Maximize Allowable Deductions Without Red Flags

Maximize allowable deductions while staying audit-safe. Learn legitimate strategies to reduce your tax burden without triggering IRS scrutiny.

Operating across multiple states means managing state tax registrations in different jurisdictions-and getting it wrong costs time and money. At My CPA Advisory and Accounting Partners, we’ve seen businesses face penalties simply because they missed a registration deadline or didn’t understand when they triggered a tax obligation.

This guide walks you through the registration requirements, compliance strategies, and tools that keep your business on the right side of state tax law.

Sales tax registration applies when you sell tangible personal property or taxable services in a state. You trigger this obligation the moment you create economic nexus-meaning you have sufficient sales volume in that jurisdiction. Texas requires businesses selling or leasing tangible personal property or taxable services to complete the Texas Online Tax Registration Application, with processing taking 2–3 weeks through the eSystems portal. The permit covers Sales and Use Tax, the 911 Surcharge and Fees, and the Sales Tax Surcharge on Diesel Equipment. Texas permits print the next business day after approval and arrive within 7–10 business days, but this timeline assumes you submit correct documentation including your NAICS code, which classifies your business activities for tax purposes.

Income tax registration becomes mandatory when you have employees in a state or when you’re a resident earning out-of-state income. However, nine states impose no state income tax: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. Payroll tax registration is separate and applies whenever you have employees in a state. You’ll need to register in each state where you have employees and follow each state’s rules for withholding, unemployment tax, and reporting. The default rule across most states is that withholding follows the work state, meaning where services are actually performed, not necessarily where your company is based or where the employee lives.

Multi-state compliance becomes complex because each state defines residency, nexus, and withholding thresholds differently. Some states use a convenience-of-the-employer test, meaning if an employee works remotely for your company’s convenience rather than necessity, you may owe withholding in that employee’s home state-Connecticut, Delaware, Nebraska, New Jersey, and Pennsylvania apply this rule. New York nonresidents can apportion income based on days worked inside versus outside the state, but you’ll need documentation proving outside work was necessary, not optional. Reciprocal agreements between states simplify this: if two states have reciprocity, you typically withhold only for the employee’s state of residence. Without reciprocity, you may owe withholding in both the work state and the residence state. Many states enforce threshold requirements before withholding kicks in-some require withholding only after a certain number of days worked or wage amount is reached.

Missing a registration deadline carries real penalties. South Carolina businesses registering through MyDORWAY can process applications in up to 5 business days, but delays compound when you register late. North Carolina charges no fee for sales tax registration, but the state warns that private third-party websites often charge fees for inaccurate registrations, so register directly through official channels. Each state maintains its own timeline and requirements, which means you need a system to track when obligations arise in each jurisdiction where you operate.

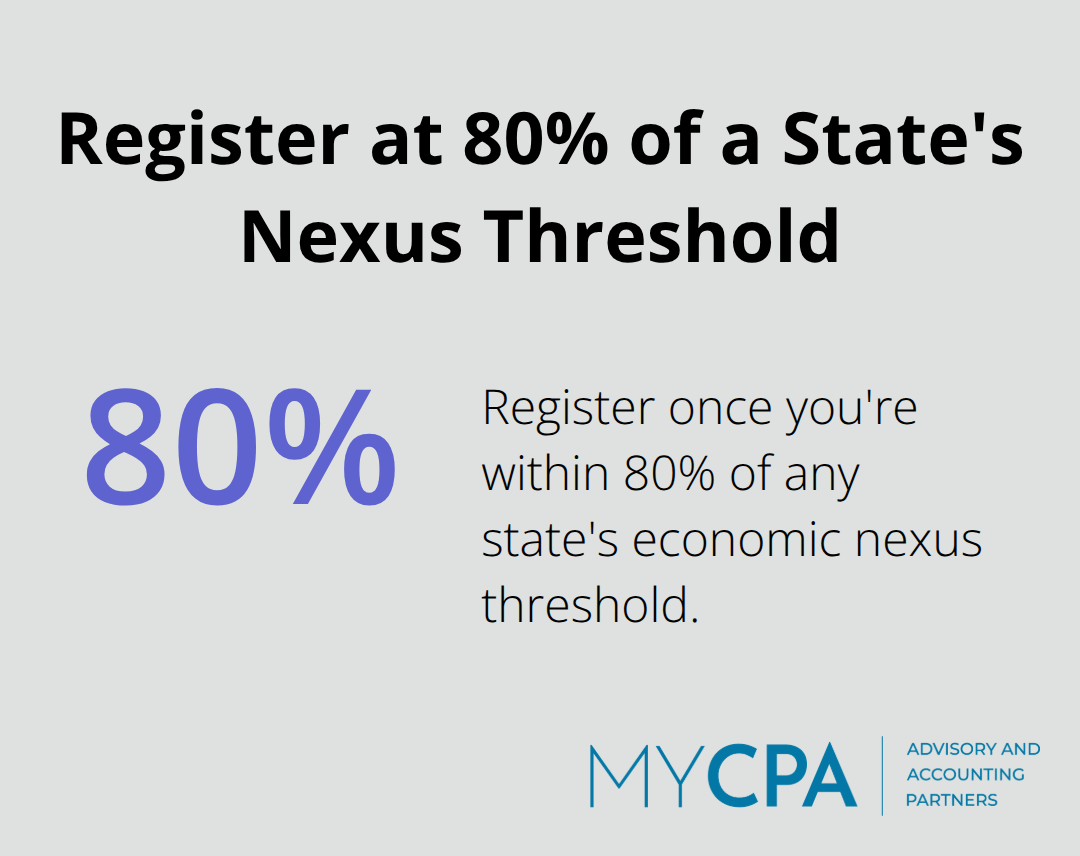

Sales tax nexus determines whether you owe registration in a state, and most businesses misunderstand when this obligation actually begins. Economic nexus-the sales volume threshold that creates a tax obligation-varies significantly by state. South Dakota set the precedent in 2018, and now most states follow similar thresholds: typically $100,000 in annual sales or 200 transactions within a 12-month period trigger registration. However, some states operate differently. Vermont requires registration at just $10,000 in sales, while other states use different transaction counts or time windows. The moment you cross that threshold in any state, you’ve triggered a registration obligation that applies retroactively in many jurisdictions. This means if you hit $100,000 in sales in November but don’t register until January, you owe back taxes and penalties dating to when you first exceeded the threshold.

Track your sales by state monthly-not quarterly or annually-to catch when you’re approaching these thresholds. Many business owners discover too late that they’ve operated without proper registration for months, resulting in significant back-tax bills plus interest and penalties.

The practical move is to establish a quarterly review of sales by state and register proactively once you’re within 80 percent of any state’s threshold. Don’t wait until you’ve crossed it.

Income tax withholding for remote workers and distributed teams operates on entirely different logic than sales tax. The default rule is straightforward: withhold income tax in the state where work is actually performed, not where your employee lives or where your company is headquartered. This creates real complications when employees work across state lines. If an employee works three days in your home state and two days in another state each week, you owe withholding in both states-unless those states have a reciprocal agreement, which reduces withholding to the employee’s residence state only.

Reciprocal agreements exist between certain state pairs, primarily in the Northeast and Midwest regions, so check whether your employee’s work state and residence state have reciprocity before calculating withholding. Many states also enforce thresholds: you may not owe withholding in a state until an employee works a minimum number of days there or earns above a specific amount.

Connecticut, Delaware, Nebraska, New Jersey, and Pennsylvania use a convenience-of-the-employer test, meaning if an employee works remotely for your operational convenience rather than necessity, you owe withholding in their home state even if they rarely visit your office. New York nonresidents can apportion income based on actual days worked in-state versus out-of-state, but you’ll need documentation proving outside work was necessary. This distinction matters significantly when you structure remote work arrangements.

Map each employee’s work location and residency, identify reciprocity rules, and document the business reason for remote work arrangements. Configure your payroll system to withhold correctly in each state-payroll software mistakes here are expensive and create compliance nightmares that take months to unwind with state tax authorities. The complexity of multi-state withholding demands attention to detail and systematic tracking of where your team actually works.

Most businesses fail at multi-state tax compliance not because they misunderstand the rules, but because they lack a system to track what’s due and when. We at My CPA Advisory and Accounting Partners see this repeatedly: companies register in one state, miss deadlines in another, and discover the problem only when they receive a penalty notice. The solution isn’t complex, but it requires discipline.

Start by creating a master spreadsheet that lists every state where you have sales tax nexus, employees, or income tax obligations. Include the registration deadline for each state, the renewal date, the responsible person’s name, and the login credentials for each state’s tax portal. Update this document quarterly as your business expands into new states or as you hire employees in different locations. Set calendar reminders 30 days before each deadline-not the day of. Most states process registrations within 2–3 weeks, so submitting 30 days early gives you a buffer if the state requests additional documentation or if you discover missing information.

Texas requires a NAICS code that classifies your business activities, and if you submit the wrong code, the eSystems portal will reject your application, costing you weeks. South Carolina’s MyDORWAY system processes applications in up to 5 business days, but only if you provide all required documents upfront. North Carolina charges no registration fee, but the state explicitly warns that third-party websites charge fees for inaccurate registrations that create compliance headaches later. Register directly through official state portals every time.

Your payroll system must sync with this registration calendar. If you hire an employee in a new state, that hire triggers a payroll tax registration obligation in that state-often within days. Many employers don’t register until their first payroll runs, which means they’re already delinquent. Document the hire date, the state where work will occur, and the date you submitted the payroll tax registration application. This coordination prevents costly oversights that compound quickly.

Coordinate with a tax professional or accountant who understands multi-state compliance. They catch registration gaps you might miss and help you navigate reciprocity agreements, convenience-of-the-employer tests, and state-specific thresholds. A qualified professional saves you time and protects your business from penalties that accumulate fast.

Technology simplifies multi-state compliance significantly. Payroll software like ADP or Guidepoint flags when new employees trigger registration obligations in different states. Tax compliance platforms like Thomson Reuters ONESOURCE or Vertex monitor your sales by state and alert you when you approach economic nexus thresholds. These tools cost money, but they’re far cheaper than penalties, back taxes, and the time spent untangling non-compliance with state tax authorities. Small businesses operating in fewer than five states can manage with spreadsheets and calendar reminders, but once you exceed that threshold, automation becomes necessary.

State tax registrations across multiple jurisdictions demand attention, but the payoff justifies the effort. You protect your business from penalties that accumulate quickly and from the operational disruption that comes with state tax audits. The businesses we at My CPA Advisory and Accounting Partners work with consistently report that proactive registration and systematic tracking eliminate compliance surprises.

Your immediate action is to audit your current registrations in every state where you operate. List each state where you have sales, employees, or income tax obligations, then verify that your registrations remain current and that your payroll system reflects the correct withholding rules for each employee’s work location. If reciprocity agreements, convenience-of-the-employer tests, or state-specific thresholds create confusion, professional guidance matters significantly.

My CPA Advisory and Accounting Partners provides tax services and business advisory expertise designed to simplify multi-state compliance and protect your financial health. The investment in professional support pays for itself the first time it prevents a penalty or catches a registration gap before a state does.

Privacy Policy | Terms & Conditions | Powered by Cajabra