Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Most startups fail because they run out of money, not because their business idea is flawed. The difference between those that survive and those that don’t often comes down to one thing: smart growth planning for startups.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how the right financial strategy transforms ambitious founders into sustainable business owners. This guide walks you through the exact steps to align your funds with your growth goals.

Your burn rate is the speed at which you spend cash each month. Calculate this by dividing your total monthly operating expenses by the cash you have on hand. A startup spending $50,000 monthly with $300,000 in the bank has a nine-month runway. That’s not a comfortable position.

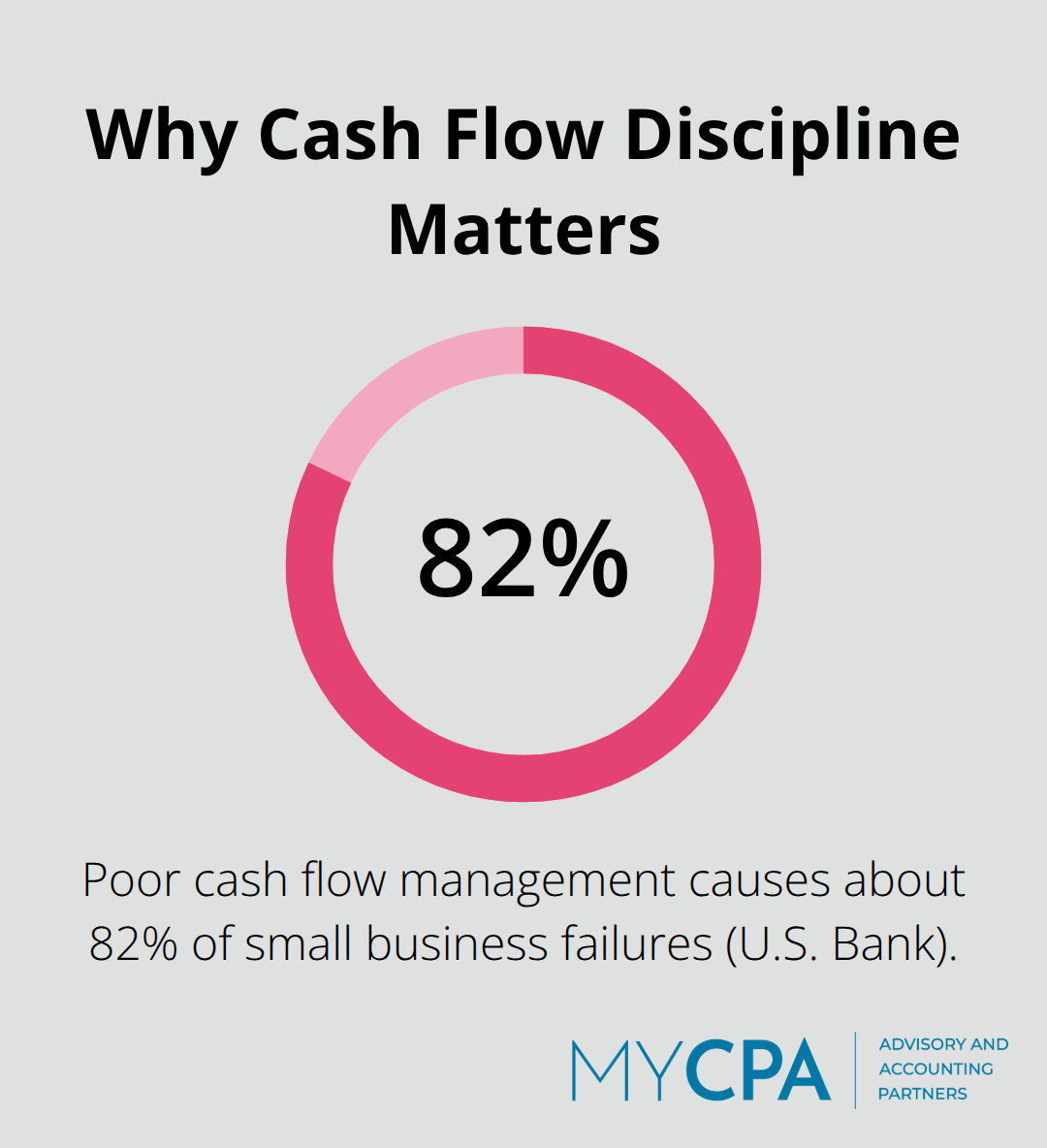

According to data from U.S. Bank, poor cash flow management causes about 82% of small business failures, which means most founders underestimate how quickly their money disappears. Track your burn rate weekly, not monthly. Weekly tracking catches spending spikes before they derail your runway.

Start by listing every fixed cost: salaries, rent, software subscriptions, insurance. These don’t change month-to-month. Then list variable costs: marketing spend, materials, freelance contractors. Variable costs shift based on your growth rate, so be honest about what you actually spend, not what you hope to spend. Many founders cut their variable cost estimates by 30% to appear more efficient on paper. That’s a mistake that kills startups.

A startup earning $100,000 from one customer is riskier than one earning $100,000 from fifty customers. Identify where your money actually comes from and whether that revenue is predictable. Subscription revenue is more predictable than one-time sales. A SaaS startup with $5,000 in monthly recurring revenue is more bankable than one with $5,000 in sporadic project fees.

Calculate your gross margin on each revenue stream. Your gross margin is simply total revenue minus cost of goods sold (COGS). If you sell a product that costs you $60 to deliver and customers pay $100, your gross margin is 40%. That 40% must cover your operating expenses plus fuel growth. If your gross margin is 30% and your operating expenses consume 35% of revenue, you’re losing money on every sale. This is common in early-stage companies, but it’s unsustainable beyond the first 12 months.

Map your three largest fixed costs and your three largest variable costs separately. For most startups, payroll is the largest fixed cost. For software companies, cloud infrastructure and customer acquisition are the largest variables. Knowing this breakdown lets you make real decisions: if you need to cut 20% of spending, cutting payroll is painful but has immediate impact, whereas cutting a $2,000 software subscription saves money but rarely moves the needle. With this foundation in place, you’re ready to allocate your funds strategically across the areas that will actually move your growth forward.

Most founders allocate funds based on what feels urgent rather than what drives growth. You need a different approach. Start by mapping every dollar back to one of three categories: keeping the lights on, acquiring customers, and building product. Strategic allocation of budgeting by impact categories for startups requires setting clear financial targets. These percentages shift based on your stage and business model, but the principle stays constant: if you don’t track allocation by impact, you spend blind. A SaaS startup with a 40% gross margin should never spend 60% of revenue on operations because nothing remains for growth. Calculate your target allocation first, then build your budget to match it. If your actual spending drifts from your target, you’ve spotted a problem before it becomes a crisis.

Most startups underspend on customer acquisition because they fear the upfront cost. A 2024 study found that improving cash flow forecasting accuracy by 15% boosts pre-tax profits by over 3%, which means better spending decisions compound. If your customer acquisition cost to lifetime value ratio optimization is healthy, spending more on acquisition is rational. The math is straightforward: spend more on acquisition if your unit economics support it. Many founders cap their customer acquisition spending at 20% of revenue because they heard that number somewhere. That’s arbitrary. If your gross margin is 70% and your lifetime value supports it, spending 40% on acquisition is rational. Track your actual customer acquisition cost monthly and compare it to your lifetime value. If the gap widens, you have a unit economics problem that no budget reallocation will fix. If the gap is healthy, increase spending and capture market share.

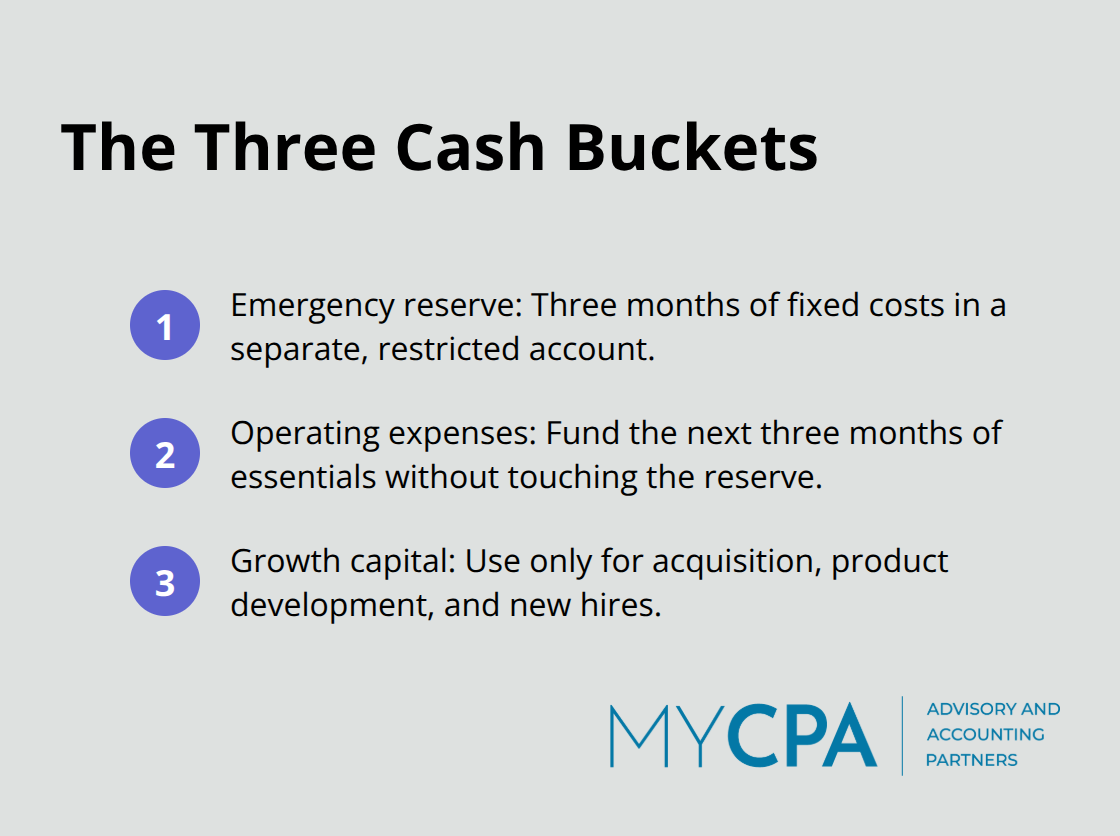

Your emergency reserve should equal three months of fixed operating costs, not one month. If your monthly fixed costs are $100,000, you need $300,000 sitting in a separate account. This sounds conservative, but it’s the difference between weathering a lost customer and shutting down. Build this reserve first before you allocate anything toward growth. Once your reserve exists, your remaining capital can fund growth without putting the business at existential risk. Many founders skip this step and treat their cash account like a checking account, pulling from it for whatever urgent problem surfaces. That’s how you end up with zero runway when a major customer delays payment by 60 days. Separate your cash into three mental buckets: emergency reserve, operating expenses for the next three months, and growth capital.

Only the third bucket should fund customer acquisition, product development, or new hires. This discipline prevents the constant scramble for cash that kills most startups in years two through five.

The tension between paying today’s bills and investing in tomorrow’s growth defines startup finance. Most founders resolve this tension poorly-they either hoard cash and miss growth opportunities, or they spend aggressively and run out of runway. The right approach sits between these extremes. Your operating budget must cover salaries, rent, software, and insurance without compromise. These costs keep your business functioning. Your growth budget funds customer acquisition and marketing activities that generate revenue. Your product budget funds development that improves your offering and competitive position. When cash gets tight, most founders cut the growth and product budgets first. That’s backward. Cutting growth spending slows revenue, which makes the cash crisis worse. Instead, scrutinize your operating budget. Can you renegotiate rent? Can you reduce headcount? Can you eliminate redundant software subscriptions? These moves hurt, but they preserve your ability to acquire customers and build product. The companies that survive downturns are those that maintain growth spending while cutting operations ruthlessly.

Startups fail not because they lack ambition, but because they spend money on the wrong things at the wrong time. The most destructive mistake is spending money on activities that don’t produce revenue while neglecting the financial guardrails that keep you alive. Many founders treat their cash account like a venture capital fund, deploying capital across marketing, hiring, product development, and tools without connecting spending to actual business results. A startup spending $15,000 monthly on a sales team that produces zero qualified leads hemorrhages cash. A startup spending $3,000 monthly on a tool that automates a process taking one person two hours weekly wastes money. The difference between these two mistakes is that the first one becomes obvious after a few months, while the second one hides in plain sight for years. You need to audit every expense against one simple question: does this directly produce revenue or prevent the business from functioning? If the answer is no, cut it immediately.

We mentioned the three-month reserve earlier, but most founders still skip this step because it feels conservative. That’s a fatal error in judgment. A startup with $300,000 in the bank and zero emergency reserve is actually in a worse position than a startup with $200,000 in the bank and a $100,000 emergency reserve. The first startup will spend down to zero within months because every unexpected cost (a major customer departure, a cloud infrastructure bill spike, a key employee departure) pulls from operating capital and compresses runway. The second startup absorbs these shocks without scrambling.

Build your emergency reserve before you spend a dollar on growth. This means calculating three months of fixed operating costs and parking that money in a separate, restricted account you don’t touch. For a startup with $80,000 in monthly fixed costs, this is $240,000. That’s real money, which is why most founders avoid it. But this reserve is the difference between handling a crisis and declaring bankruptcy. A customer payment delay of 60 days, which is common in B2B sales, becomes catastrophic without this buffer. An unexpected software licensing cost or a necessary equipment repair becomes a death spiral. Once you’ve depleted the reserve, you can’t rebuild it while managing a cash shortage.

Most startups review their finances quarterly or annually, which is far too infrequent. Three months of cash flow passes before quarterly numbers arrive, and you’ve already spent that money on problems you didn’t see. Switch to monthly financial reviews to compare actual spending against your budget and actual revenue against your forecast. This takes four hours maximum if your accounting is organized. Pull three reports: your income statement showing revenue and expenses, your cash flow statement showing money in and out by timing, and a variance report showing where spending deviated from budget.

If you spent 40% more on marketing than budgeted, you need to know why and whether that spending produced the expected customer acquisition. If revenue came in 20% below forecast, you need to adjust your burn rate calculation immediately and identify whether the shortfall is temporary or structural. Many founders avoid these reviews because the numbers are uncomfortable. That avoidance is a choice to fly blind. The founders who survive are those who face their numbers monthly and adjust spending decisions accordingly. If your cash flow problems rise faster than your revenue per customer, you need to cut acquisition spending or fix your product. If your payroll consumes 70% of revenue and your gross margin is only 50%, you need to reduce headcount or increase prices. These adjustments hurt, but they’re far less painful than discovering a cash crisis six months too late.

Aligning your funds with your growth ambitions requires three core practices: tracking your actual numbers, making allocation decisions based on impact rather than urgency, and reviewing your finances monthly without fail. Most startups that fail never establish these habits-they spend money reactively, skip the emergency reserve, and avoid their financial statements until crisis arrives. Growth planning for startups isn’t about predicting the future perfectly; it’s about building the discipline to track what’s happening, compare it to expectations, and adjust your spending accordingly.

Your burn rate, gross margin, and customer acquisition cost matter most (everything else is noise). Calculate these three numbers this week, then build your emergency reserve equal to three months of fixed operating costs before you allocate a single dollar toward growth. This feels conservative, but it’s the most aggressive move you can make because it keeps your business alive long enough to execute your strategy.

Pull your income statement, cash flow statement, and variance report every month to compare actual results against your forecast. We at My CPA Advisory and Accounting Partners help founders build the financial systems and habits that support sustainable growth, whether you need help organizing your accounting, setting up QuickBooks, or creating a financial plan that actually works.

Privacy Policy | Terms & Conditions | Powered by Cajabra