Monthly Close Checklist: Tighten Your Month-End Close

Streamline your month-end accounting with our monthly close checklist. Reduce errors and close faster with proven best practices.

IRS penalties can cost your business thousands of dollars-and they’re often preventable. Most business owners make the same compliance mistakes repeatedly, from misclassifying workers to poor record-keeping.

We at My CPA Advisory and Accounting Partners have helped countless clients achieve IRS compliance readiness by fixing these problems before audits happen. This guide shows you exactly what mistakes to avoid and how to strengthen your compliance position.

Worker misclassification tops the IRS enforcement list for small and mid-sized businesses. The IRS increased scrutiny on pass-through entities like partnerships and S corporations in 2025, and misclassifying employees as independent contractors remains their primary target. When you classify a W-2 employee as a 1099 contractor, you avoid payroll taxes, but the IRS catches this through income reporting mismatches. A single misclassification can trigger back taxes and penalties under IRC § 6694, and interest that compounds monthly.

The distinction matters legally: employees receive direction and control from you, work exclusively for your business, and depend on you for benefits. Contractors set their own hours, serve multiple clients, and handle their own taxes. If the IRS reclassifies your workers, you owe employment taxes for the past three years plus penalties, depending on whether the error was negligent or willful. The safest approach involves documenting how each worker operates and aligning their classification with IRS guidelines, not with what saves you money short-term.

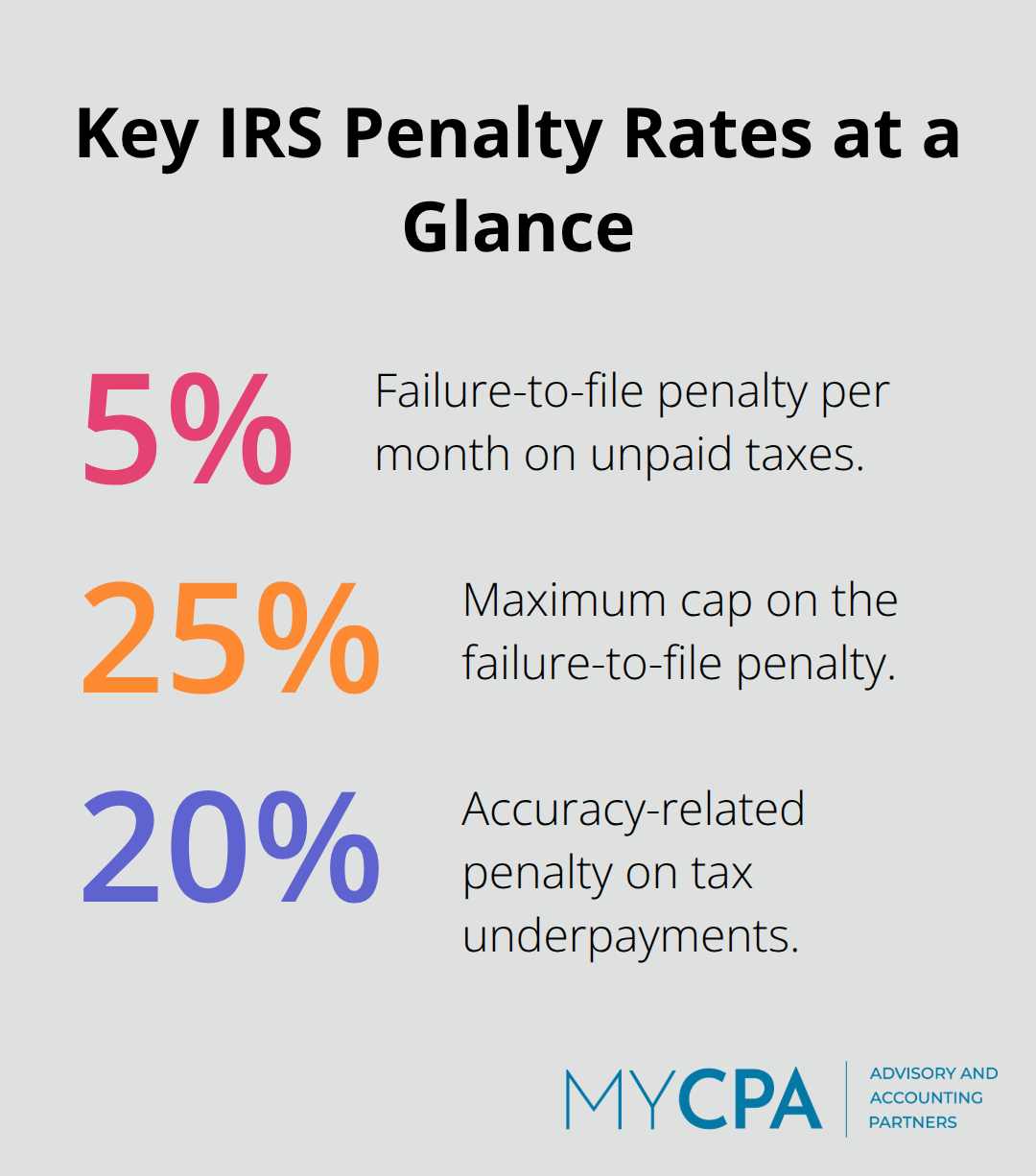

Form W-2 and 1099 filing deadlines arrive in January every year, but many business owners miss them or file incorrect information. The IRS charges information return penalties for late or inaccurate information returns: $60 per return in 2025 with a maximum of $31,500. These penalties accumulate rapidly if you have ten employees and miss the deadline. Failure to file your business tax return by April 15 triggers additional penalties of 5% of unpaid taxes per month, capped at 25%.

When you combine information return penalties with failure-to-file penalties, a single year of missed deadlines costs tens of thousands. Payroll tax deposits follow their own schedule: federal payroll taxes are due either weekly or semi-weekly depending on your payroll size. Missing even one deposit triggers a failure-to-deposit penalty ranging from 2% to 15% of the unpaid amount. The IRS does not negotiate these timelines, and extensions to file do not extend the time to pay. Set automatic reminders for January, April, June, and September to stay on track with estimated taxes and quarterly filings.

The IRS expects you to retain records for at least seven years, yet many business owners mix personal and business expenses or keep scattered receipts. When an audit occurs, the IRS examines your books for inconsistencies: mismatched income between your records and third-party reports like PayPal or Stripe 1099-Ks, unsupported expense claims, and missing documentation. If you cannot produce receipts or invoices for claimed deductions, the IRS disallows them outright, and you owe back taxes plus accuracy-related penalties of 20% of the underpayment.

Digital payment processors now issue 1099-Ks to both you and the IRS, so your records must align exactly. Many business owners claim vehicle expenses, meals, or office supplies without tracking them properly, creating red flags during examination. A dedicated business bank account and bookkeeping software like QuickBooks Online prevent mixing personal and business transactions. Poor record-keeping also slows your response to IRS correspondence and extends audit timelines, increasing stress and professional fees.

These three mistakes-worker misclassification, missed deadlines, and inadequate documentation-form the foundation of most IRS enforcement actions. Fixing them now positions your business to withstand scrutiny and move forward with confidence. The next section shows you exactly how to organize your financial records and implement systems that prevent these problems from taking root.

The gap between filing taxes and being audit-ready is enormous. Filing means submitting forms by the deadline; audit-readiness means your documentation can withstand IRS scrutiny without scrambling for missing receipts or explanations. Most business owners operate in filing mode and ignore the systems that prevent audits altogether.

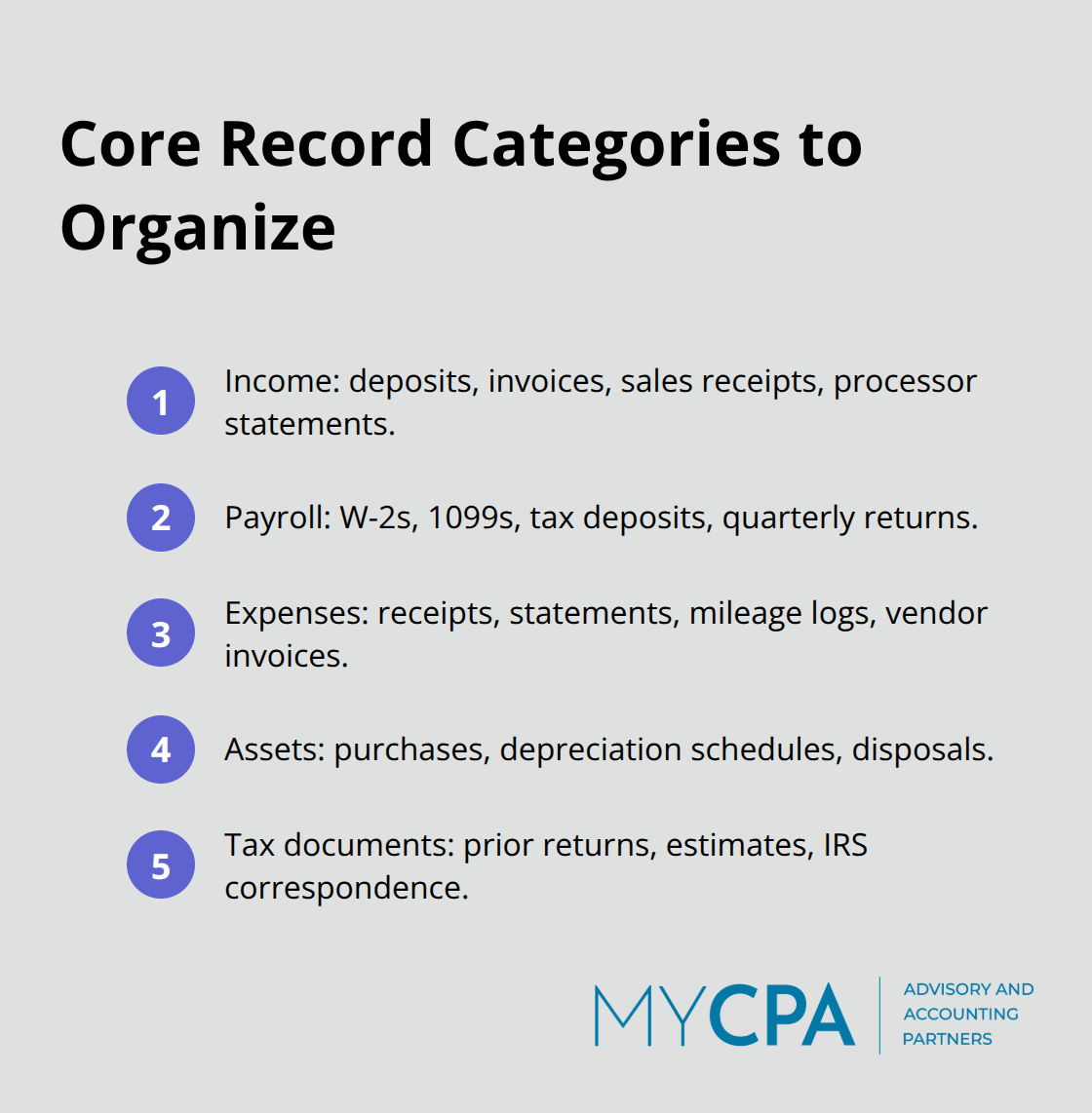

The IRS expects you to retain records for at least seven years according to federal retention rules, and your records must match third-party reports like 1099-Ks from payment processors and W-2s from payroll. Start by separating your financial life into distinct categories: income, payroll, expenses, assets, and tax documents. Income records include bank deposits, invoices, sales receipts, and payment processor statements from Stripe or PayPal. Payroll records contain W-2s, 1099s issued to contractors, payroll tax deposits, and quarterly payroll tax returns.

Expense records cover receipts, credit card statements, mileage logs, and vendor invoices organized by type (utilities, supplies, professional services, meals). Asset records track equipment purchases, depreciation schedules, and disposal documentation. Tax documents include prior year returns, estimated tax payments, and correspondence with the IRS.

Organizing by both category and year prevents you from hunting through thousands of files during an audit. Use cloud storage with version control so you can track changes and access files from anywhere. If you operate in multiple states, maintain separate folders for each state’s sales tax filings and nexus documentation. The IRS looks for consistency between your records and what third parties report, so mismatches trigger deeper examination.

Bookkeeping consistency matters more than perfection. Many business owners use QuickBooks Online or similar software but fail to reconcile accounts monthly or categorize transactions correctly, creating a mess that looks suspicious during audit. Reconciliation means comparing your bank statement to your accounting records each month and investigating discrepancies immediately.

If you deposited $50,000 in income but your records show $45,000, that five-thousand-dollar gap compounds into a major red flag. Assign the same person or team to handle bookkeeping so coding and entry methods remain consistent year-over-year. The IRS notices when expense categories change dramatically or when similar transactions are coded differently across months. Set a monthly calendar reminder to reconcile accounts before the next month begins.

Conduct a quarterly review where you examine income against your records, verify all payroll deposits match your bank, and confirm expense categories are reasonable. During these quarterly reviews, look for duplicate entries, unusual transactions, and gaps in documentation. If you discover a missing receipt for a claimed deduction, obtain supporting documentation immediately rather than hoping the IRS doesn’t ask.

Internal controls with written approval policies for large expenses and documented procedures for recording transactions create a paper trail that demonstrates good-faith compliance. The IRS views businesses with strong internal controls as lower-risk, which can shorten audit timelines and reduce penalty exposure significantly. These systems protect you far more than last-minute scrambling when an audit notice arrives.

The systems you build now determine whether you survive an audit or face devastating penalties. Most business owners wait until an IRS notice arrives to address compliance gaps, but that reactive approach costs far more than proactive planning. We at My CPA Advisory and Accounting Partners work with business owners throughout the year to identify risks before the IRS does, fix documentation issues quietly, and align your records perfectly with what third parties report to the agency.

Our tax services start with a comprehensive review of your current structure, payroll practices, and record-keeping methods to spot misclassifications, missed deadlines, and documentation weaknesses that trigger audits. Many clients discover they’ve operated with significant compliance gaps for years without realizing it until we conduct this assessment. We then implement tailored financial plans that address your specific vulnerabilities rather than applying generic solutions that miss your actual exposure.

If you operate in multiple states, we verify your sales tax nexus obligations and confirm you file in every jurisdiction where you have economic presence. If you’ve hired contractors, we review worker classification against IRS guidelines to confirm each person is coded correctly, preventing the back-tax bills that plague misclassified arrangements. We also coordinate your QuickBooks setup and management so your bookkeeping remains consistent throughout the year, eliminating the chaotic reconciliations and categorization errors that invite deeper IRS examination.

Our cross-disciplinary expertise means we coordinate payroll compliance, sales tax filing, estimated tax deadlines, and financial reporting across all your obligations so nothing falls through the cracks. This coordinated approach eliminates the stress of tracking multiple deadlines independently and reduces the likelihood that a single missed filing triggers a cascade of penalties.

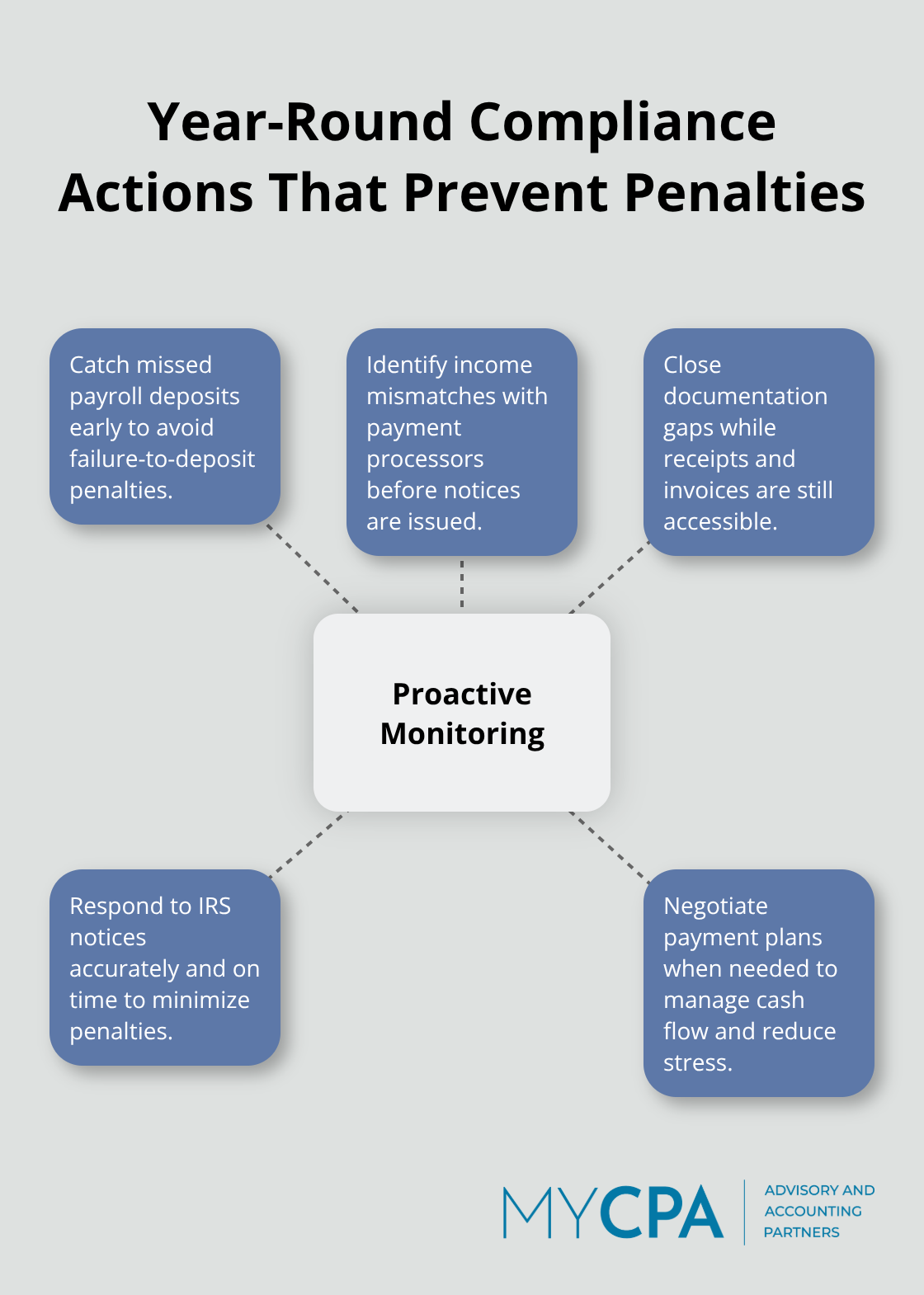

Throughout the year, we monitor your compliance position rather than checking in only at tax time. This proactive engagement means we catch missed payroll deposits, identify income reporting mismatches with payment processors, and address documentation gaps while you can still gather supporting records. If you receive an IRS notice, we provide expert representation and support to respond accurately and on time, reducing penalties and negotiating payment plans when necessary.

When an audit occurs, having prepared documentation and consistent records dramatically shortens the examination timeline and demonstrates your good-faith compliance efforts to the IRS, which can result in reduced penalties or removal altogether if reasonable cause is established.

IRS compliance readiness requires consistent systems, accurate records, and proactive monitoring throughout the year to catch problems before penalties arrive. The three mistakes covered in this guide-worker misclassification, missed deadlines, and poor documentation-account for the majority of IRS enforcement actions against small and mid-sized businesses. Fixing these issues now protects your business from thousands in back taxes, penalties, and interest that compounds monthly until paid in full.

Building audit-ready records takes effort upfront, but the payoff proves substantial. When you organize financial documents by category and year, reconcile accounts monthly, and implement internal controls with written approval policies, you create a defensible position that withstands IRS scrutiny. Consistency in bookkeeping, accurate income reporting that matches third-party processor statements, and proper worker classification eliminate the red flags that trigger deeper examination.

We at My CPA Advisory and Accounting Partners help business owners identify compliance gaps before the IRS does and coordinate obligations across payroll, sales tax, and estimated tax deadlines. Conduct a compliance review of your current structure, worker classifications, and record-keeping practices, then implement the systems outlined in this guide-or contact us for a professional compliance assessment that reveals gaps costing far more to fix later.

Privacy Policy | Terms & Conditions | Powered by Cajabra