Tax Compliance Readiness 2026: A Practical Roadmap for Growing Businesses

Prepare your business for tax compliance readiness in 2026 with our practical roadmap designed for growing companies.

Tax laws shift every year, and 2026 brings significant changes that affect how your business reports income, manages deductions, and stays compliant. We at My CPA Advisory and Accounting Partners have built this roadmap to help growing businesses navigate these updates without scrambling at tax time.

The steps ahead are straightforward: organize your records, implement the right systems, and plan strategically before the filing deadline arrives.

The One Big Beautiful Bill made permanent many provisions of the Tax Cuts and Jobs Act, and 2026 marks when these changes reshape your actual tax bill. Standard deductions jump again-to $15,750 for single filers, $23,625 for head of household, and $32,200 for married filing jointly-which means your business owners and key employees will see different take-home amounts. Income tax brackets shift upward with inflation annually, so a business generating $150,000 in pass-through income may fall into a lower effective rate than it would have in 2025.

More importantly for growing companies, bonus depreciation returns to 100%, letting you write off equipment and software purchases immediately instead of spreading deductions across years. This matters: if you plan capital investments, timing them into 2026 versus 2027 could defer tens of thousands in tax liability. The qualified business income deduction stays at 20% for pass-through entities like S corporations and LLCs, so your LLC structure remains competitive. Section 179 expensing limits also increase, meaning you can expense up to a higher threshold on machinery and vehicles without depreciating them. Real estate professionals should note that real property placed in service can no longer be expensed under Section 179, only depreciated, so your office buildout strategy needs adjustment if you were counting on immediate write-offs.

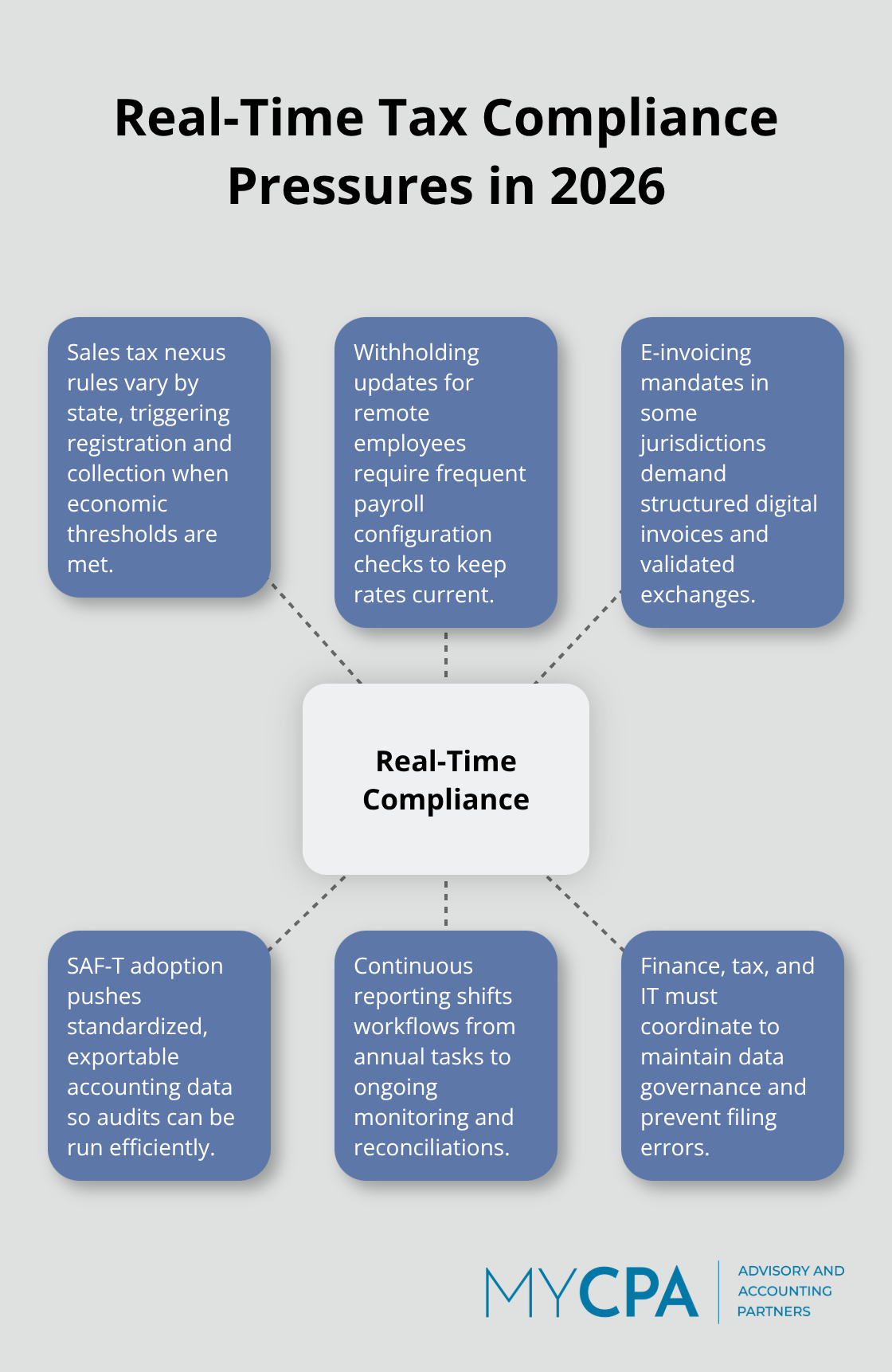

State and local tax law changes vary wildly by jurisdiction, and this is where most growing businesses stumble. If your company operates in multiple states, you face different sales tax nexus rules, updated withholding rates for remote employees, and new e-invoicing mandates in some regions. The IRS and state tax authorities are moving toward continuous real-time tax reporting instead of annual filings, driven by e-Invoicing rollouts and SAF-T (Standard Audit File for Tax) requirements increasingly adopted across jurisdictions.

This shift forces tighter collaboration between your finance, tax, and IT teams to maintain data governance and prevent errors that trigger audits.

Countries and states implementing SAF-T are essentially demanding standardized data extraction from your accounting systems, so if your current tools cannot export clean, audit-ready data in the required format, you will face manual workarounds that eat time and introduce errors. A country-by-country and state-by-state readiness assessment now positions your business ahead-map filing deadlines to your operations and identify which systems need upgrades before the year ends. Your competitive advantage in 2026 comes from having clean data, automated tax calculations, and documented processes ready before authorities demand them, not scrambling when penalties arrive. This foundation sets you up to handle the mid-year tax review and estimated payment planning that follow.

The gap between growing businesses that stay compliant and those that face penalties comes down to one thing: having systems in place before you need them. Right now, before 2026 hits full speed, is when you organize your financial records, lock in accounting tools that export clean data for SAF-T and state reporting, and establish controls that catch errors before they reach the IRS. Most growing businesses operate with spreadsheets, scattered receipts, and reactive bookkeeping until an audit forces change. That approach costs money.

A study by the National Federation of Independent Business found that businesses without documented accounting processes spent an average of 40 extra hours per year on tax prep and remediation. Start now by pulling all financial records into a single, accessible location organized by category: income, expenses, payroll, sales tax, and quarterly payments. If records live across email, bank statements, and handwritten notes, consolidate them into folders with clear naming conventions so anyone on your team can locate a 2025 receipt in under two minutes.

For growing companies with multiple locations or revenue streams, this organization becomes non-negotiable because tax authorities expect you to substantiate deductions with contemporaneous documentation. Real property placed in service, equipment purchases, and R&D costs all require backup showing dates, amounts, and business purpose. Build a filing system now that captures this information as transactions occur, not months later.

Implement accounting software that integrates with your banking and payroll systems to eliminate manual data entry and reduce reconciliation errors. Cloud-based platforms like QuickBooks Online or Xero automatically categorize transactions, flag duplicate entries, and generate reports that match your tax return line items. The critical feature for 2026 compliance is the ability to export standardized data formats that state and local tax authorities increasingly demand.

Test your current system now by running a sample SAF-T export or checking whether your software can produce data in the formats your filing states require. If it cannot, upgrade before year-end rather than scrambling in March when deadlines arrive.

Establish internal controls by assigning clear ownership: one person reviews bank reconciliations monthly, another approves expenses over a threshold, and a third person reconciles payroll taxes quarterly. These controls take three to five hours per month to maintain but catch errors before they become liabilities. Document these processes in a simple checklist or playbook so that if someone leaves your team, the next person knows exactly what to do.

For companies with remote employees across multiple states, implement a control where someone verifies that withholding rates match the employee’s current state of residence, since rates change and many growing businesses miss updates that trigger audit notices. Conduct quarterly reviews of these controls to verify they are actually being followed and adjust them if your business structure changes. This foundation removes the chaos that derails compliance and frees your time to focus on tax planning strategies that actually reduce your bill.

With your records organized, systems in place, and controls documented, you now have the infrastructure to conduct a meaningful mid-year tax review that identifies opportunities before the calendar turns to the final quarter.

Mid-year is the exact moment to stop waiting and run the numbers that determine your actual tax liability for 2026. Most growing businesses skip this step and discover in January that they owe far more than expected or missed deadlines that trigger penalties. A mid-year tax review forces you to calculate estimated quarterly payments based on actual income, not guesses, and identifies which deductions and credits your specific industry qualifies for before you lose the opportunity to claim them.

Pull your year-to-date profit and loss statement and compare it to last year’s performance. Project your full-year results by multiplying six-month results by two. If your business is seasonal or cyclical, adjust for known patterns like higher Q4 revenue or slower summer months. Calculate your federal and state tax liability using that projection and compare it to estimated payments you have already made. If you are underpaid, calculate the shortfall and divide it by remaining quarter payments so you know exactly what to remit to avoid penalties.

The IRS charges interest on underpayment starting October 1, so catching this gap in June costs far less than discovering it in December.

For pass-through entities like S corporations and LLCs, determine whether your current owner distributions and W-2 wages match your projected tax bracket. Assess whether you should adjust compensation before year-end to minimize self-employment taxes or capture additional deductions. This decision directly affects your cash flow and your tax bill, so model both scenarios before the calendar turns to Q4.

Industry-specific deductions vary wildly, and this is where most growing businesses leave money on the table. Construction companies can deduct tools under 100 percent bonus depreciation if purchased before year-end, whereas professional service firms can claim home office deductions only if they maintain a dedicated space used exclusively for business. Real estate investors should verify that any property improvements qualify as capital expenditures rather than repairs, since capital items depreciate over years while repairs deduct immediately.

Review your 2025 tax return with your CPA to identify which credits and deductions you claimed, then assess whether the same circumstances exist in 2026 or whether changes in your business structure, employee count, or revenue streams open new opportunities.

If you hired your first employee, you may qualify for the Work Opportunity Tax Credit, which is available to employers for hiring individuals from certain targeted groups who have faced barriers to employment. If you invested in renewable energy equipment or electric vehicle charging infrastructure, federal credits reduce your tax bill dollar-for-dollar. Technology companies claiming research and development expenses can elect to expense costs immediately under Section 174A rather than amortize over five years, which dramatically accelerates deductions in high-spending years.

The choice between expensing and amortization interacts with foreign tax credits and BEAT calculations for multinational firms, so model both scenarios before filing.

Create a simple spreadsheet listing your top ten expense categories alongside the deduction limits and carryforward rules that apply (this prevents missed opportunities and ensures you capture every dollar your business qualifies for). Review it quarterly to catch changes that affect your year-end planning. This approach transforms tax compliance from a reactive scramble into a proactive strategy that protects your bottom line.

Tax compliance readiness for 2026 requires three concrete actions that you can start this week: organize your financial records now, implement systems that export clean data for state and federal reporting, and conduct a mid-year review that identifies deductions and credits before year-end. Growing businesses that complete these steps avoid penalties, missed opportunities, and the reactive firefighting that distracts from running the business. Those that skip them face scrambles that cost time and money when tax season arrives.

Your competitive advantage comes from moving first while other companies are still gathering receipts in January. You will have already calculated your estimated payments, adjusted compensation for pass-through entities, and claimed industry-specific credits that reduce your actual tax bill (the difference between proactive planning and reactive compliance often reaches tens of thousands of dollars in cash flow). Pull your year-to-date numbers this week, identify which deductions your business qualifies for based on your industry and structure, and upgrade your accounting software if it cannot export standardized data formats.

We at My CPA Advisory and Accounting Partners work with growing businesses to build tax compliance readiness strategies tailored to your specific situation. Our team handles the accounting, tax planning, and business advisory work that transforms compliance from a burden into a strategic advantage. Reach out to discuss your 2026 strategy with someone who understands your business.

Privacy Policy | Terms & Conditions | Powered by Cajabra