Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Your financial statements tell a story-but only if they’re accurate, complete, and trustworthy. Weak reporting practices create confusion, expose you to compliance risks, and undermine stakeholder confidence.

At My CPA Advisory and Accounting Partners, we’ve seen how financial reporting best practices transform how businesses operate. The right systems and processes turn raw data into insights that drive smarter decisions.

Inaccurate financial reporting costs businesses real money. When data is wrong, stakeholders make decisions based on false information. Investors pull funding. Lenders deny credit. Management allocates resources to the wrong priorities. A 2025 study by the Association of Certified Fraud Examiners found that U.S. publicly traded companies lost a median 1.06% of annual revenue to known frauds. That’s not theoretical damage-it’s cash leaving your business.

Accurate reporting stops this bleeding. When your numbers are solid, investors trust your growth projections. Banks approve loans faster. Your board makes strategic decisions with confidence. Transparent financial statements attract better funding terms and accelerate capital access.

Regulatory bodies don’t tolerate sloppy reporting. The SEC, IRS, and state authorities expect consistency, completeness, and timeliness. Missing a filing deadline or submitting incorrect tax data triggers penalties, audits, and reputational damage that takes years to repair.

Accurate reporting forms the foundation of real strategic planning. You cannot forecast cash flow accurately if your historical data is unreliable. You cannot identify which product lines are profitable if your cost coding is inconsistent. You cannot spot operational inefficiencies if reconciliations happen months after transactions occur.

The businesses that win implement reporting systems that deliver verified data on a predictable schedule. They use that data to adjust pricing, cut waste, and chase opportunities faster than competitors. Your financial reports should be a competitive advantage, not a compliance burden. Strong reporting practices require consistent systems, clear processes, and disciplined execution-which is exactly what the next section covers.

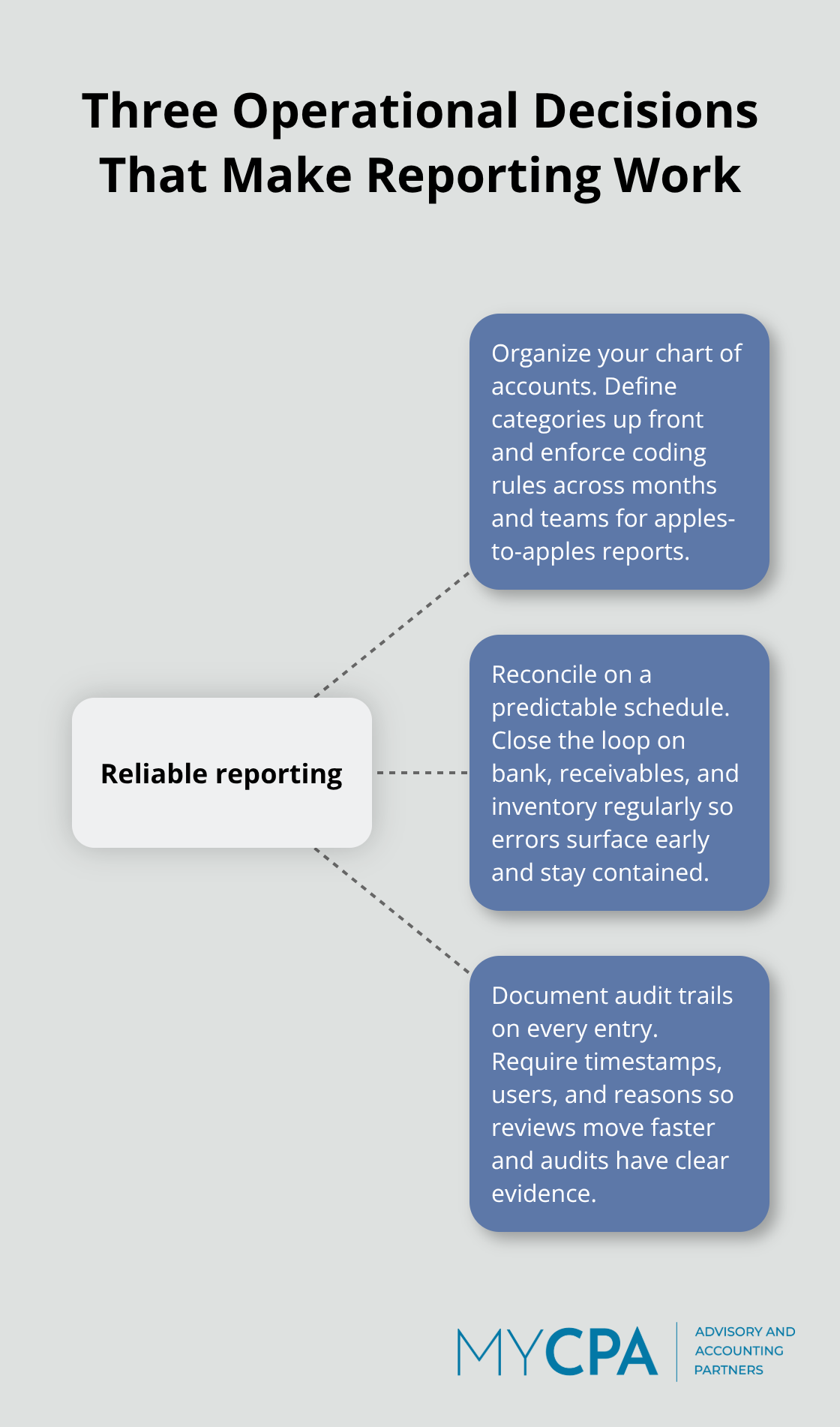

The gap between companies with reliable financials and those constantly chasing errors comes down to three operational decisions: how you organize accounts, when you verify data, and what you document. Businesses fail at reporting not because they lack software or staff, but because they skip these fundamentals.

A consistent chart of accounts acts as your financial language-every transaction coded the same way across months and years. You must define whether consulting revenue goes to service revenue or professional services, then enforce that rule everywhere. When coding standards drift, your P&L becomes unreliable. You cannot compare this quarter to last quarter if the categories keep shifting.

Set your chart of accounts before you process the first transaction, then document every rule. Real businesses use 80 to 150 accounts-not 500. Too many accounts create confusion; too few hide problems. This discipline pays off immediately when you run reports and the numbers actually make sense.

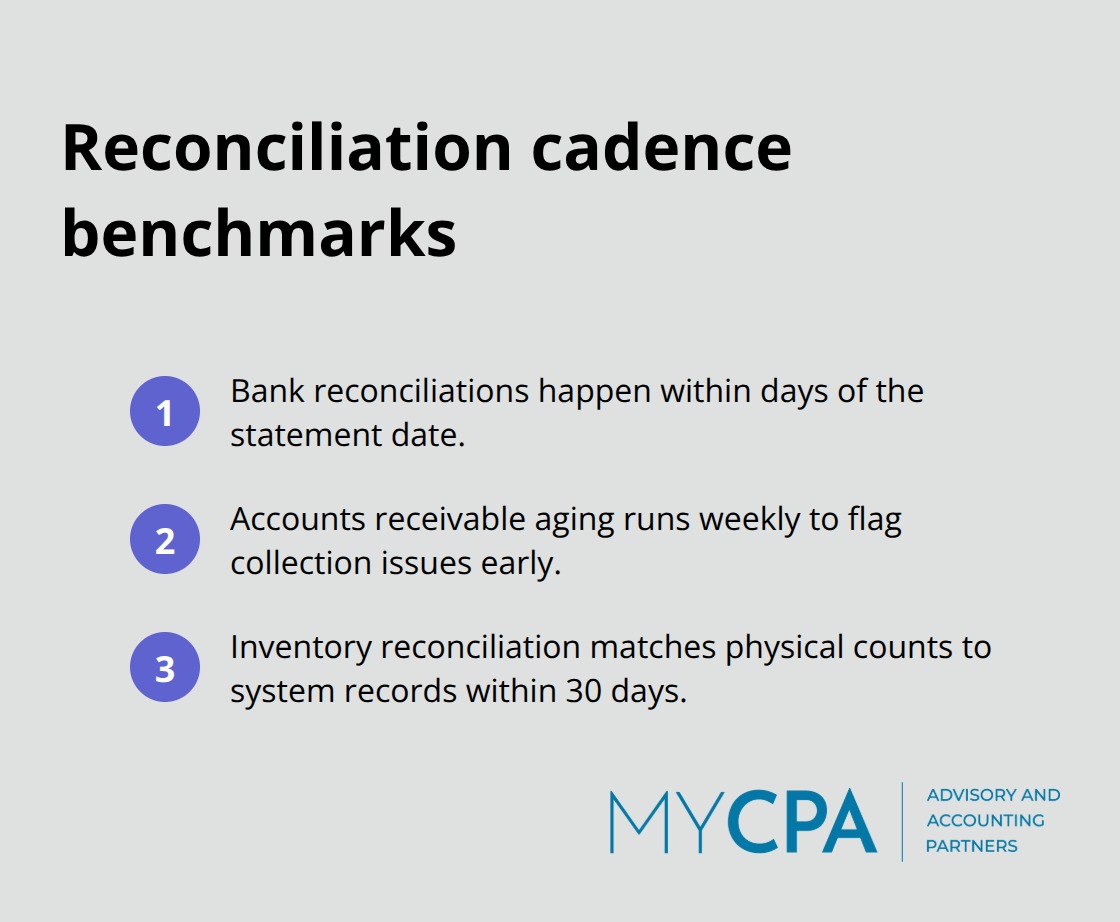

Once accounts are locked in, timely reconciliation separates companies that know their position from those that guess. Reconciliation means comparing what your accounting system says you have to what actually exists. Bank reconciliation should happen within days of the statement date, not months later. Accounts receivable aging should run weekly so you catch collection problems before they become write-offs.

Inventory reconciliation should match physical counts to system records within 30 days.

The faster you reconcile, the faster you spot errors and the less damage they cause. Companies that reconcile monthly catch issues while they are still fixable; companies that reconcile quarterly or annually often discover problems too late to recover. Speed matters because every day a discrepancy sits unresolved is a day your stakeholders operate with incomplete information.

Documentation and audit trails complete the picture. Every adjustment, reversal, and manual entry needs a timestamp, a user ID, and a reason. This is not bureaucracy-it is accountability. When an auditor or your own controller asks why a number changed, you show the entry, not guess.

Cloud-based accounting platforms like QuickBooks Online and Xero build audit trails automatically. Spreadsheets do not. If you are still managing significant portions of your financials in Excel, you are operating without a safety net. The platforms that track who changed what and when give you the visibility you need to stand behind your numbers with confidence.

These three elements-consistent accounts, timely reconciliation, and documented trails-form the backbone of reporting that stakeholders trust and that actually reflects your business. With these systems in place, you shift from spending time fixing old mistakes to spending time spotting new opportunities. The next section shows you exactly which mistakes derail even well-intentioned teams and how to avoid them.

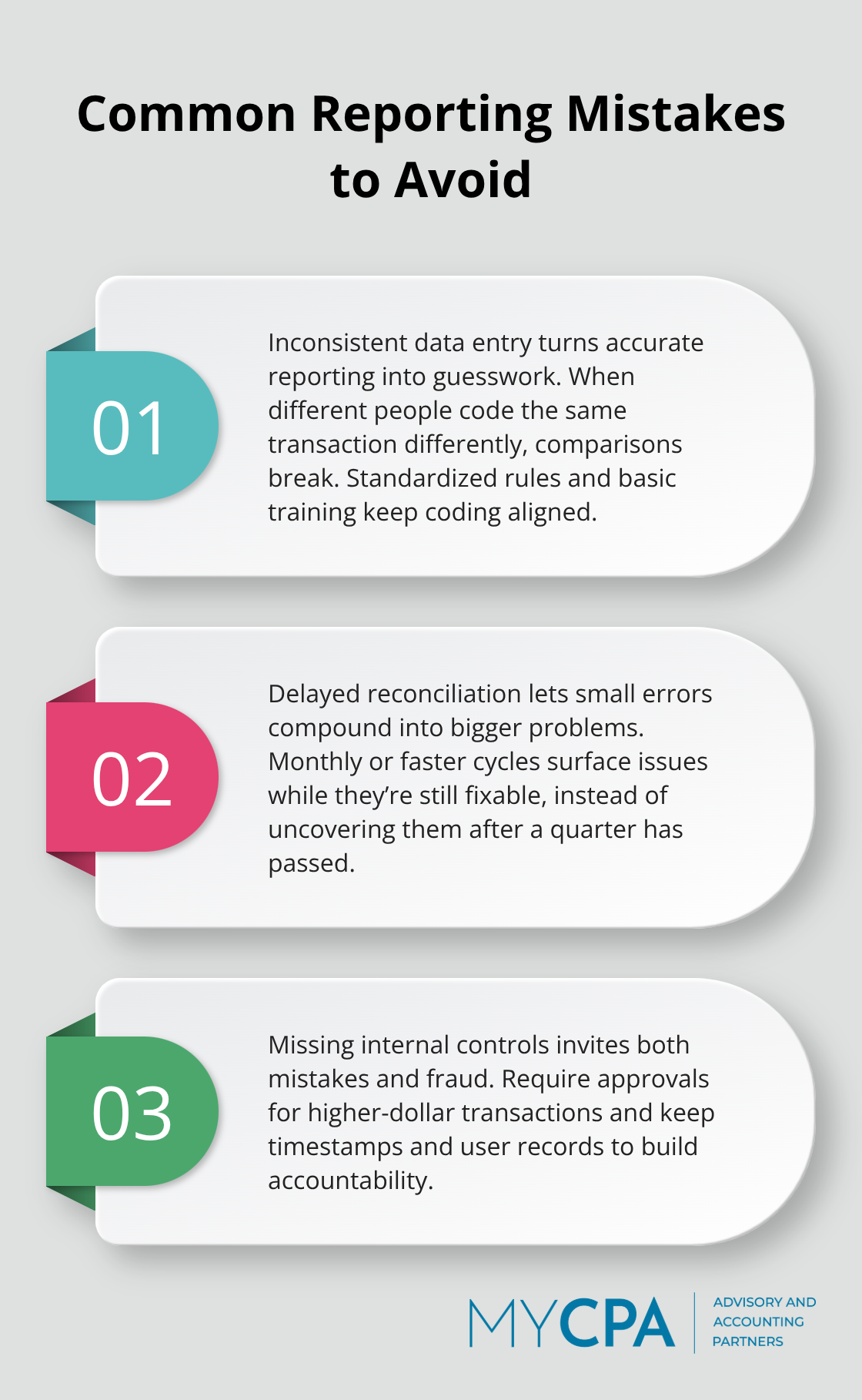

Most businesses fail at reporting because they allow inconsistent data entry to compound across months and years. When one person codes a client payment as accounts receivable and another codes it as revenue, your reports become fiction. This happens constantly in companies still relying on manual entry and spreadsheets.

A single typo in a vendor invoice-swapping digits so $5,000 becomes $50,000-cascades through your P&L and balance sheet. The damage multiplies when multiple people enter data without a shared standard.

Businesses spend weeks chasing phantom variances because nobody enforced a consistent coding rule. The fix is brutal simplicity: lock your chart of accounts, train every person who touches data on the exact same rules, and use accounting software that flags unusual entries before they post. QuickBooks Online and Xero both allow you to set default accounts and restrict who can modify transactions. Use those controls. Spreadsheets give everyone the freedom to enter data however they want, which is exactly why spreadsheets fail at scale.

You cannot fix what you do not see. When reconciliation happens quarterly instead of monthly, errors sit undetected for 90 days. A missing invoice, a duplicate payment, or a bank error compounds into a larger mess. Companies that reconcile bank accounts within three days of the statement close catch problems while they are still simple to fix. Companies that wait six weeks discover that the error has tangled itself into multiple other transactions.

The speed of reconciliation directly determines the cost of fixing mistakes. Early detection saves time and money; late detection multiplies the damage across your entire financial picture.

The absence of internal review represents the third critical failure point. A second pair of eyes catches mistakes that the first person misses. A documented approval process creates accountability. If every transaction over a certain amount requires supervisor sign-off (and that approval is timestamped and recorded), then nobody can slip a questionable entry through.

Without these controls, a single person with access to your accounting system can move money, hide losses, or create fictitious revenue with almost no friction. Build your controls to assume that mistakes and bad intentions exist, not to assume that everyone will behave perfectly. Segregation of duties is essential for internal control and prevents bigger issues from arising.

Financial reporting best practices rest on three operational decisions: organize your accounts consistently, reconcile data on a predictable schedule, and document every transaction. These fundamentals separate businesses that trust their numbers from those constantly chasing errors. Accurate reporting attracts better funding terms, accelerates loan approvals, and builds investor confidence that compounds into measurable competitive advantage.

Cloud-based platforms like QuickBooks Online eliminate the spreadsheet chaos that derails teams, while regular reconciliation cycles transform financial reporting from a quarterly scramble into a predictable rhythm. Internal controls create the checks and balances that protect your business from both honest mistakes and intentional fraud. Strong financial reporting is not a one-time project-it is an ongoing commitment to accuracy and transparency that pays dividends for years.

We at My CPA Advisory and Accounting Partners help businesses implement these practices through tailored accounting services and QuickBooks expertise. If your current reporting process feels fragmented or unreliable, our team can help you build systems that work. Financial reporting best practices transform how you operate and compete.

Privacy Policy | Terms & Conditions | Powered by Cajabra