands understanding each jurisdiction’s tax rules, transfer pricing regulations, and local accounting standards. The OECD’s transfer pricing guidelines require that intercompany pricing reflect arm’s-length principles, meaning you cannot set prices arbitrarily between your US and Canadian operations without documentation. Non-compliance triggers penalties that average 20-40% of the adjustment amount according to IRS enforcement data.

Revenue recognition itself has become a minefield under ASC 606. The standard requires you to identify performance obligations, determine transaction prices, and recognize revenue when control of goods or services transfers to the customer. For businesses with complex contracts (think software subscriptions bundled with implementation services or construction projects with milestone payments), this creates constant judgment calls. A SaaS company that bundles setup services with annual subscriptions might recognize revenue over 12 months rather than upfront, directly impacting quarterly results. Companies in healthcare, real estate, and e-commerce face particularly acute revenue recognition challenges because their transaction patterns do not fit standard templates.

Complexity compounds when you try to manage it without specialized systems and expertise. Spreadsheet-based accounting breaks down fast when you consolidate multiple entities, track foreign exchange impacts, and apply different revenue recognition methods simultaneously. You need accounting software that handles multi-entity consolidation, automated currency conversion, and audit trail documentation. More importantly, you need accounting professionals who understand your specific industry’s revenue recognition patterns and regulatory requirements. The difference between getting this right and getting it wrong is not a rounding error-it is the difference between accurate financial statements that support growth and statements that create compliance risk or hide operational problems. Regulatory bodies expect you to demonstrate that your accounting policies align with applicable standards, and they examine this closely during audits or when you file tax returns.

The investment in getting these foundations correct early pays dividends through cleaner audits, better financial visibility, and reduced risk of costly corrections later. Once you understand where your accounting breaks down, the next step is identifying which systems and processes can actually simplify the work instead of adding more layers.

The accounting software you use determines whether your complex financial structure becomes manageable or spirals into chaos. Businesses running multi-entity consolidations, international transactions, and revenue recognition across platforms that were never designed for this complexity face constant friction. Cloud-based ERP systems like NetSuite handle multi-entity consolidation natively, automate currency conversion with real-time exchange rates, and maintain audit trails that satisfy regulatory requirements across jurisdictions. These platforms cost between $10,000 and $50,000 annually depending on modules and user count, but they eliminate the manual work that creates errors in spreadsheet-based systems. The alternative-maintaining separate accounting systems for each entity and manually consolidating results-costs you roughly 15-20 hours monthly in reconciliation work alone. That time adds up to thousands of dollars in labor costs that proper software eliminates immediately.

Your chart of accounts must reflect your actual business structure from the start. If you operate three legal entities but use a single chart of accounts without entity codes, consolidation becomes impossible without a complete restatement. Set up your chart of accounts to tag every transaction by entity, revenue recognition method, and functional currency before your accounting volume grows. This upfront investment takes two weeks but prevents months of cleanup later when auditors identify structural problems. Many businesses discover their chart of accounts was designed for a single entity years ago, and fixing it after the fact means restating prior periods and explaining discrepancies to lenders or investors.

Clear financial policies separate businesses that scale cleanly from those that create compliance headaches. Document exactly when you recognize revenue for each product or service line, how you handle intercompany transactions, what currency conversion methods you use, and how you account for subsidiary acquisitions or disposals. The FASB consolidation standards and ASC 606 revenue recognition requirements are not suggestions-auditors test whether your actual practices match your documented policies. A healthcare provider had one policy for insurance reimbursements and a completely different approach for patient self-pay, creating reconciliation nightmares until standardizing the treatment resolved the issue. Your policies should specify thresholds too: at what dollar amount do you capitalize versus expense items, how frequently do you revalue foreign currency positions, what constitutes an intercompany transaction that requires elimination. Written policies also protect you during staff transitions-when your accounting manager leaves, the next person knows exactly how to handle revenue recognition rather than guessing. Schedule an annual policy review to keep your approaches aligned with regulatory changes and your evolving business model.

Specialized accounting professionals are not a luxury for large corporations-they are essential for any business operating across multiple entities, jurisdictions, or revenue models. A general bookkeeper cannot navigate ASC 606 judgment calls for bundled software contracts or explain why your transfer pricing methodology complies with OECD guidelines. The cost of hiring a specialized CPA or accounting firm runs $5,000 to $20,000 annually for ongoing support, which is trivial compared to the cost of restatements, audit adjustments, or IRS penalties. This type of specialized guidance helps business owners implement accounting structures that scale and withstand regulatory scrutiny.

Once your systems, chart of accounts, and policies align with your actual business complexity, you can move forward with confidence. The next challenge surfaces when your industry itself imposes accounting requirements that go beyond standard consolidation and revenue recognition-healthcare billing, real estate valuations, and multi-channel sales tracking each demand specialized knowledge that transforms how you report financial results.

Healthcare providers face a fundamentally different revenue recognition problem than software companies or real estate investors, yet many attempt to force their operations into generic accounting templates. Healthcare billing operates on a reimbursement model where you cannot simply recognize revenue when you deliver a service-you must track what insurance will pay, what patients will pay out-of-pocket, and what you will write off as bad debt. The Centers for Medicare & Medicaid Services reported that healthcare organizations write off an average of 3-5% of gross revenue annually due to claim denials, contractual adjustments, and patient non-payment. This means a $10 million healthcare practice actually nets $950,000 to $970,000 in collectible revenue, yet most practices record revenue at full billing amounts and adjust downward later.

The accounting problem surfaces immediately: do you recognize revenue at the full billed amount and then record a provision for doubtful accounts, or do you recognize only the amount you expect to collect? ASC 606 requires revenue recognition at the amount you expect to be entitled to receive, which forces healthcare providers to estimate payor-specific reimbursement rates upfront. A physical therapy clinic billing Medicare at 60% of posted rates, commercial insurance at 85%, and self-pay patients at 100% must track these rates separately and apply them to each claim before recognizing revenue. Miss this detail and your financial statements overstate revenue by 15-25% compared to actual cash collections.

Real estate investment property accounting demands equally specialized treatment, but for entirely different reasons. When you own rental properties, the IRS requires you to depreciate the building structure over 27.5 years while tracking land separately (land does not depreciate). The tax code also permits cost segregation studies, which allow you to accelerate depreciation on building components like roofing, HVAC systems, and parking lots over shorter periods of 5, 7, and 15 years. A $2 million property acquisition could generate $80,000 to $120,000 in additional first-year depreciation deductions through cost segregation, directly reducing taxable income. Yet most real estate investors fail to pursue cost segregation studies because they do not understand the mechanics or assume the cost is prohibitive. The study typically costs $3,000-$8,000 and pays for itself in tax savings within one year if you own multiple properties.

Beyond depreciation, real estate accounting requires you to track capital improvements separately from repairs. The IRS distinguishes between replacing a roof (capitalized, depreciated over 27.5 years) versus patching a roof (expensed immediately). Misclassifying $50,000 in capital improvements as repairs overstates current-year income and creates audit risk.

E-commerce and multi-channel sales tracking introduce a different complexity: you cannot recognize revenue the same way across channels with different fulfillment timelines and return policies. Direct-to-consumer sales through your website may have a 30-day return window, while wholesale orders to retailers are final. Marketplace sales through Amazon or Shopify involve the platform holding inventory, reducing your control over goods before the customer receives them. ASC 606 states you recognize revenue when you transfer control of goods to the customer, but control transfers at different points depending on the channel. An e-commerce business selling $5 million annually across direct sales, Amazon, Shopify, and wholesale must track control transfer points separately for each channel.

Failure to implement channel-specific policies creates audit adjustments. One company recognized marketplace revenue incorrectly because it treated Amazon sales identically to direct sales, overstating revenue recognition by two weeks for roughly 40% of annual transactions. The accounting fix required implementing channel-specific revenue recognition policies and reconciling each channel’s timing separately during close.

Each of these industries demands that you stop viewing accounting as a universal process and start treating it as a business function shaped by your operational model. Healthcare requires payor-mix analysis and claim-level revenue tracking. Real estate demands depreciation optimization and capital-versus-repair classification discipline. E-commerce requires channel-specific revenue timing and return provision modeling. Generic accounting software and general bookkeepers cannot navigate these distinctions-you need systems that accommodate industry-specific workflows and professionals who understand the regulatory and tax implications baked into your revenue model. The cost of this specialization is far lower than the cost of overstating revenue, missing tax deductions, or restating financials because your accounting did not match your actual business operations.

Complex accounting solutions require three foundational shifts in how you approach your finances. Stop treating accounting as a back-office function and start viewing it as a strategic tool that shapes what you can see about your business. Multi-entity consolidation, cross-border transactions, and industry-specific revenue recognition are not problems to tolerate-they are opportunities to build financial visibility that drives better decisions.

Invest in systems and expertise that match your actual complexity rather than forcing your business into generic templates. The difference between spreadsheet accounting and cloud-based ERP systems is not convenience-it is the difference between financial statements you can trust and statements that hide operational problems. Specialized accounting guidance pays for itself immediately through tax optimization, audit efficiency, and regulatory compliance.

We at My CPA Advisory and Accounting Partners work with business owners who operate across multiple entities, jurisdictions, and revenue models. Audit your current accounting setup against the complexity you actually operate within, and reach out to discuss how we can help you implement tailored financial services that align your accounting with your business model and build the financial controls that support confident growth.

Privacy Policy | Terms & Conditions | Powered by Cajabra