Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Tax planning for 2025 requires more than hoping for the best at tax time. The tax landscape has shifted, with new rates, bracket changes, and expiring provisions that directly impact your bottom line. We at My CPA Advisory and Accounting Partners have seen too many business owners and individuals leave money on the table by reacting instead of planning ahead.

This guide walks you through the changes that matter and the strategies that work.

The One Big Beautiful Bill Act reshaped the tax code starting January 1, 2025, and the shifts are substantial enough to rewrite your planning playbook. The standard deduction increased to $31,500 for married filing jointly in 2025 and $15,750 for single filers in 2025, compared to prior-year amounts. More importantly, the federal tax brackets remain in place, but your effective tax burden depends heavily on how you position your income. The 37% top rate still applies, but it now kicks in at $768,700 for married filing jointly and $640,600 for single filers in 2026, meaning high earners face a narrower window before hitting the ceiling. The Child Tax Credit expanded to $2,200 per qualifying child under 17, starting in 2025 with annual inflation adjustments, and this directly reduces your tax bill dollar-for-dollar, not just your taxable income.

The SALT deduction cap increased to $40,000 for 2025, a significant win for residents in high-tax states like California, New York, and New Jersey. This threshold remains at $40,000 through 2029 before reverting to $10,000 in 2030, so accelerating state and local tax payments into 2025 and 2026 makes financial sense if you’re near the cap. The estate tax exemption jumped to $15 million per person for 2026, indexed for inflation, creating a narrow window for high-net-worth individuals to gift or transfer assets before the exemption potentially decreases after 2026.

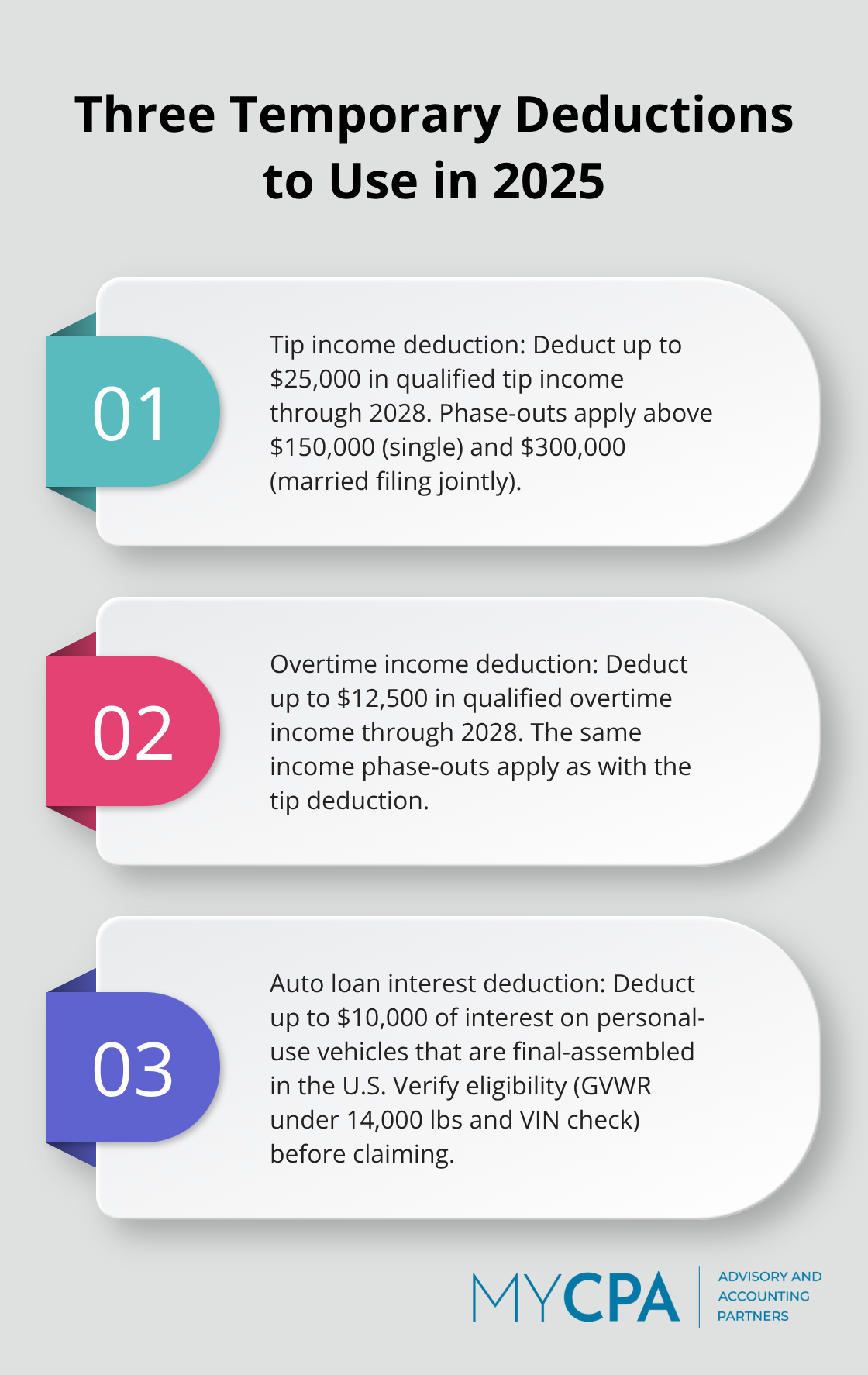

Three new deductions arrived in 2025 that most filers overlook. Qualified tip income up to $25,000 annually becomes deductible through 2028, phasing out above $150,000 in income for single filers and $300,000 for married couples. Service industry workers benefit directly from this cut to your tax burden.

Qualified overtime income up to $12,500 annually also qualifies for deduction through 2028 with identical phase-outs. The auto loan interest deduction allows up to $10,000 in annual interest on personal-use vehicle loans for cars assembled in the United States, phasing out above $100,000 in income for singles and $200,000 for married couples. Verify vehicle eligibility through the NHTSA VIN Decoder before claiming this deduction, as the vehicle must have a gross vehicle weight rating under 14,000 pounds and be final-assembled domestically.

Seniors gained a new deduction of up to $6,000 per person for 2025 through 2028, phasing out above $75,000 in income for singles and $150,000 for married couples. The Qualified Business Income deduction remains permanent at 20% with higher income thresholds of $75,000 for singles and $150,000 for married couples. Self-employed individuals and business owners can now deduct 100% of business equipment placed in service after January 19, 2025, which accelerates depreciation benefits significantly.

The clean energy tax credits expire at the end of 2025, and missing these deadlines costs you thousands. Home energy credits for windows, doors, insulation, and HVAC systems disappear after December 31, 2025, so purchases must close before year-end to qualify. The electric vehicle tax credit of up to $7,500 expires for vehicles acquired after September 30, 2025. The qualified commercial clean vehicle credit also expires for acquisitions after September 30, 2025, affecting business fleets. A 0.5% adjusted gross income floor on charitable deductions begins in 2026, tightening deduction eligibility, so bunching charitable contributions into 2025 and considering donor-advised funds to spread distributions over multiple years protects your deduction strategy.

These changes create both opportunities and urgency. The window to claim expiring credits closes fast, and the new deductions require careful income planning to maximize their value. Understanding which provisions apply to your situation determines whether you pay more or less in 2025 taxes.

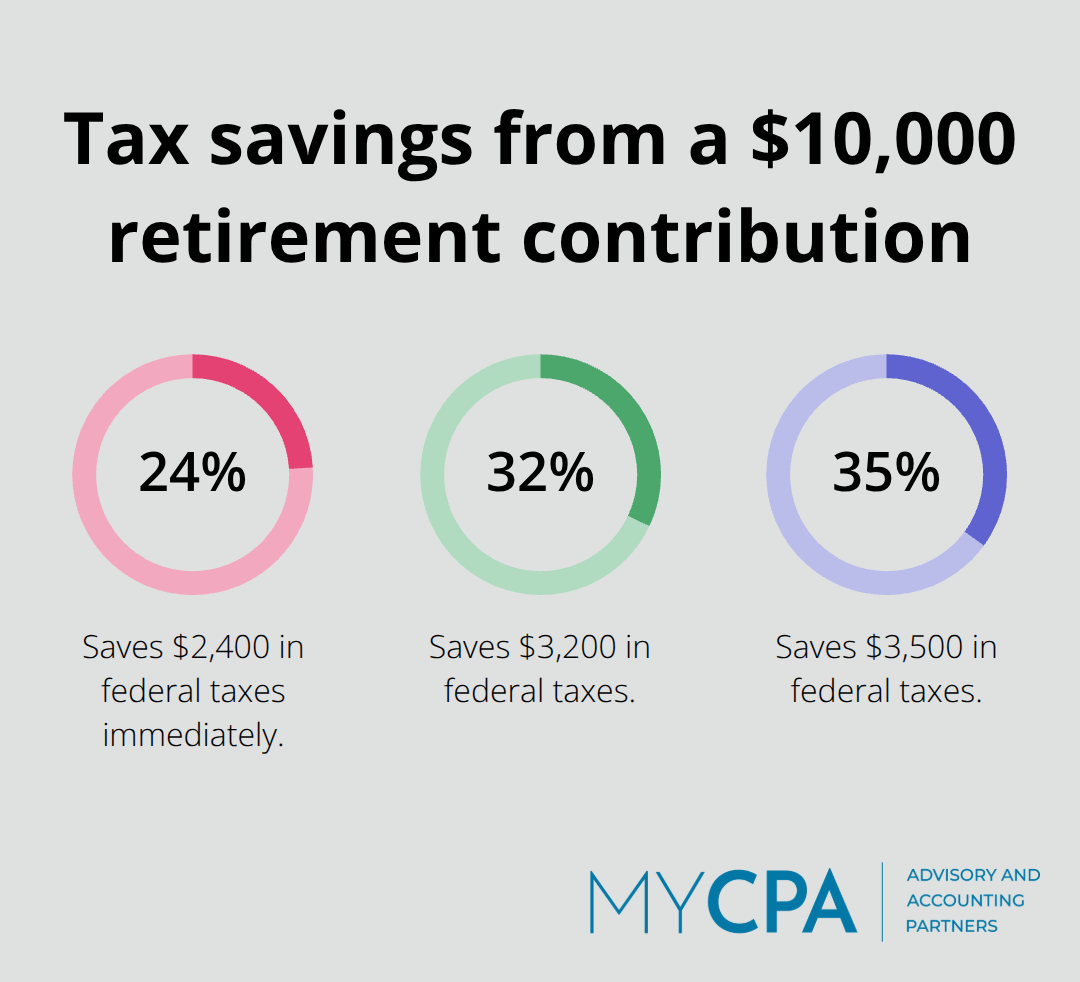

The real power of 2025 tax planning sits in timing decisions you control right now. Most people treat income and deductions as fixed, but they’re not. You can shift when income arrives, accelerate or defer deductions, and frontload retirement contributions to shrink your taxable income substantially. The IRS allows traditional IRA contributions up to $7,000 for 2025, or $8,000 if you’re age 50 or older, and these contributions reduce your taxable income dollar-for-dollar. If you’re self-employed or own a business, a Solo 401(k) lets you contribute up to $23,500 as the employee plus an additional 25% of compensation as the employer in 2025, combining employee deferrals and employer contributions in ways that W-2 employees cannot access. The math is straightforward: a $10,000 retirement contribution at a 24% tax bracket saves you $2,400 in federal taxes immediately. For high earners approaching the 32% or 35% brackets, that same contribution saves $3,200 to $3,500. You must make 2025 contributions by December 31, 2025 to claim them on your 2025 tax return (except IRAs, which allow contributions until April 15, 2026).

Roth conversions deserve serious attention in 2025 because you pay taxes on the converted amount at your current rate, but the funds grow tax-free forever and bypass required minimum distributions in retirement. If you’ve experienced a business loss, market downturn, or lower-income year, a Roth conversion locks in that lower tax rate. The strategy works best when your income dips temporarily, allowing you to convert larger amounts at a reduced tax cost.

The 20% Qualified Business Income deduction remains permanent with higher income thresholds, meaning self-employed individuals and business owners can deduct 20% of qualified business income once they fall below $75,000 (single) or $150,000 (married filing jointly). To maximize this deduction, structure your business to separate active business income from passive investment income, and track W-2 wages paid to employees because higher wages increase your allowable QBI deduction.

Charitable giving timing changed dramatically for 2026 because a 0.5% adjusted gross income floor on charitable deductions takes effect, making bunching contributions into 2025 financially smarter. If you donate $20,000 annually, consider donating $40,000 in 2025 and $0 in 2026 to clear the AGI floor in one year instead of spreading deductions across two years where one year falls below the threshold. Donor-advised funds serve this strategy perfectly because you claim the full deduction in 2025 when you fund the account, but distribute to charities over multiple future years at your own pace.

The SALT deduction cap at $40,000 through 2029 creates a deadline mentality for state and local tax planning. If you live in California, New York, or New Jersey, your annual state income tax plus property taxes likely approach or exceed $40,000, meaning you hit the cap regardless. The smarter move involves paying January 2026 estimated state taxes in December 2025 to accelerate the deduction into the year with lower AGI or higher other deductions. Estimated tax payments themselves carry strategic value because business owners who underpay face penalties and interest, but overpaying gives the IRS an interest-free loan. Calculate your 2025 income projection now and adjust quarterly estimated payments accordingly.

For business owners, the 100% bonus depreciation on equipment placed in service after January 19, 2025 accelerates deductions dramatically. A $50,000 piece of machinery can be fully deducted in 2025 instead of depreciated over five or seven years, compressing your taxable income and freeing cash for reinvestment or debt paydown. This provision applies to qualifying property, so verify that your equipment meets the requirements before claiming the deduction. The timing advantage here is substantial-placing equipment in service before year-end captures the full deduction in 2025 rather than waiting until 2026. These income and contribution strategies work best when coordinated together, which is why business owners and high-income individuals benefit from professional guidance to model different scenarios and identify which combination delivers the largest tax reduction for their specific situation.

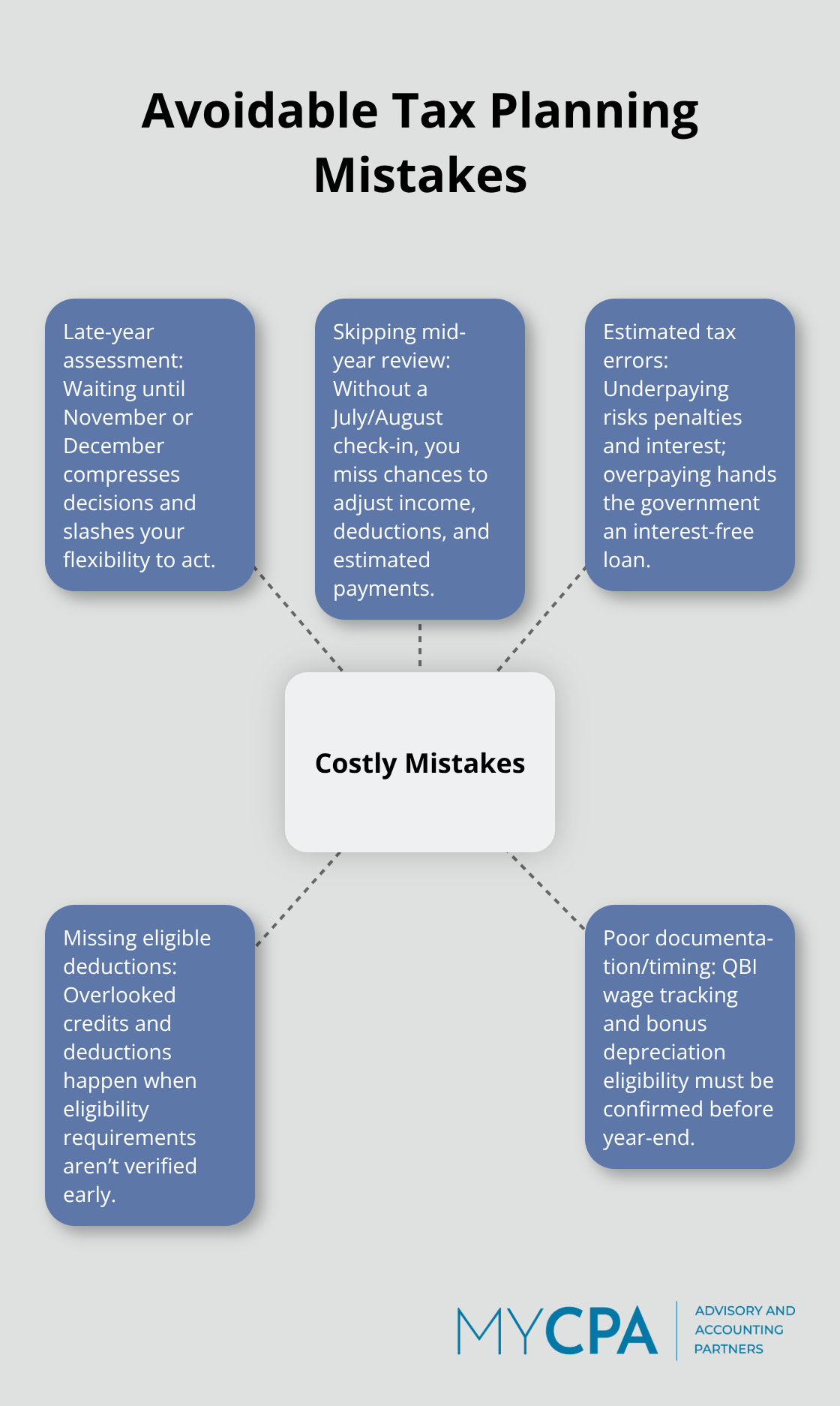

Most tax planning failures happen long before April, yet people treat December as the first planning month. Business owners and high-income earners make the same costly errors repeatedly, and nearly all of them are preventable. The biggest mistake is waiting until year-end to assess your tax position, then scrambling to make decisions in a compressed timeframe with incomplete information. In November, you’ve already earned most of your annual income, spent most of your business revenues, and lost the flexibility to shift timing strategically. A business owner who discovers in December that they’re facing a $50,000 tax bill has far fewer options than someone who identified that liability in August and spent four months adjusting quarterly estimated payments, accelerating deductions, or timing equipment purchases.

The IRS data shows that approximately 37% of taxpayers qualify for simplified filing, yet the remaining 63% miss deductions and credits worth thousands because they don’t conduct a mid-year tax review. A mid-year tax review in July or August gives you time to adjust course, but December decisions constrain your options severely. The compressed timeframe forces you to make reactive choices instead of strategic ones, and reactive choices almost always cost more in taxes than proactive planning would have saved.

Estimated tax payments reveal another critical mistake: business owners who underpay face penalties and interest charges that compound throughout the year, while those who overpay surrender an interest-free loan to the government. The correct approach calculates your projected 2025 income now, compares it to your current quarterly payments, and adjusts the remaining installments accordingly. If your business had a strong first half and you’re tracking toward a higher income year, increase your third and fourth quarter estimates to prevent penalties. Conversely, if revenue declined mid-year, reduce estimates to avoid overpayment.

Missing eligible deductions and credits represents the third category of expensive mistakes, but this one cuts deeper because people simply don’t know what they qualify for. The $10,000 auto loan interest deduction applies only to vehicles with a gross vehicle weight rating under 14,000 pounds and final-assembled in the United States, verified through the NHTSA VIN Decoder. A business owner who financed a vehicle without checking eligibility beforehand loses the deduction entirely. The tip income deduction up to $25,000 requires meticulous documentation throughout 2025, not retroactive reconstruction in March 2026, and the IRS expects detailed records showing daily tip amounts.

The senior deduction of up to $6,000 phases out above $75,000 for single filers, meaning a retiree with $76,000 in income loses eligibility entirely, yet many seniors don’t realize they could reduce income through strategic timing of IRA distributions or charitable contributions to stay below the threshold. The charitable deduction changes starting in 2026 create urgency to bunch contributions into 2025, but only if your AGI and deduction pattern actually benefit from bunching. Someone who donates $5,000 annually and has an AGI of $100,000 gains nothing from accelerating gifts because their charitable deductions never exceeded the 0.5% AGI floor anyway. The error lies in applying generic strategies without calculating your specific numbers first.

Qualified Business Income deduction optimization requires tracking W-2 wages paid to employees because wages directly increase your allowable QBI deduction, yet many self-employed individuals don’t maintain this documentation systematically. The 100% bonus depreciation on equipment placed in service after January 19, 2025 demands that you verify equipment qualifies before December 31, 2025, not after you’ve already made the purchase. Waiting until tax time to discover your equipment doesn’t meet the requirements means losing a deduction worth thousands. The common thread across all these mistakes is that they require action during the year, not reaction at tax time.

Tax planning for 2025 succeeds when you act now instead of waiting until April. The changes we’ve covered-from the expanded SALT deduction cap to the 100% bonus depreciation on equipment to the expiring clean energy credits-create real opportunities to reduce your tax bill, but only if you implement them before December 31, 2025. A business owner who delays equipment purchases until January 2026 loses the full deduction in 2025, and a high-income earner who fails to bunch charitable contributions into 2025 faces a tighter deduction threshold in 2026.

Your tax planning for 2025 priorities require three concrete actions. Conduct a mid-year income assessment in July or August to identify whether you’re tracking toward a higher or lower tax bracket than expected, then adjust quarterly estimated payments and timing decisions accordingly. Verify that you qualify for every deduction and credit available to you-the auto loan interest deduction, the senior deduction, the tip income deduction, the overtime deduction-by checking eligibility requirements now rather than discovering disqualifications at tax time.

Professional guidance matters because tax planning requires coordination across multiple strategies (a Roth conversion that makes sense in isolation might trigger the Medicare surtax or reduce your eligibility for other credits when viewed holistically). We at My CPA Advisory and Accounting Partners help business owners and individuals model different scenarios, identify which strategies deliver the largest tax reduction for their specific situation, and implement those strategies with confidence. Start your tax planning for 2025 today by scheduling a consultation with our team to review your income projection, identify applicable deductions and credits, and build a coordinated strategy that works for your situation.

Privacy Policy | Terms & Conditions | Powered by Cajabra