Strategic Financial Advisory: Aligning Numbers With Vision

Align your financial strategy with business vision using strategic financial advisory to drive sustainable growth and profitability.

Most business owners leave thousands of dollars on the table each year simply because they don’t know where to look. At My CPA Advisory and Accounting Partners, we’ve seen firsthand how strategic planning and attention to detail can transform your tax situation.

Minimizing tax liabilities legally isn’t about cutting corners-it’s about working smarter with what the tax code already allows. This guide walks you through the deductions, strategies, and mistakes that matter most.

Most business owners operate under incomplete information about what the tax code allows them to deduct. The difference between a mediocre tax return and a strategic one often comes down to knowing exactly which expenses qualify and how to document them properly.

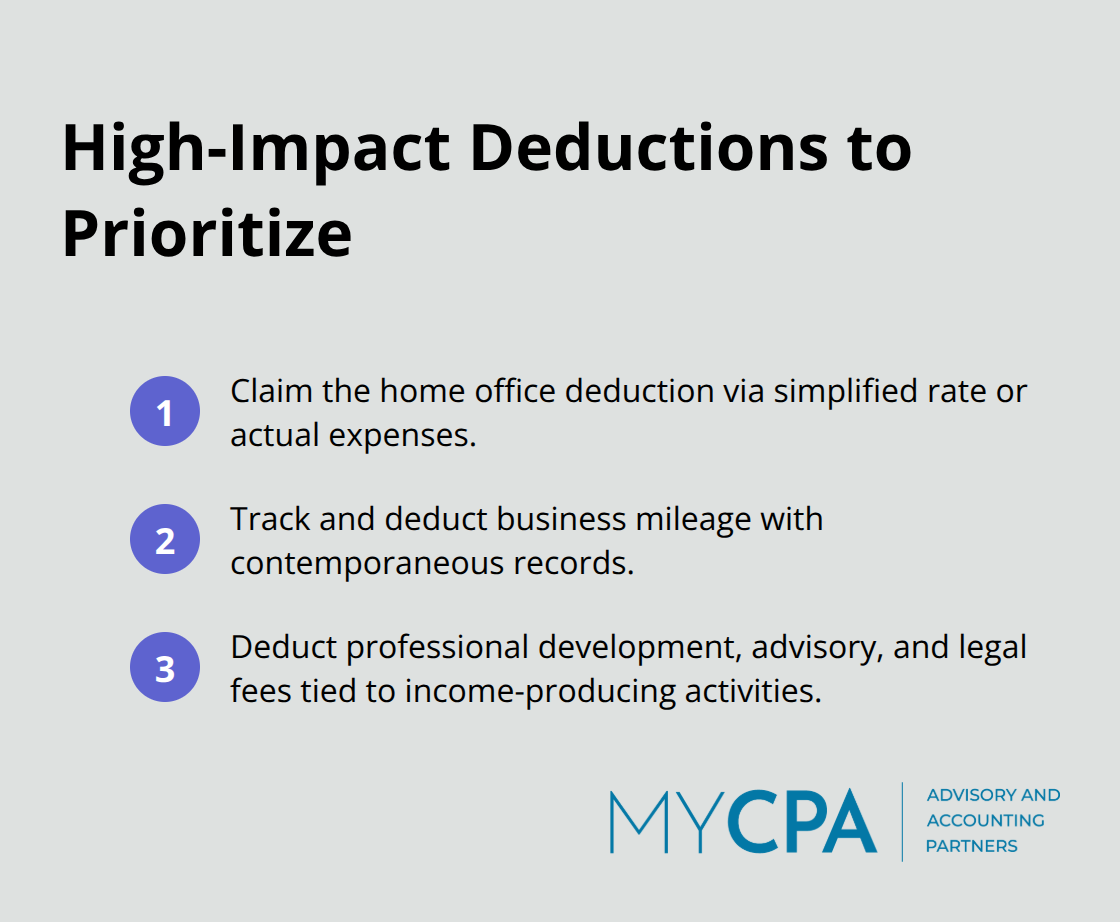

Home office deductions alone can save thousands annually if you structure them correctly. The IRS allows you to deduct either actual expenses with detailed records or use the simplified method at $5 per square foot (maximum 300 square feet). For someone working from a dedicated office space, the itemized approach frequently exceeds the simplified calculation.

Vehicle expenses present another substantial opportunity most practitioners overlook. You can deduct business mileage in 2026, but only if you maintain contemporaneous records. Apps like MileIQ or QuickBooks Self-Employed create real-time logs that satisfy IRS requirements far better than reconstructing mileage from memory.

Professional development costs that directly support your income-producing activities qualify as fully deductible expenses. This includes CLE credits, industry conferences, online certifications, coaching, and specialized software subscriptions. Advisory and legal fees paid to CPAs, lawyers, and consultants for tax planning or business strategy qualify as deductions and typically generate returns far exceeding their cost. Many business owners fail to capitalize on these because they view them as discretionary rather than strategic investments.

Self-employed professionals have access to retirement vehicles that W-2 employees don’t. A Solo 401(k) allows you to contribute up to $24,500 in employee deferrals plus an additional $8,000 catch-up contribution if you’re age 50 or older in 2026, with the ability to add employer contributions up to 25% of compensation. A SEP IRA caps contributions at 25% of net self-employment income with a $70,000 maximum in 2026. For high earners exceeding $200,000 in net income, these accounts function as genuine tax shelters.

A defined benefit plan offers even more aggressive deductions for those with consistent income, though it requires actuarial calculations and ongoing administration. Health Savings Accounts provide triple tax advantages: contributions are deductible, growth is tax-free, and withdrawals for qualified medical expenses avoid taxation entirely. In 2026, individual coverage limits rise to $4,400 with a $1,000 catch-up for those 55 and older.

Maxing all available retirement accounts can reduce taxable income by $50,000 to $100,000 annually depending on your business structure and income level. The strategic timing of these contributions matters significantly. You can make SEP IRA contributions until your tax return filing deadline plus extensions, allowing you to fund the account after year-end if cash flow permits. This flexibility lets you optimize contributions based on actual year-end income rather than estimates made in January.

The real power emerges when you combine multiple deduction strategies with proper documentation and timing. Your next move involves understanding how to sequence these deductions throughout the year-a topic that separates tax-aware business owners from those who scramble at year-end.

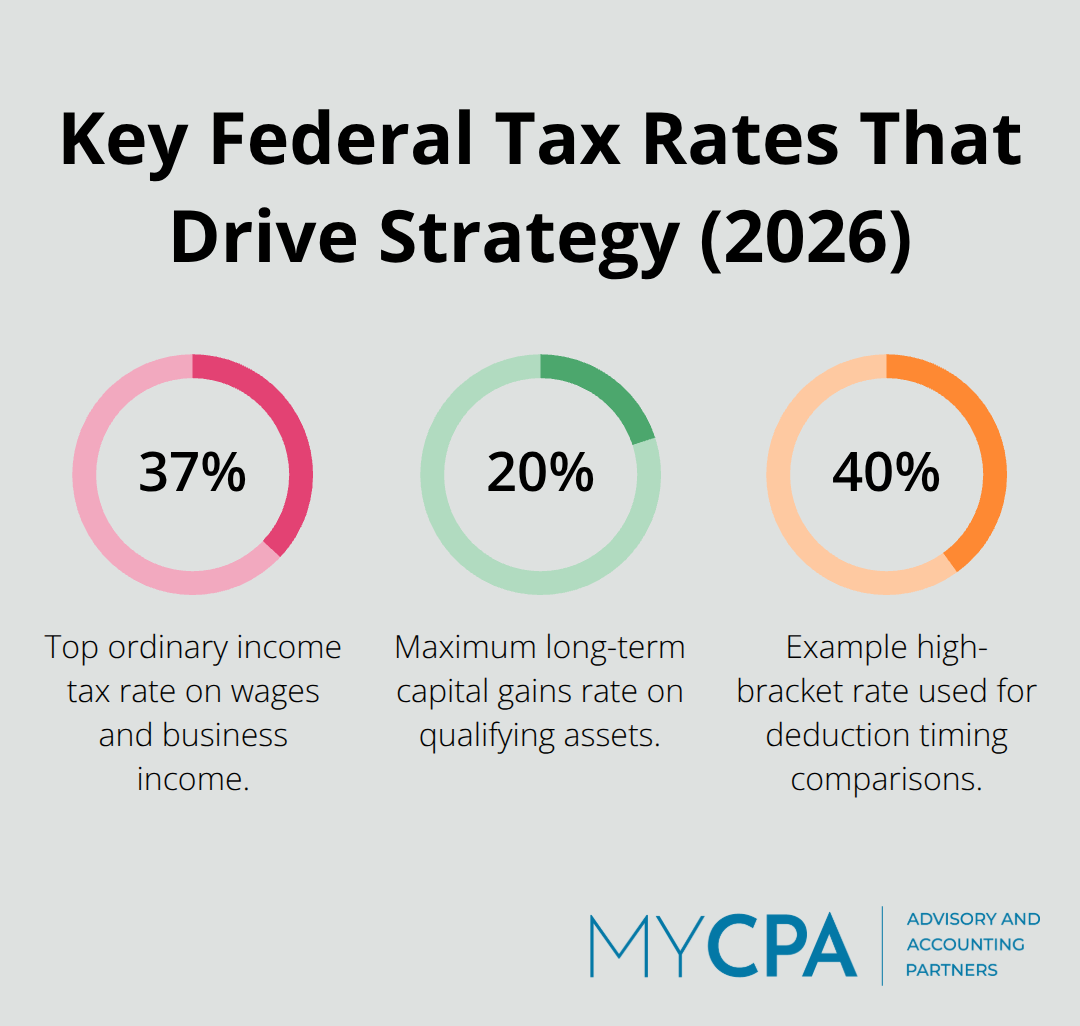

Most business owners treat tax planning as a December crisis rather than a continuous process, and that mistake costs them dearly. The difference between a reactive tax return and a proactive tax strategy is thousands of dollars in unnecessary liability. Strategic tax planning means making deliberate moves throughout the year based on your actual income trajectory, not guesses made in January. The IRS taxes ordinary income at rates up to 37 percent while long-term capital gains cap at 20 percent, creating powerful incentives to structure income strategically. If you earn over $200,000 as a self-employed professional, your marginal tax rate likely exceeds 40 percent when combined with self-employment tax and potential net investment income tax. That gap between your marginal rate and favorable capital gains rates represents genuine opportunity if you plan ahead.

Timing matters because once December arrives, your income for the year is largely locked in. The owner earning $180,000 in October faces a different tax picture than one earning that amount in June, yet most don’t adjust their strategy accordingly. Deferring substantial income into the following year keeps you in a lower bracket, but you must set this up before year-end through legitimate means like delaying client invoicing, restructuring service delivery dates, or adjusting bonus timing if you’ve incorporated. Conversely, accelerate deductions into high-income years when the math favors it. If you know Q4 will be unusually profitable, front-load professional development costs, equipment purchases, or advisory fees in that same year rather than spreading them across both years. A $10,000 deduction saves you $4,000 in a 40-percent-bracket year but only $2,400 in a 24-percent year. That $1,600 difference compounds across multiple deductions and transforms your bottom line.

Entity structure influences how much tax you actually owe, yet most practitioners never revisit this decision after initial setup. An S-Corporation election fundamentally changes how income flows through your return. If you operate as a sole proprietor earning $250,000 annually, you pay self-employment tax on net earnings at 15.3 percent. That’s roughly $37,000 in self-employment tax alone. An S-Corp requires you to pay yourself reasonable W-2 wages subject to payroll tax, then distribute remaining profits as dividends that avoid self-employment tax entirely. The IRS requires S-Corporation reasonable compensation documentation, meaning you can’t pay yourself $50,000 in wages and take $200,000 in distributions. But if your reasonable wage is $120,000 and you distribute $130,000 in profits, you’ve eliminated self-employment tax on that $130,000 distribution. For someone in the 37-percent bracket, avoiding 15.3-percent self-employment tax on $100,000 in distributions saves $15,300 annually. This strategy only makes sense above roughly $200,000 in net income because S-Corp compliance costs, payroll processing, and additional tax return complexity cost $2,000 to $4,000 yearly. Below that threshold, the savings don’t justify the overhead.

Quarterly estimated tax payments separate successful business owners from those facing April surprises. The IRS requires estimated payments in four installments if you expect to owe $1,000 or more in taxes. Missing quarterly deadlines triggers penalties that compound throughout the year. The penalty rate in 2026 is the federal short-term rate plus 3 percent, currently around 8 to 9 percent annually. Many owners underpay estimates because they base calculations on prior-year income without adjusting for current growth. If you earned $100,000 last year and made $150,000 this year, quarterly estimates based on last year’s return will leave you short by approximately $15,000 come April. Recalculate estimates quarterly as your income emerges to prevent this problem entirely. Spreadsheet tracking of monthly revenue and expenses takes thirty minutes monthly but reveals whether you’re on pace to exceed prior-year income and signals when to increase estimated payments. The alternative is writing a check for $15,000 or more in April while simultaneously owing penalties for underpayment.

Strategic planning throughout the year transforms tax season from a financial emergency into a manageable administrative process with predictable outcomes. Yet knowing which strategies apply to your specific situation requires understanding how common mistakes derail even well-intentioned owners-mistakes that the next section addresses directly.

The gap between knowing the right strategies and executing them correctly separates owners who cut their tax bills in half from those who leave money on the table despite reading guides like this one. We at My CPA Advisory and Accounting Partners see the same preventable mistakes repeatedly, and they share a common thread: poor record-keeping infrastructure combined with commingled finances that make deductions impossible to substantiate. The IRS doesn’t care about your intentions or your memory of business expenses. It cares about documentation. When the IRS audits a Schedule C return, the agency disallows deductions at a rate exceeding 30 percent for sole proprietors because owners lack contemporaneous records proving expenses were legitimate business costs. This isn’t theoretical risk.

The National Society of Accountants reports that inadequate recordkeeping ranks among the top three reasons businesses face audit adjustments and penalties.

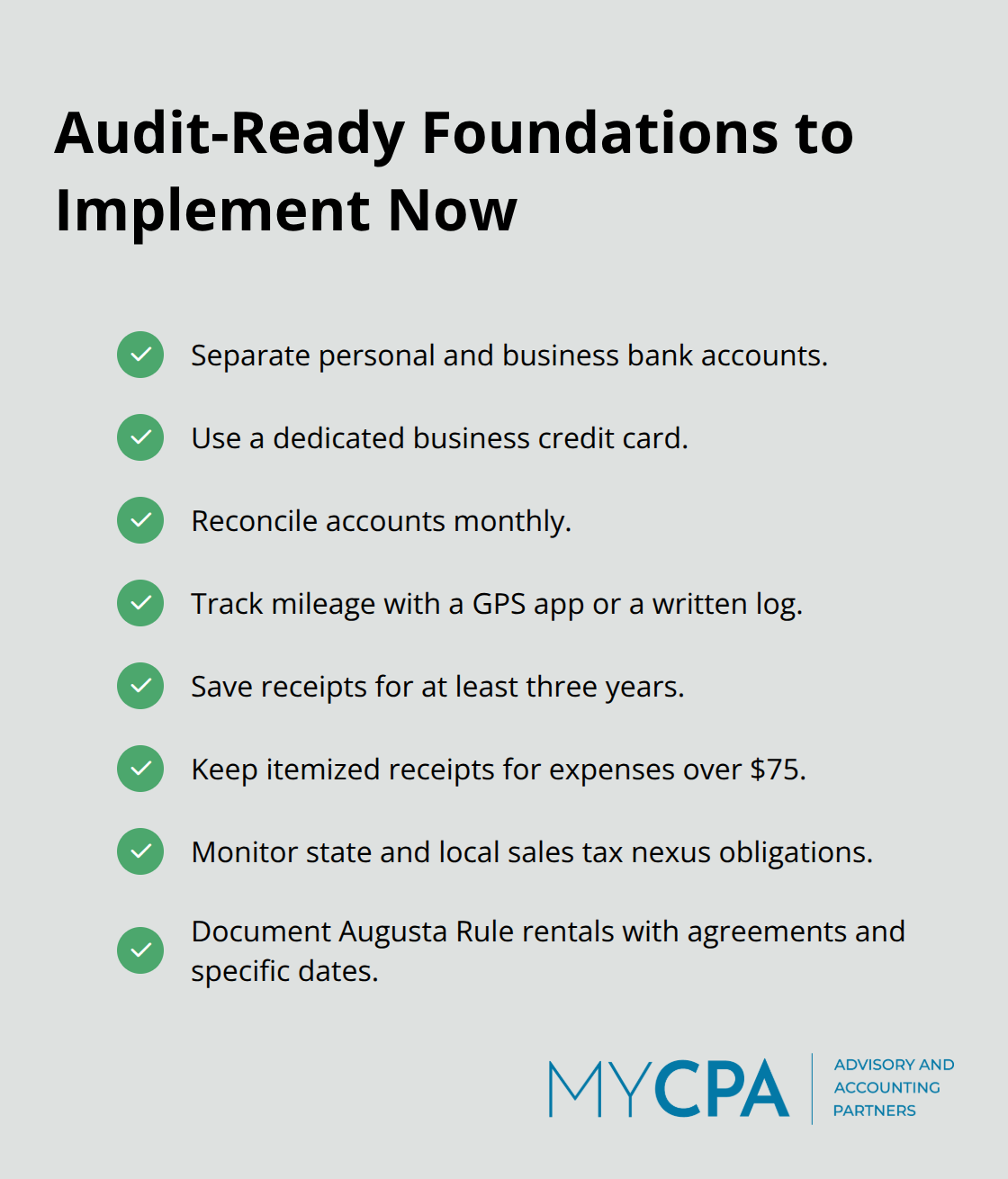

Your personal and business finances must live in completely separate bank accounts and credit cards. If you withdraw cash for a client dinner and then use the same cash to pay your electric bill, that expense becomes virtually impossible to defend during an audit. The IRS assumes commingled funds are personal until proven otherwise, and the burden of proof falls on you. Many owners operate under the false belief that they can reconstruct expenses later or that mental notes suffice. This approach fails consistently.

Set up a dedicated business checking account before your first dollar of income arrives. Use a business credit card exclusively for deductible expenses. Reconcile both monthly. This single discipline transforms your audit defense from nonexistent to bulletproof while simultaneously making tax preparation faster and cheaper.

Mileage tracking presents a critical vulnerability because the IRS demands contemporaneous records created at or near the time you drive, not reconstructed months later. The standard mileage rate in 2026 remains substantial, and tracking business miles generates real deductions that reduce your tax liability dollar-for-dollar at your marginal rate. Yet most owners either skip mileage tracking entirely or attempt to estimate it in December, both approaches that fail audit scrutiny.

Apps like MileIQ automatically log trips using your phone’s GPS and cost roughly $5 monthly, creating an auditable record without manual effort. Alternatively, a simple notebook kept in your vehicle where you record the date, destination, business purpose, and miles driven satisfies IRS requirements completely. The difference between tracking mileage and ignoring it typically amounts to $3,000 to $8,000 annually depending on your practice area and driving volume.

Receipts for business expenses must remain in your possession for at least three years, though six years is safer for high-value items or if you claim depreciation. The IRS has specific receipt thresholds: for expenses under $75, you can rely on a credit card statement as proof, but for anything exceeding $75, you need an itemized receipt showing what you purchased. Many business owners photograph receipts with phone apps like Expensify, which automatically extracts transaction details and stores them digitally. This approach beats filing cabinets of paper because digital records survive office moves, water damage, and the simple passage of time.

State and local tax obligations represent a blind spot where owners hemorrhage money without realizing it. Sales tax nexus rules shifted dramatically since the Supreme Court’s Wayfair decision in 2018, which eliminated the physical presence requirement for sales tax collection. If you sell products or certain services across state lines, you likely owe sales tax in states where you have economic nexus, typically triggered at $100,000 to $500,000 in annual sales depending on the state.

Many service-based professionals wrongly assume sales tax doesn’t apply to them, but several states tax professional services including consulting, accounting, and legal work. Your state’s revenue department website publishes specific nexus thresholds and filing requirements, and ignorance carries penalties ranging from 5 percent to 25 percent of unpaid taxes plus interest compounding monthly.

The Augusta Rule under Section 280A(g) allows you to rent your home to your business for up to 14 days per year tax-free if you structure it correctly, but only if you’ve properly separated personal and business use. This strategy requires documented rental agreements and contemporaneous records proving business use on specific dates. Without this documentation, the IRS disallows the deduction entirely and potentially reclassifies personal expenses as business write-offs, triggering additional tax liability and penalties.

Knowledge alone never transforms your tax situation-execution does. The business owner who reads about S-Corp elections but never implements one gains nothing, and the practitioner who understands mileage deductions yet fails to track them leaves thousands unclaimed. The difference between a mediocre tax outcome and an exceptional one comes down to consistent action throughout the year combined with proper documentation that withstands IRS scrutiny.

Your immediate priority involves establishing the infrastructure that makes minimizing tax liabilities legally possible. Separate your personal and business finances completely, implement mileage tracking through an app or notebook, and retain receipts while reconciling accounts monthly. These foundational steps cost almost nothing but eliminate the audit vulnerabilities that destroy deductions and trigger penalties-without this infrastructure, even sophisticated tax strategies fail because you lack documentation to defend them.

Beyond these fundamentals, minimizing tax liabilities requires expertise that extends beyond what most business owners can manage alone. A single misstep on reasonable compensation documentation can trigger IRS penalties exceeding the entire tax savings your S-Corp election generated, and misunderstanding sales tax nexus can result in years of back taxes plus interest and penalties. Contact My CPA Advisory and Accounting Partners to explore how tailored financial services can transform your tax situation and provide the peace of mind that comes from knowing your strategy is optimized, documented, and defensible.

Privacy Policy | Terms & Conditions | Powered by Cajabra