Maximize Allowable Deductions Without Red Flags

Maximize allowable deductions while staying audit-safe. Learn legitimate strategies to reduce your tax burden without triggering IRS scrutiny.

Most business owners don’t realize their cash flow reporting is the difference between survival and failure. We at My CPA Advisory and Accounting Partners have seen too many companies collapse not because they were unprofitable, but because they ran out of cash.

The good news: cash flow visibility is completely within your control. This guide shows you exactly how to turn your cash data into decisions that protect your business.

Cash flow problems kill businesses faster than unprofitability ever could. A company with strong profits can still collapse if it runs out of cash to pay employees, suppliers, or debt obligations. According to research from the U.S. Small Business Administration, cash flow shortages rank among the top reasons businesses fail, yet many owners overlook cash reporting until it’s too late. The difference between survival and growth comes down to one thing: knowing where your cash actually is and where it’s going.

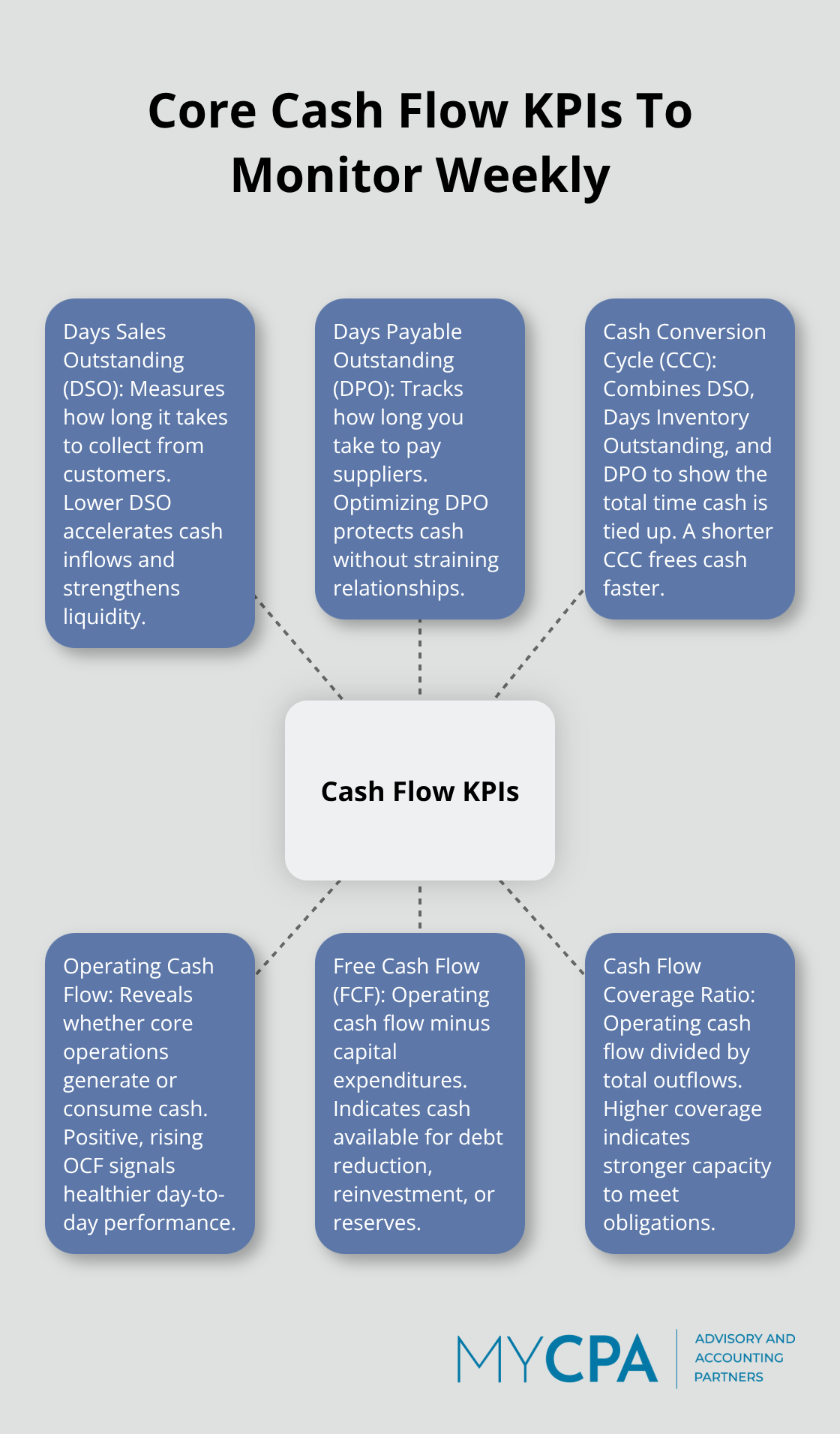

Without proper cash flow reporting, you’re essentially running your business in the dark. You might see positive net income on your income statement while your bank account drains because customers haven’t paid invoices yet or you’ve invested heavily in inventory. This disconnect between profit and cash is where most owners get blindsided. The indirect method of calculating operating cash flow, which starts with net income and adjusts for non-cash items like depreciation and changes in working capital, reveals this gap clearly. When you track Days Sales Outstanding (DSO), you gain specific visibility into a major cash drain. If your DSO climbs above 45 days, you hold cash that should be in your bank account. Similarly, Days Payable Outstanding (DPO) shows how long you take to pay suppliers-stretching this too far damages relationships, but optimizing it around 30 days protects your liquidity without burning bridges. Operating cash flow, calculated as net income plus non-cash expenses minus increases in working capital, tells you whether your core operations actually generate cash or consume it.

Real-time cash flow visibility transforms decision-making from reactive to proactive. Monthly reporting leaves you a month behind reality; weekly or rolling 13-week cash flow forecasts let you spot problems before they become crises. When you know your Cash Conversion Cycle-the total time from paying for inventory to collecting cash from sales-you can pinpoint exactly where bottlenecks exist. A shorter cycle means faster liquidity recovery. Free Cash Flow (FCF), calculated as operating cash flow minus capital expenditures, shows you exactly how much cash remains after sustaining your business, which is what you can actually use for debt reduction, reinvestment, or contingencies.

Dashboards that couple cash flow KPIs with operational metrics provide a holistic view that static reports simply cannot match. The moment you implement real-time reporting, your ability to negotiate better payment terms, adjust customer credit policies, or optimize supplier arrangements improves dramatically because you have current data, not historical guesses.

Many business owners treat their income statement as the primary measure of health, but profit and cash flow tell completely different stories. A sale on credit increases profit immediately but doesn’t put cash in your bank account. You might report strong earnings while your working capital ties up thousands in unpaid invoices and excess inventory. This timing mismatch creates the illusion of success when your actual liquidity position is deteriorating. The Cash Flow Coverage Ratio-operating cash flow divided by total cash outflows (debt service, capital expenditures, and dividends)-reveals whether your operations actually support your obligations. A higher ratio signals stronger financial health and creditworthiness to lenders and investors. Without this visibility, you make decisions based on incomplete information, which leads to missed opportunities and preventable crises.

Cash flow data only matters if you act on it. Dashboards and integrated reporting platforms transform raw numbers into signals that trigger decisions. When your DSO rises, you know to tighten credit terms or accelerate collections. When your Cash Conversion Cycle lengthens, you identify whether inventory moves too slowly or suppliers demand faster payment. When your Free Cash Flow shrinks, you adjust capital spending or negotiate better terms before cash runs dry. This shift from passive observation to active management is where cash flow reporting delivers real value. The businesses that thrive are the ones that monitor these metrics weekly, not yearly, and respond to trends before they become emergencies.

Your next step involves understanding exactly what components make up an effective cash flow report and how to structure them so they actually guide your decisions.

Your cash flow statement breaks into three distinct sections, and each one tells a different part of your financial story. Operating activities show the cash your core business generates-this is where you see whether your day-to-day operations actually produce cash or consume it. When you calculate operating cash flow using the indirect method, you start with net income and adjust for non-cash items like depreciation, then account for changes in working capital such as increases in accounts receivable or inventory. If your operating cash flow is positive and trending upward, your business generates real cash from selling products or services. If it’s negative or stagnant while net income looks healthy, you have a working capital problem that demands immediate attention.

Investing activities capture cash spent on long-term assets like equipment, real estate, or technology systems, as well as proceeds from selling those assets. Capital expenditures reduce your available cash, which is why Free Cash Flow-operating cash flow minus capital expenditures-matters far more than operating cash flow alone. A business might generate $100,000 in operating cash flow but spend $120,000 on new equipment, leaving negative free cash flow and forcing you to borrow or deplete reserves. Financing activities reveal cash from loans, equity investments, and dividend payments, showing how you’re funding operations and returning cash to owners. This section exposes whether you’re becoming more or less dependent on debt.

Most business owners focus only on whether money came in or went out, but effective reporting requires tracking where money moved within each section and why. Days Sales Outstanding directly impacts your operating cash flow because it measures how long customer payments sit as receivables instead of bank deposits; if your DSO averages 50 days but your industry standard is 30 days, you’re holding $50,000 in cash unnecessarily for every $1 million in annual sales. Similarly, Days Inventory Outstanding shows how long products sit in inventory before sale, and Days Payable Outstanding reveals how long you stretch supplier payments.

Your Cash Conversion Cycle combines these three metrics and tells you exactly how many days pass between spending cash on inventory and receiving cash from customers. This metric transforms abstract numbers into concrete operational reality.

Seasonal patterns create the most dangerous blind spot in cash flow management. Retail businesses see cash surge in November and December but drain in January through September. Construction companies invoice millions but wait 60 days for payment while payroll runs weekly. Manufacturing businesses tie cash in inventory for months before converting it to sales. Without identifying these patterns, you’ll either maintain excessive cash reserves during slow periods or face crises during peaks.

Track your actual cash position week by week for 24 months and plot it on a chart; you’ll immediately see where seasonal pressure hits hardest and can plan credit lines or payment schedules accordingly. This forward-looking approach transforms seasonal volatility from a threat into a manageable variable. Once you understand these three sections and the metrics that drive them, you’re ready to implement strategies that actually move the needle on your cash position.

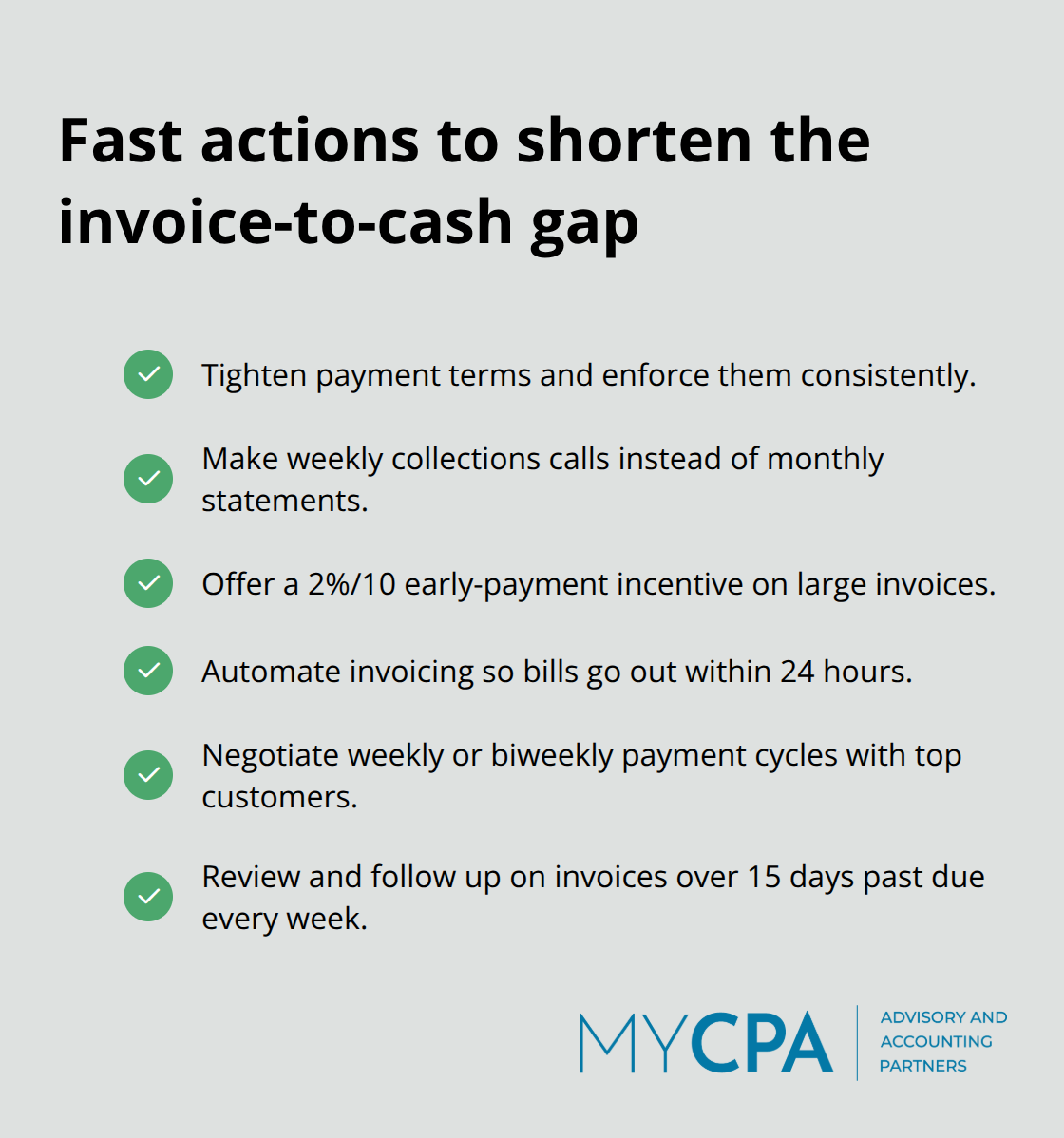

The gap between when you invoice customers and when cash hits your bank account is where most businesses hemorrhage liquidity. Owners who generate strong sales often struggle with cash because they never tightened their collection process. If your Days Sales Outstanding sits above 45 days, you’re essentially giving customers an interest-free loan while your own bills come due. Start by auditing your current DSO against industry benchmarks-retail typically runs 7 days, manufacturing around 60 days, and B2B services often stretch to 45 days or higher. The moment you know your actual DSO, you have a target to beat.

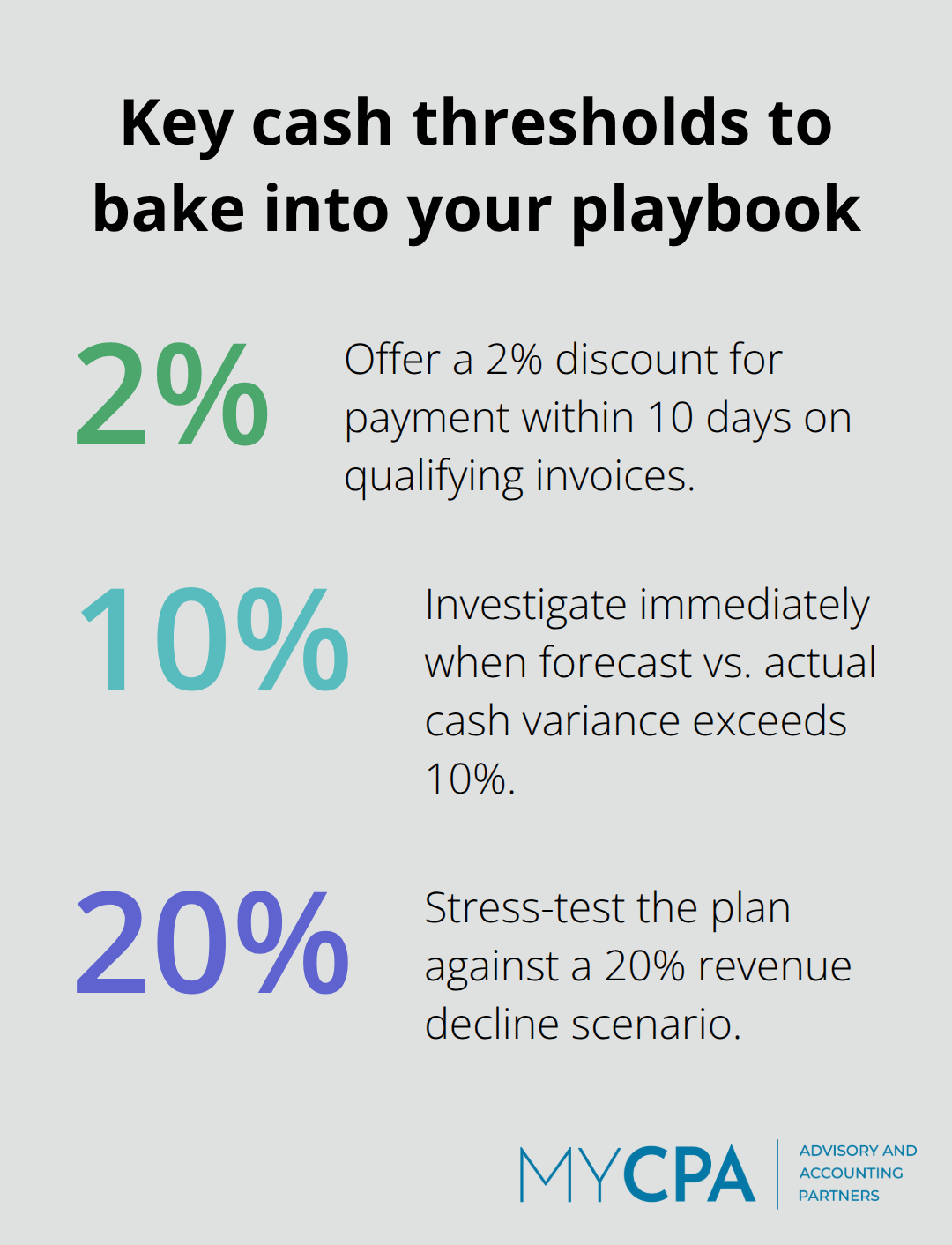

Tighten your payment terms in writing for every new customer and enforce them consistently; customers who know you’ll chase unpaid invoices pay faster than those who don’t. Implement weekly collections calls instead of monthly statements-the difference in conversion time is dramatic. Offer a 2 percent discount for payment within 10 days on invoices over $5,000; the cost of that discount is far less than the cost of carrying receivables for 60 days. Automate your invoicing so customers receive bills within 24 hours of delivery, not a week later.

For your largest customers, negotiate weekly or biweekly payment cycles instead of net 30 or net 60. This single change compresses your cash conversion cycle significantly. Monitor which invoices age past your terms weekly, not monthly, and follow up personally on anything over 15 days past due. Your cash conversion cycle shrinks the moment collections become a priority, not an afterthought.

Your Days Payable Outstanding matters equally because stretching supplier terms without damaging relationships improves short-term cash. Try 30 days as your baseline and negotiate longer terms only with suppliers who can absorb it-never sacrifice relationships for marginal cash gains. Suppliers who trust you’ll pay on time offer better pricing and priority service during shortages, which creates far more value than delaying payment by 15 days.

Contact your top five suppliers and ask what payment terms they offer for consistent, on-time payment. Many suppliers reward reliability with discounts or extended terms that you never knew existed. For smaller suppliers, paying in 20 days instead of 30 might earn you a 1 to 2 percent discount that compounds throughout the year. The key is negotiating from a position of strength-when you pay reliably, you have leverage to ask for better terms.

Your cash reserves function as a shock absorber for seasonal swings, unexpected expenses, and market downturns, yet most owners carry too little or miscalculate how much they actually need. Calculate your weekly cash burn by dividing total monthly operating expenses by 4.3 weeks, then multiply by the number of weeks you want to survive without revenue. If your monthly expenses run $50,000, your weekly burn is roughly $11,600; maintaining 13 weeks of reserves means holding $150,800 minimum. This isn’t excessive-it’s survival insurance.

Run your actual cash position backward 24 months and identify the lowest point you hit; that’s your minimum threshold. Establish a secondary line of credit now, before you need it, because lenders won’t extend credit during crisis. Many owners carry credit lines they hope never to use, but that backstop prevents forced decisions during tight periods. Build a simple monthly variance report comparing forecasted cash to actual cash; when variance exceeds 10 percent, investigate immediately because small misses compound.

Plan for contingencies by stress-testing your cash position under a 20 percent revenue decline scenario-if you’d survive 8 weeks, you need more reserves. Seasonal businesses should build reserves during strong months specifically to cover weak periods rather than borrowing into weakness. Set a cash target as a percentage of annual revenue-typically 10 to 20 percent-and treat reaching that target like hitting a sales goal.

This discipline transforms cash reserves from a nice-to-have into a non-negotiable business requirement.

Cash flow reporting transforms raw financial data into decisions that determine whether your business survives or thrives. You now understand that profit and cash are fundamentally different, that your operating cash flow reveals whether your core business actually generates cash, and that metrics like Days Sales Outstanding and your Cash Conversion Cycle expose exactly where your liquidity gets trapped. The businesses that win act on this information weekly, not yearly.

Start with one metric and one action, then build from there. Audit your current cash flow reporting process and identify the biggest gap between where you are and where you need to be. If your DSO exceeds industry benchmarks, tighten collections immediately. If you lack visibility into seasonal patterns, map your actual cash position over the past 24 months. If you’re uncertain whether your cash reserves are adequate, calculate your weekly burn rate and set a target.

We at My CPA Advisory and Accounting Partners help business owners implement cash flow strategies that actually work. Contact us today to discuss how we can strengthen your cash flow management and help you build the financial foundation your business deserves.

Privacy Policy | Terms & Conditions | Powered by Cajabra