Tax Planning for Corporations: Maximizing Corporate Efficiency

Maximize corporate tax efficiency with proven strategies, deductions, and entity structures for better results.

Most corporations leave money on the table every year through missed deductions and inefficient tax strategies. We at My CPA Advisory and Accounting Partners have seen firsthand how tax planning for corporations can reduce your tax burden by thousands of dollars.

The right approach combines understanding your tax liabilities with strategic planning across entity structure, timing, and investments. This guide walks you through proven methods to maximize your corporate efficiency.

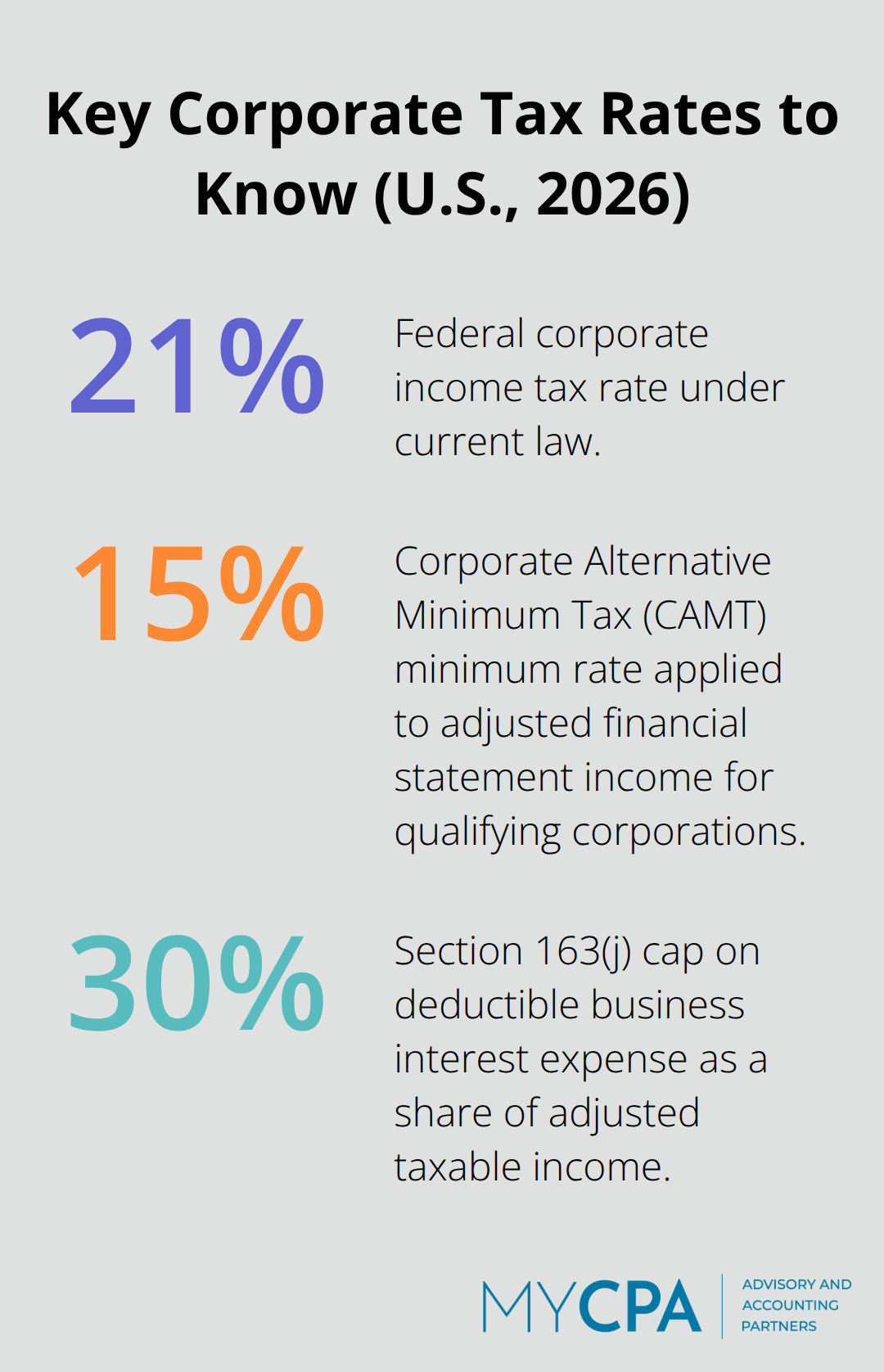

The federal corporate tax rate sits at 21 percent under current law, but that number masks the real cost of taxation. When you factor in state and local taxes, most corporations face an effective rate between 24 and 30 percent. For a company earning $1 million in taxable income, that translates to $240,000 to $300,000 in annual tax liability.

Most businesses treat taxes as a compliance obligation rather than a strategic decision point. Corporations that operate this way systematically miss thousands in deductions simply because no one connects operational decisions to tax outcomes throughout the year.

The Corporate Alternative Minimum Tax, or CAMT, adds another layer of complexity for larger firms with significant financial statement income. This tax requires calculations under both the regular tax system and a 15 percent minimum tax to determine which applies. Your tax bill depends on adjusted financial statement income, not just taxable income, making real-time visibility into accounting methods essential.

Most corporations systematically miss deductions that sit right in front of them. Section 179 allows immediate deductions for qualifying equipment and software purchases in 2026, yet many companies depreciate assets over years instead of claiming the full deduction upfront.

Bonus depreciation at 100 percent for qualified property placed in service after January 19, 2025 provides another powerful tool that requires intentional asset-purchase timing. These two mechanisms work together to accelerate deductions and improve near-term cash flow when you plan asset purchases strategically.

Interest expense limitations under Section 163(j) cap deductions at 30 percent of adjusted taxable income, but smaller businesses with average gross receipts under $31 million retain full deductions. Your business structure and size directly affect available deductions, making this calculation essential during planning.

Research and development costs represent perhaps the most overlooked opportunity, with the federal R&D credit providing substantial savings for companies investing in software development, engineering, or product innovation. Documentation matters here-the IRS requires contemporaneous records showing which activities qualify, and many companies lose credits simply because they failed to maintain proper support.

Retirement plan contributions offer dual benefits: they reduce taxable income while attracting and retaining talent, with 2026 contribution limits reaching approximately $69,000 for SEP IRAs and over $30,000 for solo 401(k) plans including catch-up provisions.

State tax conformity creates hidden exposure as well, since not all states follow federal bonus depreciation rules, potentially creating unexpected state-level liabilities that offset federal savings. Understanding these state-level differences prevents costly surprises and ensures your tax strategy works across all jurisdictions where you operate.

With these deduction and credit opportunities in mind, the next step involves structuring your entity and timing your income strategically to capture maximum tax efficiency.

Your choice of business structure determines far more than liability protection-it fundamentally affects how much tax you pay annually. A C corporation, S corporation, partnership, and LLC each carry different tax consequences, and the wrong structure can cost tens of thousands of dollars per year. The federal corporate tax rate holds at 21 percent, but pass-through entities like S corporations and partnerships allow income to pass through to owners at individual rates, which can range from 10 to 37 percent depending on personal circumstances.

For many mid-sized businesses earning $500,000 to $5 million annually, an S corporation structure with reasonable W-2 wages for owner-employees often delivers superior results compared to a C corporation or LLC taxed as a C corporation. The IRS scrutinizes S corporation salary decisions closely, so your wages must reflect reasonable compensation for the work performed-but distributions beyond that salary face only self-employment tax on a portion of income, creating legitimate savings. A manufacturing company generating $2 million in taxable income might pay $420,000 in federal tax as a C corporation but only $280,000 as an S corporation with properly structured owner compensation, assuming similar state tax treatment. The catch is that restructuring mid-year creates complications, so this decision belongs in your annual planning process rather than as an afterthought. C corporations make sense primarily when you plan to retain earnings for reinvestment, operate internationally, or pursue acquisition strategies where buyer preferences favor corporate structures.

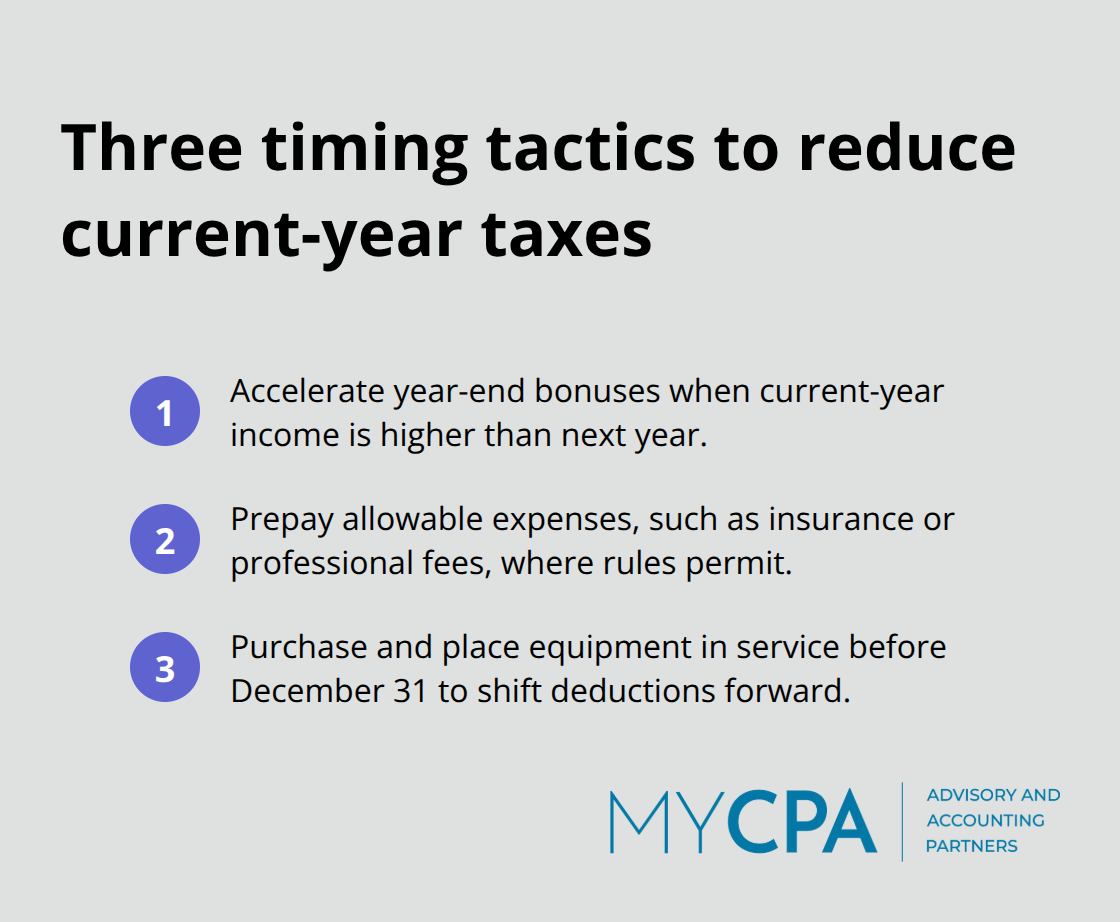

Income and expense timing represents your second major lever for tax efficiency, and most corporations miss opportunities here through inaction rather than deliberate strategy. You accelerate deductible expenses into the current year when you anticipate lower income next year, but deferring income into future years requires careful cash-flow management since you still owe the money. Bonus accruals to employees, prepaid professional fees, and strategic equipment purchases all shift deductions forward when the timing works in your favor. A professional services firm projecting $800,000 in profit this year but only $400,000 next year should consider accelerating year-end bonuses, paying insurance premiums in advance where allowed, and purchasing office equipment before December 31 to reduce current-year taxable income.

The Section 179 deduction limit for 2026 sits at approximately $1.3 million with a $3.22 million phase-out threshold, meaning businesses that time major asset purchases strategically capture full deductions in a single year rather than spreading depreciation across multiple years. You can claim the entire deduction upfront instead of depreciating equipment over years, which accelerates cash-flow benefits significantly when you plan purchases with tax outcomes in mind.

Capital gains management works differently than ordinary deductions-long-term capital gains face preferential rates, but the timing of asset sales matters considerably. You can hold qualified small business stock for five or more years under Section 1202 to achieve 100 percent exclusion from taxable income, compared to 50 percent for three-year holdings, making the holding period a genuine planning variable. Real estate investors should track property basis carefully and consider 1031 exchanges to defer gains indefinitely when trading up to larger properties, though this strategy requires precise timing and qualified intermediary involvement.

Your entity structure and timing decisions form the foundation for tax efficiency, but capturing available credits and deductions requires a more detailed examination of your specific operations and investments.

Retirement plan contributions deliver the most straightforward tax reduction available to corporations, yet most businesses treat them as afterthoughts rather than strategic levers. A 2026 SEP IRA allows contributions up to 25 percent of compensation or $72,000 annually, whichever is less, while a solo 401(k) with catch-up provisions reaches over $30,000 for owner-employees. You can establish these plans as late as December 31 and still claim contributions for the current tax year on your return, making year-end planning far more flexible than many business owners realize. This means a $500,000 profit projection in November can shift dramatically lower through strategic retirement contributions made before year-end, directly reducing both federal and state taxable income. Matching contributions for employees amplify the deduction further while improving retention in competitive labor markets where 73 percent of workers prioritize retirement benefits in job decisions according to the Employee Benefit Research Institute.

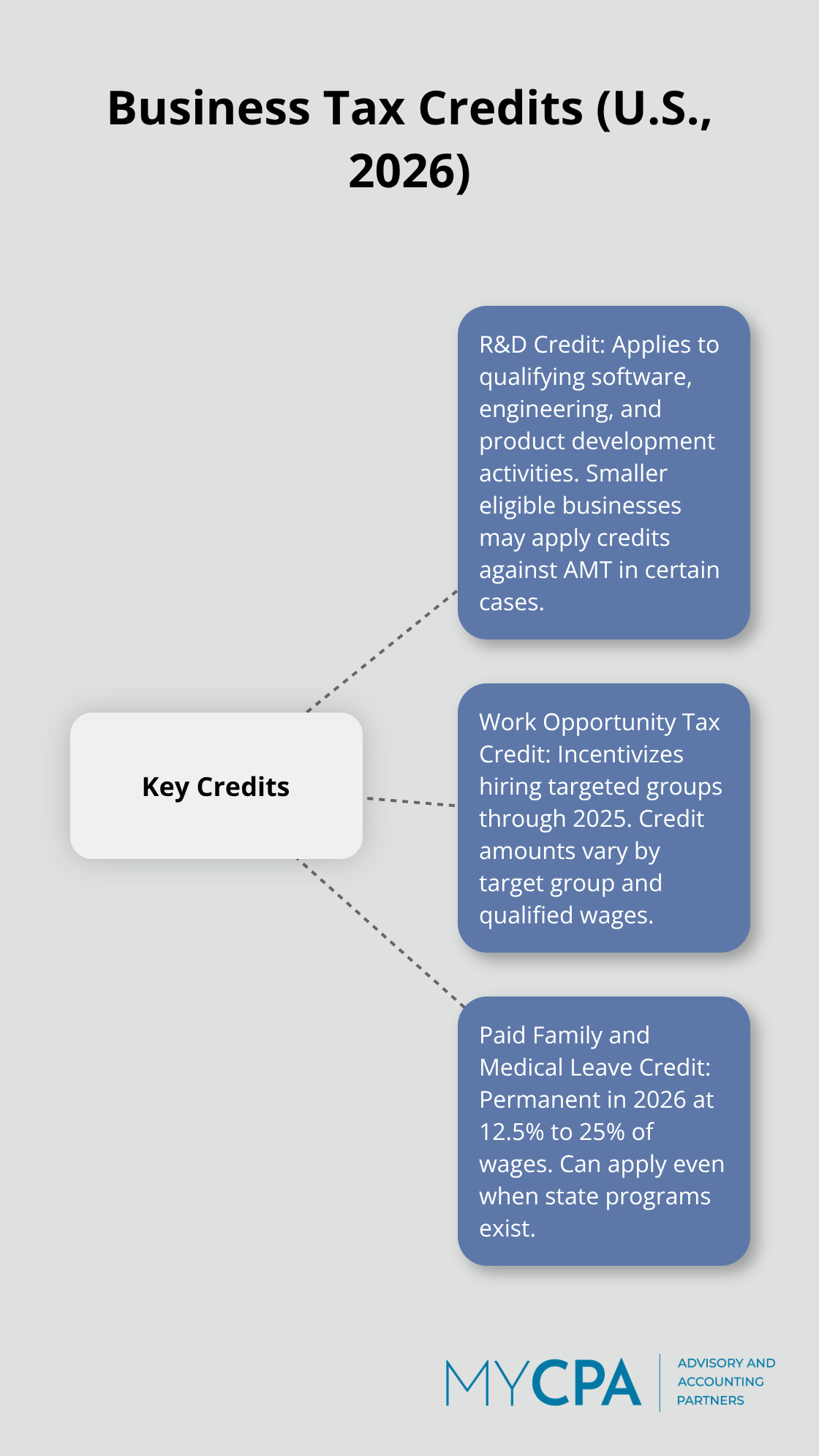

Tax credits function differently than deductions and demand separate attention in your planning process. The Research and Development credit under Section 41 applies to companies investing in software development, engineering, or product innovation, with eligible smaller businesses able to claim credits against AMT liability in certain cases. The Work Opportunity Tax Credit provides substantial savings for hiring targeted groups through 2025, with credit percentages varying by group and wage levels. The Paid Family and Medical Leave credit becomes permanent in 2026 at 12.5 to 25 percent of wages, applying even where state programs exist, making this a genuine opportunity for forward-thinking employers.

Documentation matters intensely here: the IRS requires contemporaneous records proving which activities qualify, and many companies forfeit thousands annually through inadequate support.

Net Operating Losses created in the current year can be carried forward indefinitely under post-2017 rules, though they face an 80 percent limitation in carryforward years, meaning a $500,000 loss offsets only $400,000 of income in future profitable years. Pre-2018 losses follow different rules with 100 percent offset capability, creating a genuine planning variable if you operate across multiple tax years. Form 4466 enables quick refunds of overpaid estimated taxes when a loss year precedes profitable years, accelerating cash recovery rather than waiting for amended returns. The interaction between regular tax, CAMT, and these carryforwards requires modeling multiple scenarios to ensure your planning optimizes after-tax cash flow across years rather than solving for single-year tax rates.

Tax professionals who maintain updated technical knowledge on CAMT thresholds, BEAT implications at 10.5 percent permanently from 2026, and international provisions prevent costly errors that self-directed planning frequently produces. We at My CPA Advisory and Accounting Partners understand how these mechanisms interact and can help you streamline your tax planning process that accounts for multiple tax systems operating simultaneously. The complexity of modern corporate taxation makes professional guidance not optional but essential for businesses serious about tax efficiency.

Tax planning for corporations works best when you treat it as an ongoing strategic function rather than a once-yearly compliance exercise. The strategies outlined here-from entity structure optimization to retirement plan contributions to credit documentation-compound over time and create measurable improvements in after-tax cash flow. A company that implements these approaches systematically can reduce effective tax rates by several percentage points, translating to tens of thousands of dollars annually depending on size and industry.

The real opportunity emerges when you connect operational decisions to tax outcomes throughout the year. When your finance team, operations, and tax advisors communicate regularly, you capture deductions that would otherwise disappear and time major purchases to maximize depreciation benefits. Most corporations miss these opportunities simply because no one owns the planning process, and tax planning for corporations remains fragmented across departments rather than integrated into strategic decision-making.

Start your tax planning process by auditing your current tax profile, establishing planning priorities based on your specific situation, and scheduling a strategy discussion with a qualified tax professional before year-end. We at My CPA Advisory and Accounting Partners help corporations implement tax planning strategies that align with broader business goals, and our tax services and accounting expertise work together to minimize tax liabilities while strengthening your financial foundation.

Privacy Policy | Terms & Conditions | Powered by Cajabra