Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Growing fast feels great until your margins start shrinking. We at My CPA Advisory and Accounting Partners see this pattern constantly: businesses scale revenue but watch profitability slip away.

The good news is that cost control strategies don’t have to slow you down. With the right approach, you can grow aggressively while protecting what matters most-your bottom line.

Margin erosion during growth happens because fixed and variable costs respond differently to expansion. Fixed costs-salaries, rent, insurance, software licenses-remain constant whether you produce 100 units or 10,000 units. Variable costs, like raw materials and direct labor, move with production volume. When you scale fast, you often add fixed costs in anticipation of revenue that takes longer to materialize. A manufacturing company might hire 20 people and lease a larger facility to handle expected growth, but if that growth stalls or takes six months longer than planned, those fixed costs sit there eating into every sale.

Most businesses fail to track which costs are truly variable and which are fixed. Companies underestimate their COGS by ignoring indirect costs-utilities that support production, quality control staff, equipment maintenance. These hidden expenses compress margins faster than anyone realizes. A 10% revenue increase often fails to translate to a 10% profit increase when fixed costs remain constant. If your gross margin was 40% at $1 million in revenue, scaling to $1.5 million with the same fixed overhead structure does not automatically give you 40% gross margin on the new revenue. The incremental margin on that additional $500,000 is lower because the fixed costs are already paid.

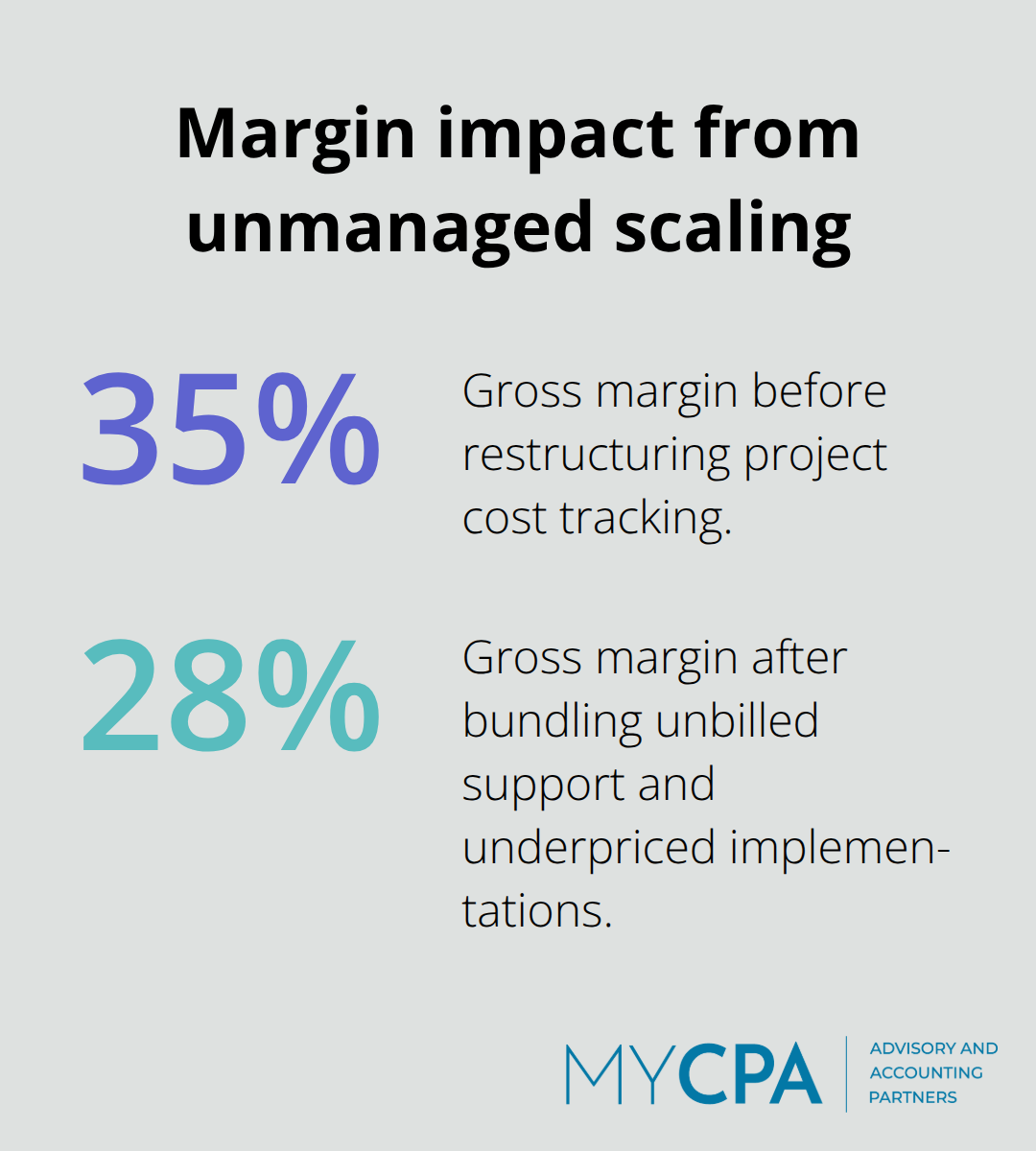

A software reseller scaled from $5 million to $15 million in revenue without restructuring how they tracked project costs. They discovered their actual gross margin had dropped from 35% to 28% because they bundled in unbilled support hours and underpriced implementations. A food manufacturer experienced similar pain when they added production capacity but failed to negotiate volume discounts proportional to their increased material purchases-their COGS actually increased as a percentage of revenue even though unit costs should have fallen.

These companies treated scaling as a revenue problem, not a cost problem.

Inflation compounds margin compression when material costs or labor rates rise. A business that does not adjust pricing or aggressively cut waste watches margins compress quarter after quarter. The stark lesson: scaling without intentional cost management creates a false sense of growth. Your top line grows, but your ability to invest in the business, pay down debt, or distribute profits shrinks. The antidote is understanding exactly which costs move with volume and which do not, then actively managing both categories as you expand. This requires monthly tracking of your cost structure, not annual reviews.

The businesses that protect profitability during growth treat cost control as a strategic priority from day one, not an afterthought when margins start disappearing. They understand their true cost structure and monitor it relentlessly. This foundation sets the stage for implementing practical strategies that actually work-strategies that separate companies that scale profitably from those that watch their margins disappear.

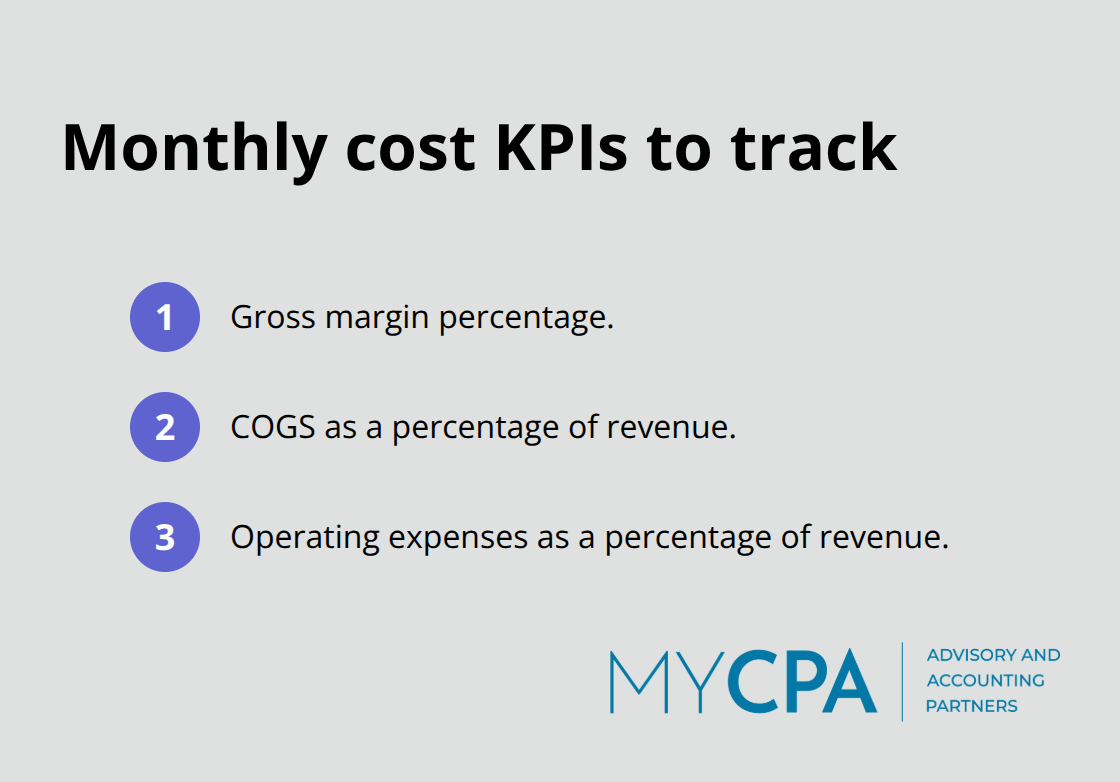

The gap between understanding your cost structure and actually controlling it is where most scaling businesses fail. Knowing that fixed costs sit idle when revenue stalls is one thing. Taking monthly action to manage them is entirely different. Companies that protect margins during growth shift from annual cost reviews to monthly cost tracking with specific accountability. Start tracking three numbers each month: gross margin percentage, COGS as a percentage of revenue, and operating expenses as a percentage of revenue. If any of these metrics moves unfavorably by more than 2% month-over-month, you need to know why and develop a plan to fix it within 30 days.

Most businesses wait for quarterly or annual financial statements to spot problems, but by then the damage compounds into significant margin erosion.

Activity-based costing assigns costs to the actual activities that drive them rather than spreading overhead evenly across all products or services. A manufacturer might discover that custom orders consume 40% of production labor but generate only 20% of revenue, revealing a pricing problem that standard cost accounting would hide. This method exposes which products or services actually drain resources and which ones generate real profit. The insight transforms how you price and which offerings you prioritize as you scale. Without this visibility, you continue investing in low-margin work while underpricing high-value offerings.

Automation eliminates the waste that inflates costs during scaling. Repetitive manual processes like data entry, invoice processing, and payroll administration consume labor hours that should be reserved for high-value work. A services firm scaling from 15 to 50 employees will either automate these functions or watch administrative costs balloon. Implement cloud-based accounting software that connects your invoicing, expense tracking, and payroll systems so data flows without manual re-entry. This alone typically saves 5 to 10 hours per week in administrative work, freeing your team to focus on activities that actually generate revenue.

Vendor consolidation and strategic negotiation directly protect margins because material costs often represent 40 to 60% of COGS in manufacturing and product businesses. Rather than spreading purchases across five vendors, consolidate volume with two or three preferred suppliers and negotiate volume discounts that reflect your growth trajectory. Request tiered pricing that drops automatically as your order volumes increase, and lock in material costs for 12 months when possible to hedge against inflation. A food manufacturer that consolidated suppliers and secured volume commitments reduced material costs by 8% while improving delivery reliability. These negotiations become more powerful as your scale increases, so structure them to reward growth.

Assign one person on your finance team explicit responsibility for monthly KPI monitoring and cost variance analysis. This person should flag any line item that deviates more than 5% from budget and present findings to leadership within two weeks. The discipline of monthly reviews, combined with clear ownership, transforms cost management from a sporadic exercise into a predictable rhythm that catches problems early. When someone owns the numbers, costs stay visible and controllable. This foundation of disciplined cost tracking positions you to make the technology investments that amplify your control even further as complexity increases.

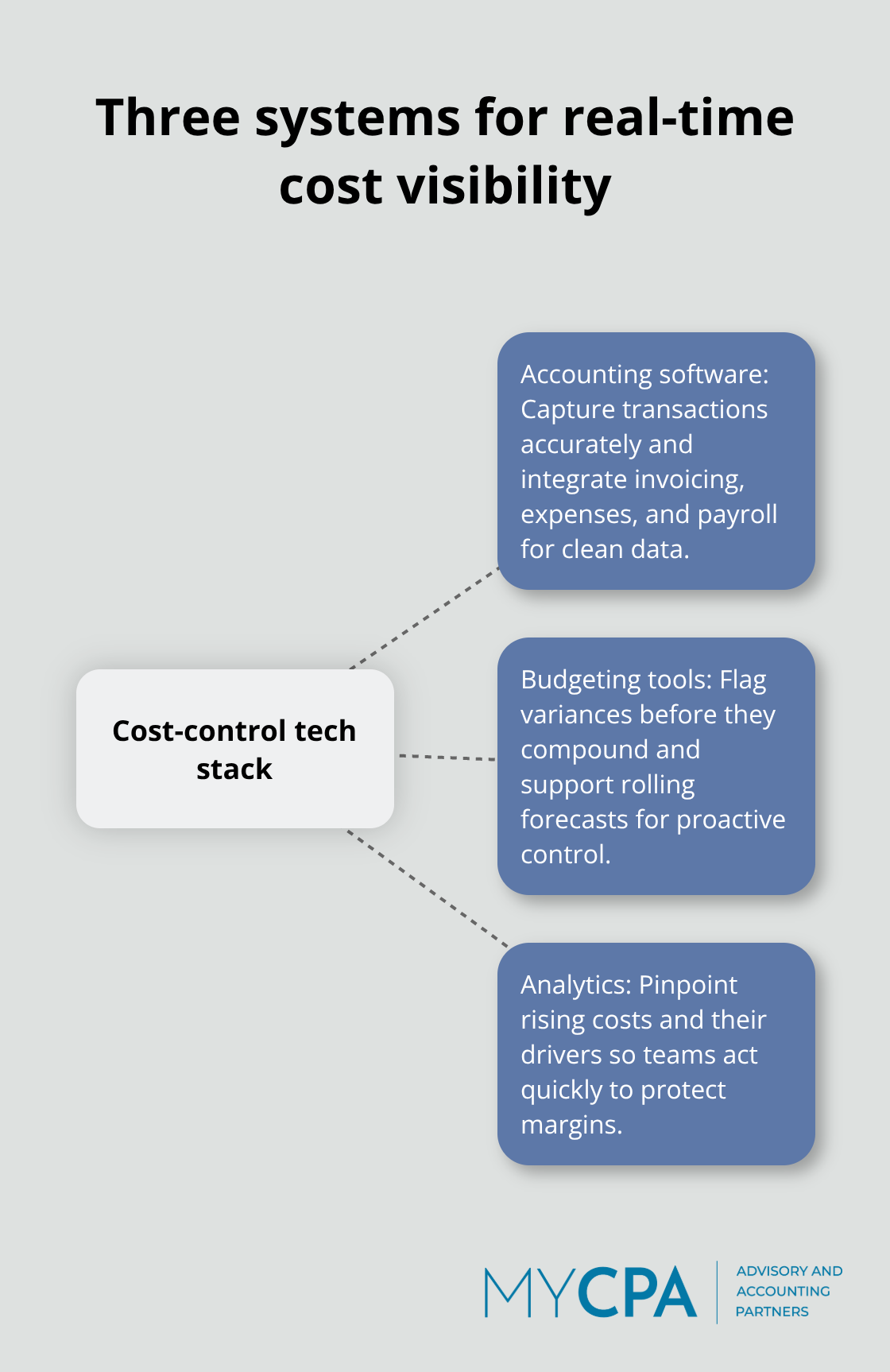

Monthly cost tracking and activity-based costing reveal problems, but without the right technology stack, your team spends more time collecting data than acting on it. Real-time visibility into your cost structure requires three interconnected systems working together: accounting software that captures transactions accurately, budgeting tools that flag variances before they compound, and analytics that pinpoint exactly where costs are rising and why.

Most scaling businesses operate with fragmented systems where data lives in spreadsheets, accounting software, and separate project management tools. This fragmentation creates blind spots that margin erosion exploits. A services firm spent 12 hours weekly consolidating data from three systems just to produce one monthly cost report, meaning leadership saw numbers 20 days after the month ended. Overspending patterns were already baked into the next month’s operations. They replaced this setup with integrated cloud accounting software connected to project management platforms, cutting reporting time to 2 hours and enabling real-time cost visibility. The shift paid immediate dividends: they caught a project running 18% over budget in week two instead of week six, adjusted staffing, and recovered most of the margin loss.

Budgeting and forecasting tools matter most when they surface cost overruns early enough to correct them. Standard accounting systems show you what happened; forecasting tools show you what will happen if current trends continue. Set up rolling 13-week cash flow forecasts that project COGS, operating expenses, and headcount costs based on actual spending patterns and revenue pipeline. When your forecast shows operating expenses rising above 35% of revenue, that signals time to pause hiring or accelerate vendor negotiations before the damage accumulates. This proactive approach stops cost problems from compounding into significant margin erosion.

Data analytics transforms raw cost data into actionable insights by identifying which cost drivers are controllable and which are fixed. A manufacturing client discovered through cost driver analysis that their quality control expenses were rising 3% monthly because they had not adjusted inspection protocols for higher production volumes, not because quality processes were inherently expensive. Once they restructured inspections around volume thresholds, costs stabilized. This insight only emerged because they tracked cost data granularly by function and correlated it with production metrics. Without analytics connecting those dots, they would have assumed quality control was simply becoming more expensive as they scale.

Your technology foundation should prioritize systems that connect your accounting data to operational metrics, not standalone tools that generate reports nobody acts on. Your system should answer three questions automatically each month: where did costs increase, which activities drove those increases, and what should we change next. When technology answers those questions before your next leadership meeting, cost control stops being a reactive exercise and becomes genuinely strategic. The right tools transform cost data from historical records into forward-looking intelligence that shapes how you allocate resources and protect profitability as you expand.

Protecting margins during growth comes down to one fundamental principle: treat cost control as a strategic priority, not an afterthought. The businesses that scale profitably understand their true cost structure, monitor it monthly, and act on what the numbers reveal. They know which costs move with volume and which sit idle, and they manage both categories intentionally as revenue expands.

The cost control strategies outlined here work because they address the real problem-margin erosion does not happen because you grew too fast, but because you stopped paying attention to costs while chasing revenue. Monthly KPI tracking catches problems before they compound, activity-based costing reveals which products and services actually generate profit, and vendor consolidation eliminates waste that inflates expenses during scaling. Technology that connects your accounting data to operational metrics transforms cost management from a reactive exercise into genuine strategy.

If you are scaling and want to protect your bottom line, we at My CPA Advisory and Accounting Partners offer business advisory services designed to help you build the financial discipline that separates profitable growth from hollow expansion. We work with business owners to establish the systems, processes, and accountability structures that keep costs visible and controllable as complexity increases.

Privacy Policy | Terms & Conditions | Powered by Cajabra