Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Tax season brings opportunity, not just obligation. The right strategies can significantly reduce what you owe while keeping everything above board.

We at My CPA Advisory and Accounting Partners have helped countless business owners and self-employed professionals minimize taxes legally in 2026. This guide walks you through proven approaches that work.

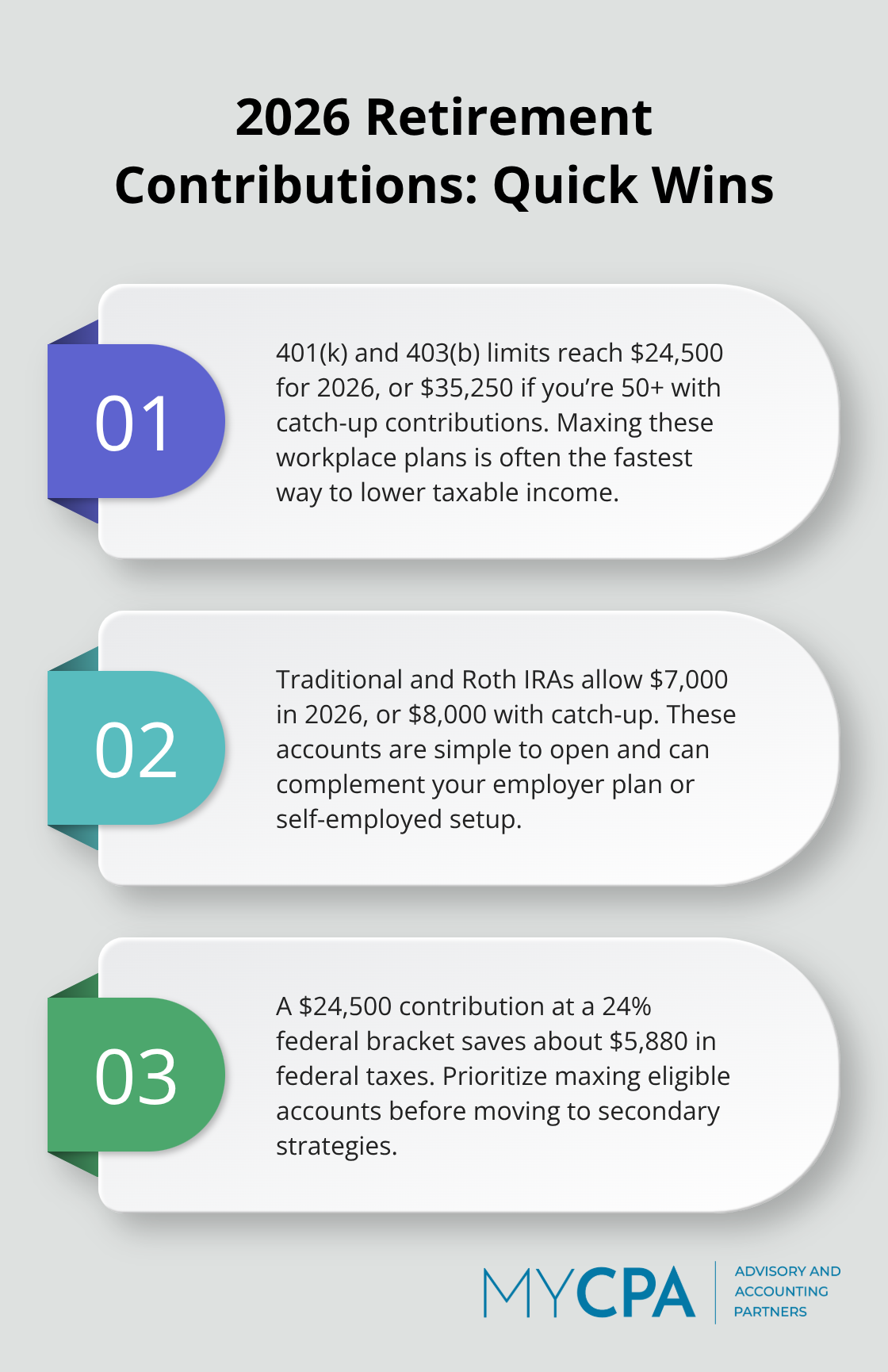

The IRS sets annual contribution limits specifically to encourage tax-deferred saving, and these limits form your most direct path to reducing taxable income in 2026. For traditional 401(k) and 403(b) plans, you can contribute up to $24,500 in 2026, or $35,250 if you’re 50 or older with catch-up contributions. Individual Retirement Accounts allow $7,000 annually, or $8,000 with catch-up contributions. These contributions reduce your taxable income dollar-for-dollar, which means a $24,500 contribution saves approximately $5,880 in federal taxes alone for someone in the 24% bracket. The math is straightforward: maximize these accounts first before exploring other strategies.

Health Savings Accounts offer something most retirement plans don’t: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. This triple advantage makes HSAs exceptionally valuable. In 2026, contribution limits reach $4,150 for self-only coverage and $8,300 for family coverage. You can only contribute to an HSA if you’re enrolled in a high-deductible health plan with a minimum deductible of $1,550 self-only or $3,100 family. Many business owners overlook this account because they assume it’s only for current medical expenses, but HSAs function as stealth retirement accounts once you turn 65-you can withdraw funds for any purpose (taxed as ordinary income, but without the 20% penalty), making them superior to standard savings accounts. If you have the cash flow, max your HSA alongside your 401(k) for maximum tax efficiency.

If you’re self-employed without employees, a Solo 401(k) versus SEP-IRA comparison shows that a Solo 401(k) outperforms in almost every scenario because it allows both employee deferrals and employer contributions within the same account, while a SEP-IRA limits you to employer contributions only. A Solo 401(k) also permits loans against your balance-something SEP-IRAs prohibit-giving you emergency liquidity without triggering taxable withdrawals. The administrative burden is slightly higher, but the tax savings justify it. For 2026, you could theoretically contribute $70,000 to a Solo 401(k) versus roughly $35,000–$40,000 to a SEP-IRA depending on net self-employment income. That difference compounds over decades.

You should set up whichever account matches your income and cash-flow situation by September to maximize 2026 contributions, since procrastination often costs thousands in missed deductions. Once you establish these tax-advantaged accounts, the next step involves identifying which business expenses you can legally write off to further reduce your tax burden.

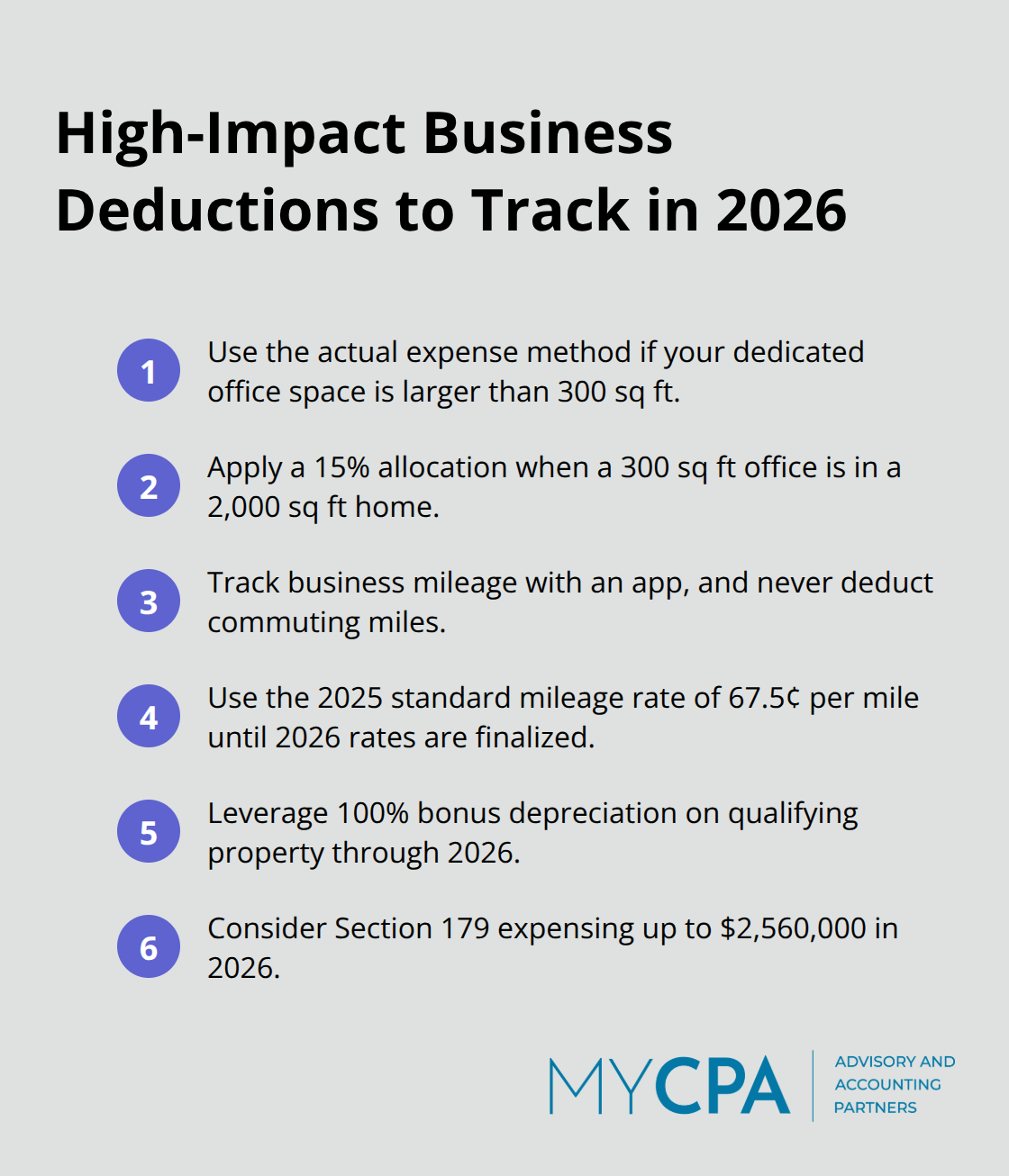

Home office deductions remain one of the most underutilized tax breaks available to self-employed professionals and remote workers. The IRS allows two methods: the simplified approach at $5 per square foot (capped at 300 square feet, or $1,500 annually) or the actual expense method where you deduct a percentage of your home’s mortgage interest, property taxes, utilities, insurance, and repairs based on the office’s square footage relative to your total home size. The actual expense method almost always wins for anyone with a dedicated office space larger than 300 square feet. If your home is 2,000 square feet and your office occupies 300 square feet, you deduct 15% of all qualifying home expenses. For someone with a $12,000 annual mortgage interest, $3,000 in property taxes, $2,000 in utilities, and $1,500 in homeowner’s insurance, that 15% allocation equals $2,850 in deductions versus the $1,500 simplified cap.

Document your home’s square footage and office dimensions now, photograph your dedicated workspace, and maintain records of all home-related expenses throughout 2026. The IRS scrutinizes home office claims, so consistency matters more than aggressiveness.

Vehicle and equipment expenses demand equally rigorous documentation because the IRS knows these categories invite overstatement. For vehicle deductions, track actual mileage for business purposes using a log or app like MileIQ or Stride Health. The standard mileage rate for 2026 hasn’t been finalized yet, but 2025 rates sit at 67.5 cents per mile for business use, and you cannot deduct commuting miles.

Alternatively, use the actual expense method by tracking fuel, maintenance, insurance, and depreciation on a percentage basis matching business mileage to total mileage. Most people find mileage tracking simpler and more defensible during audits.

Equipment purchases trigger depreciation rules that require attention. Bonus depreciation allows you to deduct 100% of qualifying property like machinery, computers, and vehicles in the year purchased, but this benefit phases down after 2026. Real estate components like parking lots depreciate over 15 years while building structures depreciate over 39 years, so work with a tax professional to properly allocate costs if you’ve made property improvements.

Section 179 expensing lets you immediately deduct up to $2,560,000 in qualifying equipment purchases in 2026, though the rules contain strict limitations on total annual purchases. Keep detailed purchase receipts, maintain an equipment log with acquisition dates and business-use percentages, and categorize expenses by type because misclassification invites audit risk and lost deductions.

These three expense categories-home office, vehicles, and equipment-typically generate the largest deductions for business owners, but only when documentation proves legitimate business use and proper allocation. Sloppy records cost more in missed deductions and audit exposure than the time spent organizing them correctly. Once you’ve maximized these business expense deductions, the next critical lever involves timing your income and deductions strategically across tax years to further reduce your overall tax burden.

Income timing and strategic deductions represent your second-order tax lever after maximizing retirement accounts and business expenses. The fundamental principle is straightforward: pull deductions into high-income years and push income into lower-income years when your tax bracket permits it. This requires planning by November at the latest, before year-end decisions lock in your 2026 tax position.

If you expect significantly higher income in 2026 than 2027, accelerate discretionary business expenses like equipment purchases, professional development, or maintenance projects into 2026 to offset that peak year. A $50,000 deduction saves $12,000 in taxes at the 24% bracket but only $9,250 at the 18.5% bracket for someone in a lower-income year, making the $2,750 difference worth the administrative effort of timing. The IRS allows this timing flexibility for cash-basis taxpayers, which includes most self-employed professionals and small business owners.

Conversely, if you know 2027 will be a lower-income year due to sabbatical, business transition, or planned reduced hours, defer invoicing clients or project completions into 2027 when your marginal tax rate will be lower. This strategy works particularly well for service-based businesses where you control when you complete and bill projects. The key is documenting your intent and executing the deferral consistently-the IRS scrutinizes sudden income shifts, so maintain clear records of why you deferred revenue.

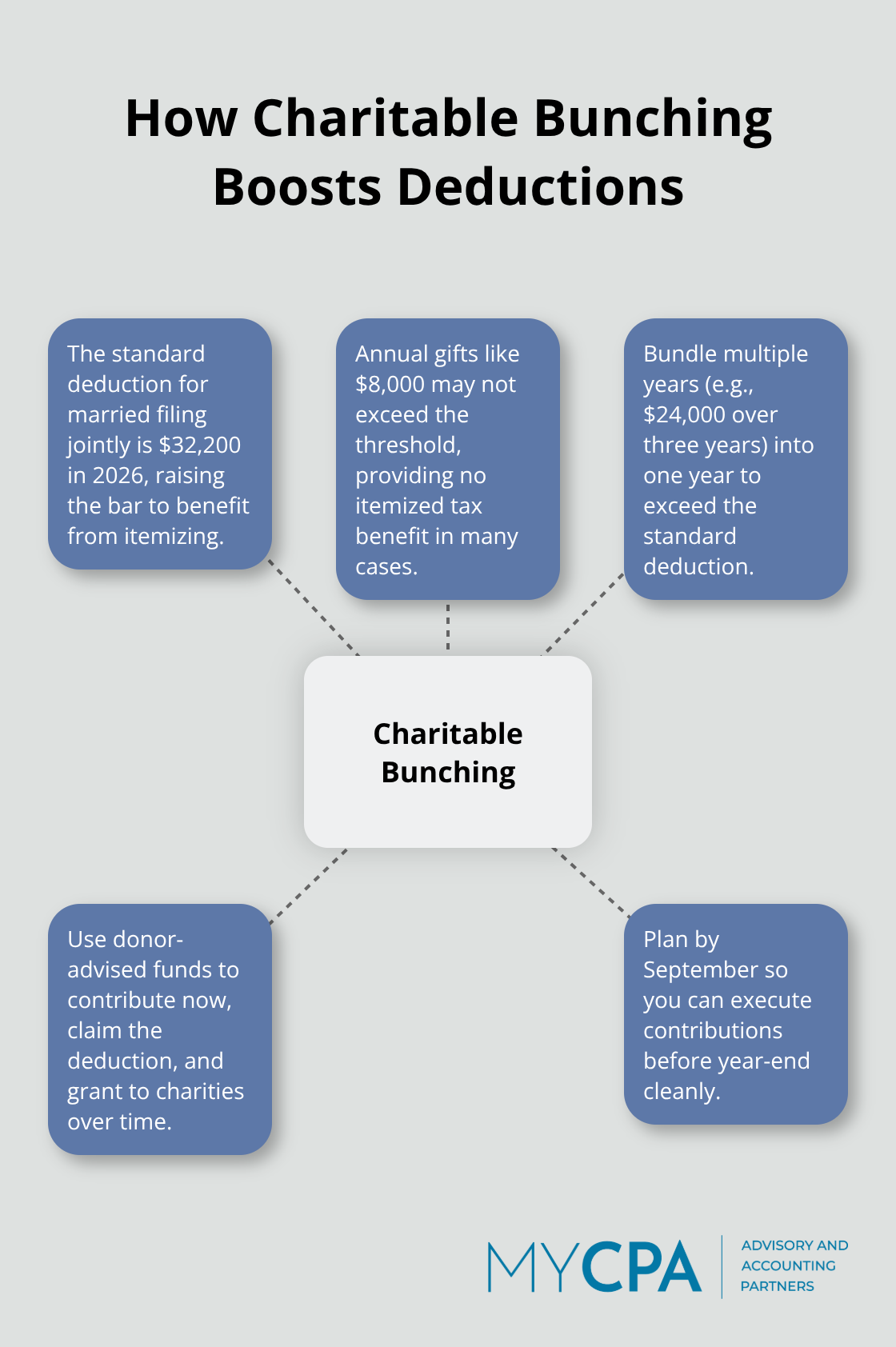

Charitable donations have become more complex under 2026 tax rules, which impose stricter itemization thresholds for high earners. The standard deduction for married filing jointly reaches $32,200 in 2026, meaning you must exceed this threshold to benefit from itemizing deductions. If you donate $8,000 annually, you’ll never reach the itemization threshold and lose all charitable deduction value.

Instead, use a charitable giving bunching strategy where you group multiple years of deductions into a single year to surpass the standard deduction. If you planned to donate $24,000 over three years, donate the full $24,000 in year one to exceed the standard deduction, then take the standard deduction in years two and three. This strategy works even better with donor-advised funds, which allow you to contribute a lump sum, claim an immediate deduction, and distribute funds to charities over subsequent years.

For 2026, the annual gift exclusion remains $19,000 per recipient, so you can front-load 529 college savings accounts with multiple years of contributions using this exclusion without triggering gift tax. This approach combines education planning with tax efficiency-you reduce your taxable estate while funding qualified education expenses that grow tax-free. Model your charitable strategy by September so you can execute bunching decisions before December and capture the full deduction benefit.

The strategies outlined above form a complete framework for minimizing taxes legally in 2026. Maximizing retirement contributions and health savings accounts reduces your taxable income immediately, while documenting business expenses like home office deductions, vehicle tracking, and equipment depreciation captures legitimate write-offs that most business owners leave on the table. Timing your income and deductions strategically across tax years amplifies these benefits further, especially when you bunch charitable giving into high-deduction years or defer revenue to lower-bracket periods.

Tax planning only works when you execute it consistently and document it thoroughly. The IRS expects to see organized records, and audits happen when deductions appear aggressive or unsupported (this is where professional guidance becomes invaluable). We at My CPA Advisory and Accounting Partners work with business owners and self-employed professionals to build personalized tax strategies that align with your specific income, business structure, and financial goals.

Review your 2026 income projection by September, identify which retirement accounts and business expenses apply to your situation, and model your charitable giving strategy before year-end. If you’re uncertain about depreciation rules, entity structure optimization, or whether you’re capturing all available deductions, that uncertainty costs money. Visit My CPA Advisory and Accounting Partners to discuss how we can help you keep more of what you earn while staying fully compliant with tax law.

Privacy Policy | Terms & Conditions | Powered by Cajabra