Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Most startups leave money on the table every year simply because they don’t know which tax strategies actually work. The difference between a startup that pays thousands in unnecessary taxes and one that doesn’t often comes down to planning.

At My CPA Advisory and Accounting Partners, we’ve helped countless founders realize that tax minimization for startups isn’t about cutting corners-it’s about understanding your options. This guide walks you through the specific moves that can legally reduce what you owe.

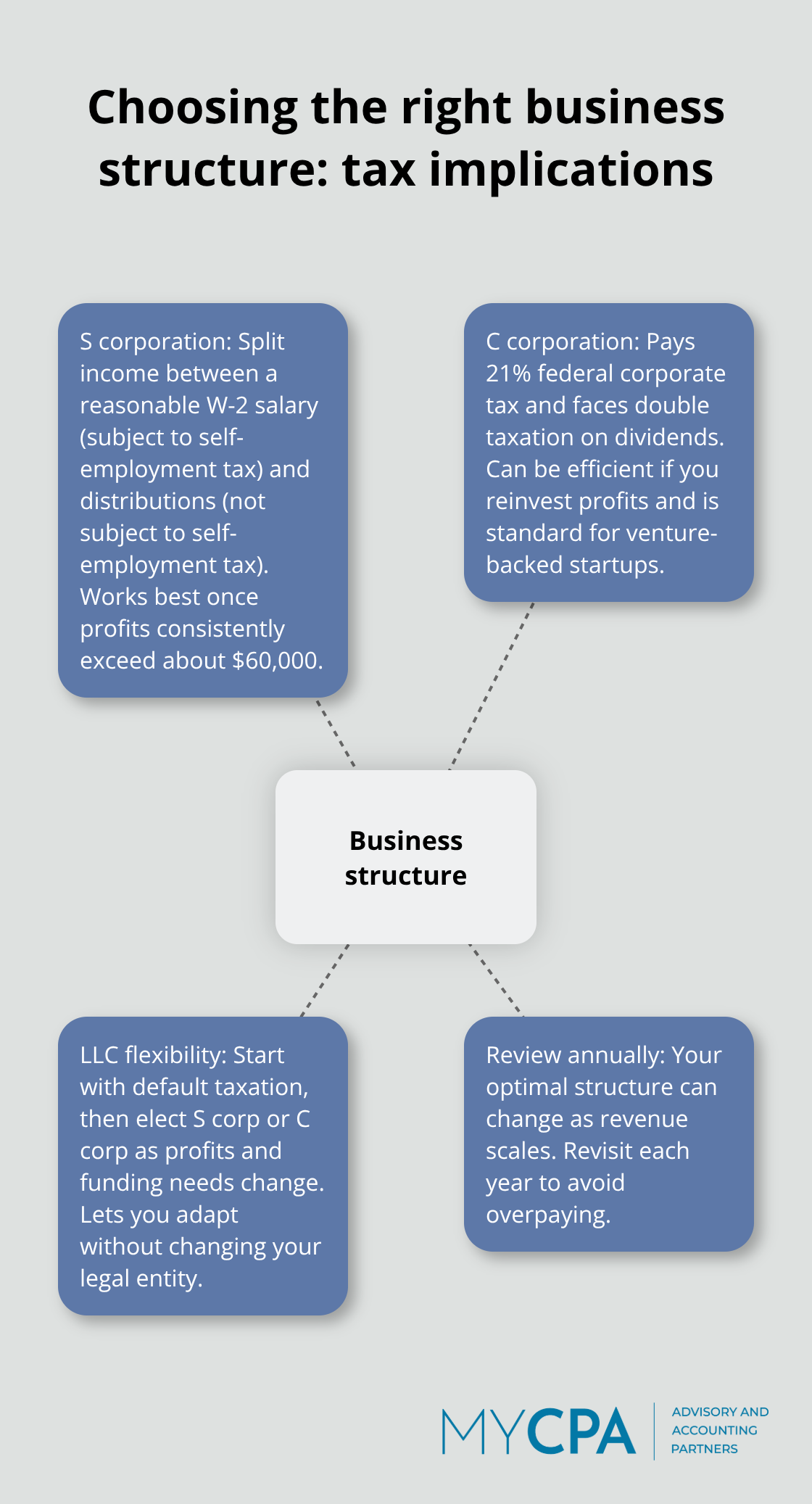

Your choice of business structure determines whether you pay taxes once or twice, whether profits flow through to your personal return, and how much self-employment tax you owe. The three most common structures for startups each handle taxes differently, and picking the wrong one costs real money. An S corporation can save you thousands annually compared to an LLC taxed as a sole proprietorship, but only if your income justifies the extra paperwork. A C corporation makes sense if you’re raising venture capital and plan to reinvest profits, since the 21% federal corporate rate may be lower than your personal rate. An LLC gives you flexibility-you can choose to be taxed as an S corporation, C corporation, or sole proprietorship depending on your situation, which means you’re not locked into one approach forever. The SBA notes that your structure choice directly influences taxes, personal liability, ability to raise money, and required filings, so you must decide this before you register your business. Most founders wait too long to make this decision, then discover they’re paying double taxation or missing out on pass-through benefits that could have saved them money from day one.

If your startup generates consistent profit above $60,000 annually, an S corporation election typically saves money through self-employment tax reduction. With an S corp, you split income into a reasonable W-2 salary (which is subject to self-employment tax) and distributions (which are not). If you earn $100,000 as an LLC sole proprietor, you pay self-employment tax on the full amount-roughly 15.3% in combined Social Security and Medicare taxes. If you’re taxed as an S corp instead, you might pay yourself a $60,000 salary (with self-employment tax) and take $40,000 in distributions (with no self-employment tax), cutting your tax bill by around $4,600 annually. The IRS requires your salary to be reasonable for the work you actually do, so you can’t pay yourself $1,000 and take $99,000 in distributions. State rules matter too-some states recognize S corp treatment for federal purposes, while others tax S corp profits differently, so check your specific state before you commit.

A C corporation is a separate tax entity that pays federal income tax at 21%, then shareholders pay tax again when they receive dividends. This double taxation sounds bad, but it disappears if you don’t take dividends and instead reinvest profits into the business. If your startup is burning cash on product development, hiring, or equipment, reinvesting profits rather than distributing them means you only pay the 21% corporate rate. Once you’re profitable and want to extract cash, double taxation becomes a real cost. For founders seeking venture capital, a C corporation is often required because investors expect this structure and it simplifies equity transactions. The SBA confirms that C corporations are well-suited for raising capital via stock. If you’re bootstrapping and reinvesting everything, a C corp can be tax-efficient.

An LLC offers a unique advantage: you elect how the IRS taxes you without changing your legal structure. You can start as a sole proprietor, switch to S corp taxation when profits justify it, then move to C corp treatment if you raise capital-all while remaining an LLC legally. This flexibility means you don’t lock yourself into one tax approach forever. Many startups use this strategy to adapt their tax treatment as they grow. Your state’s rules on LLC taxation vary, so verify what your state allows before you make an election. The ability to shift your tax classification without restructuring your business makes an LLC a practical choice for founders who aren’t sure which direction their company will take. As your revenue climbs and your situation changes, your tax strategy can change with it.

Your initial structure choice isn’t permanent. As your startup scales, what made sense at $50,000 in revenue may not work at $500,000. An S corp election that saves $4,600 annually might become inefficient once you’re taking significant distributions. A C corporation that made sense for venture funding might create unnecessary tax complexity if you bootstrap instead. The SBA emphasizes that you should review your structure annually as your business grows. Many founders ignore this step and overpay taxes for years simply because they never revisited their original choice. Your tax professional can model different scenarios and show you exactly how much each structure costs at your current income level. This analysis takes a few hours but often reveals thousands in annual savings.

Most startups claim only a fraction of the deductions they qualify for, then wonder why their tax bill feels so high. The home office deduction offers the easiest win and costs almost nothing to document. If you use 300 square feet of your home exclusively for business, you can deduct either 30% of your rent or mortgage interest, utilities, and property tax using the actual expense method, or claim $5 per square foot using the simplified method. The simplified method gets you $1,500 annually with almost no paperwork, which is why most startups should use it first.

Equipment purchases hit differently because the IRS lets you deduct the full cost immediately under Section 179, rather than spreading depreciation over five years. If you buy a $3,000 laptop, $5,000 in software licenses, or $8,000 in machinery this year, you can deduct all of it now, not later. This matters most in years when your startup is profitable because immediate deductions lower your taxable income right away. The catch is that Section 179 has annual limits that change, and some assets don’t qualify, so verify your specific purchases with a professional before you assume they’re eligible.

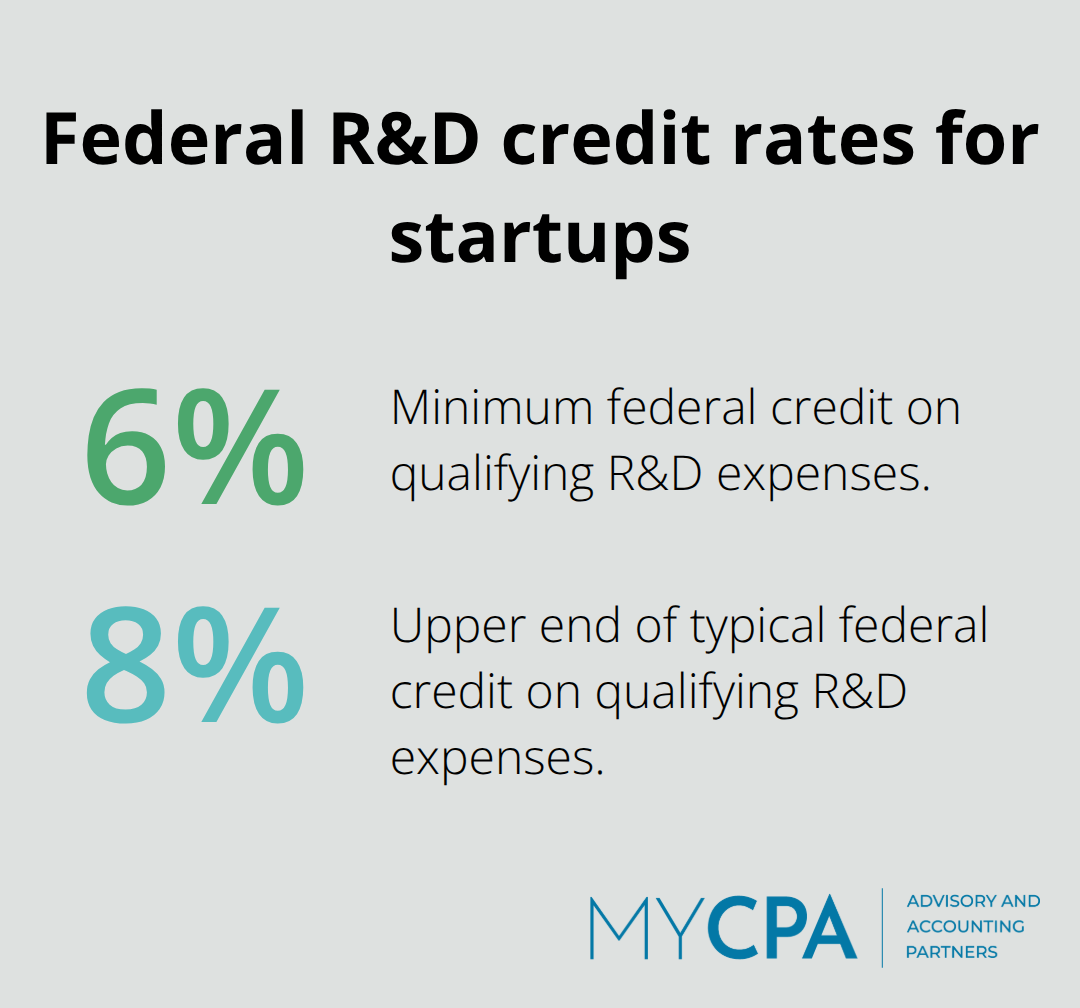

Research and Development tax credits represent the single biggest missed opportunity for startups. The IRS allows you to credit 6 to 8 percent of qualifying R&D expenses against your federal tax liability, and eligible startups with less than $5 million in gross receipts can offset payroll taxes instead of income taxes, which means you get cash back even if you’re not profitable. Qualifying activities include developing software, improving processes, building prototypes, or enhancing products, and qualifying costs span salaries for employees doing R&D work, contract research payments, cloud hosting, and supplies.

The four-part test requires that your work involve a permitted process, be technological in nature, aim to eliminate uncertainty, and follow a process of experimentation. Most startups document their R&D poorly and never claim the credit, but if you maintain receipts and timesheets showing which employees spent time on R&D projects, you can file Form 6765 with your tax return and claim thousands in credits retroactively. Startups with proposals under the American Innovation and Jobs Act could eventually see the credit rate rise to 20 percent and the startup cap increase to $500,000, though these expansions are not yet law.

The payroll tax offset for eligible small businesses lets you offset payroll taxes for up to five years, which provides immediate cash flow relief while you’re still investing in development. This strategy works especially well for pre-revenue or early-stage startups that need liquidity to fund operations.

If your startup generated losses in prior years or expects losses this year, those losses carry forward indefinitely and offset profits in future years, reducing your tax bill when you finally become profitable. If you lost $50,000 in year one and earned $100,000 in year two, you only owe tax on $50,000 of profit. Document those losses carefully because the IRS will ask for proof if you claim them years later. Once you understand which deductions and credits apply to your situation, the next step is timing those deductions strategically to maximize their impact.

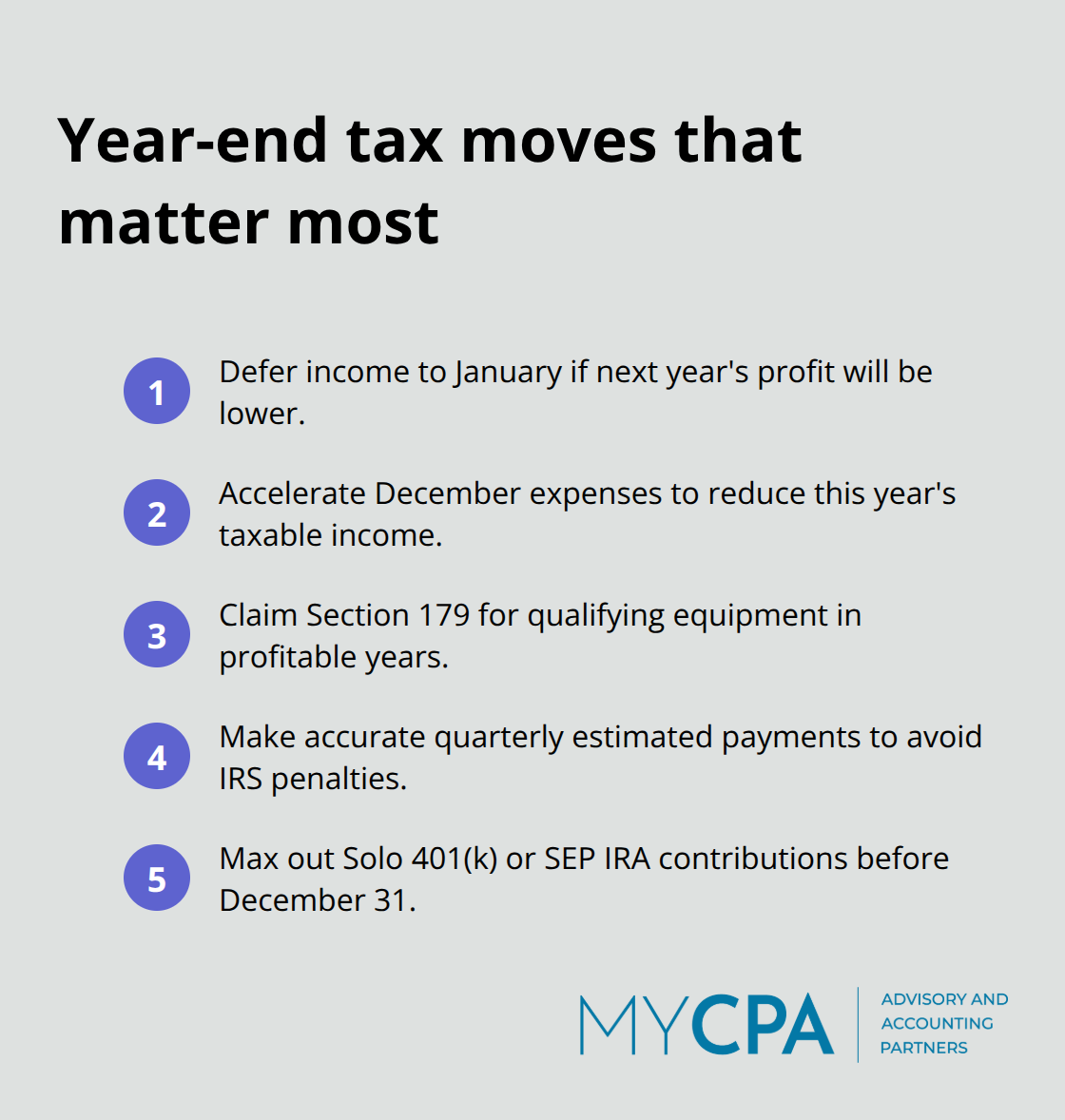

The difference between a startup that pays $15,000 in taxes and one that pays $8,000 often comes down to decisions made in November and December. Most founders treat year-end as a time to look backward at what happened, but it’s actually your last chance to shape your tax outcome for the entire year. Timing matters because income and expenses recognized in December count toward your current tax year, while those recognized in January count toward next year. If you’re profitable this year and expect losses next year, you can defer income to January and accelerate expenses to December to reduce your current tax bill significantly. The IRS allows you to defer certain income if you haven’t received it or payment hasn’t been unconditionally made available to you by year-end, which means you can ask clients to delay invoicing until January without triggering a tax consequence. Conversely, you can order equipment, software licenses, or supplies in December and claim the deduction this year even if you don’t pay the invoice until January, as long as you’ve received the goods or services. This strategy works best when you control your billing and purchasing timeline, which is easier for service-based startups than product companies. A profitable startup with $80,000 in discretionary spending can reduce taxable income by that full amount through accelerated purchases into December, potentially saving $20,000 to $30,000 in federal and state taxes combined.

Quarterly estimated tax payments protect you from underpayment penalties and interest charges that the IRS assesses if you owe more than $1,000 at tax time without paying enough throughout the year. Most startups underestimate their quarterly obligations because they confuse cash flow with taxable income, then face a surprise bill in April. The IRS calculates penalties based on the federal funds rate plus 3 percent, which compounds quarterly, so underpaying early in the year costs more than underpaying late in the year. If you owe $10,000 in taxes for the year and pay nothing until April, you’ll owe roughly $300 to $400 in penalties and interest depending on the quarter. Calculating your quarterly payment requires you to estimate your full-year profit, which means you need accurate monthly financial statements, not guesses. Many startups pay 25 percent of their estimated annual tax liability each quarter, which works if your income is consistent, but if you had a strong Q1 and expect to lose money in Q4, you can adjust your quarterly payments to match actual projected income. You can file Form 1040-ES to calculate your estimated payment, or work with a tax professional to model different scenarios.

Retirement contributions offer one of the last opportunities to reduce taxable income before December 31st closes the window. A Solo 401(k) contribution limits for self-employed founders 2024 as a self-employed founder allows you to contribute as both employee and employer, which directly reduces your taxable income dollar-for-dollar. A startup founder earning $100,000 in profit who contributes $20,000 to a Solo 401(k) only pays tax on $80,000 of income, saving roughly $5,200 in combined federal and state taxes. SEP IRAs offer another option with lower administrative burden, allowing contributions up to 25 percent of your net self-employment income. The SECURE Act 2.0 expanded contribution limits starting in 2024, so verify current limits with your tax professional before year-end because contribution deadlines are firm and you cannot catch up later if you miss December 31st.

Tax minimization for startups works when you combine the right business structure with strategic deductions and year-end planning. The three moves that matter most are choosing between an S corporation, LLC, or C corporation based on your profit level and growth plans, claiming every deduction and credit you qualify for, and timing your income and expenses to reduce your tax burden before December closes the window. Most startups leave thousands on the table simply because they never revisit their structure as they grow, miss R&D credits they qualify for, or fail to plan their year-end tax position until it’s too late.

Professional guidance transforms tax planning from guesswork into a concrete strategy. A tax professional models different scenarios at your current income level, identifies credits you didn’t know existed, and ensures your quarterly estimated payments match your actual profit rather than your cash flow. We at My CPA Advisory and Accounting Partners help business owners minimize tax liabilities while maintaining accurate financial reporting and proactive planning.

Calculate your current business structure’s tax cost, then model what an S corporation or different entity would cost at your projected year-end income. Pull together your R&D documentation and verify whether you qualify for credits. Contact My CPA Advisory and Accounting Partners to build your personalized tax strategy today, and lock in the deductions and timing strategies that move your bottom line.

Privacy Policy | Terms & Conditions | Powered by Cajabra