Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Startups need capital to grow, but the path to funding isn’t one-size-fits-all. We at My CPA Advisory and Accounting Partners know that choosing the right growth funding options can make or break your business trajectory.

This guide walks you through the main financing paths available, from traditional bank loans to venture capital and beyond. You’ll learn what each option costs you and what it demands in return.

Traditional bank loans remain one of the most accessible funding sources for startups with stable revenue and organized finances. Banks evaluate three core factors: how much capital you need for your current stage, whether your business generates predictable profits, and how you manage cash. If you have six to twelve months of operating history showing consistent revenue, you already stand in a stronger position than most early-stage founders. The U.S. Small Business Administration reports that SBA 7(a) loans have a maximum loan amount of $5 million, with technology and healthcare startups among the top recipients. These government-backed loans average around 7.5% interest rates and maintain roughly 28% approval rates for small-business applicants. What makes SBA loans attractive is the partial government guarantee, which reduces lender risk and allows banks to approve businesses that wouldn’t qualify for conventional financing. The application process takes longer than alternative options-typically four to eight weeks-but the payoff comes through favorable terms and repayment periods stretching up to ten years.

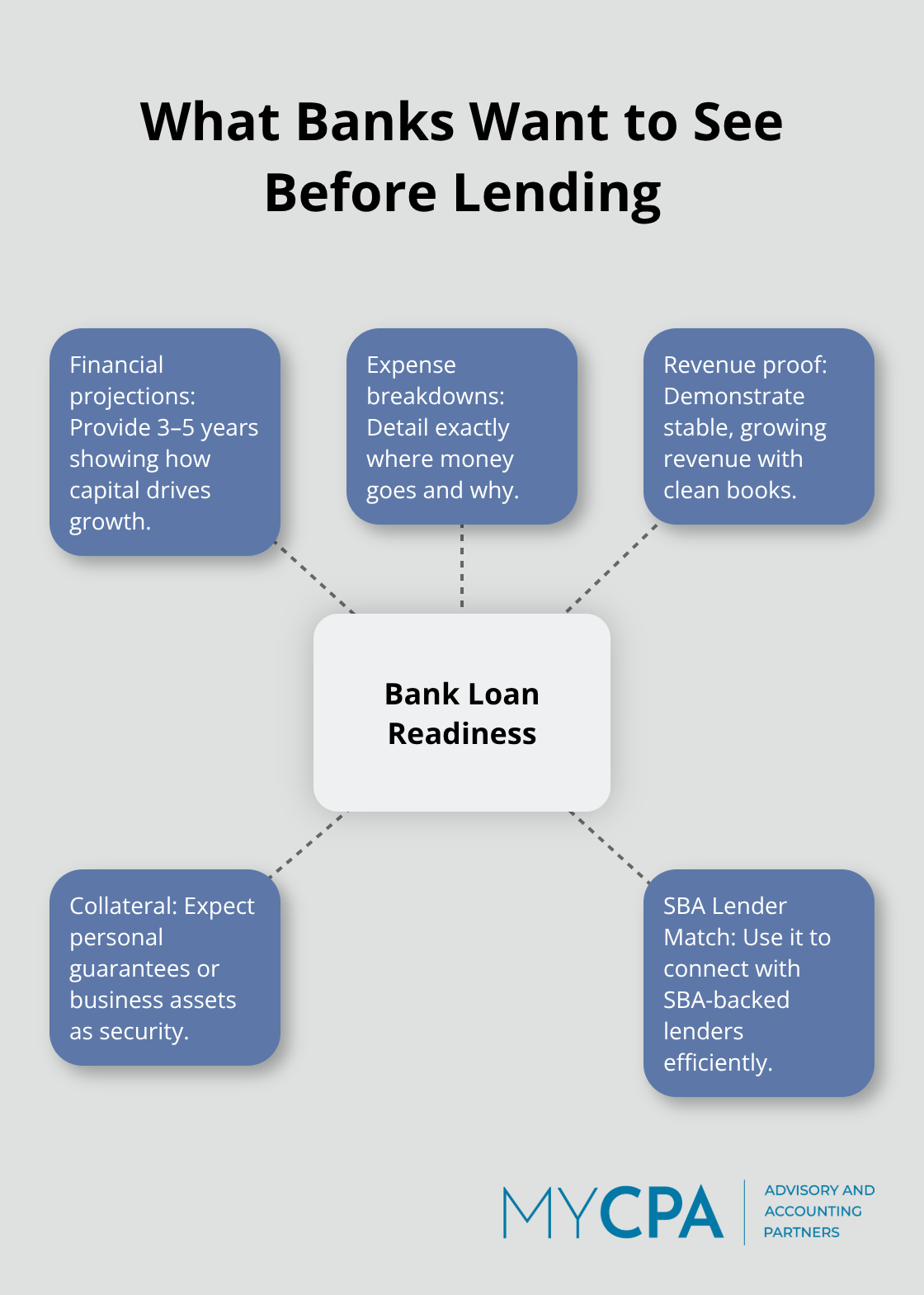

Lenders evaluate startups based on concrete financial evidence, not potential or vision. You’ll need three to five years of financial projections showing how capital directly drives growth, along with detailed expense breakdowns demonstrating you understand where money goes. Banks want proof your revenue is stable and growing, which means clean bookkeeping and accurate records matter enormously. If your books are disorganized, lenders assume your business operations are equally messy. Collateral requirements vary by loan type, but traditional bank loans often require personal guarantees or business assets as security. The SBA’s Lender Match tool helps you connect with banks offering SBA-backed loans, which is far more efficient than cold-calling local branches.

Bank loans preserve your ownership and control-you don’t give away equity or board seats. However, debt creates monthly payment obligations regardless of whether revenue grows or shrinks. For startups with volatile income, this fixed obligation becomes risky. You’re also personally liable if the business defaults, meaning creditors can pursue personal assets. The interest costs add up over time; a $250,000 loan at 7.5% over seven years costs roughly $65,000 in interest alone. This works well for businesses with predictable unit economics and customer contracts, but it’s dangerous for startups still finding product-market fit.

If your startup doesn’t yet qualify for bank loans-or if debt feels too restrictive for your growth stage-alternative funding sources offer different risk profiles and timelines. Venture capital, angel investors, and crowdfunding platforms each provide capital without the monthly payment burden, though they demand different trade-offs in equity and control.

Traditional bank loans won’t work for startups that lack revenue history, operate in high-risk sectors, or want to avoid monthly debt payments. Equity financing and alternative sources offer different paths forward. Venture capital and angel investors provide growth capital without requiring immediate repayment, though they demand equity stakes and often board involvement. CB Insights reports that the highest risk period for startups falls between years two and five, when cash runways deplete and founders must prove sustainable revenue. VC funding solves this runway problem by injecting substantial capital upfront.

Series A rounds typically raise around $9.3 million with valuations between $10 million and $30 million, giving founders breathing room to hire, iterate, and scale. Angel investors operate differently-they’re high-net-worth individuals who invest personal capital, typically seeking 15-25% equity in exchange for their investment plus mentorship and networks. Platforms like AngelList connect startups with angels actively searching for opportunities in specific sectors.

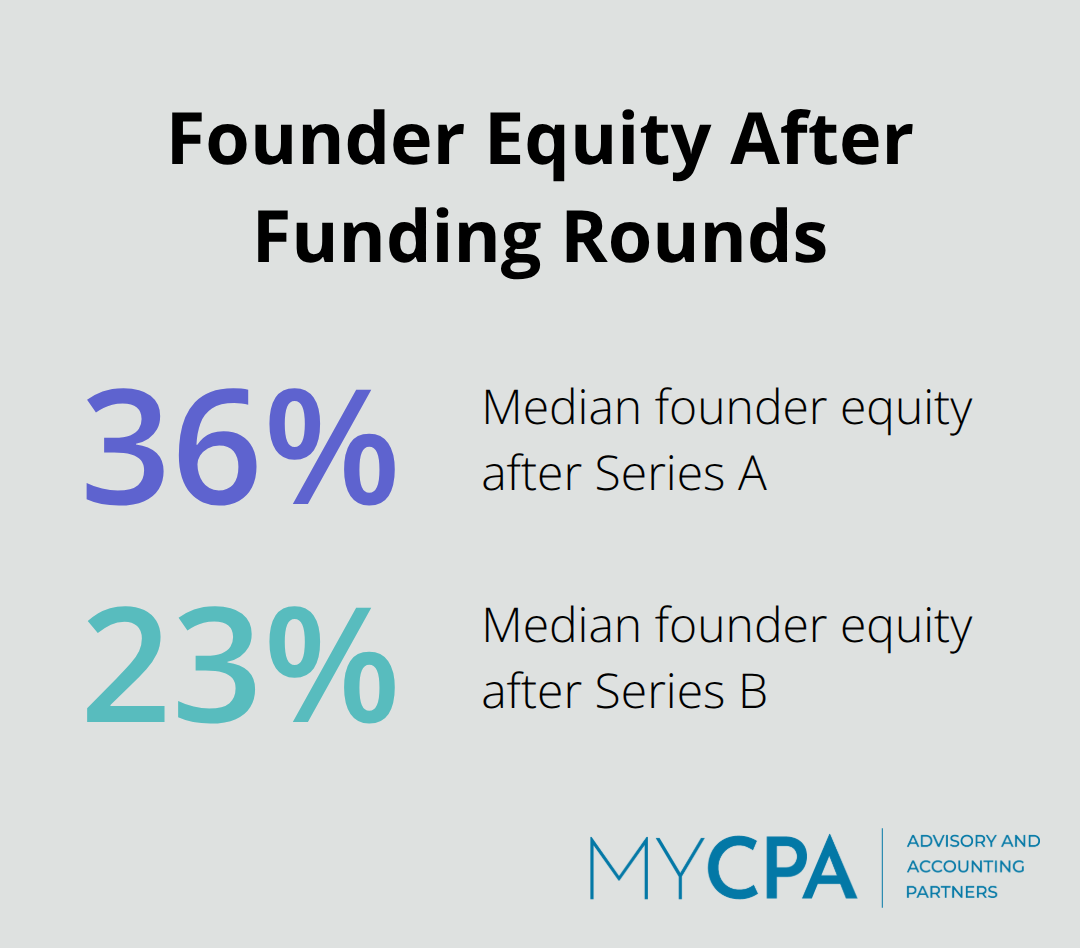

The ownership cost becomes apparent quickly. After Series A, median founder equity drops to roughly 36%. After Series B, it falls to 23%.

This dilution accelerates with each round, meaning early equity decisions carry enormous weight. If you give away 30% to seed investors and another 25% to Series A, you’ve surrendered more than half your company before Series B even closes.

Crowdfunding sidesteps the equity question entirely by raising capital from many small backers who receive perks or products rather than ownership stakes. Platforms like Kickstarter and Indiegogo work exceptionally well for physical products and creative ventures-you keep full control and avoid debt. The catch: you must deliver on promises, and platforms take 5-10% fees.

Government grants and SBA programs like SBIR (Small Business Innovation Research) and STTR (Small Business Technology Transfer) offer non-dilutive capital for R&D-focused startups, though competition is fierce and timelines stretch six to twelve months. Revenue-based financing represents a hybrid approach, tying repayments to monthly income rather than fixed schedules. This flexibility protects cash flow during slow months, but repayment rates typically consume 3-8% of monthly revenue until the cap is reached, making profitability harder to achieve.

Most successful startups combine multiple sources across stages. A founder might bootstrap initially, secure a small grant, then raise angel capital, then pursue an SBA loan once revenue stabilizes, and finally venture capital for aggressive scaling. This staged approach balances risk, preserves equity when possible, and matches capital sources to business maturity. The key lies in understanding which funding type aligns with your current stage and growth ambitions-a decision that requires honest assessment of your business fundamentals and financial position.

Your business stage determines which funding sources actually work. A pre-revenue startup cannot qualify for bank loans, so pursuing SBA financing wastes months of effort. A bootstrapped company generating $50,000 monthly in predictable revenue can access traditional bank loans immediately, making equity dilution unnecessary. Founders often chase the wrong funding path-they pursue venture capital when bank loans fit better, or they take equity when debt would preserve control. The fix starts with honest assessment: how much runway do you have left, what revenue are you currently generating, and how fast do you need to scale? If you have twelve months of operating history with consistent customer contracts, traditional debt financing works. If you’re pre-revenue or in a high-risk sector like deeptech, equity or grants make sense. Lenders care more about how much capital you need for your current stage than how much you think you can qualify for. A Series A company burning $400,000 monthly needs venture capital because no bank will lend that amount without revenue to support it. A service business generating $100,000 monthly can borrow $300,000 via SBA financing at 7.5% interest without touching equity.

Equity looks free until you calculate what it actually costs you. Median founder equity drops to 36% after Series A and 23% after Series B according to venture funding data. That 25% Series A investment might fund eighteen months of growth, but you’ve permanently surrendered a quarter of your company’s future value. If your startup eventually sells for $50 million, that equity stake was worth $12.5 million. Debt costs far less-a $250,000 loan at 7.5% over seven years costs roughly $65,000 in interest, a fraction of what equity dilution extracts. This math heavily favors debt when your business can support monthly payments. Revenue-based financing offers a middle path, tying repayment to monthly income rather than fixed schedules, with lenders collecting between 5% and 15% of monthly revenue until the full repayment cap is reached. The choice between debt and equity hinges on cash flow stability and growth timeline. Startups with volatile revenue cannot handle fixed debt payments, making equity essential. Startups with predictable revenue should exhaust debt options before surrendering equity. One founder secured a $150,000 bank loan at 7.5% instead of raising a $200,000 seed round that would have cost 15% equity-a decision that preserved roughly $7.5 million in future value (assuming a $50 million exit).

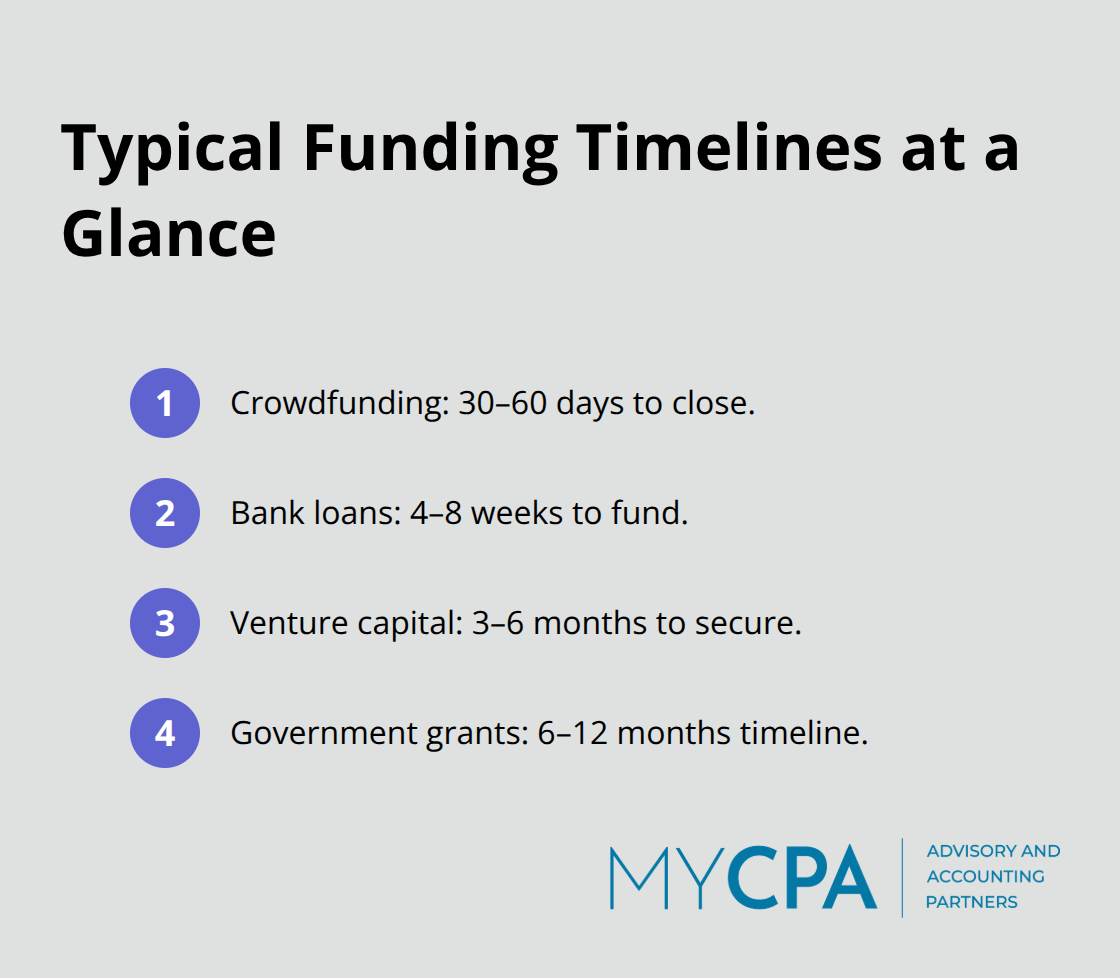

Crowdfunding closes in thirty to sixty days, traditional bank loans take four to eight weeks, venture capital requires three to six months, and government grants stretch six to twelve months. Speed matters when your runway is shrinking, but permanent capital structures matter more.

Equity dilution lasts forever, while debt eventually disappears. A founder desperate for capital in three weeks might crowdfund or tap a credit card at 0% introductory APR, but this creates technical debt that surfaces later. The strategic approach matches timeline to funding type: if you need capital in two weeks, equity or short-term credit cards work; if you have three months, bank loans become viable; if you have six months, SBA loans and venture capital enter the picture. Most successful startups combine sources across stages rather than betting everything on one path. Bootstrap for eight months while building revenue, apply for an SBA loan once you hit $30,000 monthly revenue, then pursue venture capital when you’ve proven unit economics. This staged approach reduces pressure to accept unfavorable terms and preserves optionality. Founders who rush into venture capital before proving product-market fit often regret the dilution when they realize a smaller, debt-backed company would have succeeded.

Calculate exactly how much capital you need for your next twelve months of operations, not how much you hope to raise. Most founders overestimate their funding requirements, which leads them to accept worse terms than necessary. If you need $150,000 to hire two engineers and expand marketing, don’t pursue a $500,000 Series A round that demands 20% equity. A bank loan or revenue-based financing covers your actual need without the dilution. Lenders evaluate startups based on concrete financial evidence, not potential or vision. You’ll need three to five years of financial projections showing how capital directly drives growth, along with detailed expense breakdowns demonstrating you understand where money goes. Banks want proof your revenue is stable and growing, which means clean bookkeeping and accurate records matter enormously. If your books are disorganized, lenders assume your business operations are equally messy.

Collateral requirements vary by loan type, but traditional bank loans often require personal guarantees or business assets as security.

Most successful startups combine multiple sources across stages. A founder might bootstrap initially, secure a small grant, then raise angel capital, then pursue an SBA loan once revenue stabilizes, and finally venture capital for aggressive scaling. This staged approach balances risk, preserves equity when possible, and matches capital sources to business maturity. The key lies in understanding which funding type aligns with your current stage and growth ambitions-a decision that requires honest assessment of your business fundamentals and financial position. Founders who understand their actual capital needs and match them to appropriate funding sources avoid months of wasted effort pursuing the wrong options.

Startup growth funding options require matching your actual business stage, revenue reality, and growth timeline to the right financing vehicle. We at My CPA Advisory and Accounting Partners work with founders constantly who pursued the wrong options, wasting months chasing venture capital when bank loans would have worked, or accepting equity dilution when debt financing fit perfectly. Your decision framework starts with three concrete questions: how much capital do you actually need for the next twelve months, what revenue are you currently generating, and how much equity can you afford to surrender without compromising long-term ownership?

The cost of equity dilution compounds across rounds-after Series A, median founder equity drops to 36%, and after Series B, it falls to 23%. That permanent loss of ownership far exceeds what debt financing costs; a $250,000 loan at 7.5% interest over seven years costs roughly $65,000 in total interest, a fraction of what surrendering 25% equity extracts from your company’s future value. Speed matters, but permanence matters more-crowdfunding closes in thirty to sixty days, bank loans take four to eight weeks, and venture capital requires three to six months, yet equity decisions last forever while debt eventually disappears.

Before committing to any growth funding path, get your financial house in order because clean bookkeeping, accurate projections, and organized expense tracking are what lenders and investors actually evaluate. My CPA Advisory and Accounting Partners specializes in helping founders build the financial clarity that unlocks better funding opportunities through accounting services, tax planning, and business advisory support. The right option depends entirely on where your business stands today.

Privacy Policy | Terms & Conditions | Powered by Cajabra