Monthly Close Checklist: Tighten Your Month-End Close

Streamline your month-end accounting with our monthly close checklist. Reduce errors and close faster with proven best practices.

Wealth management tax planning isn’t just about reducing what you owe-it’s about keeping more of what you earn. Most people leave thousands on the table each year by missing straightforward optimization opportunities.

At My CPA Advisory and Accounting Partners, we’ve seen how the right strategy transforms a client’s financial picture. This guide walks you through proven techniques that actually work.

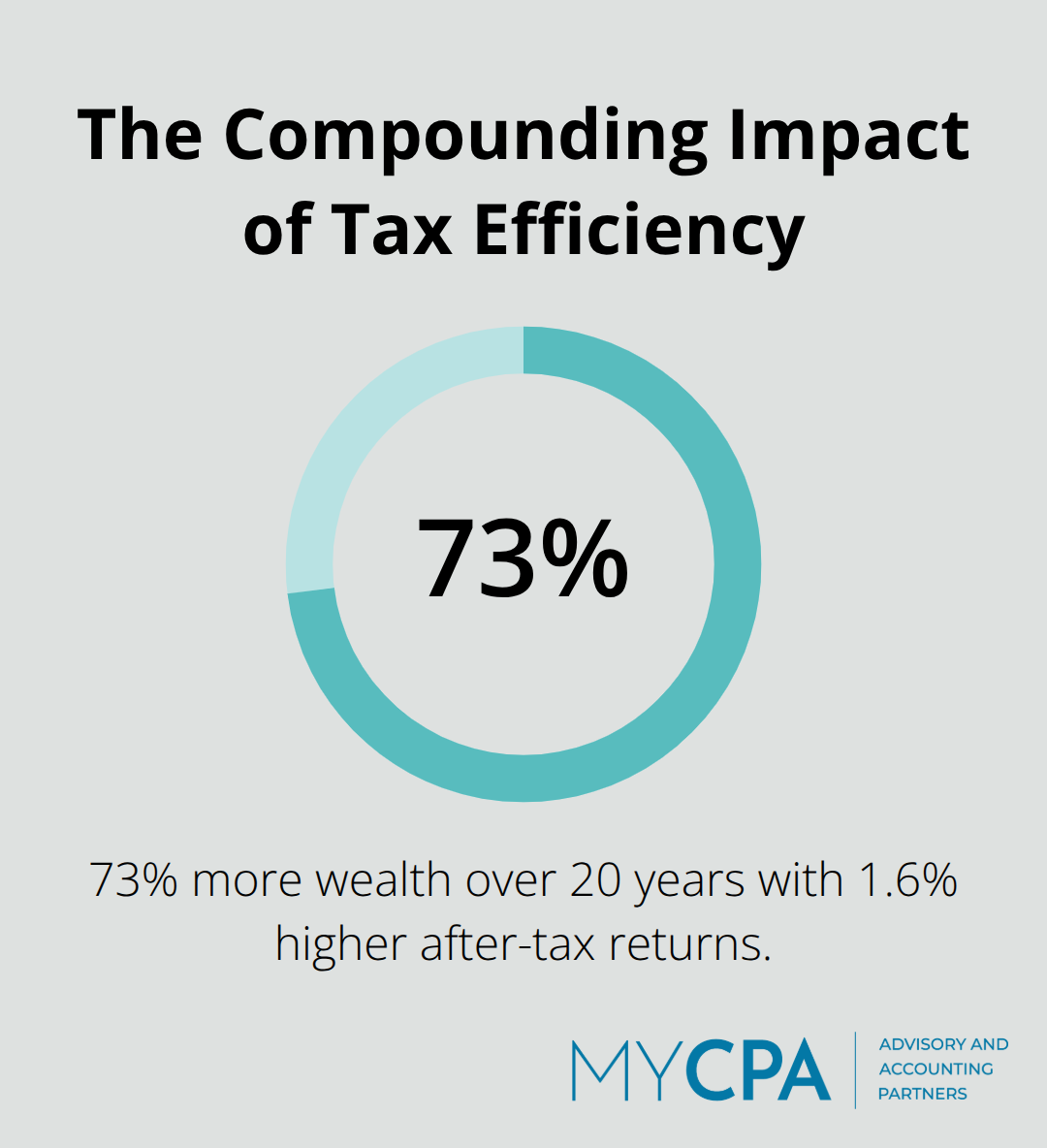

The difference between a good investment portfolio and a tax-efficient one often comes down to three specific decisions: where you hold your investments, how you handle losses, and which accounts you prioritize for contributions. These choices compound over decades. A hypothetical investor earning 1.6% higher after-tax returns annually could accumulate roughly 73% more wealth over 20 years compared to someone ignoring tax efficiency, according to wealth management research. That’s not theoretical-it’s the direct result of intentional strategy.

Most people think about tax-loss harvesting only when markets crash. That’s wrong. You can harvest losses year-round using tax-loss harvesting to offset gains and reduce your current tax bill. When a position declines, you sell it to lock in the loss, then immediately purchase a similar but not identical security to maintain your target allocation. The IRS wash-sale rule requires you to wait 30 days before repurchasing the same security, but direct indexing strategies sidestep this limitation entirely by allowing security-level loss harvesting within your portfolio. This approach works especially well for concentrated stock positions or volatile holdings. Tax-loss harvesting generates what’s called tax alpha-real, measurable returns that don’t depend on market performance. If you hold taxable accounts, this should happen continuously, not once per year.

Asset location means positioning specific investment types in specific account types to minimize taxes. Bonds and income-generating assets belong in tax-advantaged accounts like 401(k)s and IRAs because that income gets taxed at your ordinary rate anyway. Growth assets like equities belong in taxable accounts where long-term capital gains receive preferential tax treatment. This simple reallocation can meaningfully improve after-tax outcomes over time. For 2025, the 401(k) employee deferral limit is $23,500, with a $7,500 catch-up contribution if you’re 50 or older, according to the IRS. Combined with employer contributions, your total can reach $70,000 annually. That’s substantial tax-deferred growth that most people leave untouched. Roth accounts add another layer: contributions grow tax-free with no required minimum distributions at age 73, making them particularly valuable for younger investors or those expecting higher future tax rates.

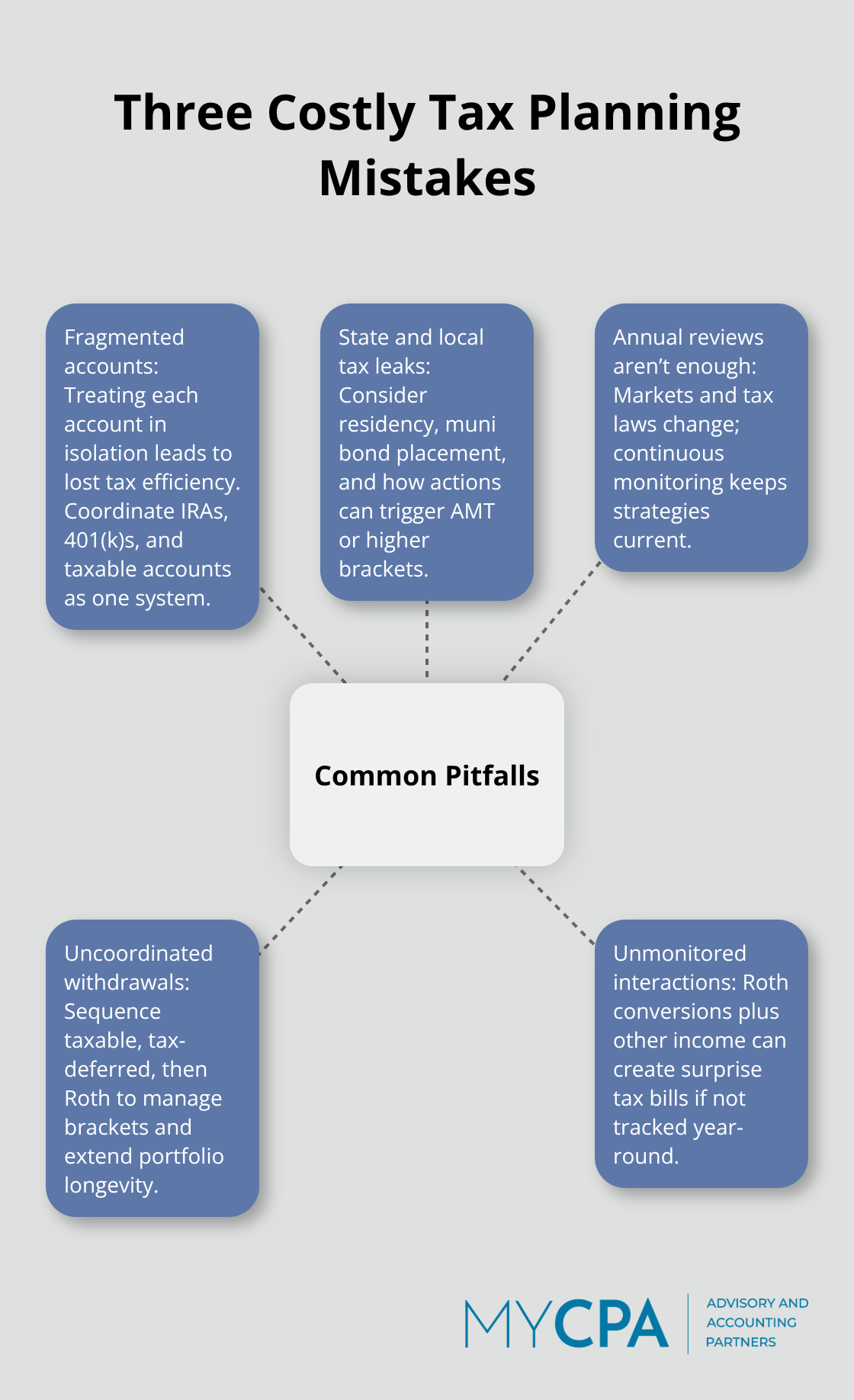

Most high-net-worth individuals maintain several accounts simultaneously-traditional IRAs, Roth IRAs, 401(k)s, and taxable brokerage accounts. Treating these accounts in isolation wastes significant tax-optimization potential. Instead, view them as a unified system where each account type serves a specific purpose. A hybrid strategy, such as converting after-tax 401(k) contributions to a Roth 401(k) in the year they’re contributed, captures benefits of both account types and accelerates tax-free growth. Withdrawal sequencing also matters: taking from taxable accounts first, then tax-deferred accounts, then Roth withdrawals strategically manages your tax brackets and extends your nest egg’s longevity. This coordinated approach transforms your entire portfolio into a tax-optimization machine rather than a collection of separate buckets.

Most high-net-worth individuals maintain multiple investment and retirement accounts spread across different institutions. The fatal mistake is treating each account as independent rather than as part of a coordinated system. You might maximize contributions to your 401(k) while simultaneously making poor asset location decisions in your taxable brokerage account, or you could harvest losses in one account while triggering unnecessary gains in another. This fragmented approach wastes the compounding benefits of tax efficiency.

Clients who’ve accumulated substantial wealth often pay far more in taxes than necessary simply because their accounts don’t work together. The IRS 2025 contribution limits allow $23,500 in 401(k) deferrals, yet many people neglect to use these limits strategically across their entire portfolio. When you coordinate these accounts instead, you transform your entire portfolio into a tax-optimization machine rather than a collection of separate buckets.

State and local taxes compound the coordination problem significantly. If you live in a high-tax state like California or New York but maintain investment accounts in lower-tax jurisdictions, you miss opportunities to optimize your tax residence and account structure. Municipal bonds provide federal tax-exempt interest and potential state tax benefits depending on where you live, but only if you position them intentionally within your overall strategy.

A Roth conversion that makes sense in January might create a devastating tax bill in December if you haven’t accounted for state income tax implications or other income sources triggering the Alternative Minimum Tax. These interactions happen silently across your accounts unless you actively monitor them. Most people discover the damage only when filing their annual return, at which point the opportunity to adjust has passed.

The third critical mistake is treating tax planning as an annual event rather than a continuous process. Markets move, tax laws change, and your personal circumstances shift throughout the year. The Tax Cuts and Jobs Act provisions that benefited individuals expire in 2026, potentially affecting tax rates, SALT deductions, and estate exemptions, yet many people haven’t adjusted their strategies.

Tax-loss harvesting opportunities emerge whenever markets decline or individual holdings underperform, and waiting until December to address this means missing months of potential tax alpha generation. Your withdrawal sequencing strategy needs adjustment whenever your income changes, you receive a bonus, or you approach retirement. A client who maxes out their 401(k) in March faces very different tax planning decisions than someone who defers contributions throughout the year. Quarterly reviews with a qualified advisor catch these timing issues and adapt your strategy to real-world changes. Without this continuous attention, even a well-constructed plan becomes outdated and inefficient within months.

These mistakes-fragmented accounts, overlooked state tax implications, and infrequent reviews-create the conditions where advanced strategies become necessary. The next section shows how high-net-worth individuals move beyond basic tax efficiency to implement sophisticated approaches that generate measurable wealth preservation.

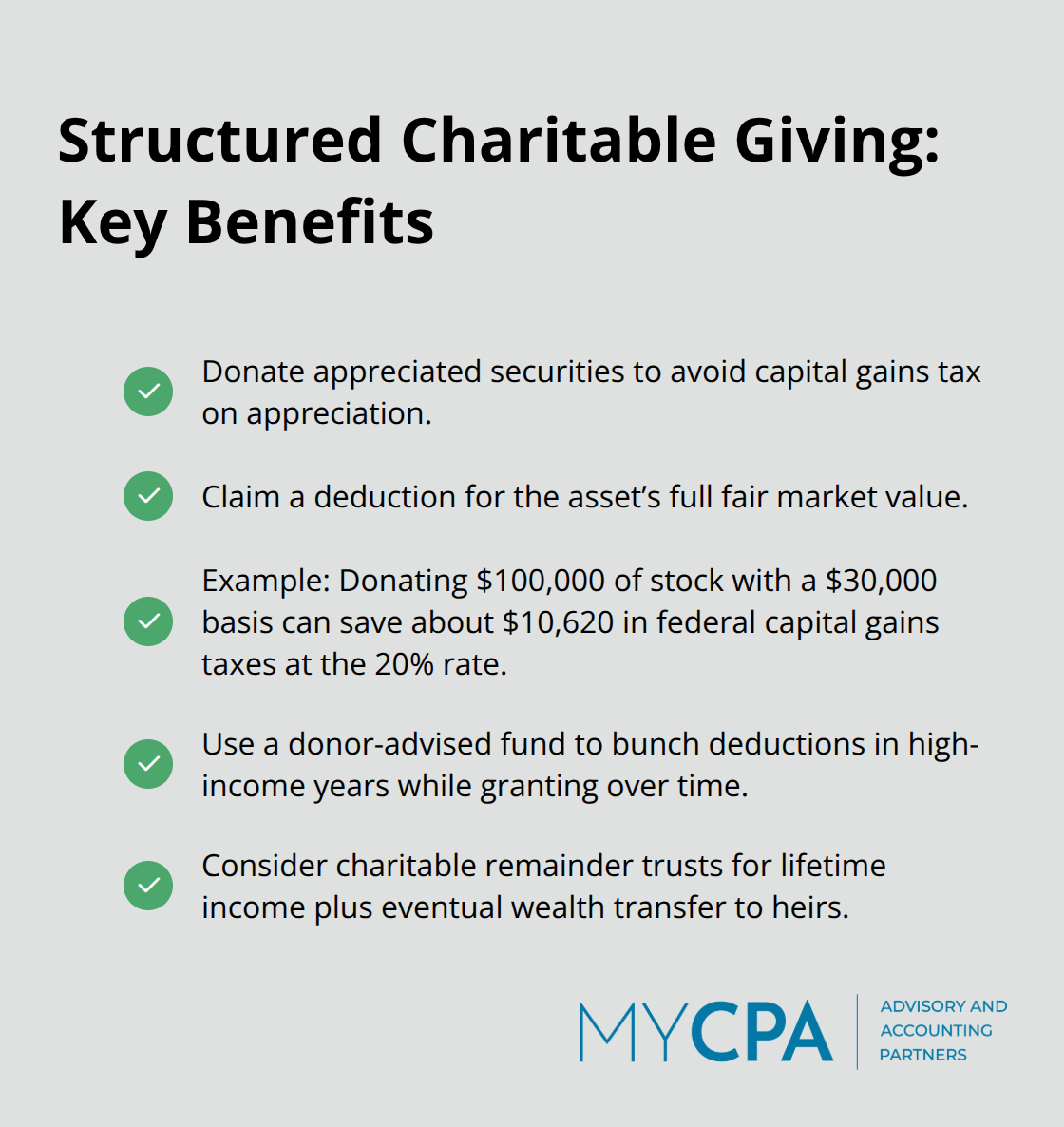

Charitable giving transforms philanthropy into a wealth-transfer mechanism when you structure it correctly. Instead of writing a check from your checking account, donate appreciated securities directly to a charity or donor-advised fund. You avoid capital gains taxes on the appreciation while claiming a deduction for the full fair market value. If you own stock worth $100,000 that cost you $30,000, donating that stock saves you roughly $10,620 in federal capital gains taxes at the 20% long-term rate, plus state taxes depending on your location. That’s money staying in your pocket instead of the IRS’s.

A donor-advised fund lets you contribute appreciated assets in a high-income year, claim the deduction immediately, and distribute to charities over multiple years. This timing flexibility becomes invaluable when you sell a business or realize concentrated gains. For ultra-high-net-worth families, charitable remainder trusts provide lifetime income while passing remaining assets to heirs, creating a dual benefit: immediate income tax deduction plus eventual wealth transfer. The math works especially well for illiquid assets like real estate or private business interests that you’d rather not sell outright.

Your business or investment vehicle’s legal form determines how much you actually keep after taxes. If you operate as a pass-through entity like an S-corporation or LLC, you control when income passes to your personal return, allowing strategic timing around major purchases, charitable contributions, or other deductions. An S-corp election lets you split income between W-2 wages and distributions, potentially reducing self-employment taxes substantially. The IRS requires reasonable W-2 compensation, but distributions above that threshold avoid the 15.3% self-employment tax.

For someone earning $300,000 annually from a service business, optimizing this structure could save $20,000 to $40,000 yearly. This decision alone justifies a conversation with a qualified tax advisor who understands your specific situation and can model the tax impact before you commit to a structure change.

Qualified opportunity zone investments offer a structural advantage that most investors overlook. You can defer capital gains taxes if you invest those gains into designated economically distressed areas, and gains from the opportunity zone investment itself face no tax if held for ten years. These zones exist in every state, making them accessible regardless of location. The combination of deferral plus eventual tax elimination creates a powerful wealth-preservation tool for investors with substantial capital gains.

Entity optimization means positioning investments across multiple legal structures-some in your personal name, others in trusts or entities-to manage basis step-up at death, control liability exposure, and coordinate with your overall estate plan. The decision between holding appreciated assets in your personal name versus inside a trust or family limited partnership affects both current taxes and eventual transfer taxes, yet most people never consider this choice. A trust structure can provide creditor protection while a family limited partnership can facilitate gradual wealth transfer to the next generation at discounted valuations. These structures work together to accomplish multiple objectives simultaneously rather than forcing you to choose between tax efficiency and liability protection.

Tax optimization compounds into substantial wealth preservation because it addresses the actual mechanics of how taxes affect your portfolio: where you hold investments, how you harvest losses, and when you take withdrawals. Implementing even three of these approaches generates measurable after-tax returns that exceed the cost of professional guidance. Coordinating your 401(k), Roth accounts, and taxable investments as a unified system transforms your entire portfolio into a wealth management tax planning machine.

The Tax Cuts and Jobs Act provisions expire in 2026, which will reshape individual tax rates and estate exemptions, making proactive planning essential now rather than later. A qualified advisor catches timing issues, coordinates across multiple accounts, and identifies opportunities specific to your situation that generic strategies miss. We at My CPA Advisory and Accounting Partners understand that wealth management tax planning requires cross-disciplinary expertise spanning tax services, accounting, and business advisory to work effectively.

Schedule a conversation with a tax professional who can review your current account structure, identify coordination gaps, and model the impact of implementing these strategies. My CPA Advisory and Accounting Partners offers tailored tax services and business advisory designed specifically for individuals and business owners seeking tax efficiency and confident financial management. Start with your highest-impact opportunity-whether that’s maximizing 401(k) contributions, implementing tax-loss harvesting, or restructuring how you hold appreciated assets.

Privacy Policy | Terms & Conditions | Powered by Cajabra