Internal Controls Checklist for Solid Financial Health

Discover your internal controls checklist to strengthen financial health, prevent fraud, and maintain accurate records. Essential guide for business owners.

Weak internal controls cost businesses thousands in errors, fraud, and compliance violations every year. We at My CPA Advisory and Accounting Partners have seen firsthand how companies struggle without proper safeguards in place.

This internal controls checklist gives you a practical roadmap to strengthen your financial foundation. You’ll learn what controls matter most and how to fix the gaps that put your business at risk.

Internal controls are the specific procedures and policies your business puts in place to safeguard assets, maintain accurate financial records, and prevent fraud. They’re not theoretical concepts-they’re the daily operational rules that determine who can approve a purchase order, who reconciles the bank account, and who has access to your accounting software. Without them, your financial data becomes unreliable, your assets vulnerable, and your compliance standing questionable.

The connection between controls and financial accuracy is direct and measurable. When you separate duties-meaning one person doesn’t handle every step of a transaction-errors drop significantly because multiple eyes catch mistakes before they become problems.

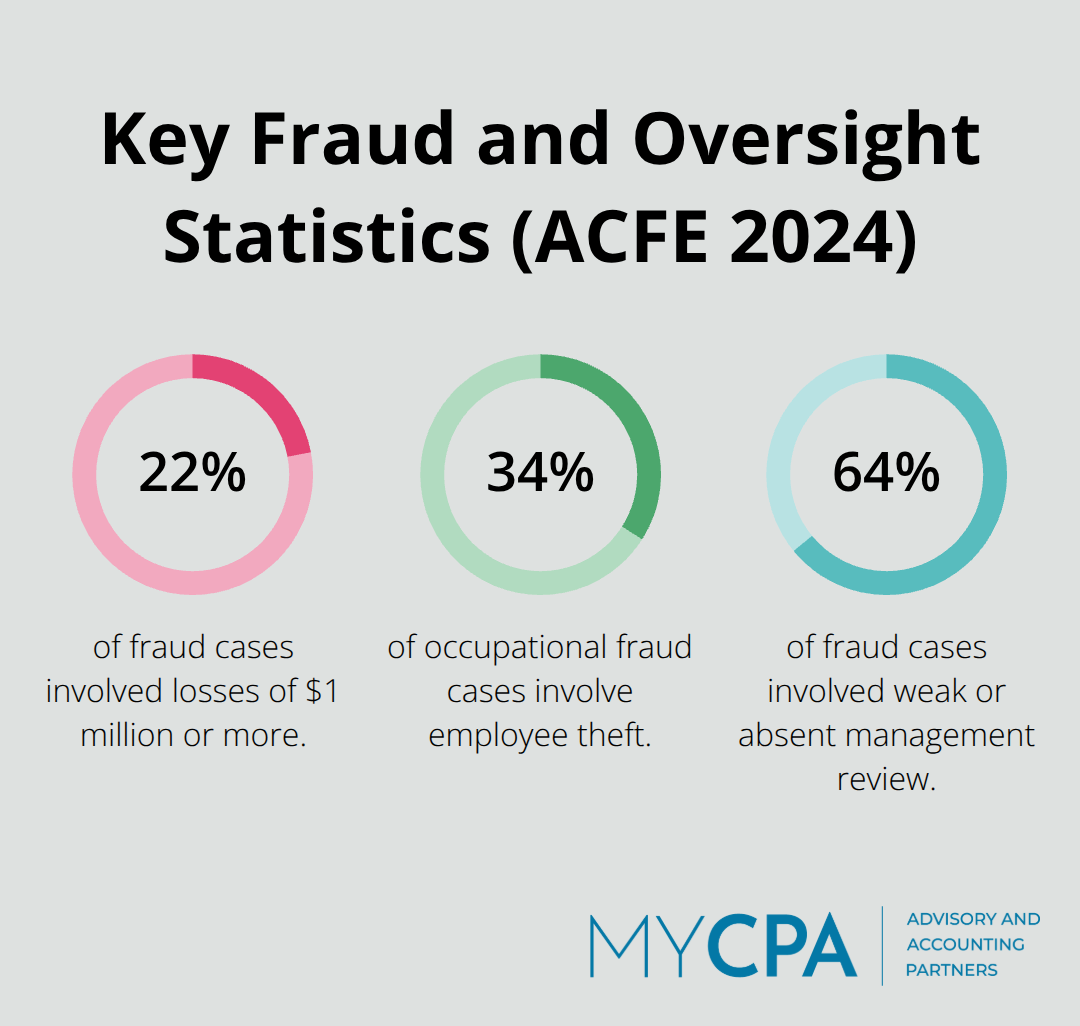

According to the 2024 ACFE Report, 22% of fraud cases involved losses of $1 million or more, with a median loss of $145,000.

That’s not just about preventing theft. It’s about catching billing errors, duplicate payments, inventory shrinkage, and accounting mistakes that bleed money from your bottom line every single month.

The impact of internal controls on business risk management goes far beyond compliance. When you implement formal authorization thresholds-say, requiring manager approval for expenses over $500-you create accountability at every transaction level. Your bank reconciliations become a monthly early-warning system that catches unauthorized wire transfers, fraudulent charges, or system errors before they compound.

Physical asset controls prevent inventory shrinkage, which retailers and restaurants face as a significant operational challenge. Documentation standards create an auditable trail that protects you during tax audits, customer disputes, and regulatory reviews.

Businesses that treat internal controls as operational infrastructure rather than compliance checkboxes consistently report lower error rates, faster financial close cycles, and stronger relationships with auditors and lenders. These stakeholders view control maturity as a sign of management competence and financial discipline. The specific vulnerabilities your business faces-whether cash-heavy operations or service-based companies-require different safeguards tailored to your actual risk profile. Understanding which controls matter most for your industry sets the foundation for the essential controls every business needs to implement.

Segregation of duties remains the single most effective fraud deterrent available to any business, yet most companies implement it poorly or not at all. The principle is straightforward: no single employee should handle every step of a financial transaction. One person receives inventory, another approves the invoice, a third processes payment. This separation forces collusion rather than allowing solo theft.

In restaurants where cash handling dominates operations, segregation of duties cuts fraud risk dramatically. The person who takes the order shouldn’t reconcile the cash drawer. The manager who authorizes refunds shouldn’t process them. The Association of Certified Fraud Examiners reports that 34% of occupational fraud cases involve employee theft-a statistic that underscores why this control matters.

When staffing is lean, rotate duties monthly or assign a trusted employee to cover one task while you perform random record audits as verification. Without this control, your business becomes vulnerable to the very fraud that costs companies thousands annually.

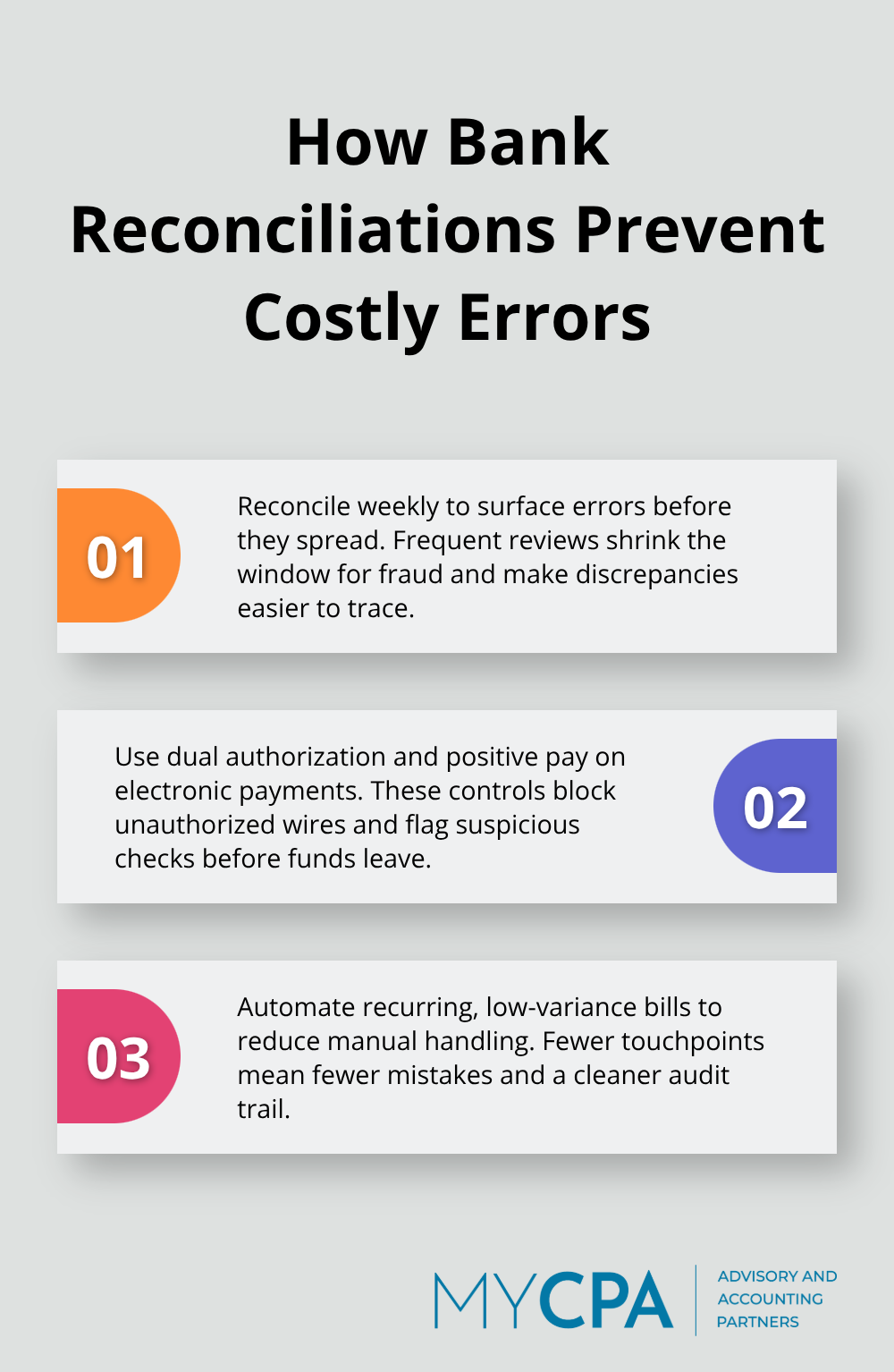

Bank reconciliations catch errors before they compound into serious problems, yet many business owners skip this step monthly or assign it inconsistently. Reconcile your business account weekly, not monthly. Match every deposit to your point-of-sale system or invoice records. Investigate discrepancies the same day they appear.

Electronic payments require dual authorization for wire transfers and positive pay protocols to prevent unauthorized transactions. Set up automatic recurring payments for utilities and fixed expenses rather than writing checks manually, which introduces more opportunities for error or fraud. This weekly discipline transforms your bank account from a black box into a transparent financial control that catches problems before they spread.

Physical asset controls demand monthly inventory counts, with liquor inventory tracked nightly in hospitality businesses. Compare actual counts to software predictions and investigate variances immediately. This hands-on approach prevents shrinkage from eroding your margins month after month.

Documentation standards create the audit trail that protects you during tax reviews and customer disputes. Every transaction needs a supporting document: invoice, receipt, bank statement, or contract. Specify retention periods in writing and enforce them. This documentation discipline transforms your accounting from a scattered collection of files into a coherent financial record that auditors trust and lenders respect.

These four controls work together to create a financial system that catches errors, prevents fraud, and produces reliable data. The next step involves identifying which weaknesses currently exist in your business and how to address them systematically.

Most businesses fail at internal controls not because they lack good intentions but because they skip the unglamorous work of approval documentation and access management. You implement segregation of duties, set up bank reconciliations, and think the job is done. Then a manager approves a $50,000 wire transfer without written authorization. An accounts payable clerk gains access to the general ledger and makes unauthorized adjustments. A vendor invoice gets paid twice because nobody verified it against the receiving record. These aren’t rare edge cases-they’re the daily operational gaps that turn control frameworks into expensive paperwork exercises.

The first breakdown happens when approval thresholds exist on paper but not in practice. You’ve defined that expenses over $500 need manager sign-off, yet employees submit reimbursements without receipts and managers rubber-stamp them during busy seasons. The Association of Certified Fraud Examiners found that 64% of fraud cases involved weak or absent management review, meaning your approval process either doesn’t function or nobody enforces it consistently.

Integrate approval workflows into your accounting software rather than relying on email chains. Set up automated exceptions that flag transactions exceeding thresholds and route them to the correct approver before payment processes. Require supporting documentation as a mandatory field in your system-no receipt, no approval code, no payment. Test your approval process quarterly by submitting fake transactions to confirm they actually get stopped.

The second breakdown involves documentation that exists but isn’t organized or retrievable. You keep invoices in a filing cabinet, email attachments scattered across inboxes, and bank statements in a folder labeled “2025 Bank.” When an auditor or tax examiner asks for proof that you verified a $25,000 contractor payment, you spend three hours searching. This disorganization costs time and creates audit risk because you can’t demonstrate control.

Establish a centralized document management system where every transaction has a supporting file linked to the accounting record. Create a simple filing structure: vendor name, invoice date, amount. Specify that original invoices stay in one location, digital scans in another, and retention periods in writing. Perform a three-way match for every vendor payment-compare the purchase order to the invoice to the goods receipt-and document that you completed this match in your system. Financial reporting accuracy depends on precise data practices that give you confidence in your records.

The third breakdown occurs when monitoring happens sporadically or gets deprioritized when cash flow tightens. You reconcile the bank account monthly, but reconciliations lag by two weeks. You count inventory quarterly instead of monthly. You review credit card statements once a quarter instead of weekly. This infrequent monitoring means fraudulent activity sits undetected for months.

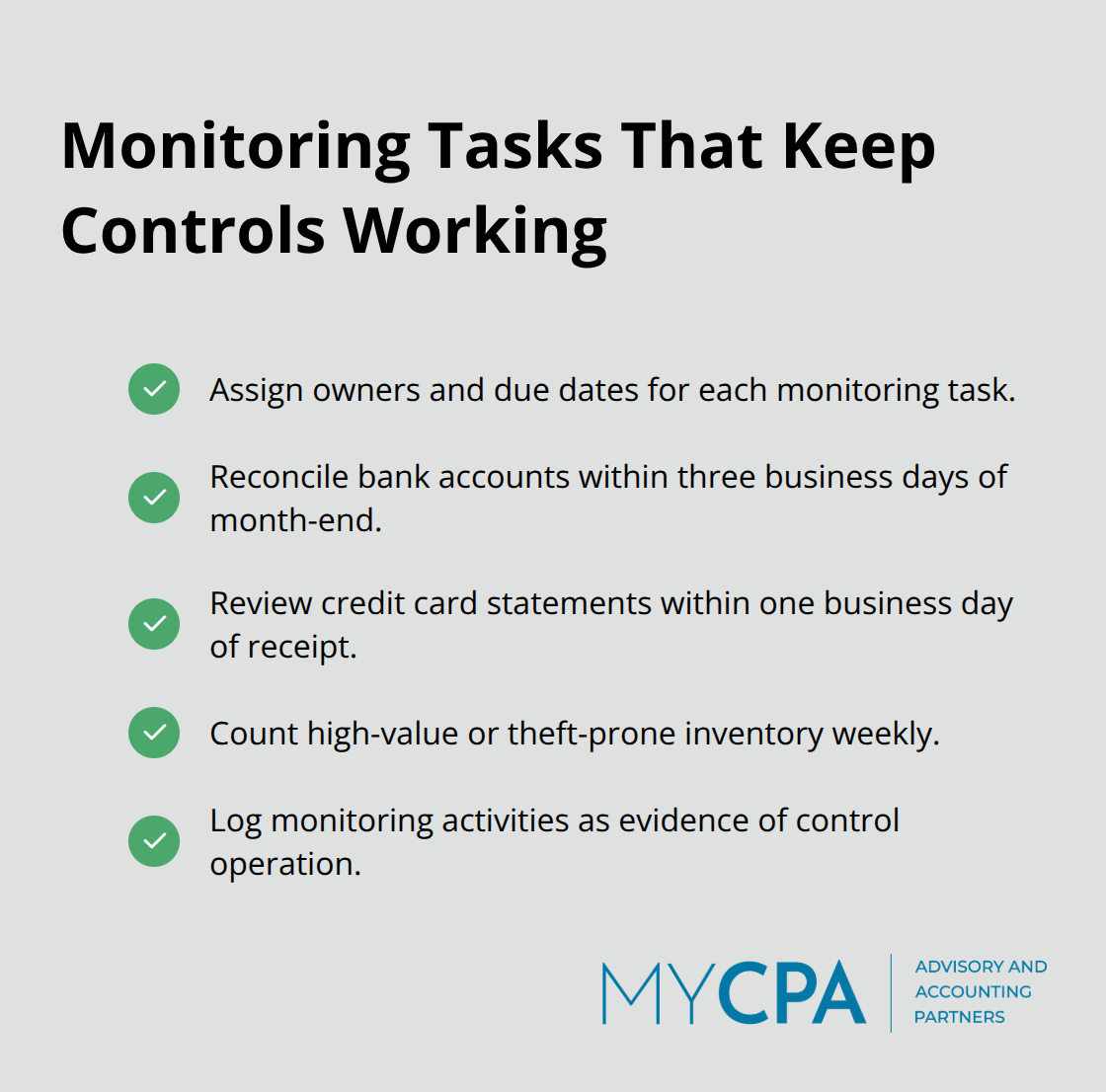

Establish a monitoring calendar and assign specific people to specific tasks on specific dates. Reconcile your bank account within three business days of month-end. Review credit card statements within one business day of receipt. Count high-value or theft-prone inventory weekly.

Document these monitoring activities in a log so you have evidence that controls actually operated.

The fourth breakdown involves access controls that sound good in theory but create chaos in practice. You give your accounts payable clerk access to the bank account portal to verify deposits, but they can also initiate wire transfers. Your store manager has access to inventory adjustment screens and can increase stock without approval. Your bookkeeper can modify customer invoices after they’ve been sent. These overly broad access permissions exist because setting up granular access takes time and coordination.

Conduct an access audit today: list every employee who can approve payments, modify financial records, or access cash. For each person, document exactly what they should be able to do. Then meet with your IT provider or accounting software administrator and restrict access to match that documented list. Remove unnecessary permissions even if it means creating a second person to handle certain tasks. Test access controls by attempting unauthorized transactions and confirming the system blocks them.

Internal controls operate as an ongoing operational discipline, not a one-time project you complete and forget. The four core controls-segregation of duties, bank reconciliations, inventory tracking, and documentation standards-form your financial foundation and protect against fraud, errors, and compliance violations that compound over time. An internal controls checklist helps you identify gaps systematically, track your progress, and maintain consistency as your business grows.

Strengthening your financial foundation requires three concrete actions. Document your current control procedures in writing so everyone understands the rules and you have evidence that controls exist. Integrate controls into your accounting software through automated workflows and access restrictions rather than relying on manual processes. Establish a monitoring calendar with assigned owners and specific dates so controls operate consistently instead of getting deprioritized during busy seasons.

Most business owners lack the time and expertise to design and implement controls alone, which is where professional guidance makes the difference. We at My CPA Advisory and Accounting Partners help you identify vulnerabilities, design controls that fit your operations, and implement systems that catch problems before they damage your bottom line. Contact us today to discuss how we can help you build the financial foundation your business deserves.

Privacy Policy | Terms & Conditions | Powered by Cajabra