Legally Reduce Taxes: Practical Pathways To Tax Savings

Legally reduce taxes with proven strategies. Explore deductions, credits, retirement plans & entity structures to minimize what you owe the IRS.

Most startups don’t fail because they lack customers or revenue. They fail because they run out of cash.

At My CPA Advisory and Accounting Partners, we’ve seen this pattern repeatedly. Startups with strong sales still collapse when cash flow dries up. That’s why proactive cash flow advisory isn’t optional-it’s survival.

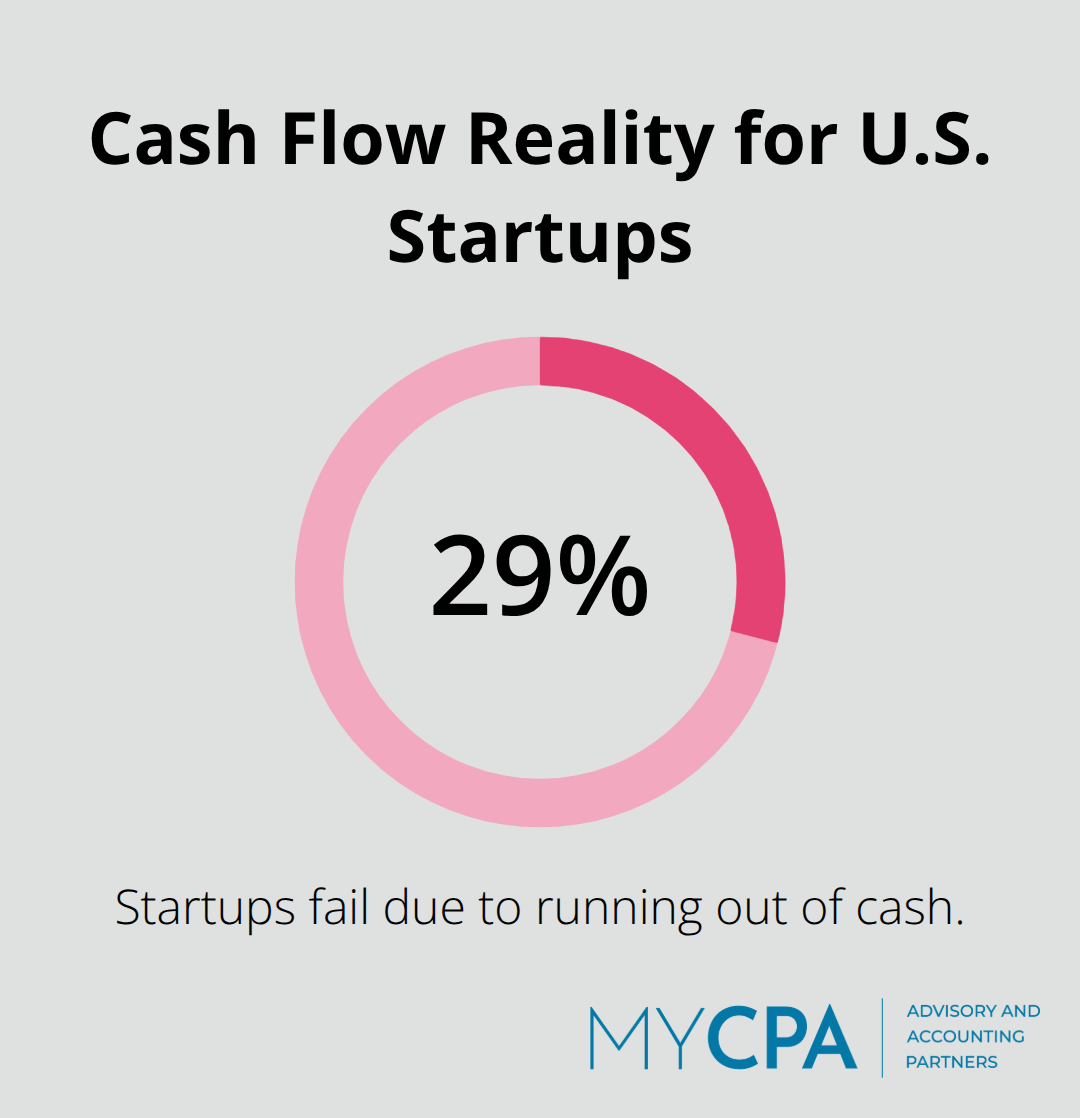

About 29% of startups fail because they run out of cash, according to failure analysis data. This statistic matters because it reveals a hard truth: revenue and cash are not the same thing. A startup can book $100,000 in sales this month and still face a payroll crisis next week if customers haven’t paid their invoices.

Cash flow is the oxygen your business needs to survive, and without it, growth stops immediately. The timing of money moving in and out of your bank account determines whether you can keep your team employed, pay suppliers on time, and invest in the opportunities that move your business forward. Many startups with strong sales pipelines collapse because they never treated cash flow as a strategic priority until it became a crisis.

Late customer payments represent the number one cash flow problem for startups. Even if your contract says net-30, customers often pay net-45 or net-60, and some never follow their own payment terms at all. This matters because a single customer delay can force you to cover payroll from your reserves or, worse, delay paying your own vendors. The solution is aggressive: implement a payment incentive program where customers who pay within 7 days receive a 2% discount. This converts future cash into immediate cash and shifts the financial burden away from your startup. Track which customers consistently pay late and either renegotiate terms upfront or stop extending credit to them. Many startups treat payment timing as a minor administrative issue when it should be a revenue conversation.

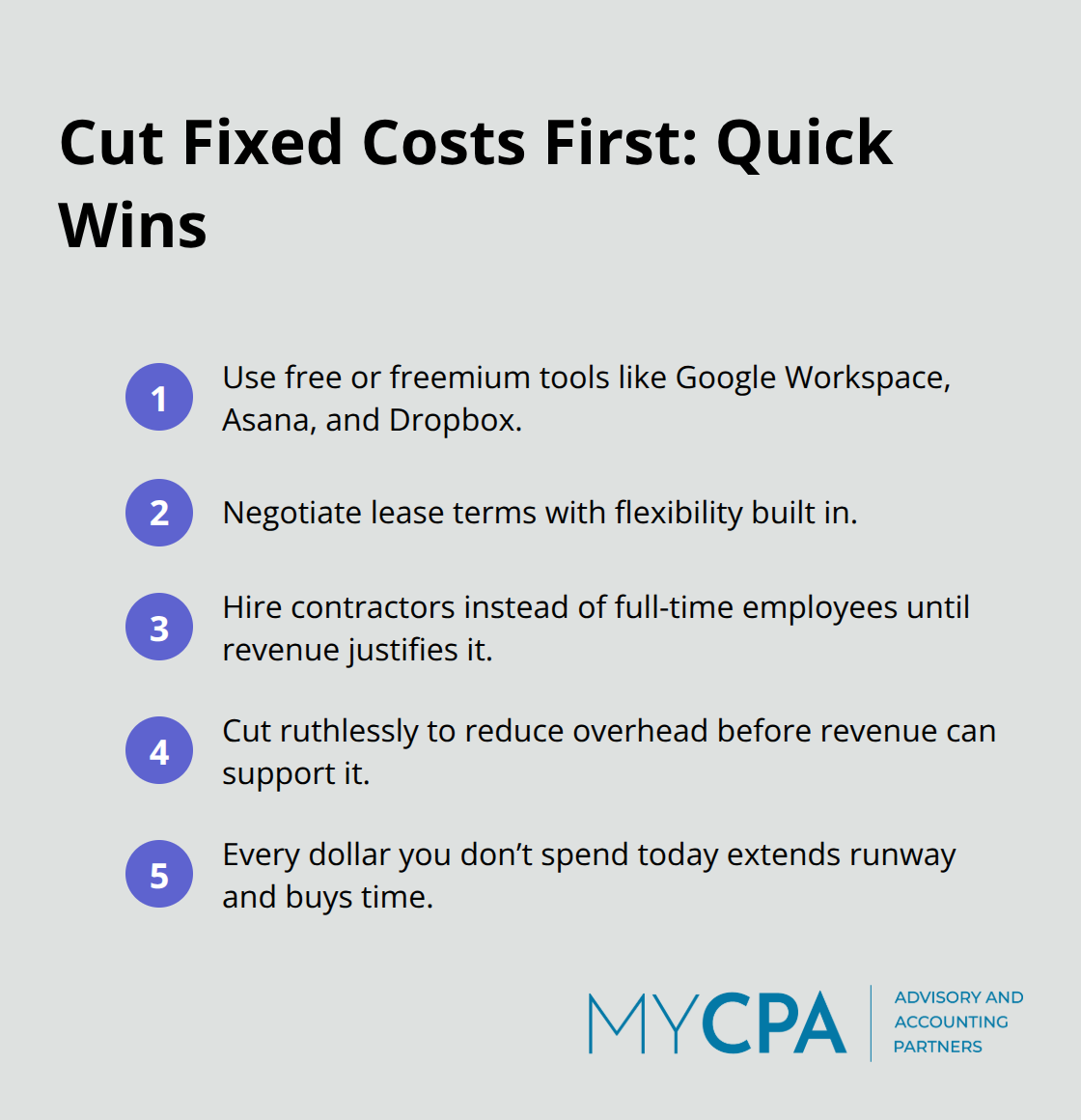

Startups hemorrhage cash on fixed expenses that don’t scale with revenue. Software subscriptions, office space, payroll, and infrastructure costs stay constant whether you close deals or not. A founder might spend $50,000 per month on fixed costs but only close $40,000 in deals, creating a monthly cash burn that shrinks runway every single week. The hard truth is that many startups maintain too much overhead before they’ve proven revenue can support it. Cut ruthlessly: use free or freemium tools like Google Workspace, Asana, and Dropbox instead of paid alternatives. Negotiate lease terms with flexibility built in.

Hire contractors instead of full-time employees until revenue justifies the commitment. Every dollar you don’t spend today buys you more time to find product-market fit, and time is your most valuable asset when cash is tight.

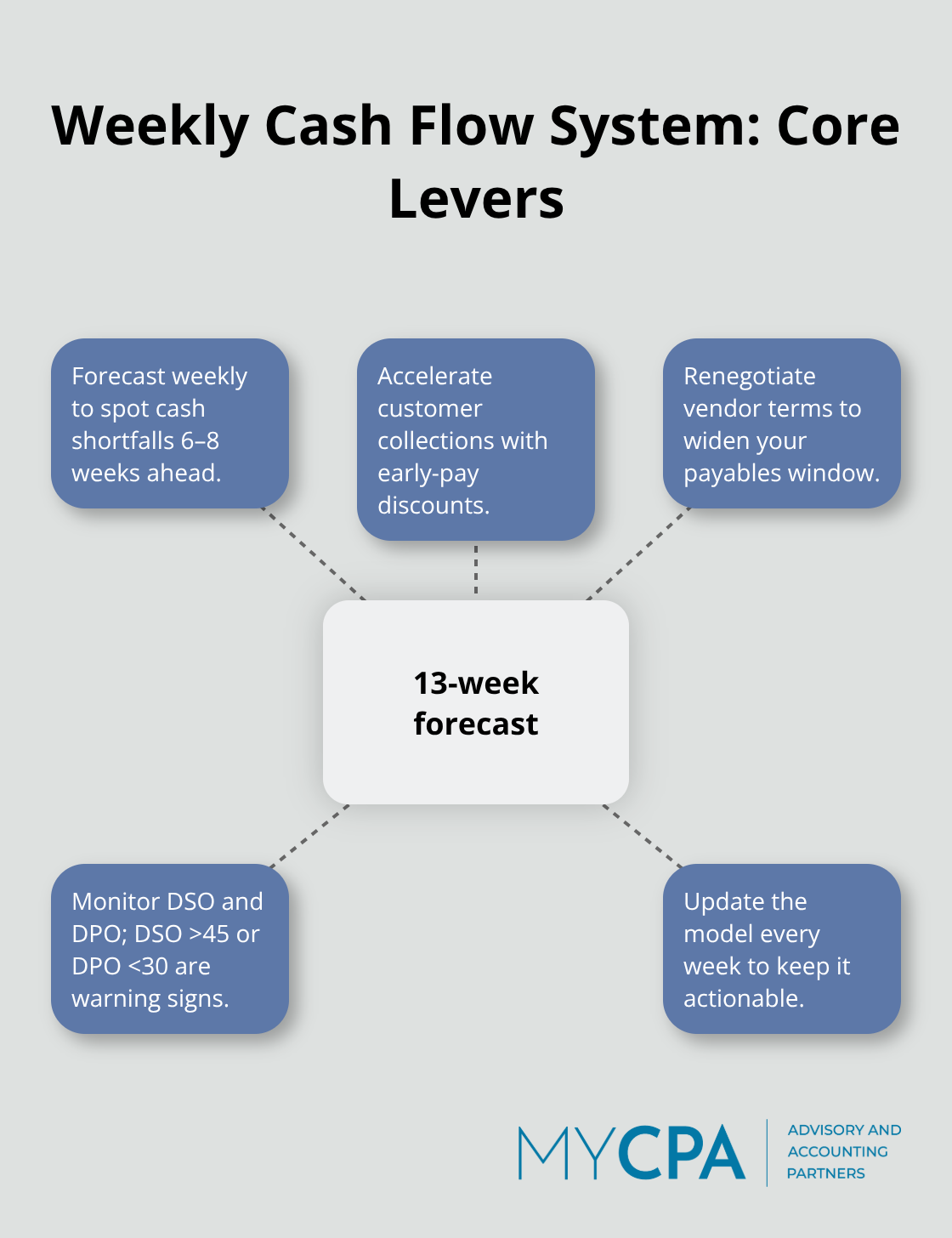

Most startups operate on monthly financial statements, which means they discover cash problems weeks after the damage occurs. A 13-week cash flow forecast gives you a detailed look at projected inflows and outflows, helping you keep your finances organized and plan for future funding. This approach tracks cash receipts and disbursements week by week, not month by month, so you spot shortfalls 6 to 8 weeks in advance. You can then adjust spending, accelerate collections, or plan a fundraising round before payroll becomes impossible. Weekly updates keep your forecast accurate and actionable, transforming cash management from a reactive scramble into a disciplined strategic practice.

Startups make their first critical cash flow mistake when they extend payment terms to customers without modeling the cash impact. A founder agrees to net-45 terms to win a deal, then net-60 for the next customer, and suddenly the company’s cash conversion cycle stretches to 90 days. That means you fund customer operations for three months before seeing a dime. If you spend $50,000 monthly on operations but customers don’t pay for 90 days, you need $150,000 in cash reserves just to survive the float. Most startups lack that buffer.

The solution demands brutal honesty: calculate your cash conversion cycle before you accept any payment terms. If a customer demands net-60 but your runway only supports net-30, either charge a premium for extended terms or walk away. The deal isn’t worth it if it kills your business.

The second mistake is overestimating revenue projections in your cash flow model. Founders often assume customers will pay on time, close at the expected rate, or adopt the product faster than reality allows. But even with better tools, startups routinely assume best-case scenarios instead of building contingency into their models.

A startup that projects $200,000 in monthly revenue but actually closes $140,000 faces a sudden $60,000 monthly shortfall. The fix is conservative modeling: use historical data from your actual customers, not industry benchmarks. If you’ve closed three deals averaging 45-day sales cycles, don’t assume the fourth will close in 30 days. Add a 20–30% buffer to your expense forecasts and reduce revenue projections by 15–20% from your sales pipeline estimates. This isn’t pessimism; it’s survival math.

The third mistake is ignoring seasonal fluctuations and customer payment timing. Many businesses experience predictable revenue swings-retail peaks in Q4, construction slows in winter, professional services may have summer slowdowns. If you don’t forecast these patterns, you’ll be caught off-guard when cash dries up in slow months.

Map out the last 24 months of your revenue and identify the troughs. Then set aside cash reserves during peak months to cover the valleys. Seasonal awareness transforms cash flow from a monthly guessing game into a disciplined practice where you prepare for the next downturn. This foundation positions you to implement the practical strategies that actually move the needle on your cash position.

The gap between startups that survive and those that fail often comes down to one practice: weekly cash flow forecasting. Not monthly forecasting, not quarterly planning, but a detailed week-by-week view of exactly when money moves in and out of your bank account. A 13-week forecast gives you 6 to 8 weeks of visibility into cash shortfalls before they become emergencies. This window is long enough to adjust spending, accelerate customer collections, or plan a fundraising round before payroll becomes impossible.

The mechanics are straightforward: start with your current bank balance, project weekly customer payments based on historical data (not optimistic assumptions), list every disbursement by category, and calculate the net cash position each week. Many founders skip this because they think monthly accounting is sufficient, but monthly reporting is a rear-view mirror. A customer who promises payment net-30 might actually pay on day 45, and that 15-day gap could trigger a payroll crisis if you’re not watching week by week.

Update your forecast every single week, replacing the oldest week with a new one seven days out. This rolling approach keeps your model current and forces you to confront reality instead of stale projections. The tools don’t matter at first-Google Sheets works fine. What matters is the discipline of updating it consistently and acting on what it tells you.

The second lever is accelerating customer payments, and this requires abandoning the idea that payment terms are non-negotiable. Offer a 2% discount to customers who pay within 7 days instead of waiting 30. For a customer paying $10,000, that’s $200 in discount cost to convert future cash into immediate cash. The math is brutal: if your startup spends $50,000 monthly and operates with a 3-month runway, you have $150,000 in the bank. A customer delay from net-30 to net-60 consumes $50,000 of that runway. A 2% discount that pulls payment forward by three weeks is a bargain.

Simultaneously, tighten vendor payment terms in the opposite direction. Most startups pay vendors net-30 automatically, which means you’re funding their operations. Renegotiate to net-60 where possible, and delay non-critical payments to day 45 or 50. This isn’t dishonest if you’re transparent about your timeline-most vendors will accept extended terms to keep your business. The goal is to widen the gap between when you pay out and when you collect in, creating a natural cash reserve. If customers pay you in 45 days and you pay vendors in 60 days, that 15-day spread becomes working capital you can deploy elsewhere.

Track your Days Sales Outstanding and Days Payable Outstanding to optimize your cash flow effectively. If DSO climbs above 45 days, your collection process is broken and needs immediate attention. If DPO falls below 30 days, you’re leaving cash on the table by paying too fast.

Cash flow management demands weekly attention and constant adjustment, not a one-time project that you complete and forget. The startups that survive treat their cash position like a vital sign, checking it regularly and responding immediately when something looks wrong. A 13-week forecast becomes stale within days without updates, and a spending plan that worked last month may not work this month if customer payments shift or unexpected expenses arise.

Proactive cash flow advisory prevents the financial crises that kill otherwise healthy businesses. When you forecast week by week, accelerate customer collections, and negotiate vendor terms strategically, you transform cash management from a reactive scramble into a disciplined strategic practice. Investors trust founders who demonstrate they understand their cash position and act on it, which often determines whether you raise capital on favorable terms or survival terms.

We at My CPA Advisory and Accounting Partners understand that managing cash flow while building a business overwhelms most founders. Our team helps startups implement the systems and discipline needed to transform cash flow into a competitive advantage through accurate accounting, business advisory, and proactive financial planning.

Privacy Policy | Terms & Conditions | Powered by Cajabra