Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Starting a business means juggling countless responsibilities, and tax compliance often gets pushed to the back burner. The reality is that startups face serious penalties and cash flow problems when they miss tax deadlines or mishandle their obligations.

We at My CPA Advisory and Accounting Partners have seen firsthand how early planning prevents costly mistakes. This playbook walks you through the tax requirements you need to meet, the pitfalls to avoid, and how to build a tax-efficient foundation from day one.

Federal income tax filings, payroll deposits, and state compliance requirements form the backbone of startup tax obligations. Miss these deadlines and you face penalties that compound quickly. The IRS charges a 5% penalty per month for late tax return filing, capped at 25%, plus interest on any unpaid balance. Payroll tax penalties are even steeper: fail to deposit withheld taxes on time and you’ll owe 2% to 15% depending on how late the deposit is. Startups drain cash reserves trying to catch up after falling behind, which is entirely preventable with a clear calendar and automated workflows.

Your business structure determines your federal filing deadline. C-corporations file Form 1120 by March 15 following the tax year; S-corporations and partnerships file Form 1120-S and Form 1065 by the same date. Sole proprietors and single-member LLCs report income on Schedule C attached to their personal Form 1040, due April 15. Set up your accounting system now to capture every transaction, rather than scrambling in January. If you expect to owe $1,000 or more in federal income tax for 2026, you must make quarterly estimated tax payments on April 15, June 15, and September 15 to avoid penalties. Many founders underestimate their tax liability and skip these payments, only to face a bill they can’t absorb. Calculate your estimated tax using IRS Publication 505 or work with a tax advisor to optimize your tax planning strategy and get the amount right from the start.

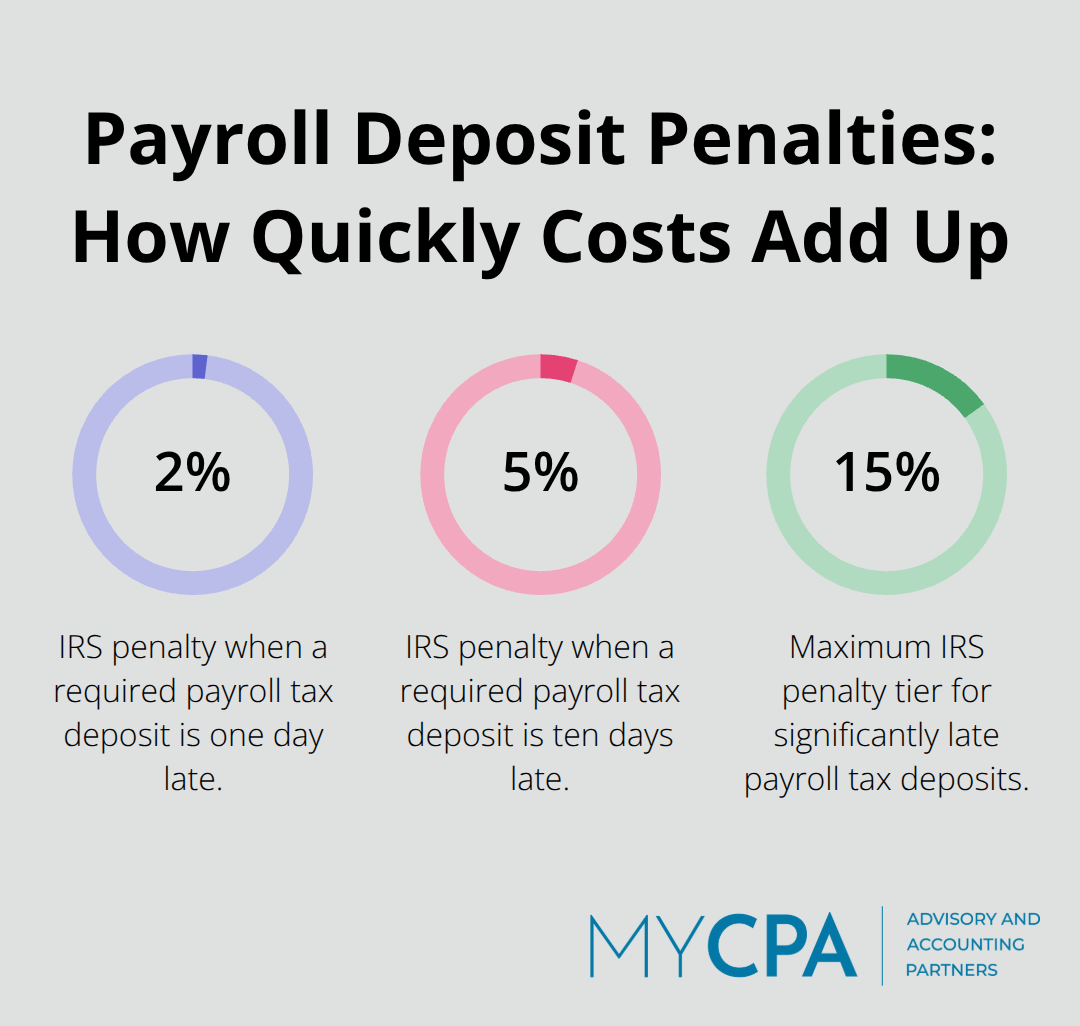

The moment you hire your first employee, payroll tax obligations kick in immediately. You must withhold federal income tax, Social Security tax at 6.2%, and Medicare tax at 1.45% from each paycheck. You also owe matching amounts for Social Security and Medicare, plus federal unemployment tax at 0.6% on the first $7,000 of each employee’s annual wages. These withheld and employer taxes must be deposited electronically through the Electronic Federal Tax Payment System (EFTPS) or Direct Pay on a strict schedule: semi-weekly or monthly depending on the size of your payroll. Deposit one day late and the IRS assesses a 2% penalty; ten days late and it jumps to 5%. Startups treat payroll tax deposits as optional during cash-flow crunches, which is a serious mistake. Set up automatic transfers on your deposit due dates so there’s no room for error. If you’re unsure of your deposit frequency, the IRS will tell you based on your tax liability reported on Form 941, which you file quarterly. State payroll tax requirements vary widely: some states piggyback federal withholding rules while others impose additional state income tax or disability insurance deductions. Know your state’s rules before your first payday.

Sales tax rules depend on your business model and location. If you sell physical products or taxable services in a state, you must register for a sales tax permit in that state and any others where you have economic nexus. As of 2026, economic nexus thresholds range from $100,000 to $500,000 in annual sales depending on the state; once you cross that threshold, you’re required to collect and remit sales tax even without a physical location. Collect the tax from customers at the point of sale, then remit it monthly, quarterly, or annually based on your state’s schedule. Failure to register can result in back-tax assessments plus penalties and interest. If you operate in multiple states, track which ones require registration and set calendar reminders for each filing deadline-missing one state’s deadline doesn’t excuse missing another. Some startups use sales tax automation software to calculate tax at checkout and file returns automatically, which reduces manual errors significantly.

These deadlines form the foundation of your tax obligations, but they’re only the start. The next section covers the mistakes that trip up most founders and how to sidestep them before they damage your business.

Misclassifying workers as independent contractors ranks among the costliest mistakes we see. The IRS uses a three-part test to determine worker status: behavioral control, financial control, and relationship of the parties. Many founders treat anyone without a W-2 as a contractor to avoid payroll taxes, but the IRS disagrees in most cases. If you hire someone to work on your product full-time, provide them equipment, set their schedule, and control their methods, they’re an employee regardless of what you call them.

Misclassification penalties run 1.5% of unpaid wages plus 40% of unpaid payroll taxes, and the IRS audits this aggressively. One startup faced a $180,000 back-tax bill when audited after classifying five full-time engineers as contractors. The safer path: if someone works full-time on your core business, make them an employee from day one. If you genuinely need contractors, keep them project-based, let them use their own tools, and document the independent nature of the relationship clearly.

Failing to track deductible expenses costs startups real money because they simply don’t claim what they’re entitled to. The IRS allows startups to deduct ordinary and necessary business expenses, yet most founders spend on items they could write off and never capture them in their books. Software subscriptions, cloud hosting, office supplies, professional fees, and even home office space are deductible if properly documented.

The challenge isn’t what’s deductible but proving it when the IRS asks. Keep receipts and categorize expenses in real time using accounting software rather than dumping credit card statements into a shoebox in March. If you use a single credit card for personal and business purchases, separate them immediately into your accounting system so your books reflect only business activity. This separation prevents audit risk and makes tax planning far less painful.

Missing quarterly estimated tax payments happens because founders don’t forecast their tax liability accurately. Calculate your expected profit for 2026, apply the combined federal and state tax rate, divide by four, and make those quarterly payments on April 15, June 15, September 15, and January 15. Underpayment penalties compound: miss one quarter and the IRS charges interest from the original due date, not when you finally pay.

Set up a separate savings account now and transfer one-quarter of your estimated tax liability each month so the money sits there when payments are due. This removes the temptation to spend tax money on operations and keeps cash flow predictable. Automation matters here-set up automatic transfers on your payment due dates so nothing falls through the cracks.

These mistakes are preventable with systems in place before they happen. The next section shows you how to build a tax-efficient financial foundation that catches these issues before they become problems.

Your business structure shapes everything about your tax life, and most founders select incorrectly because they don’t understand the long-term consequences. A Delaware C-corporation works best for VC-backed startups because it signals legitimacy to investors, simplifies equity grants, and preserves Qualified Small Business Stock (QSBS) eligibility, which can exclude part of your gains from capital gains tax if you hold the stock for at least five years and meet other requirements. An S-corporation or LLC might feel simpler at formation, but switching structures later during fundraising costs thousands in legal fees and creates diligence friction that investors hate. The IRS Section 1202 QSBS rules require you to track stock issuance records from day one, so selecting the right structure and documenting it properly now saves you from scrambling at exit. If you’re bootstrapping without investor plans, an S-corporation election on an LLC can reduce self-employment taxes significantly, but only if your payroll is set up correctly and your accountant files the election on time. Talk with a tax professional for 30 minutes before you file incorporation paperwork to prevent structural mistakes that cost far more to fix later.

Your accounting system must capture every transaction in real time, categorized correctly, so nothing falls through the cracks and your books reflect reality. Open a dedicated business bank account immediately and never deposit personal funds or withdraw for personal use, because commingling opens you to personal liability. Use accounting software like QuickBooks to record expenses the day they occur rather than waiting until tax season, because you’ll forget details and lose receipts if you delay. Connect your bank account directly to your accounting software so transactions import automatically and reconcile monthly to catch errors before they compound. Implement a monthly close process where you review income and expense categories, verify that everything is categorized correctly, and flag any suspicious transactions before they become audit problems. This discipline takes two to three hours monthly but saves you from the chaos of scrambling in March when your accountant asks for records you don’t have.

Treat monthly bookkeeping as non-negotiable infrastructure, not a task to squeeze in when cash flow permits. If your books are disorganized, tax professionals spend billable hours just cleaning them up, which means you pay extra for the same advice you could have received from clean records. Monthly discipline prevents costly mistakes and positions your startup for smooth tax filings and audits. Start this habit now, before your business scales and records become impossible to untangle.

Tax compliance doesn’t have to derail your startup. The foundation you build now-clean bookkeeping, correct worker classification, timely estimated payments, and the right business structure-prevents the penalties and cash flow crises that sink early-stage companies. Startups that treat tax as infrastructure rather than an afterthought gain a competitive advantage because they avoid scrambling to fix problems in March or facing surprise audit bills that drain reserves.

The mistakes covered in this playbook are entirely preventable. Misclassifying workers, losing track of deductible expenses, and missing quarterly payments happen because systems aren’t in place, not because founders are careless. A 30-minute conversation with a tax advisor before you incorporate, elect an S-corporation status, or issue founder equity prevents costly mistakes that are expensive to unwind later (and we at My CPA Advisory and Accounting Partners specialize in exactly these structural decisions for early-stage companies).

Open a dedicated business bank account this week, set up accounting software, and contact My CPA Advisory and Accounting Partners to review your business structure and build a tax-efficient foundation for startups tax compliance in 2026.

Privacy Policy | Terms & Conditions | Powered by Cajabra