2026 Tax Planning: Smart Moves for the Year Ahead

Maximize your 2026 tax savings with smart planning strategies. Explore deductions, credits, and moves to reduce your tax bill this year.

Tax laws are shifting in 2026, and waiting until April to figure out your strategy is a mistake. The changes affect your retirement accounts, business structure, investment income, and estate planning.

We at My CPA Advisory and Accounting Partners have put together this guide to help you understand what’s changing and how to respond now. The moves you make today will directly impact your tax bill next year.

The IRS has adjusted tax brackets, standard deductions, and retirement contribution limits for 2026, but the shifts are smaller than you might expect. The standard deduction rises to $32,200 for married couples filing jointly and $16,100 for single filers, according to the IRS. The seven federal tax brackets remain unchanged, with the top rate staying at 37% for incomes over $768,700 for married couples and $640,600 for singles. What matters more than bracket creep is how you position your income around these thresholds.

If you’re self-employed or own a business, the good news is that business deductions remain largely stable. The SALT deduction cap increases to $40,400 for 2026 through 2029, which matters significantly if you live in a high-tax state like California, New York, or New Jersey. This increase makes itemizing more attractive for higher earners, especially when combined with charitable contributions. The phase-out for SALT deductions begins around $500,000 for single filers, so you should work backwards from your total deductible items to determine whether itemizing beats the standard deduction.

The lifetime gift and estate tax exemption jumps to $15,000,000 per individual in 2026. For married couples, that’s $30,000,000 combined. This represents a significant window because these exemptions are set to drop sharply after 2025 unless Congress acts. The annual gift tax exclusion holds steady at $19,000 per recipient per year, which means you can transfer $19,000 to as many people as you want without eating into your lifetime exemption.

If you have substantial assets or want to transfer wealth to your children or grandchildren, 2026 is the year to act. You can gift $19,000 to each child, grandchild, or other family member without any tax consequence. For education or medical expenses paid directly to providers, no limit applies at all. Additionally, if you’re married and haven’t coordinated your gifting strategy with your spouse, you’re leaving money on the table. Each spouse has a separate $15,000,000 exemption, so a couple can transfer up to $30,000,000 during their lifetime without federal estate tax.

The Qualified Charitable Distribution limit increases to $111,000 for 2026 if you’re over 70½ and want to donate directly from your IRA to charity while satisfying required minimum distributions. This approach avoids counting the distribution as taxable income. These changes create multiple pathways to reduce your tax exposure while accomplishing your wealth and legacy goals, which is why the next section focuses on how to maximize retirement contributions and tax-advantaged accounts to amplify these benefits.

The 2026 retirement contribution limits represent your biggest tax-saving opportunity, and most people miss the deadline by waiting. The IRS increased 401(k) and 403(b) contribution limits to $24,500 for 2026, up from $23,500 in 2025. If you’re 50 or older, you can add a catch-up contribution, bringing your total to $32,500. Employees aged 60 to 63 have access to an even higher catch-up of $11,250, allowing a total contribution of $35,750. These contributions reduce your taxable income dollar-for-dollar, which means someone in the 37% tax bracket saves $9,065 in federal taxes alone by maxing out their 401(k).

Traditional IRA contribution limits rose to $7,500 for 2026, with a $1,100 catch-up for those 50 and older. Health Savings Account limits jumped to $4,400 for individual coverage and $8,750 for family coverage, according to the IRS. The HSA stands out as the most tax-efficient account available because contributions are deductible, earnings grow tax-free, and withdrawals for medical expenses face no tax. Most people treat the HSA as a current-year spending account when they should invest it and let it compound for decades.

Starting in 2026, catch-up contributions to employer-sponsored plans must be made with after-tax dollars if you earn more than $150,000. This doesn’t eliminate the benefit, but it means the money goes in as a Roth contribution instead of pre-tax, which matters for your tax planning. The window to contribute for 2026 closes on December 31, 2026, so the time to act is now, not when you file your return in 2027.

Long-term capital gains rates remain fixed at 0%, 15%, and 20% in 2026, but the income thresholds that determine which rate applies to you have expanded. Single filers pay 0% on gains up to $49,450 of taxable income and 15% on gains between $49,450 and $545,500, according to the IRS. Married couples filing jointly get 0% treatment on gains up to $98,900. This means if you’re in the 15% bracket, you have room to harvest gains strategically without jumping to the 20% rate.

The Net Investment Income Tax applies to higher earners and triggers on investment income when modified adjusted gross income exceeds $200,000 for singles or $250,000 for joint filers. This isn’t a capital gains tax; it’s a separate tax on investment income, so your total federal rate on long-term gains could reach 23.8% at the top bracket. Tax-loss harvesting becomes essential for offsetting these gains. If you sold a winning stock earlier in the year, identify underperforming positions in your portfolio and sell them to lock in losses that offset the gains. These losses carry forward indefinitely if they exceed your annual gains.

The mistake most people make is holding onto losers for psychological reasons or refusing to sell winners because they think the market will keep rising. Sell winners strategically within your tax bracket thresholds and use losses to offset the gains. Appreciated securities also work for charitable giving: if you donate stock instead of cash, you avoid capital gains tax on the appreciation and still claim the charitable deduction at fair market value. Someone donating a stock worth $10,000 that they bought for $3,000 saves $1,050 in capital gains taxes (at the 15% rate) while claiming a $10,000 charitable deduction.

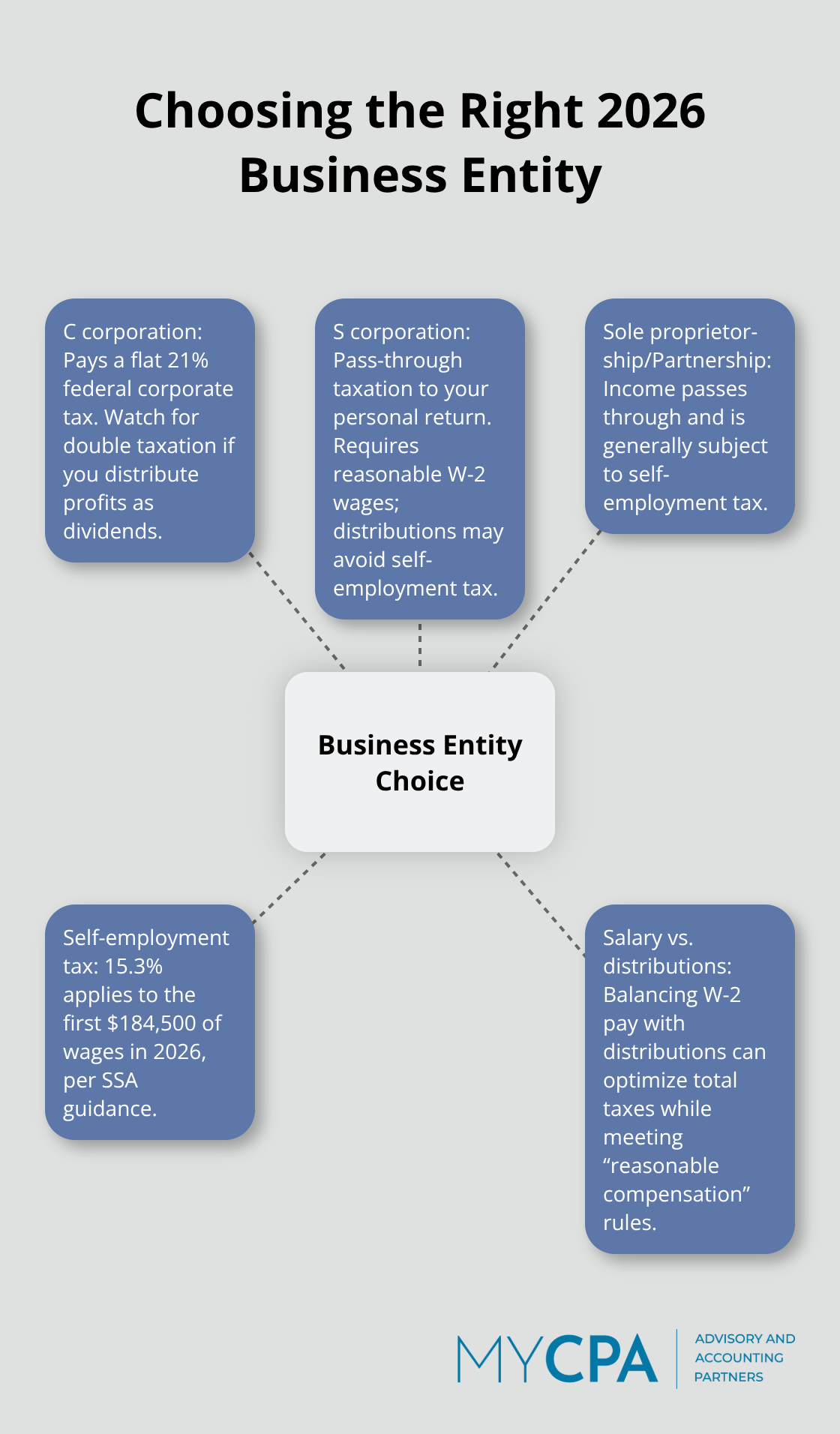

Your choice of business entity determines whether you pay corporate tax, self-employment tax, or both. C corporations pay a flat 21% federal corporate tax rate, while S corporations, sole proprietorships, and partnerships are pass-through entities where income flows to your personal return at your individual rate. If your business generates $100,000 in profit and you’re in the 24% tax bracket, a C corporation saves you money by paying 21% tax at the corporate level, but only if you don’t take all the profits out as salary.

The problem is dividends are taxed twice: once at the corporate level and again at your personal level when distributed. An S corporation avoids double taxation because profits pass through to your return, but you must pay yourself reasonable wages and pay self-employment tax on those wages. The self-employment tax is 15.3% on the first $184,500 of wages for 2026, according to the Social Security Administration.

If you own a service business generating $150,000 in profit, you can reduce self-employment tax by splitting income between a reasonable salary and S corporation distributions. Pay yourself $90,000 in W-2 wages and take $60,000 as a distribution. You pay self-employment tax on the $90,000 but not the $60,000, saving roughly $7,650 in taxes. The IRS scrutinizes S corporations that underpay wages, so your reasonable wage must reflect what similar roles earn in your industry. This decision should be finalized by March 15, 2026, for most entities, since entity elections have firm deadlines. If you’re currently operating as a sole proprietor or partnership and generating substantial income, converting to an S corporation or evaluating a C corporation structure could reduce your tax burden significantly. A professional review of your current structure against these 2026 thresholds will reveal whether a change makes financial sense for your situation.

Most business owners and high-income earners leave money on the table because they treat tax planning as a task for March or April rather than an ongoing process throughout the year. The moment you wait until tax season arrives, you’ve already lost access to the most powerful deductions and strategies available. If you own a business that generates $200,000 in profit and discover in April that you could have converted to an S corporation to save $15,000 in self-employment taxes, that window has closed. Entity elections must be filed by March 15, 2026, for most businesses, according to the IRS. You cannot retroactively elect S corporation status and claim the tax savings on your 2026 return. The same applies to retirement contributions. If you earn $150,000 and fail to contribute to a 401(k) until you file your return in 2027, you’ve already missed the deadline to contribute for 2026.

The money sits in your checking account earning nothing while you pay an extra $5,550 in federal taxes at the 37% marginal rate. Your business structure determines whether you pay corporate tax, self-employment tax, or both, and this decision locks in your tax rate for the entire year. C corporations pay a flat 21% federal corporate tax rate, while S corporations, sole proprietorships, and partnerships are pass-through entities where income flows to your personal return at your individual rate. If your business generates $100,000 in profit and you’re in the 24% tax bracket, a C corporation saves you money by paying 21% tax at the corporate level. An S corporation avoids double taxation because profits pass through to your return, but you must pay yourself reasonable wages and pay self-employment tax on those wages. The self-employment tax is 15.3% on the first $184,500 of wages for 2026, according to the Social Security Administration. If you own a service business that generates $150,000 in profit, you can reduce self-employment tax by splitting income between a reasonable salary and S corporation distributions. Pay yourself $90,000 in W-2 wages and take $60,000 as a distribution. You pay self-employment tax on the $90,000 but not the $60,000, saving roughly $7,650 in taxes. The IRS scrutinizes S corporations that underpay wages, so your reasonable wage must reflect what similar roles earn in your industry. This decision must be finalized by March 15, 2026, for most entities, since entity elections have firm deadlines. If you currently operate as a sole proprietor or partnership and generate substantial income, converting to an S corporation or evaluating a C corporation structure could reduce your tax burden significantly.

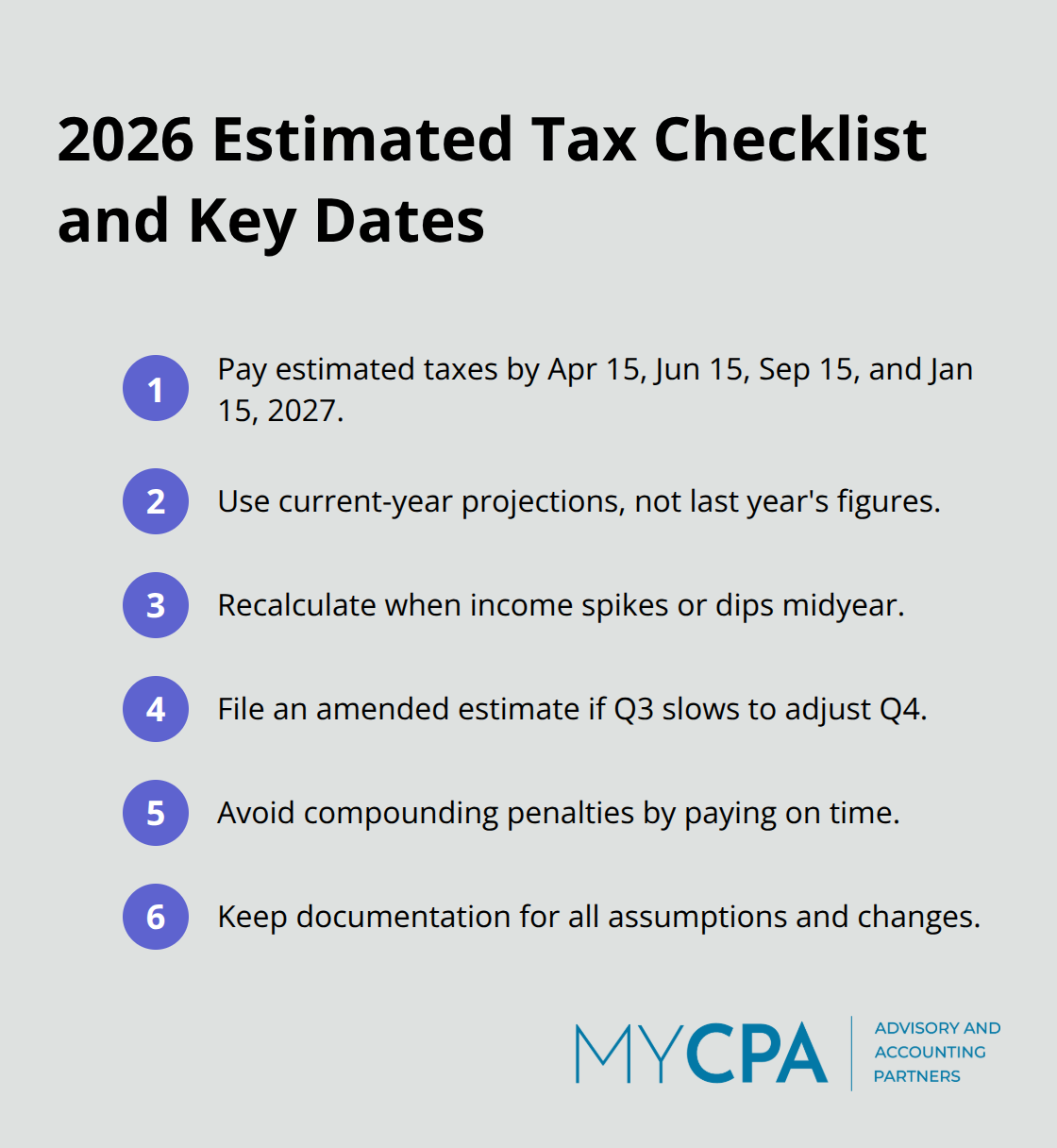

Self-employed individuals and business owners must pay estimated taxes quarterly or face penalties and interest. The IRS charges penalties even if you end up with a refund when you file, so the quarterly payment is not optional. For 2026, if you expect to owe more than $1,000 in federal income tax that will not be covered by withholding, you must make quarterly estimated tax payments on April 15, June 15, September 15, and January 15, 2027. Most people calculate estimated taxes based on the previous year’s return, but that approach fails when your income changes significantly. If your business grew 50% in 2025 and you paid estimated taxes based on 2024 income, you’ll face a substantial underpayment penalty in 2026. The penalty rate compounds quarterly, so delaying payments makes the problem worse.

A better approach involves calculating estimated taxes based on your current year’s projected income and adjusting them if circumstances change midyear. If your business slows in the third quarter, file an amended estimated tax payment and reduce the fourth quarter payment. This keeps you compliant and avoids overpaying.

A promotion, bonus, business sale, or inheritance changes your tax situation fundamentally, yet most people ignore these events until tax time. If you received a $100,000 inheritance in July 2026, that timing affects whether you should contribute more to a 401(k) or Roth IRA before year-end. Roth IRA contribution limits phase out at $242,000 to $252,000 for married couples filing jointly, according to the IRS. An inheritance that pushes your income into that range eliminates your ability to contribute directly to a Roth. Similarly, if you sold a piece of real estate and realized a $150,000 capital gain, you should immediately assess whether you can offset that gain with tax-loss harvesting or charitable contributions of appreciated securities. Waiting until April means you’ve already paid 23.8% in federal tax on that gain. A divorce, death in the family, or change in filing status also triggers different tax brackets and deductions. If you remarry mid-year, your filing status changes and your tax brackets shift. These events require immediate action, not April reflection.

The 2026 tax landscape rewards action over procrastination. The higher standard deductions, expanded retirement contribution limits, increased estate tax exemptions, and strategic capital gains brackets create genuine opportunities to reduce your tax burden, but only if you move now. Waiting until April 2027 to address these changes means you’ve already forfeited thousands in potential savings, since entity elections close on March 15 and retirement contributions lock in on December 31.

Your 2026 tax planning success depends on understanding which changes apply to your situation, making structural decisions before deadlines pass, and staying responsive when your income or circumstances shift. The standard deduction increase matters less than positioning your income strategically around the capital gains brackets and retirement contribution thresholds. The $15 million estate tax exemption proves powerful only if you coordinate gifting with your spouse and execute transfers before the exemption drops.

We at My CPA Advisory and Accounting Partners help business owners and high-income earners navigate these decisions with precision. Schedule a planning session before the end of January 2026, and bring your 2025 tax return, current business financials, and any major changes you anticipate for the year ahead. Contact our team to lock in your 2026 tax strategy while the year is still young.

Privacy Policy | Terms & Conditions | Powered by Cajabra