Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Corporate tax compliance isn’t optional-it’s the foundation of running a legitimate business. Miss a deadline, misclassify an expense, or skip proper documentation, and you’re inviting penalties, audits, and unnecessary stress.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how companies of all sizes struggle with the complexity of federal, state, and local tax rules. The good news is that staying compliant doesn’t require guesswork. This guide walks you through the requirements, common pitfalls, and proven strategies to keep your tax obligations under control.

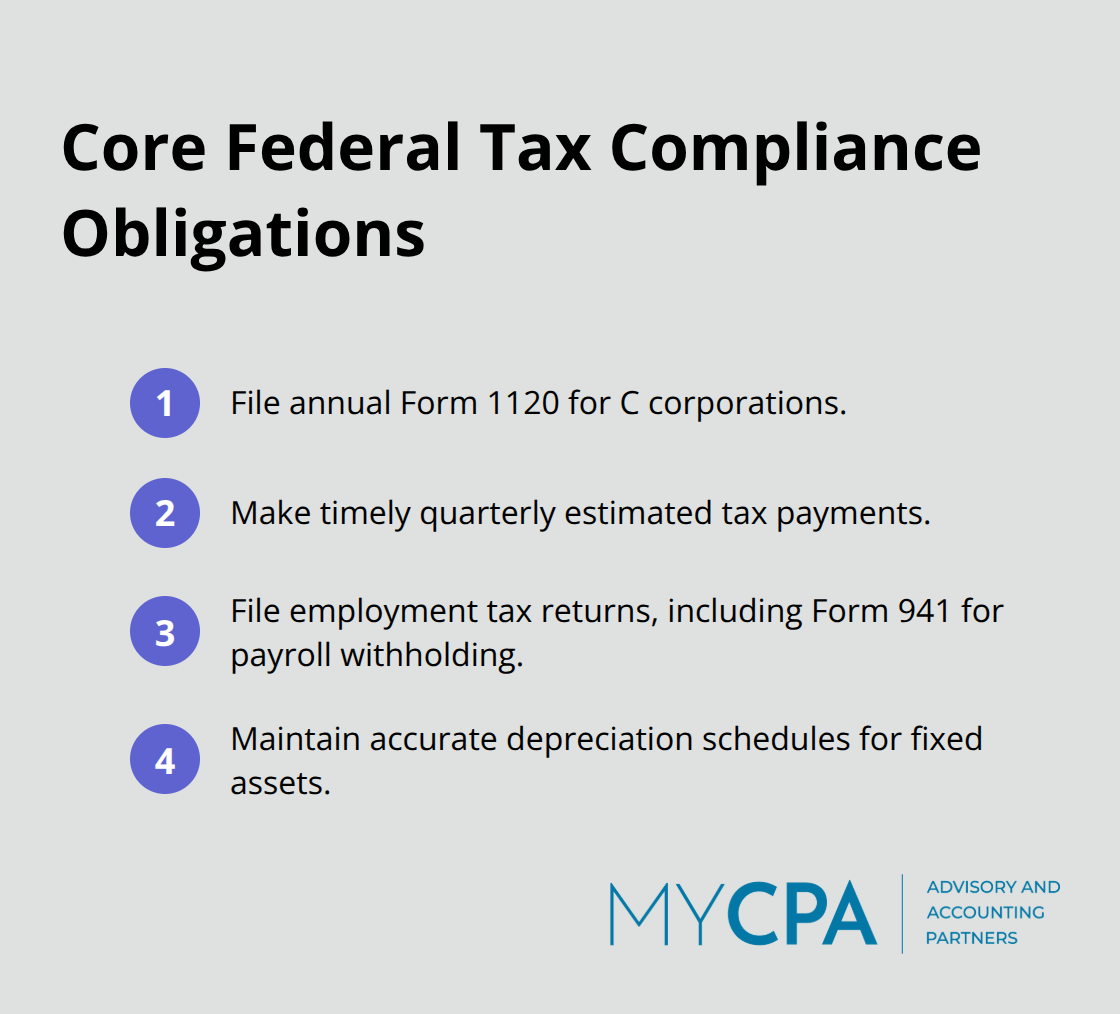

Federal tax obligations extend far beyond the annual corporate income tax return. The IRS requires Form 1120 filings for C corporations, which demand roughly 100 hours of preparation time on average according to IRS estimates, though large corporations often spend closer to 690 hours managing complex schedules and supporting documentation. Your business must also file quarterly estimated tax payments, employment tax returns including Form 941 for payroll withholding, and depreciation schedules that consume approximately 448 million compliance hours annually across all businesses. Americans spend more than 6.5 billion hours a year trying to comply with the tax code at an estimated cost of over $300 billion.

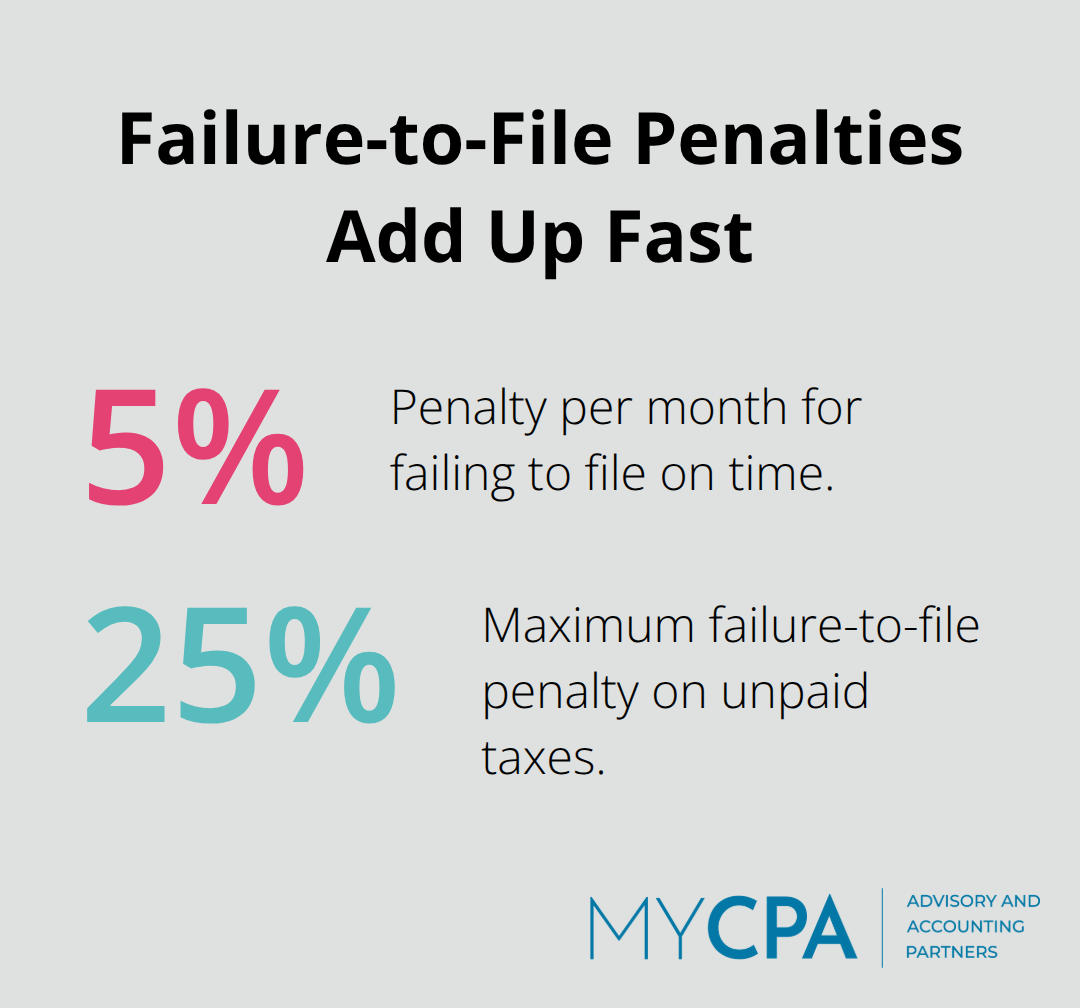

Missing a single deadline triggers penalties that compound quickly. The IRS charges failure-to-file penalties of 5 percent per month up to 25 percent of unpaid taxes, plus interest that accrues daily.

These penalties accumulate faster than most business owners anticipate, turning a missed filing into a significant financial liability within weeks. The combination of penalties and interest can exceed the original tax owed if left unaddressed for several months.

State and local tax requirements layer additional complexity because states don’t automatically conform to federal changes. Some states use rolling conformity, in which they automatically adopt federal tax changes as they occur. This fragmentation matters enormously: when the One Big Beautiful Bill Act passed in July 2025, many states hadn’t yet updated their statutes to reflect changes to depreciation rules, R&D expensing, and foreign income treatment. Illinois, for example, had to actively update its statute to address the renamed Net CFC Tested Income provision, while other states created ambiguity that invites audit risk. About 12 states now tax some portion of global intangible low-taxed income, with Massachusetts considering additions that could affect multistate filers.

Industry-specific rules add another layer of complexity to your tax obligations. Renewable energy companies qualify for investment tax credits, manufacturers claim R&D credits, and construction firms navigate prevailing wage requirements that vary by contract type and location. Each industry faces distinct compliance demands that federal and state rules don’t always address uniformly. The real danger isn’t understanding one rule perfectly; it’s missing the interactions between federal and state provisions or failing to track when states update their conformity status.

Establish a monitoring system that flags federal changes within 30 days of enactment and cross-references your specific state’s conformity approach rather than assuming alignment. This proactive approach prevents the costly surprises that emerge when tax law shifts and your business operates under outdated assumptions. The complexity of multistate operations, combined with frequent federal updates and varying state responses, makes real-time tracking essential to your compliance strategy. Understanding these obligations sets the stage for identifying where most businesses stumble-and how to avoid those costly mistakes.

Most corporate tax compliance failures stem from misclassified business expenses, which the IRS audits aggressively because they represent high-yield targets. An owner deducts a vehicle as a business asset when personal use dominates, or categorizes meals as entertainment when they fail the 50 percent deduction threshold, or claims home office expenses without meeting IRS qualification standards. Depreciation and amortization schedules present significant complexity in asset classification at scale. The problem intensifies across multiple states because a deduction allowed federally might face disallowance in your state, triggering cascading adjustments that generate additional penalties and interest. Without documentation explaining why an expense qualifies as deductible, you cannot defend it during an audit. The IRS expects contemporaneous records supporting every deduction claimed, and digital records now make this obligation manageable rather than burdensome.

The second mistake involves treating filing deadlines and extension requests as flexible timelines. The IRS charges 5 percent per month for failure-to-file penalties, capped at 25 percent of unpaid taxes, plus daily interest that never stops accruing. A business that misses the March 15 deadline for Form 1120 and files two months late faces a 10 percent penalty before interest even factors in. Extensions buy you time but do not eliminate the underlying tax liability, yet many business owners confuse an extension with a reprieve from payment. This confusion costs thousands in unnecessary penalties that accumulate faster than most owners anticipate. The combination of penalties and interest can exceed the original tax owed if left unaddressed for several months.

Inadequate record-keeping creates the conditions for both of the above failures to compound. Without integrated accounting systems, you waste time reconstructing records months after transactions occur, introducing errors and gaps that auditors exploit. Spreadsheets, invoice scans, and categorized accounting software outputs all qualify as documentation, yet many businesses operate without systems that capture this information systematically. The interaction between these three mistakes generates real damage: misclassified expenses go undetected until an audit, the audit happens after the filing deadline has passed, and weak documentation makes defending your position impossible.

Treating tax compliance as an operational discipline rather than a once-annual event prevents these interconnected failures from taking root. Real-time tracking of expenses, immediate categorization within accounting software, and regular internal reviews catch classification errors before they reach an auditor’s desk. The cost of fixing these mistakes after an audit begins far exceeds the investment in preventing them upfront. Establishing clear documentation standards and assigning responsibility for record-keeping to specific team members transforms compliance from a reactive scramble into a managed process. This foundation positions your business to implement the systems and strategies that actually reduce your tax burden rather than simply managing the fallout from poor compliance practices.

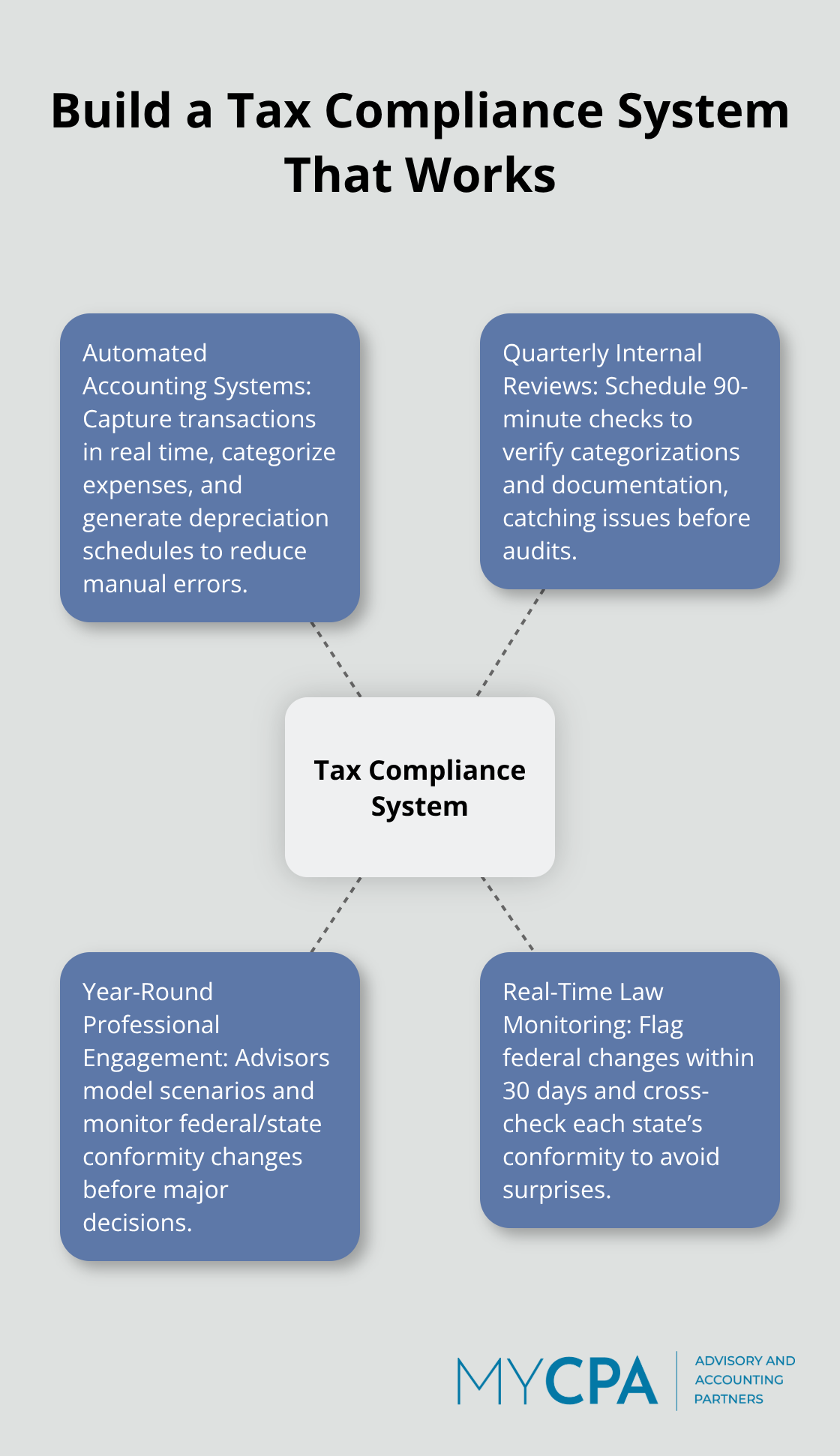

Automated accounting systems form the backbone of modern tax compliance, yet most businesses treat them as optional luxuries rather than operational necessities. The IRS estimates that Form 1120 preparation consumes roughly 100 hours for average corporations and 690 hours for large ones, largely because manual data entry and spreadsheet reconciliation waste enormous amounts of time. Integrated accounting software like QuickBooks captures transactions in real time and automatically categorizes expenses according to your chart of accounts. The software generates depreciation schedules without the manual calculations that introduce errors.

The investment in setup and training pays dividends immediately: your team stops reconstructing records months after transactions occur, and audit-ready documentation materializes automatically. Month-end close cycles compress from weeks into days. More importantly, real-time visibility into your tax position throughout the year lets you identify deduction opportunities and potential exposure before the filing deadline arrives. Configure your system to flag transactions that cross state lines, trigger multistate sales tax obligations, or qualify for industry-specific credits so nothing slips through unnoticed.

Quarterly internal tax audits catch classification errors, missing documentation, and deadline risks before they become audit vulnerabilities. Schedule a 90-minute quarterly review where someone from your finance team walks through recent transactions and verifies expense categorizations against IRS guidance. This person confirms that all supporting documentation is stored systematically. This practice costs almost nothing but prevents the cascading failures that plague unprepared businesses: a misclassified vehicle expense caught in March gets corrected before year-end rather than discovered during an IRS audit two years later.

The quarterly rhythm keeps tax compliance visible throughout the year instead of vanishing until March arrives. Your team develops familiarity with what proper documentation looks like and catches gaps while you still have time to gather missing records. This consistency transforms tax compliance from a crisis event into a managed operational function.

Work with tax professionals year-round rather than hiring them in March for annual return preparation. Year-round professional engagement means your advisor understands your business operations and stays current on state conformity changes affecting your specific jurisdictions. Your advisor models tax scenarios before major transactions occur. This relationship transforms tax planning from a reactive scramble into a strategic discipline where decisions get evaluated for tax impact before execution.

Continuous professional engagement costs less than the penalties, interest, and lost deduction opportunities that result from treating taxes as an annual event rather than an ongoing operational function. Your advisor monitors federal and state law changes, assesses how new provisions interact with your specific situation, and adjusts your compliance processes accordingly. This proactive approach prevents the costly surprises that emerge when tax law shifts and your business operates under outdated assumptions.

Corporate tax compliance stops being a burden the moment you treat it as a managed operational function rather than an annual scramble. The three mistakes we covered-misclassified expenses, missed deadlines, and weak documentation-all stem from the belief that tax obligations can wait until March. Automated accounting systems eliminate the manual waste that consumes hundreds of hours annually, quarterly internal reviews catch problems while you still have time to fix them, and year-round professional engagement transforms tax planning from guesswork into strategy.

The real benefit of proactive tax management extends beyond compliance itself. When your tax position is clear and defensible, you identify legitimate deduction opportunities that reduce your actual tax liability rather than simply managing penalties and interest. You gain visibility into how major business decisions affect your tax burden before you execute them, and your team stops wasting time reconstructing records to focus on work that generates revenue.

We at My CPA Advisory and Accounting Partners help business owners build exactly this kind of corporate tax compliance infrastructure through tax services and business advisory expertise that combines automated systems, quarterly reviews, and year-round professional engagement. The investment in getting this right pays for itself through reduced penalties, recovered deductions, and the peace of mind that comes from knowing your tax obligations are handled correctly.

Privacy Policy | Terms & Conditions | Powered by Cajabra