Monthly Close Process: Streamline Your Bookkeeping

Streamline your monthly close process with practical steps to organize bookkeeping, reduce errors, and close your books faster each month.

Most business owners leave thousands of dollars on the table each year by missing deductions and tax strategies they’re entitled to claim. At My CPA Advisory and Accounting Partners, we’ve seen firsthand how legal tax minimization can transform a company’s bottom line when done strategically.

This guide walks you through the specific deductions, retirement accounts, and business structures that actually reduce your tax burden. You’ll find practical steps you can implement before year-end.

Most business owners claim the obvious deductions-salaries, rent, supplies-and stop there. The gap between what they claim and what they’re legally entitled to deduct often amounts to thousands of dollars annually. Legal Tax Deductions You Might Be Missing represent some of the largest missed opportunities, yet many owners overlook them entirely.

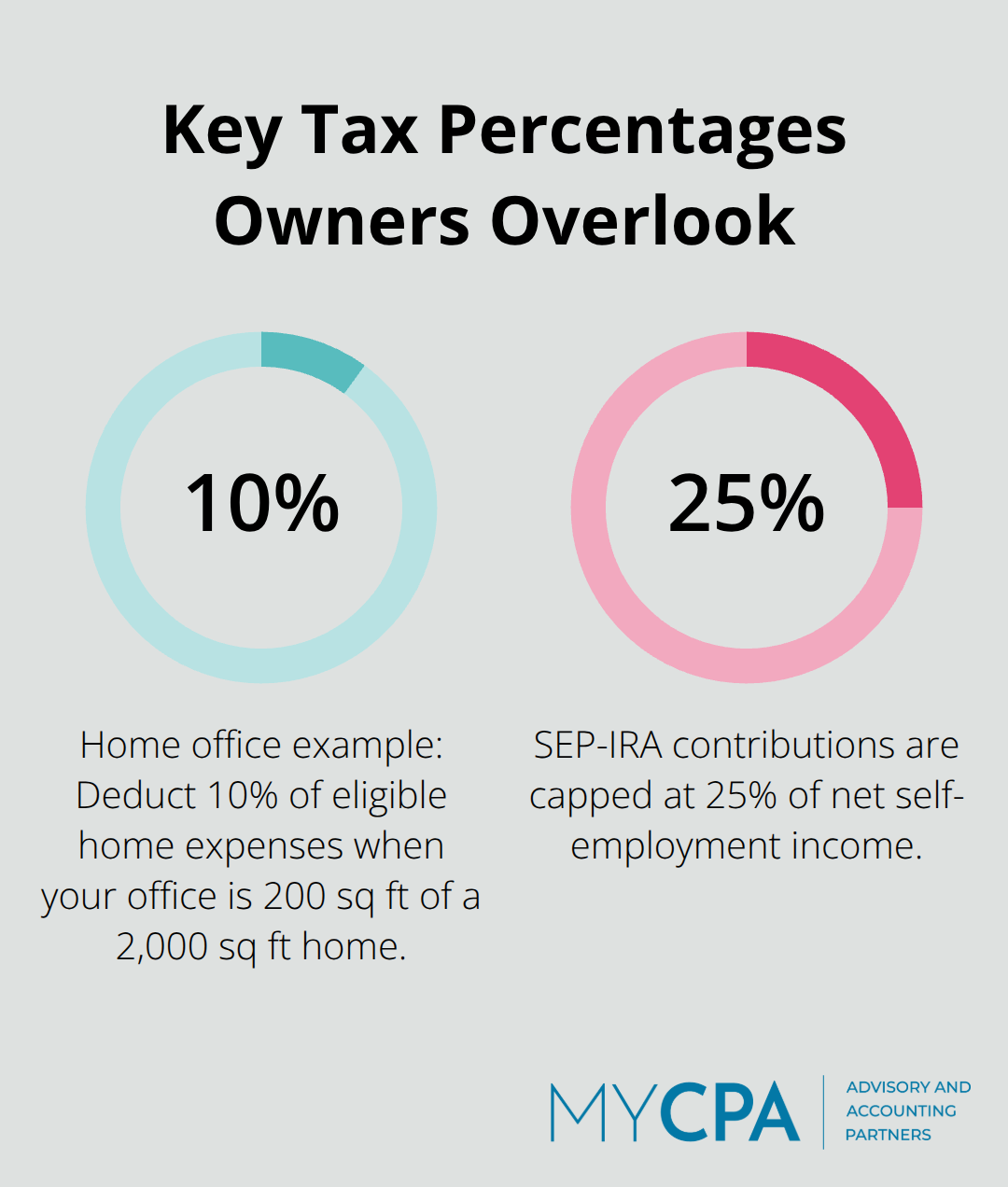

The IRS allows two methods for home office deductions. The simplified option costs $5 per square foot (capped at 300 square feet, so maximum $1,500 annually). The actual expense method lets you deduct a percentage of mortgage interest, property taxes, utilities, insurance, and repairs based on your home office’s square footage. If your home office occupies 200 square feet of a 2,000 square foot home, you deduct 10% of those expenses.

Many owners skip this entirely because they assume the simplified method is too small to matter. Actual expenses often exceed $3,000 to $5,000 yearly for a dedicated workspace. Calculate both methods and claim whichever produces the larger deduction. The actual expense approach typically wins for owners with substantial home office space or high utility costs.

You can either use the standard mileage rate or track actual expenses including gas, maintenance, insurance, and depreciation. For self-employed and business use, the rate is 70 cents per mile. The mileage method is simpler, but actual expenses frequently generate larger deductions for owners who drive substantial business miles.

Document every trip with dates, destinations, and business purpose. The IRS scrutinizes vehicle deductions heavily, and poor records invite audits. A simple spreadsheet or mileage app prevents disputes and substantiates your claims when the IRS questions them.

Education and training expenses directly reduce taxable income when they maintain or improve skills required for your current business. Accounting software courses, industry certifications, tax strategy workshops, and professional memberships all qualify. The IRS distinguishes between education that qualifies for deductions and education that doesn’t-training for a new career doesn’t count, but training to stay current in your field does.

A $1,500 tax planning seminar or $2,000 industry conference is fully deductible if it relates to your existing business. Many owners hesitate claiming these because they view professional development as personal investment rather than business expense. That’s incorrect. If the training maintains your professional competency or improves your ability to run your business more efficiently, it’s deductible.

Consider meals during business travel, subscriptions to professional publications, and dues to industry associations. The key is connecting the expense directly to your business operations. A $150 monthly subscription to industry research that informs your business decisions qualifies. Tracking these throughout the year prevents the end-of-year scramble and ensures you don’t overlook categories.

Many owners underestimate total professional development spending because they track it informally instead of systematically categorizing it in their accounting system. These overlooked deductions compound annually, reducing your taxable income far more than most business owners realize.

Self-employed business owners face a tax disadvantage compared to employees with 401(k) plans-until they take control of their retirement savings. A Solo 401(k) or SEP-IRA transforms retirement contributions from an afterthought into one of your largest tax deductions.

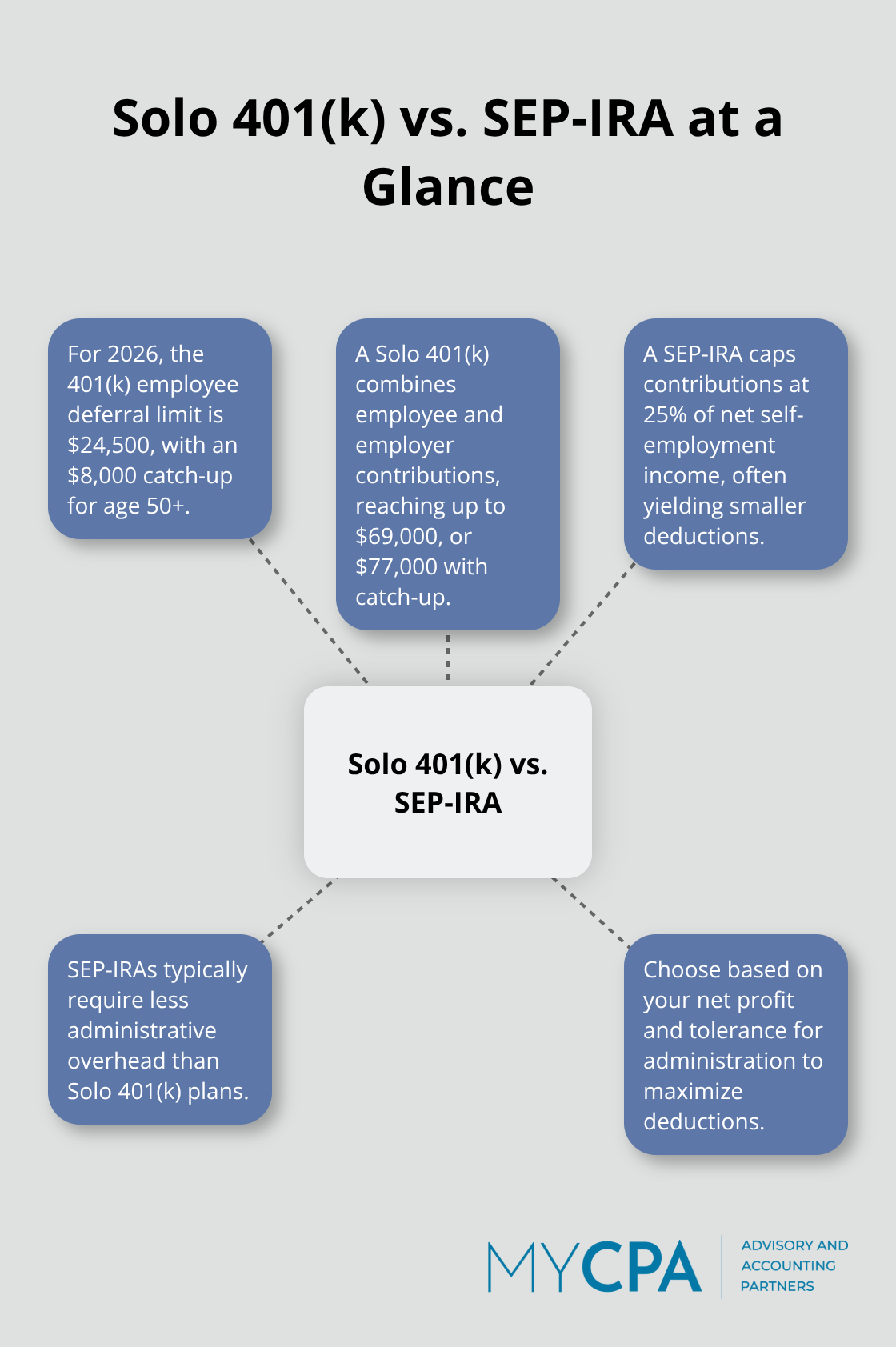

For 2026, the 401(k) contribution limit reaches $24,500 with an $8,000 catch-up for those 50 and older, according to IRS guidance. A Solo 401(k) allows you to contribute as both employee and employer, potentially reaching $69,000 annually (or $77,000 with catch-up contributions). A SEP-IRA caps contributions at 25% of net self-employment income, typically generating smaller deductions but requiring less administrative overhead.

The choice depends on your net profit and administrative tolerance. If you earn $150,000 in net profit, a Solo 401(k) lets you contribute substantially more than a SEP-IRA, making it the superior choice for most business owners with moderate to high income.

The timing matters significantly-contributions must be made by your tax filing deadline, including extensions, giving you flexibility into the following year to maximize deductions when you know your actual income. Most owners wait until January to fund retirement accounts, missing the strategic advantage of knowing their exact year-end numbers and adjusting contributions accordingly.

Calculate your estimated net profit by November, then fund the account strategically to land in the optimal tax bracket. This approach transforms retirement savings from a routine task into a deliberate tax-reduction tool.

Income timing and expense acceleration work together to minimize taxes in high-earning years. If you’re heading toward your highest income year on record, accelerate discretionary expenses into December-prepay insurance premiums, purchase equipment before year-end, or front-load professional development spending. Conversely, defer income recognition when possible by delaying client invoicing or deferring bonuses to January.

The IRS allows business owners significant flexibility here, and smart timing can shift $20,000 to $50,000 of taxable income between years depending on your situation. A contractor who bills clients in late December versus early January creates a meaningful tax difference across two years. Similarly, purchasing $30,000 in equipment in December versus January generates immediate depreciation deductions that reduce current-year taxable income.

These aren’t aggressive strategies-they’re standard practice among tax-efficient business owners. The key is planning these moves in November, not scrambling in December. Your tax professional can model different scenarios and show you the exact savings from each timing decision, turning abstract tax strategy into concrete dollar amounts.

Once you’ve optimized your retirement contributions and income timing, the structure of your business itself becomes your next lever for tax reduction. The choice between operating as an S-Corp, LLC, or sole proprietorship can save you thousands annually in self-employment taxes.

The difference between operating as a sole proprietor, LLC, or S-Corp can mean $10,000 to $40,000 annually in self-employment taxes. Most business owners default to their initial structure without reconsidering whether it still makes sense as their income grows.

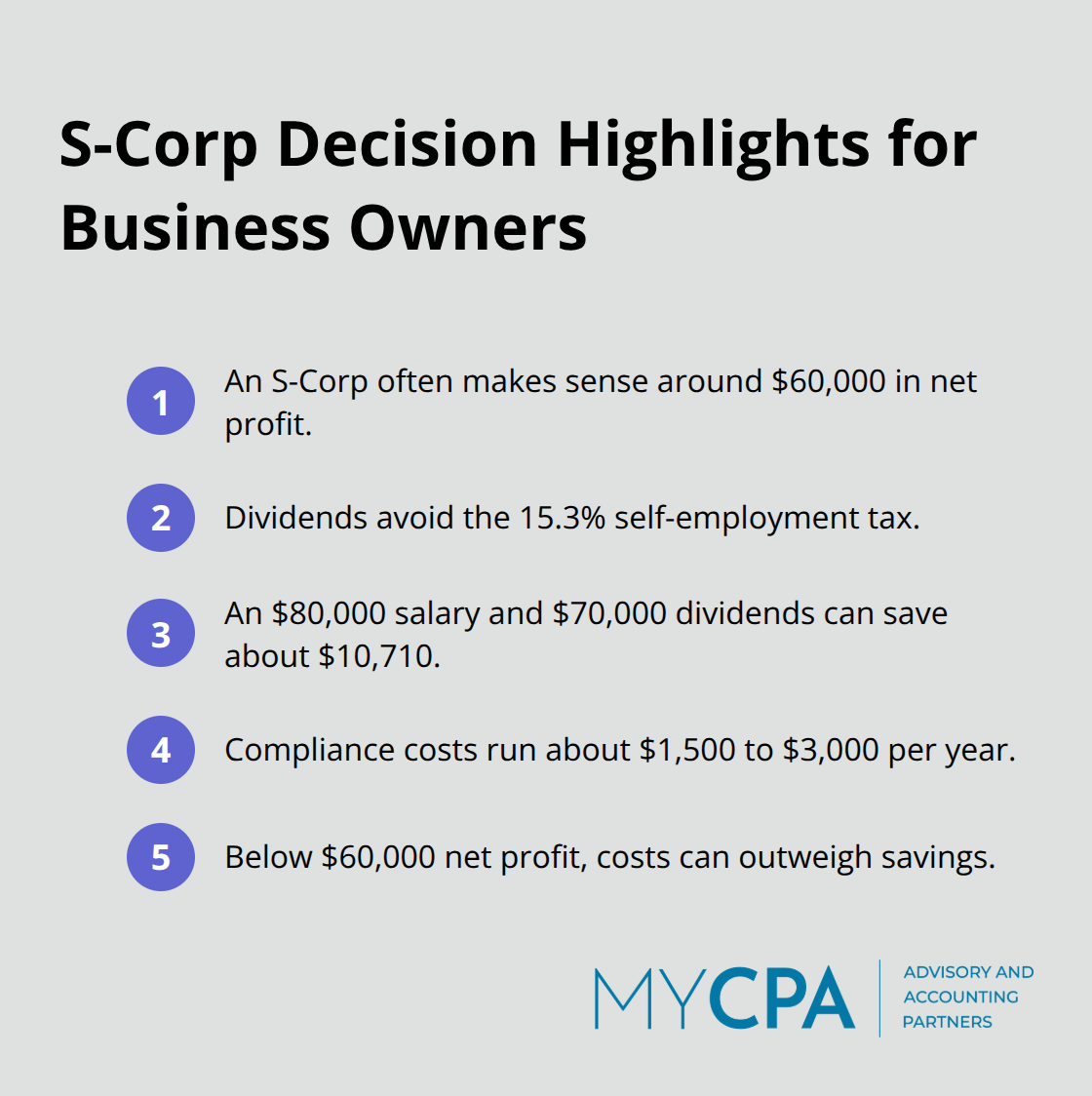

An S-Corp election becomes advantageous once you reach roughly $60,000 in net profit, though the exact threshold depends on your specific situation. Operating as an S-Corp requires you to pay yourself a reasonable salary (subject to payroll taxes) and distribute remaining profits as dividends, which avoid the 15.3% self-employment tax.

If you earn $150,000 in net profit and split it as $80,000 salary and $70,000 dividends, you save approximately $10,710 in self-employment taxes compared to claiming the full $150,000 as self-employment income under a sole proprietorship or standard LLC. The administrative burden of S-Corps includes payroll processing, quarterly filings, and separate tax returns, adding roughly $1,500 to $3,000 annually in accounting and payroll costs. At lower income levels (under $60,000 net profit), these compliance costs exceed the self-employment tax savings, making an S-Corp election uneconomical.

The IRS scrutinizes S-Corp salary levels closely. If you operate a service business and take a suspiciously low salary while extracting large dividends, the IRS will reclassify those dividends as wages subject to payroll taxes plus penalties. The reasonable salary standard means a marketing consultant earning $200,000 cannot claim a $20,000 salary; the IRS expects compensation reflecting actual market rates for similar roles.

An accountant or consultant in your market typically earns $70,000 to $120,000 annually, so your S-Corp salary must fall within realistic ranges. This constraint prevents aggressive tax planning but protects you from audit risk and penalties.

An LLC taxed as an S-Corp offers the flexibility of an LLC with the tax benefits of an S-Corp, making it the preferred structure for most business owners once income justifies the added complexity. This hybrid approach combines liability protection with tax efficiency without the rigid formalities that traditional S-Corps demand.

Quarterly estimated tax payments determine whether you face penalties and interest or end the year with manageable tax liability. Self-employed business owners must pay quarterly estimated taxes in April, June, September, and January based on projected annual income. Underestimating creates an underpayment penalty calculated on the shortfall amount, and the IRS charges interest on top of penalties.

Most owners base quarterly payments on prior-year income, which works fine if income remains stable but fails catastrophically in growth years. If you earned $100,000 last year and made quarterly payments of $7,500 (totaling $30,000), but this year you’ll earn $200,000, you’ll face substantial penalties on the $20,000 underpayment plus interest charges. Adjusting quarterly payments in September or October when you realize income will exceed projections prevents this scenario entirely.

A safer approach involves paying 100% of prior-year tax liability across four quarters, which eliminates underpayment penalties even if current-year income rises dramatically. This strategy trades slightly higher quarterly payments for complete protection against penalty exposure.

Equipment purchases in December generate immediate depreciation deductions under Section 179, allowing you to deduct qualifying equipment purchases versus spreading depreciation across multiple years. A $50,000 server purchase in December creates a full deduction in the current year rather than a five-year depreciation schedule, shifting $50,000 of taxable income to future years.

Prepaying professional liability insurance, property taxes, or business licenses before December 31 accelerates deductions into the current year when you need them most. These tax planning strategies compound with retirement contributions and income deferral decisions, creating tax savings that transform how much of your profit actually flows to the IRS versus your business bank account.

The strategies outlined above represent the core of legal tax minimization for business owners. Home office deductions, vehicle expense tracking, professional development costs, retirement account optimization, and strategic business structure decisions collectively reduce your tax burden by thousands annually. These aren’t theoretical concepts-they’re concrete actions that transform how much of your profit reaches your bank account versus the IRS.

The gap between what most business owners pay in taxes and what they’re legally entitled to minimize often exceeds $15,000 to $30,000 yearly. Professional tax planning matters because the tax code rewards owners who plan strategically rather than react at filing time. A tax professional models different scenarios, quantifies savings from each decision, and ensures your implementation stays compliant with IRS requirements.

Start with a review of your current deductions against the categories outlined here, then connect with our team to model the financial impact and implement changes before year-end. We at My CPA Advisory and Accounting Partners help business owners implement tax-efficient strategies tailored to their specific situation, ensuring you capture every legal deduction while maintaining compliance.

Privacy Policy | Terms & Conditions | Powered by Cajabra