Strategic Financial Advisory: Aligning Numbers With Vision

Align your financial strategy with business vision using strategic financial advisory to drive sustainable growth and profitability.

Most people leave thousands of dollars on the table each year simply because they don’t have a salary tax planning strategy. The difference between a haphazard approach and a deliberate one can mean keeping an extra $5,000 to $15,000 annually, depending on your income level.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how small adjustments to deductions, timing, and income coordination add up fast. This guide walks you through the concrete tactics that actually work.

The federal tax system uses seven brackets ranging from 10% to 37%, and this is where most people get confused. Your bracket is not a single rate applied to all your income. Instead, you pay the lowest rate on your first dollars earned, then move progressively upward as you earn more. For 2026, a single filer pays 10% on the first $11,600 of income, then 12% on income between $11,601 and $47,150, and so on up to 37% on income exceeding $640,600. Earning an extra dollar does not suddenly make all your previous income taxable at a higher rate. Only that additional dollar and subsequent dollars face the higher rate. This distinction matters because strategic moves like deferring bonuses or accelerating deductions shift where your last dollars land in the bracket structure, potentially saving thousands.

Your effective tax rate is dramatically lower than your marginal bracket. If you earn $100,000 as a single filer in 2026, your marginal bracket is 22%, but your effective rate is roughly 12%. This gap exists because you pay lower rates on your first dollars. Inflation pushes wages upward annually, and many filers fail to adjust their payroll withholding accordingly, creating bracket creep where you drift into higher brackets without realizing it. The 3.8% Net Investment Income Tax surcharge applies when your modified adjusted gross income exceeds $200,000 for single filers or $250,000 for married couples, meaning more high-income earners hit this surcharge each year. Knowing your exact effective rate helps you decide whether to bunch deductions into one year or spread them across two, and whether deferring income actually saves money or simply delays payment.

The single biggest misconception we encounter is that earning more money always results in paying proportionally more tax. This ignores the power of deductions and credits. Maxing out a 401(k) at $24,500 in 2026 reduces your taxable income dollar-for-dollar, potentially dropping you into a lower bracket or protecting you from the NIIT surcharge. A married couple filing jointly with $300,000 in income can contribute $49,000 combined to retirement accounts, lowering their taxable income to $251,000 and avoiding the NIIT entirely. Strategic charitable giving, using donor-advised funds to bunch donations in high-income years, and timing capital gains recognition across years all let you earn substantially more while paying the same or less tax than someone with lower gross income who ignores these levers. The real opportunity lies in controlling when and how your income becomes taxable, not in limiting your earnings. These deductions and timing strategies form the foundation of what we explore next: the specific moves that reduce your tax burden year after year.

Retirement contributions remain the single most powerful deduction available, and the 2026 limits prove it. A 401(k) contribution limits for 2026 of $24,500 reduces your taxable income dollar-for-dollar, which means a filer in the 24% bracket saves $5,880 in federal tax alone. If you’re 50 or older, add another $8,000 catch-up contribution and you’ve saved an additional $1,920.

For married couples, maximizing both spouses’ 401(k)s at $24,500 each means $49,000 off your taxable income annually.

Traditional IRAs allow $7,500 in contributions for 2026 with a $1,100 catch-up for those 50 and up, though deductibility depends on whether your employer offers a retirement plan and your income level. Health Savings Accounts attached to high-deductible health plans offer triple tax benefits: contributions reduce taxable income, growth happens tax-free, and withdrawals for qualified medical expenses never face tax. A family can contribute $8,750 to an HSA in 2026 with a $1,000 catch-up if someone in the household is 55 or older. These aren’t theoretical savings; they’re immediate reductions in what you owe the IRS.

Home office deductions and business expenses get overlooked by salaried employees and freelancers alike. If you work from home even part-time, you can deduct a portion of rent, utilities, internet, and office supplies proportional to your workspace. The simplified method allows $5 per square foot of dedicated office space, capped at 300 square feet, making it easy to claim $1,500 annually without detailed tracking.

Self-employed individuals and business owners can deduct Section 179 equipment purchases up to $1,190,000 in 2024, allowing you to write off the full cost of computers, furniture, and machinery in the year purchased rather than depreciating them over years. This acceleration of deductions shifts substantial income off your tax return immediately.

Capital gains present another critical opportunity: long-term gains taxed at 0%, 15%, or 20% rates offer substantially better treatment than ordinary income, and timing when you realize those gains matters enormously. If you’re near a bracket threshold, deferring a stock sale to the following year might drop your gains into the 0% bracket entirely.

The number 0% seems to be not appropriate for this chart. Please use a different chart type.

Tax-loss harvesting lets you offset gains with losses, and you can deduct up to $3,000 of net losses against ordinary income each year, carrying forward excess losses indefinitely. This strategy transforms investment setbacks into tax advantages without requiring you to abandon your overall portfolio strategy.

Charitable giving compounds these advantages significantly. Donating appreciated securities held over one year lets you deduct the full fair market value while avoiding capital gains tax completely, a move that saves both income tax and capital gains tax simultaneously on the same dollars. This dual benefit makes charitable contributions far more powerful than most donors realize.

Donor-advised funds allow you to bunch donations in high-income years, claim the deduction immediately, and distribute funds to charities over subsequent years at your own pace. This flexibility lets you maximize deductions when your income spikes without forcing you to commit to specific charities on a tight timeline. These layered strategies-retirement accounts, business deductions, capital gains management, and charitable planning-form the foundation of tax efficiency. The next section examines how timing these moves throughout the year amplifies their impact.

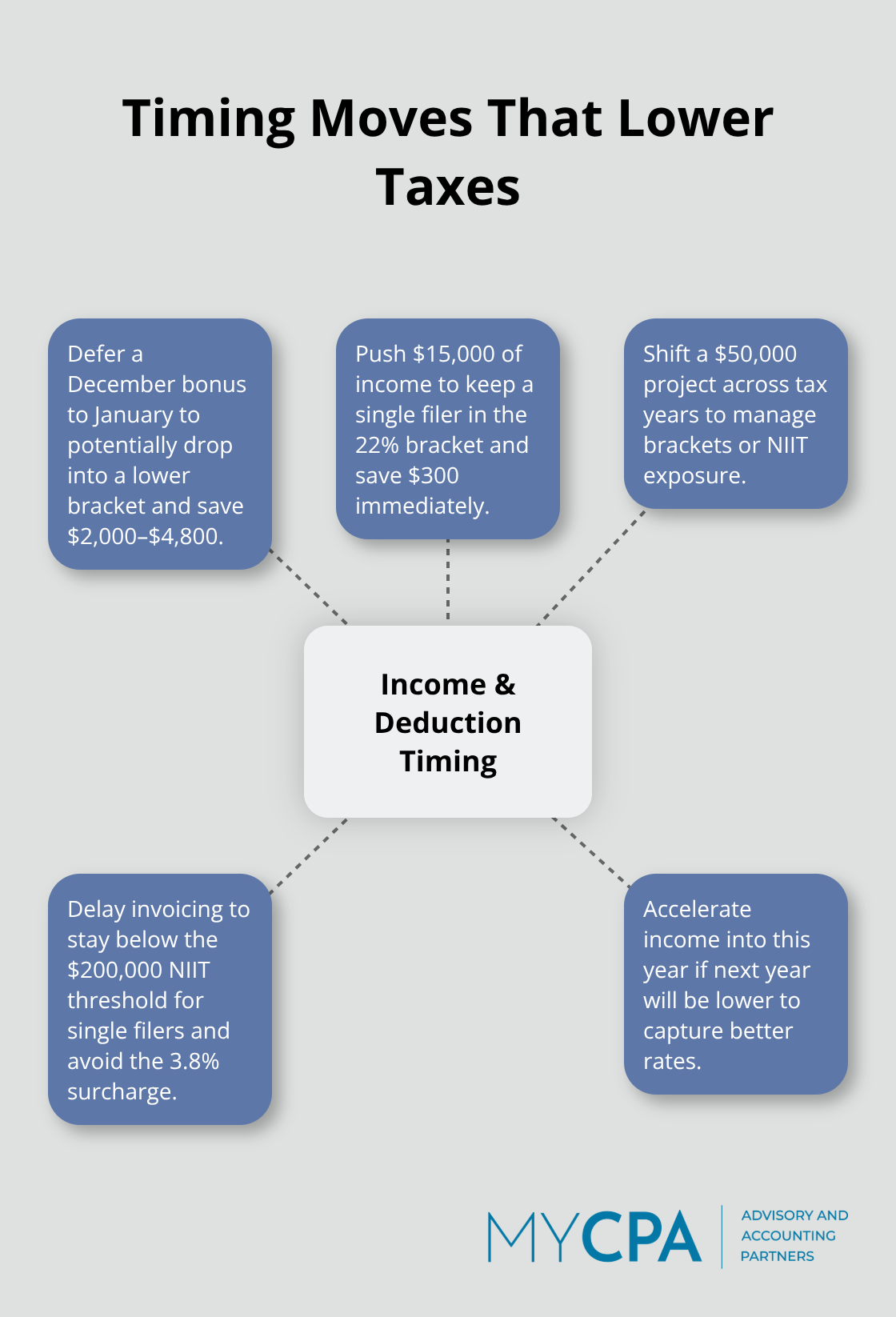

The timing of income and deductions across tax years represents one of the most underutilized levers in salary tax planning. Most employees treat their W-2 income as fixed and unchangeable, but freelancers, business owners, and anyone with variable compensation face real choices about when money lands on their tax return. A salaried employee earning a $20,000 bonus in December could negotiate to receive it in January instead, potentially dropping into a lower bracket and saving $2,000 to $4,800 in federal tax depending on their current marginal rate. This isn’t tax avoidance; it’s tax planning within the rules. The IRS acknowledges that timing matters.

If you’re projected to earn $180,000 this year and cross into the 24% bracket at $191,950 for single filers in 2026, deferring $15,000 in income keeps you in the 22% bracket, saving $300 immediately. For self-employed individuals and freelancers, the stakes climb higher. Completing a $50,000 project in late December versus early January shifts that income to a different tax year entirely. If you expect lower income next year, accelerating the project completion into this year might seem counterintuitive, but it could position you to take advantage of lower brackets or avoid the 3.8% Net Investment Income Tax surcharge that kicks in at $200,000 for single filers.

Conversely, if you’re running a strong income year and approaching the NIIT threshold, deferring client work or delaying invoice collection until January reduces this year’s modified adjusted gross income and eliminates the surcharge entirely. This strategy works particularly well when you control the timing of your income. A freelancer with $210,000 in projected income can defer $15,000 in client work to the following year, landing at $195,000 and avoiding the surcharge on investment income. That single move saves roughly $570 in federal tax without sacrificing any earnings-only their timing.

Deduction timing operates on the same principle with even more flexibility. If you’re considering a major charitable contribution, bunching multiple years of giving into a single high-income year lets you itemize deductions and exceed the standard deduction of $16,100 for single filers in 2026, whereas spreading donations across years might never cross that threshold. Model both scenarios before year-end: itemizing with bunched deductions versus spreading gifts across years and taking the standard deduction. The math often surprises people.

A married couple earning $280,000 with $18,000 in annual charitable intent might donate $36,000 in one year and nothing the next, itemizing at $36,000 plus mortgage interest and state taxes, then taking the standard deduction of $32,200 the following year. This two-year pattern produces more total tax savings than donating $18,000 annually for two years and potentially never itemizing. Donor-advised funds amplify this advantage by allowing you to claim the deduction immediately while distributing funds to charities over subsequent years at your own pace.

Business expenses follow the same logic. If you’re self-employed and considering equipment purchases, Section 179 expensing allows you to deduct the full cost immediately rather than depreciate it over years. Timing that equipment purchase into a high-income year maximizes the deduction’s value in your highest bracket. Conversely, if income dips unexpectedly, deferring the purchase until the following year might anchor the deduction in a lower bracket where it’s worth more.

The most practical approach involves a mid-year tax projection around July that estimates your full-year income, identifies your likely bracket, and flags any approaching thresholds like the NIIT or alternative minimum tax. Once you know where you’ll land, remaining months become actionable: accelerate deductions if you’re in a high bracket, defer income if you’re approaching a threshold, or bunch charitable giving if itemizing makes sense this year but not next. This forward-looking strategy transforms the final six months of your tax year from passive observation into active tax management.

The strategies outlined in this guide-retirement contributions, business deductions, capital gains timing, charitable giving, and income deferral-work because they operate within the tax code itself. You control when and how your income becomes taxable, and a $24,500 401(k) contribution, a strategically timed bonus deferral, or a charitable gift of appreciated securities each reduce your tax bill by hundreds or thousands of dollars annually. The compounding effect across multiple strategies separates people who pay what they owe from people who pay only what they must.

Your salary tax planning strategy succeeds when it aligns with your specific income level, family situation, and goals. Someone earning $120,000 benefits most from maxing retirement accounts and capturing available credits, while a freelancer at $250,000 faces NIIT surcharge exposure and gains far more from income timing decisions. A married couple with significant investment income needs capital gains coordination and charitable planning. Generic advice misses these distinctions entirely.

We at My CPA Advisory and Accounting Partners work with business owners and individuals to build tax-efficient financial plans tailored to your circumstances. Our team combines tax expertise with accounting and business advisory services to identify opportunities you’d otherwise miss and coordinate moves across your entire financial picture. Schedule a consultation with a tax professional who understands your income sources and goals, and bring your prior year return, current income projections, and any major life changes or business developments.

Privacy Policy | Terms & Conditions | Powered by Cajabra