Tax Compliance Readiness 2026: A Practical Roadmap for Growing Businesses

Prepare your business for tax compliance readiness in 2026 with our practical roadmap designed for growing companies.

Tax efficiency is a powerful tool for keeping more of your hard-earned money. Many people overlook this aspect of financial planning, potentially leaving thousands of dollars on the table each year.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how strategic tax planning can significantly boost our clients’ financial health. This guide will show you practical ways to maximize your tax efficiency and take control of your financial future.

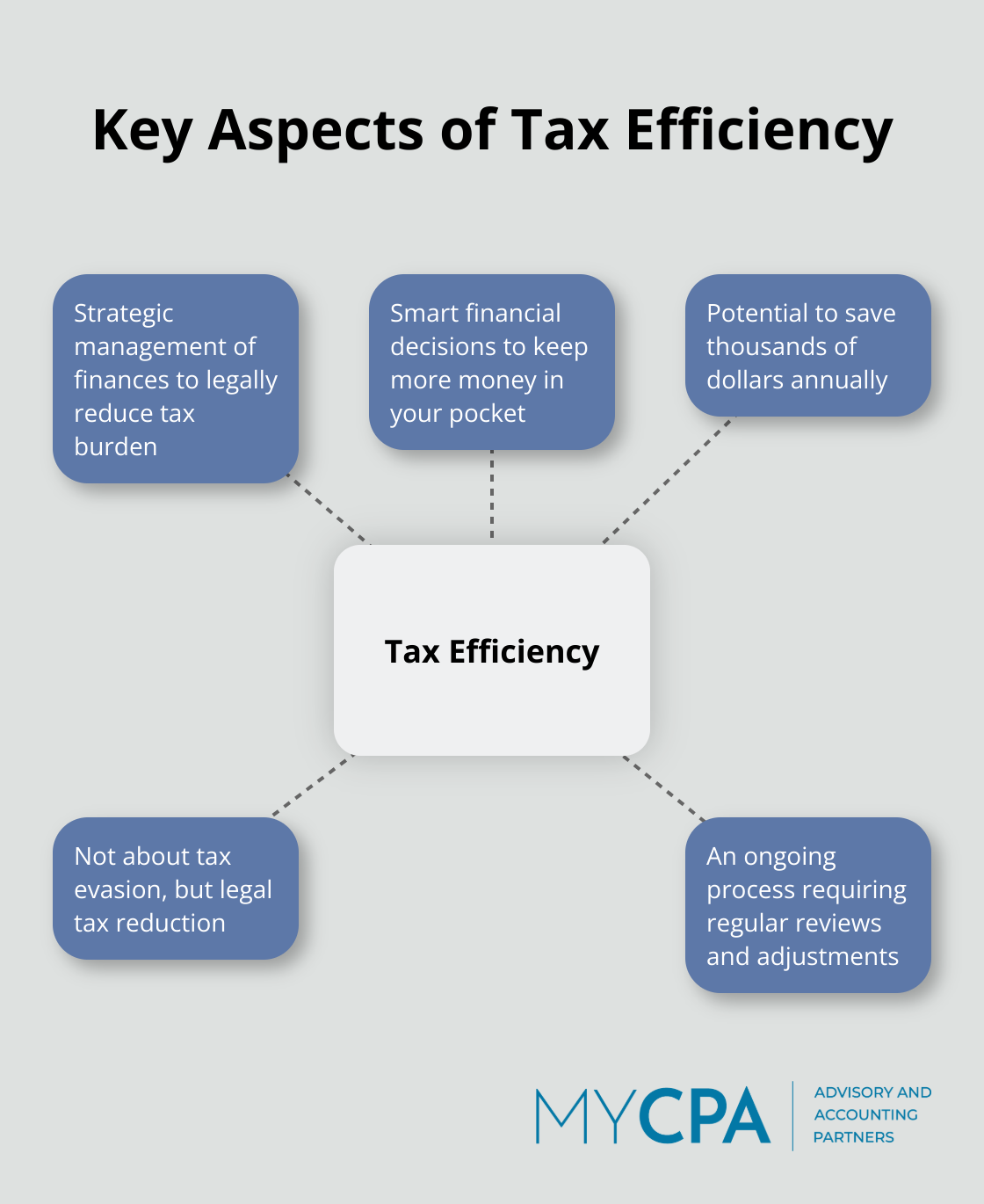

Tax efficiency is the strategic management of finances to legally reduce your tax burden. It’s not about tax evasion, but rather about keeping more money in your pocket through smart financial decisions. This approach can save individuals and businesses thousands of dollars annually.

Many underestimate the power of tax planning. The importance of understanding and applying tax efficiency strategies cannot be overstated.

This misconception couldn’t be further from the truth. Taxpayers at all income levels can benefit from tax efficiency strategies.

While some advanced techniques exist, many effective methods are straightforward. Simply choosing the right type of retirement account can significantly impact your tax bill.

Tax efficiency isn’t a one-time event but an ongoing process. Regular reviews and adjustments to your financial strategy are essential. The right approach can legally reduce your tax burden and keep more of your hard-earned money working for you.

Now that we’ve covered the basics of tax efficiency, let’s explore specific strategies to maximize your tax savings in the next section.

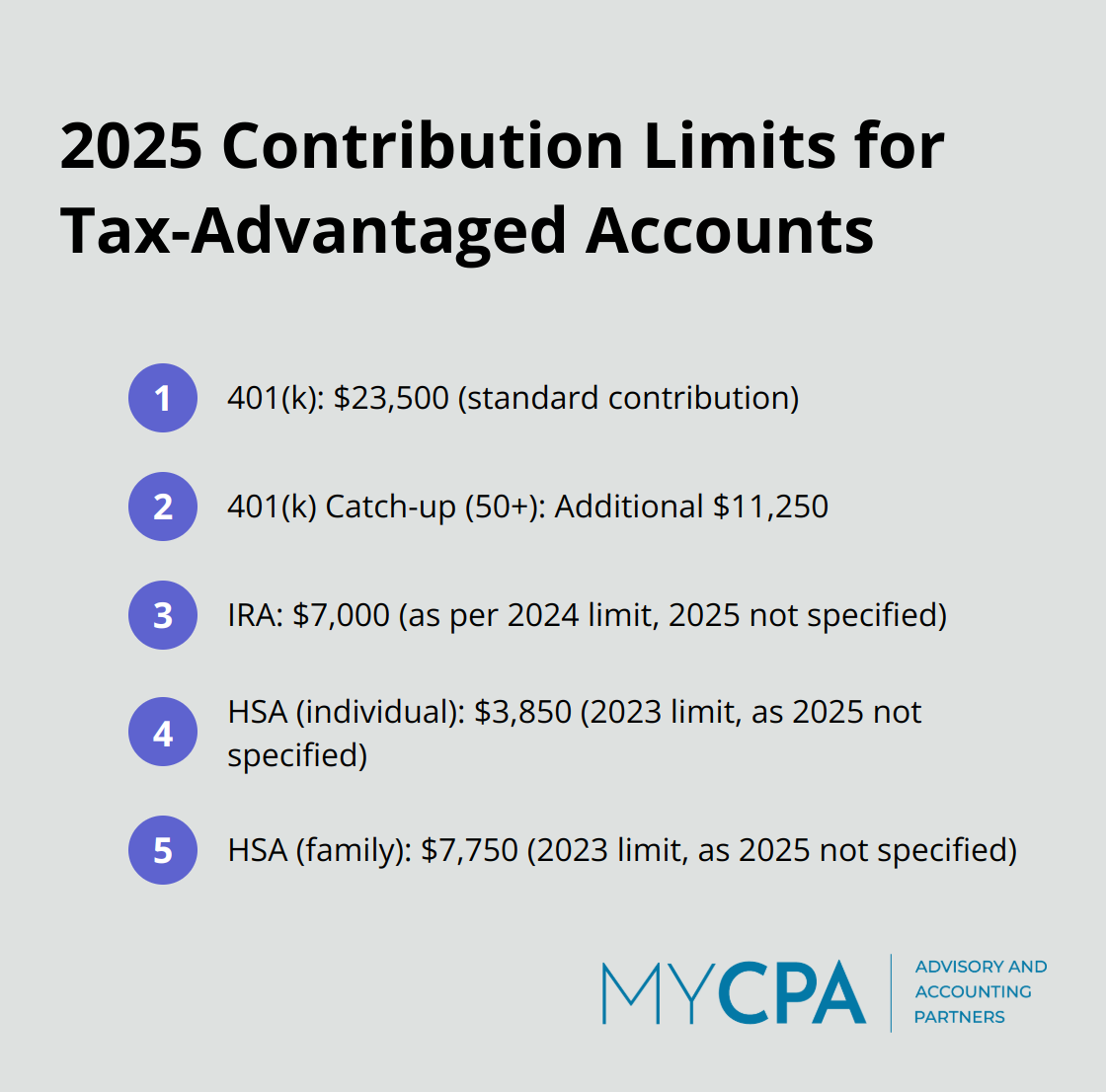

Tax-advantaged accounts serve as powerful tools for tax efficiency. Traditional 401(k)s and IRAs allow pre-tax dollar contributions, which reduce your current taxable income. For 2025, you can contribute up to $23,500 to a 401(k) (with an additional $11,250 catch-up contribution for those 50 or older).

Roth accounts offer tax-free growth and withdrawals in retirement. These accounts prove particularly beneficial if you expect to be in a higher tax bracket in the future.

Health Savings Accounts (HSAs) provide triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Timing plays a critical role in tax planning. Self-employed individuals or those with control over income receipt should consider deferring income to the next tax year if they expect to be in a lower tax bracket. Conversely, accelerating income into the current year could benefit those anticipating a higher bracket next year.

For deductions, bunching strategies can prove effective. This approach involves consolidating deductible expenses into a single tax year to exceed the standard deduction threshold. For example, you might make two years’ worth of charitable contributions in one year, then take the standard deduction the following year.

Your investment strategy significantly impacts your tax bill. Hold investments for more than a year to qualify for long-term capital gains rates (lower than short-term rates).

Consider tax-efficient fund options. Index funds and ETFs typically have lower turnover rates, resulting in fewer taxable events. Municipal bonds can provide tax-free income, especially beneficial for high-income earners in high-tax states.

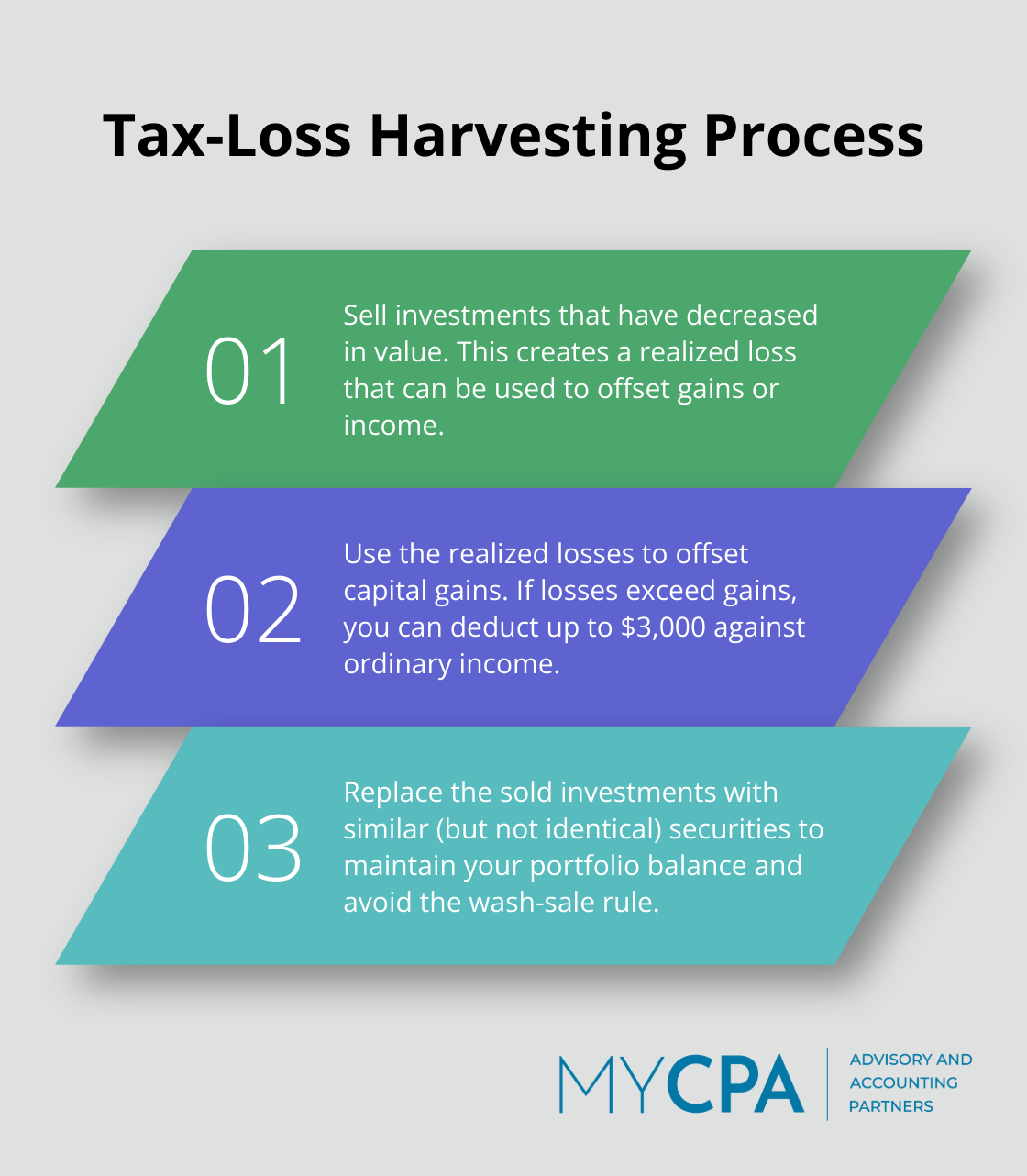

Tax-loss harvesting presents another powerful strategy. This involves selling investments at a loss to offset capital gains.

Tax efficiency requires regular review and adjustment. A proactive approach to tax planning can significantly enhance your financial well-being and keep more of your hard-earned money working for you. In the next section, we’ll explore advanced tax efficiency techniques that can further optimize your financial strategy.

Tax efficiency extends beyond basic strategies. Advanced techniques can significantly reduce your tax burden and optimize your financial strategy. This chapter explores powerful methods to enhance your tax planning.

Tax-loss harvesting allows you to sell investments that are down, replace them with reasonably similar investments, and then offset realized investment gains. The IRS allows investors to deduct up to $3,000 in capital losses against ordinary income each year (with excess carried forward to future years).

Example: If you sell Stock A for a $10,000 gain and Stock B for a $7,000 loss, your net capital gain becomes only $3,000. This technique can substantially lower your taxable income, especially in high-income years.

Caution: The wash-sale rule prohibits claiming a loss on a security if you buy the same or a substantially identical security within 30 days before or after the sale. To avoid this, replace the sold security with a similar (but not identical) investment to maintain your portfolio balance.

Charitable donations support causes you care about and reduce your tax liability. One effective method involves donating appreciated securities instead of cash. This approach allows you to avoid capital gains tax on the appreciation while still claiming a deduction for the full market value of the securities.

For those aged 70½ or older, Qualified Charitable Distributions (QCDs) offer another tax-saving opportunity. Each year, an IRA owner age 70½ or over when the distribution is made can exclude from gross income up to $100,000 of these QCDs. This amount counts towards your Required Minimum Distribution (RMD) but isn’t included in your taxable income.

Another strategy concentrates multiple years’ worth of donations into a single tax year. This may allow you to itemize deductions in that year, potentially exceeding the standard deduction threshold.

For business owners, the right business structure can lead to significant tax savings. Each structure (sole proprietorship, partnership, LLC, S corporation, or C corporation) has unique tax implications.

S corporations can help self-employed individuals save on self-employment taxes. Pay yourself a reasonable salary and take the rest as distributions to potentially reduce your overall tax burden.

LLCs offer flexibility in taxation. They can be taxed as sole proprietorships, partnerships, S corporations, or C corporations, allowing you to choose the most advantageous option for your situation.

C corporations, while facing double taxation on profits and dividends, can benefit high-income business owners due to their flat 21% tax rate on profits.

These advanced strategies require careful planning and expert guidance. A qualified tax professional can tailor these techniques to your individual financial situation, ensuring maximum tax efficiency while maintaining compliance with IRS regulations.

Tax efficiency empowers individuals to keep more of their hard-earned money. Strategic approaches can significantly reduce tax burdens and optimize financial situations. My CPA Advisory and Accounting Partners specializes in helping clients achieve optimal tax efficiency through personalized guidance and comprehensive services.

We offer expert assistance to navigate the complex world of tax planning. Our team works proactively throughout the year to implement effective strategies and support informed financial decisions. We tailor our approach to each client’s unique circumstances, goals, and risk tolerance.

Don’t leave money on the table – prioritize tax efficiency in your financial planning. Visit our website to learn how we can help you maximize your tax savings and achieve your financial goals. With our expertise, you can face tax season confidently and make the most of every opportunity to save.

Privacy Policy | Terms & Conditions | Powered by Cajabra