Monthly Close Process: Streamline Your Bookkeeping

Streamline your monthly close process with practical steps to organize bookkeeping, reduce errors, and close your books faster each month.

At My CPA Advisory and Accounting Partners, we know that smart tax planning can save you money. The goal of tax planning is tax minimization, which means legally reducing your tax burden.

Effective strategies can help you keep more of your hard-earned income while staying compliant with tax laws. In this post, we’ll explore practical ways to minimize your taxes and set you up for long-term financial success.

Tax minimization represents a legal strategy to reduce tax liability. At My CPA Advisory and Accounting Partners, we help clients pay the lowest amount of taxes permitted by law. This approach stands in stark contrast to tax evasion, which is illegal and carries severe penalties.

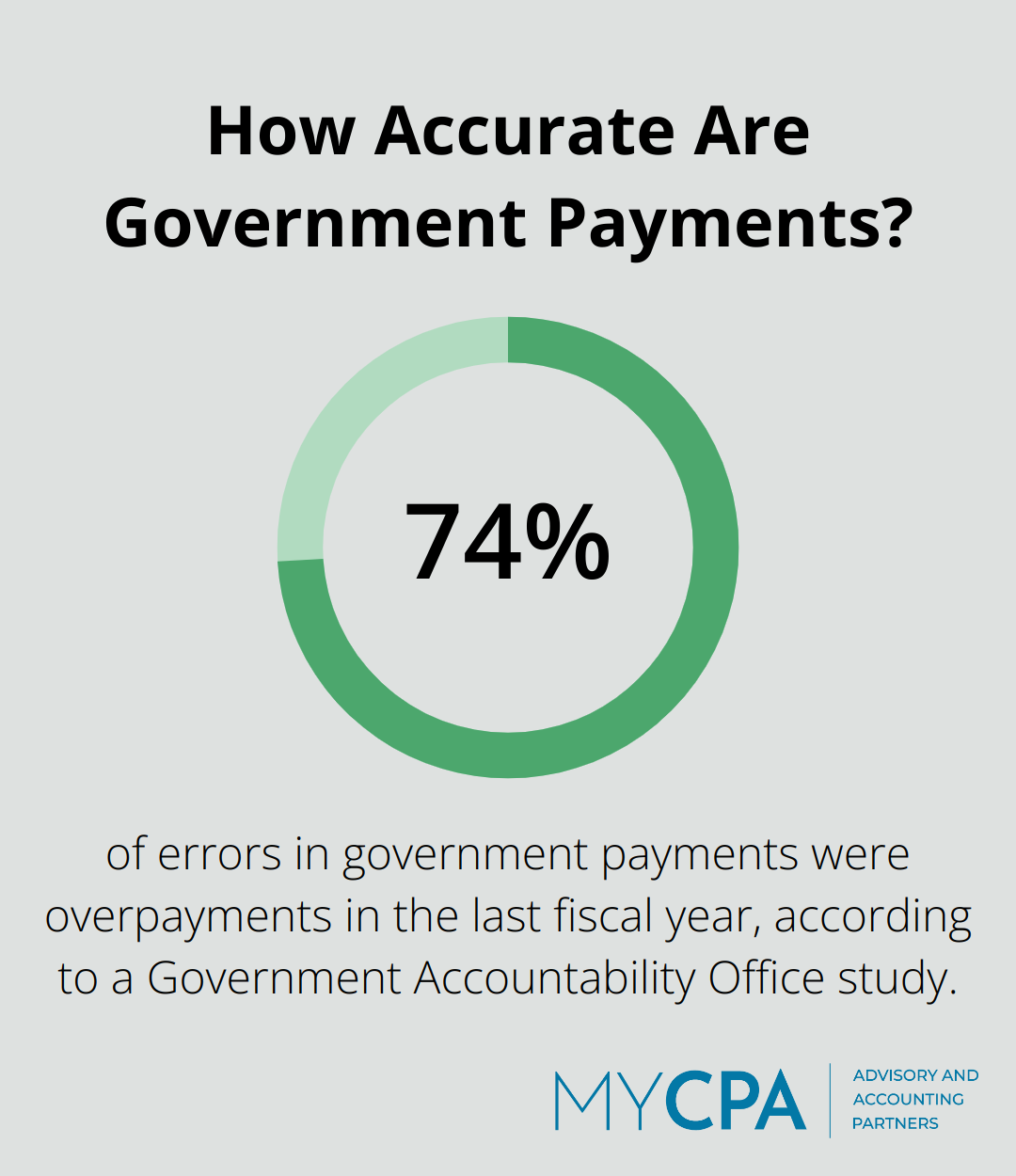

Effective tax planning plays a vital role for individuals and businesses alike. It leads to substantial savings and improved cash flow. A Government Accountability Office study revealed that more than $175 billion (74%) of errors were overpayments in the last fiscal year. This statistic underscores the need for a proactive approach to tax management.

Tax planning extends beyond the current year. It involves creating a long-term strategy that aligns with financial goals. Smart tax strategies allow for reinvestment of savings into business or personal wealth-building activities.

Many people incorrectly believe that tax minimization only benefits the wealthy or large corporations. This myth overlooks the fact that taxpayers across all income levels can profit from proper tax planning. The key lies in working with a knowledgeable professional who understands the tax code and applies it to specific situations.

Another prevalent misconception is that tax minimization always involves complex schemes. While some strategies can be intricate, many remain straightforward. For instance, maximizing contributions to retirement accounts or timing income and expenses (two simple yet effective methods) can result in substantial tax savings without unnecessary complexity.

Navigating the ever-changing tax landscape presents challenges. Tax laws are complex and undergo frequent updates. Taxpayers face a number of issues due to critical tax law changes that took place in 2022 and ongoing challenges related to the pandemic. This constant flux highlights the importance of working with a tax professional for effective tax minimization.

A skilled CPA identifies opportunities that might otherwise go unnoticed. They stay current with tax law changes and apply this knowledge to unique financial situations. This expertise leads to significant savings and helps avoid costly mistakes.

As we move forward, we’ll explore specific strategies that can help you achieve meaningful tax minimization. These practical approaches will set the foundation for long-term financial success and optimal tax efficiency.

Tax minimization benefits taxpayers across all income levels. Implementing effective strategies can help you reduce your tax burden legally and keep more money in your pocket. Let’s explore some practical approaches to optimize your tax situation.

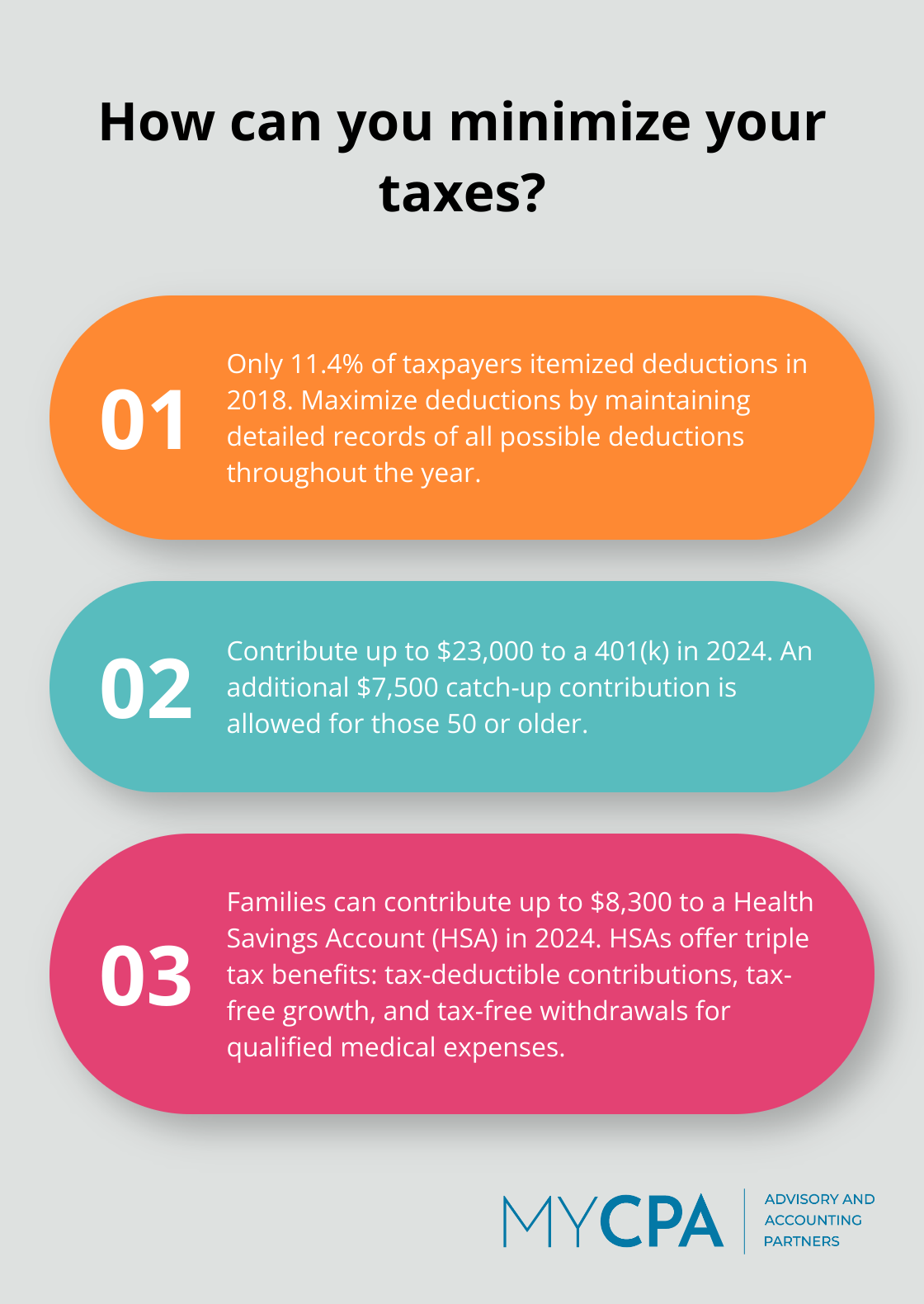

The first step in tax minimization involves claiming every deduction you’re entitled to. Many taxpayers overlook common deductions such as charitable contributions, medical expenses, and home office deductions for self-employed individuals. According to IRS statistics, only 11.4% of taxpayers itemized their deductions in the 2018 tax year. Don’t miss out on potential savings – maintain detailed records of all possible deductions throughout the year.

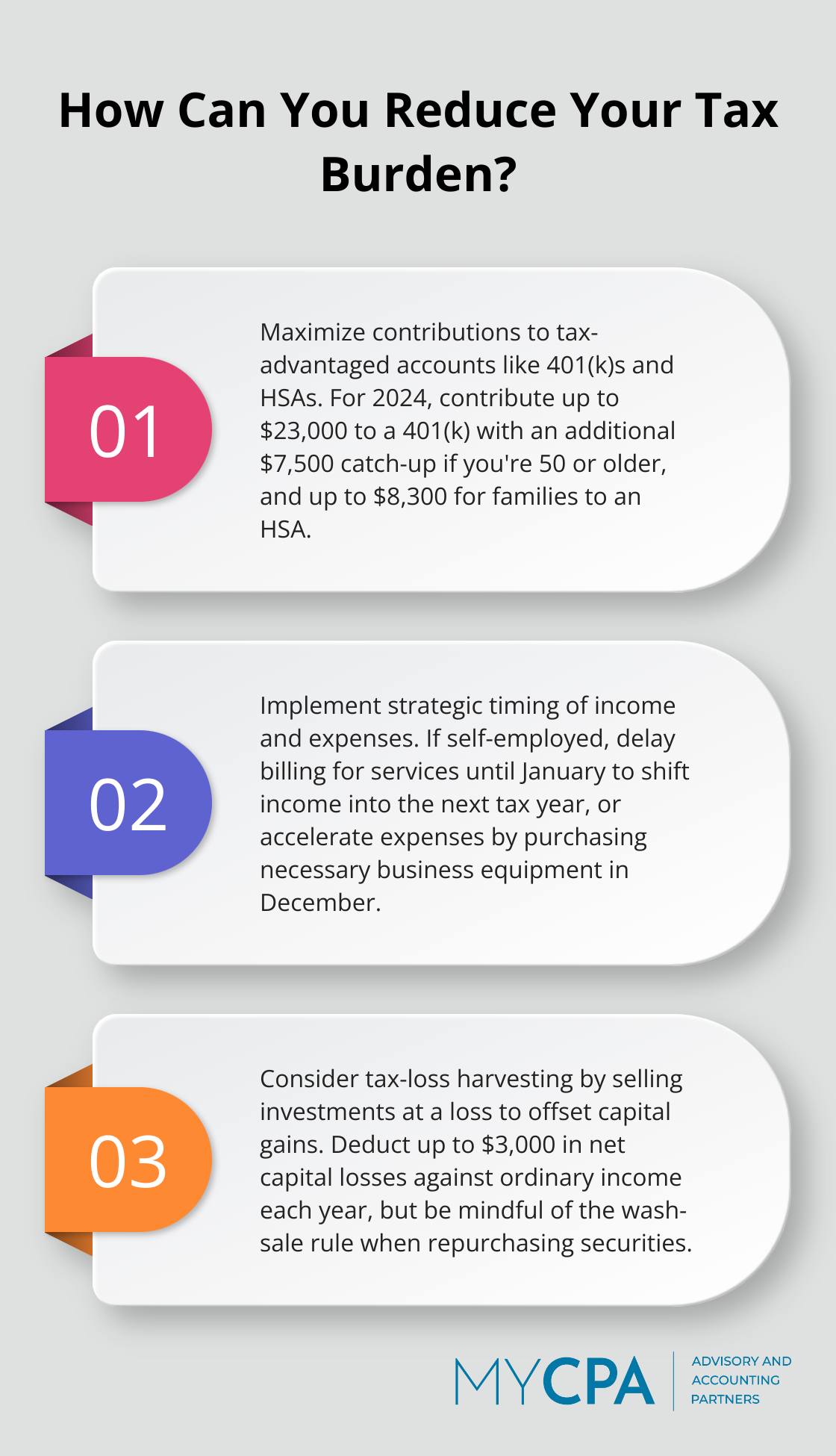

Strategic timing of income and expenses can significantly impact your tax bill. Self-employed individuals should consider delaying billing for services until January to shift income into the next tax year. Alternatively, you might accelerate expenses by purchasing necessary business equipment in December rather than waiting until the new year. This approach helps manage your tax bracket and potentially reduces your overall tax liability.

Utilizing tax-advantaged accounts offers a powerful way to reduce your taxable income. Maximize contributions to your 401(k) or IRA. For 2024, you can contribute up to $23,000 to a 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older. Health Savings Accounts (HSAs) provide triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. In 2024, families can contribute up to $8,300 to an HSA (a significant opportunity for tax savings).

Business owners should choose the right business structure to achieve significant tax savings. Each structure – sole proprietorship, partnership, LLC, S corporation, or C corporation – carries different tax implications. For example, an S corporation can help you avoid self-employment taxes on a portion of your income. However, the optimal structure depends on your specific situation. A thorough analysis of your unique circumstances will determine the most tax-efficient structure for your business.

For investors, tax-loss harvesting presents an effective strategy. This involves selling investments at a loss to offset capital gains. The IRS allows you to deduct up to $3,000 in net capital losses against your ordinary income each year, with any excess carried forward to future years. This strategy requires careful planning and consideration of the wash-sale rule (which prohibits repurchasing a substantially identical security within 30 days).

While these strategies provide a solid foundation for tax minimization, implementing them effectively requires expert knowledge of tax laws and careful planning. Working with a professional can help you develop a comprehensive tax minimization plan tailored to your specific financial situation. In the next section, we’ll discuss the benefits of partnering with a CPA and how professional guidance can enhance your tax minimization efforts.

CPAs offer invaluable knowledge and experience in tax minimization. They maintain current understanding of tax laws and regulations, which allows their clients to benefit from the latest tax-saving opportunities. A CPA analyzes individual financial situations and develops custom strategies to reduce tax burdens.

For instance, a CPA might uncover industry-specific tax credits that clients were unaware of. The Research and Development (R&D) tax credit (often overlooked) can provide substantial savings for businesses engaged in qualifying activities.

The upfront cost of hiring a CPA often pales in comparison to the potential tax savings and time preserved. CPAs handle complex tax situations efficiently, which reduces the risk of errors that could lead to costly audits or penalties. In fiscal year 2023, the IRS closed 582,944 tax return audits, resulting in $31.9 billion in recommended additional tax. Working with a CPA helps clients avoid becoming part of these statistics.

Effective tax minimization requires ongoing attention and adjustments, not just a once-a-year event. CPAs provide year-round support to help clients make informed financial decisions that impact their tax situation. They advise on the tax implications of major life events, such as buying a home, starting a business, or planning for retirement.

CPAs often specialize in specific industries, which allows them to provide targeted advice. This specialized knowledge can lead to significant tax savings. For example, a CPA with expertise in real estate can guide clients through complex tax rules related to property investments, depreciation, and 1031 exchanges.

In the event of an audit, a CPA proves invaluable. They represent clients before the IRS, handle correspondence, and navigate the complexities of the audit process. This support not only reduces stress but also increases the likelihood of a favorable outcome.

Tax minimization through effective planning empowers financial success. We explored strategies from maximizing deductions to optimizing business structures, which can lead to significant savings when implemented correctly. The goal of tax planning is tax minimization, and this objective extends beyond a single tax year, offering long-term benefits that compound over time.

Implementing a comprehensive tax minimization plan requires expertise and ongoing attention. While some strategies may seem straightforward, the complexities of tax laws (and frequent changes in regulations) make professional guidance invaluable. Working with a CPA ensures you take advantage of all available opportunities while remaining compliant with tax laws.

At My CPA Advisory and Accounting Partners, we help individuals and businesses achieve optimal tax efficiency. Our team of experts provides personalized strategies tailored to your unique financial situation. Take the first step towards financial optimization by partnering with My CPA Advisory and Accounting Partners for comprehensive tax minimization and financial management.

Privacy Policy | Terms & Conditions | Powered by Cajabra