Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Tax filing season brings stress for most business owners. Between missed deductions, expense misclassifications, and disorganized records, thousands of dollars slip away unnecessarily each year.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how tax filing improvements transform a chaotic process into a streamlined one. This guide shows you exactly how to file faster, more accurately, and with significantly lower tax bills.

Business owners lose thousands annually because they confuse what qualifies as a legitimate business expense. The IRS distinguishes between personal expenses and business deductions with strict rules, and misclassifying even a few items can trigger audits or penalty assessments. A common mistake involves treating mixed-use expenses as fully deductible. If you use your car partly for personal errands and partly for client meetings, only the business percentage qualifies. The IRS expects you to track actual mileage or maintain detailed logs. Home office deductions follow similar logic: you can deduct rent, utilities, or mortgage interest only for the square footage you genuinely use for business, not your entire house.

Another frequent error involves meals and entertainment. The rules shifted significantly, and many business owners still claim 100% of client lunches when only 50% is deductible under current tax law. Personal expenses disguised as business costs create the highest audit risk. Clothing, commuting, and hobby-related purchases frequently get flagged because owners incorrectly assume any work-related purchase qualifies.

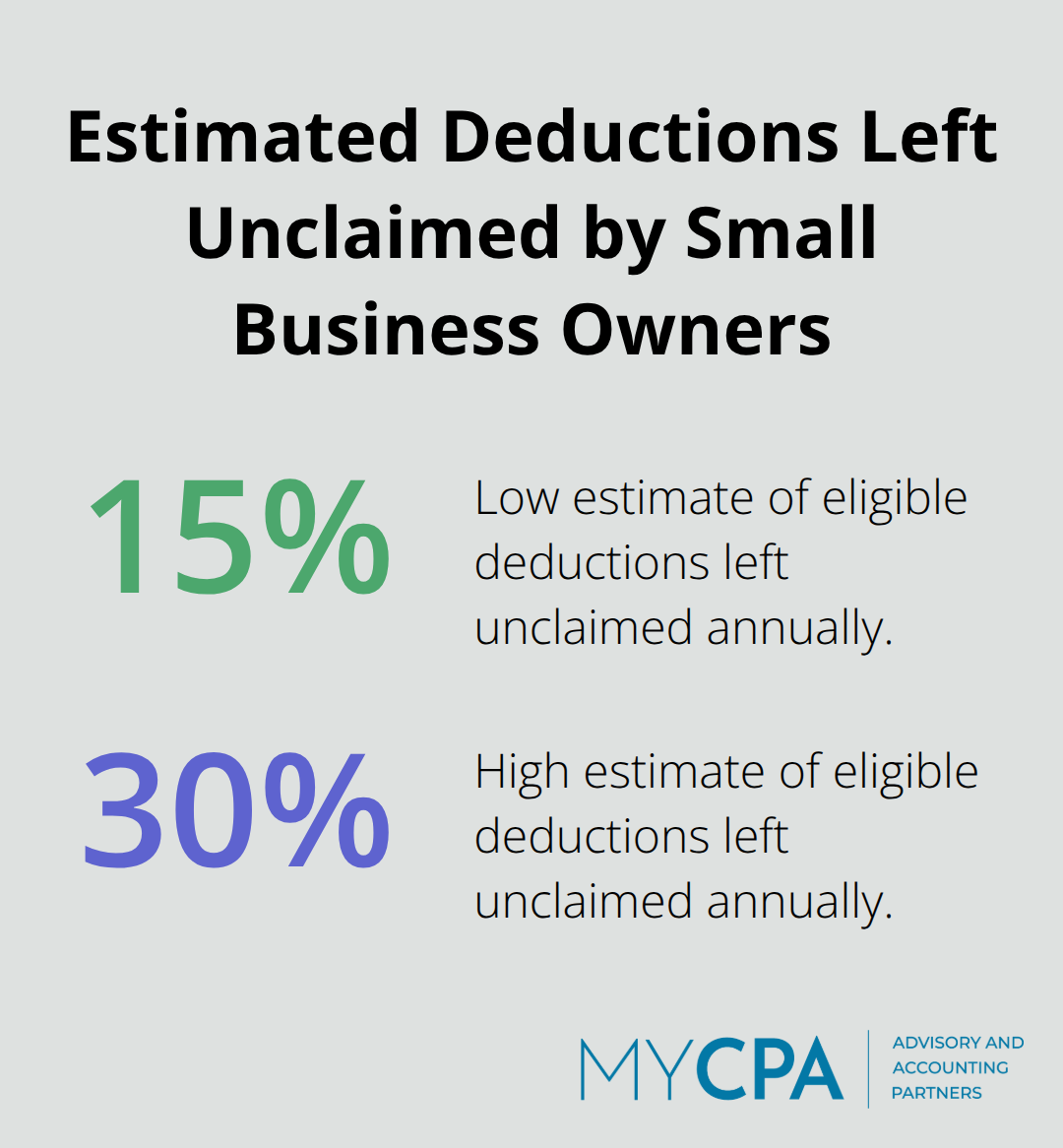

Beyond misclassification, business owners systematically miss deductions they’re entitled to claim. Health insurance premiums for self-employed individuals, home office internet costs, professional development courses, and equipment purchases under $2,500 often go unclaimed simply because owners don’t track them consistently. The IRS data shows that small business owners leave between 15% and 30% of eligible deductions on the table annually.

Separating personal and business finances from day one prevents most of these problems. A dedicated business bank account makes expense tracking automatic and creates a clear audit trail the IRS respects. Without this separation, you’ll spend hours reconstructing transactions and risk missing deductions because personal spending gets tangled with legitimate business costs. Many owners use personal credit cards for business purchases, then struggle to categorize expenses correctly during tax season. This approach guarantees missed deductions and increases audit probability significantly.

The solution is straightforward: establish a business checking account immediately, use it exclusively for business transactions, and reconcile it monthly against your accounting records. Once your finances are organized, modern tools and strategies can accelerate your entire filing process.

Automated bookkeeping eliminates the manual data entry that consumes weeks during tax season. Cloud-based accounting software like QuickBooks captures transactions in real time, categorizes expenses automatically, and syncs across all your business accounts. When your bookkeeping happens continuously rather than cramming everything into January and February, you avoid the bottleneck that forces rushed decisions and missed deductions. Real-time tracking also catches expense misclassifications immediately, not months later when an accountant reviews your return. Software like QuickBooks integrates with your bank feeds, credit cards, and payment processors, meaning transactions populate your records without manual entry. This automation reduces human error significantly-the same errors that trigger audits and penalty assessments.

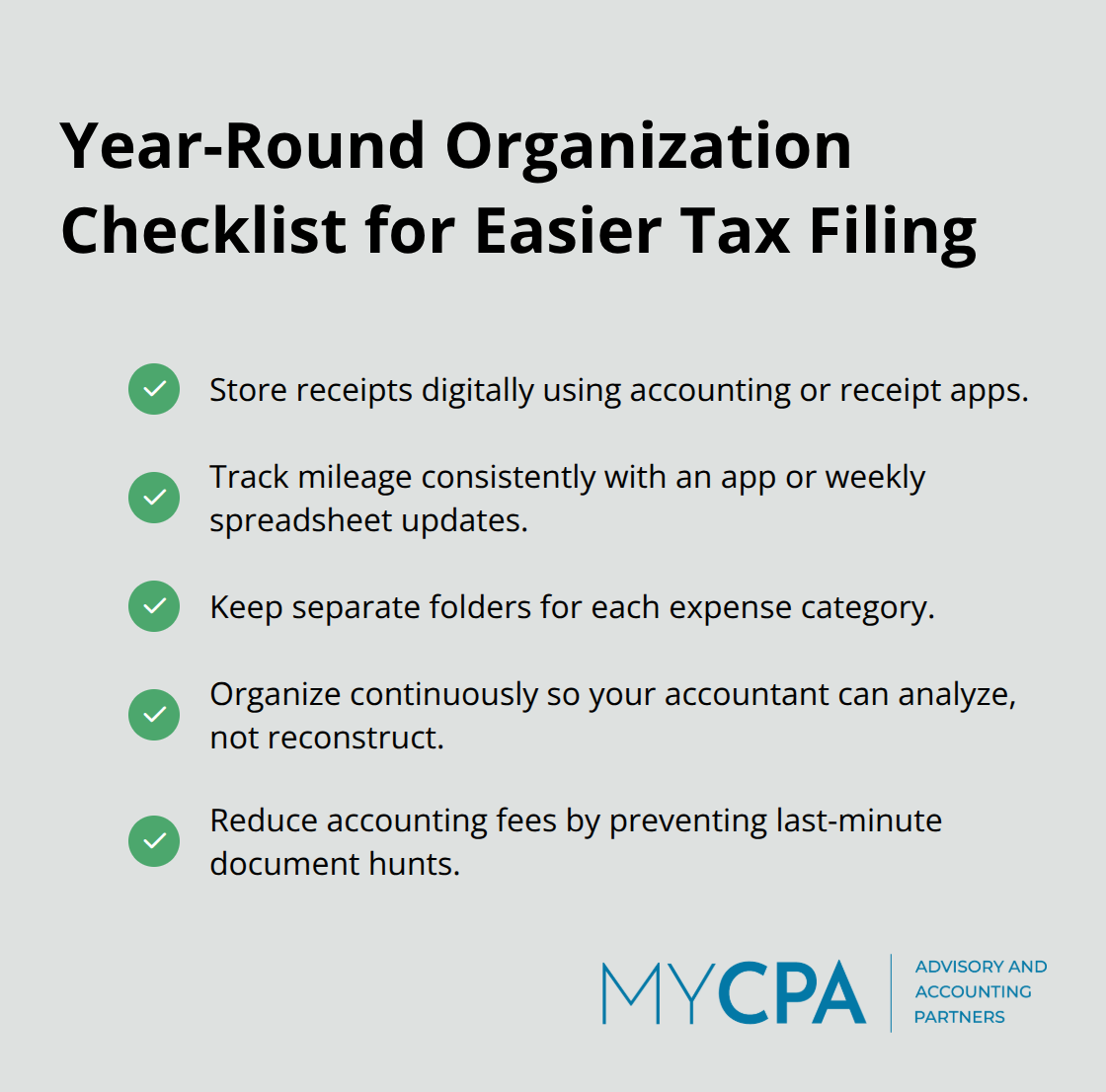

Organization throughout the year transforms tax filing from crisis mode to routine maintenance. Store receipts digitally using apps like Expensify or your accounting software’s mobile features rather than stuffing them in a drawer. Document mileage logs consistently if you claim vehicle deductions, using either an app or a simple spreadsheet updated weekly. Maintain separate folders for each expense category: equipment purchases, professional services, supplies, and meals.

When you organize continuously, your accountant spends their time analyzing your finances and identifying deductions instead of reconstructing transactions from chaotic records. This efficiency directly reduces accounting fees-many accountants charge hourly rates that spike when they must hunt for documentation.

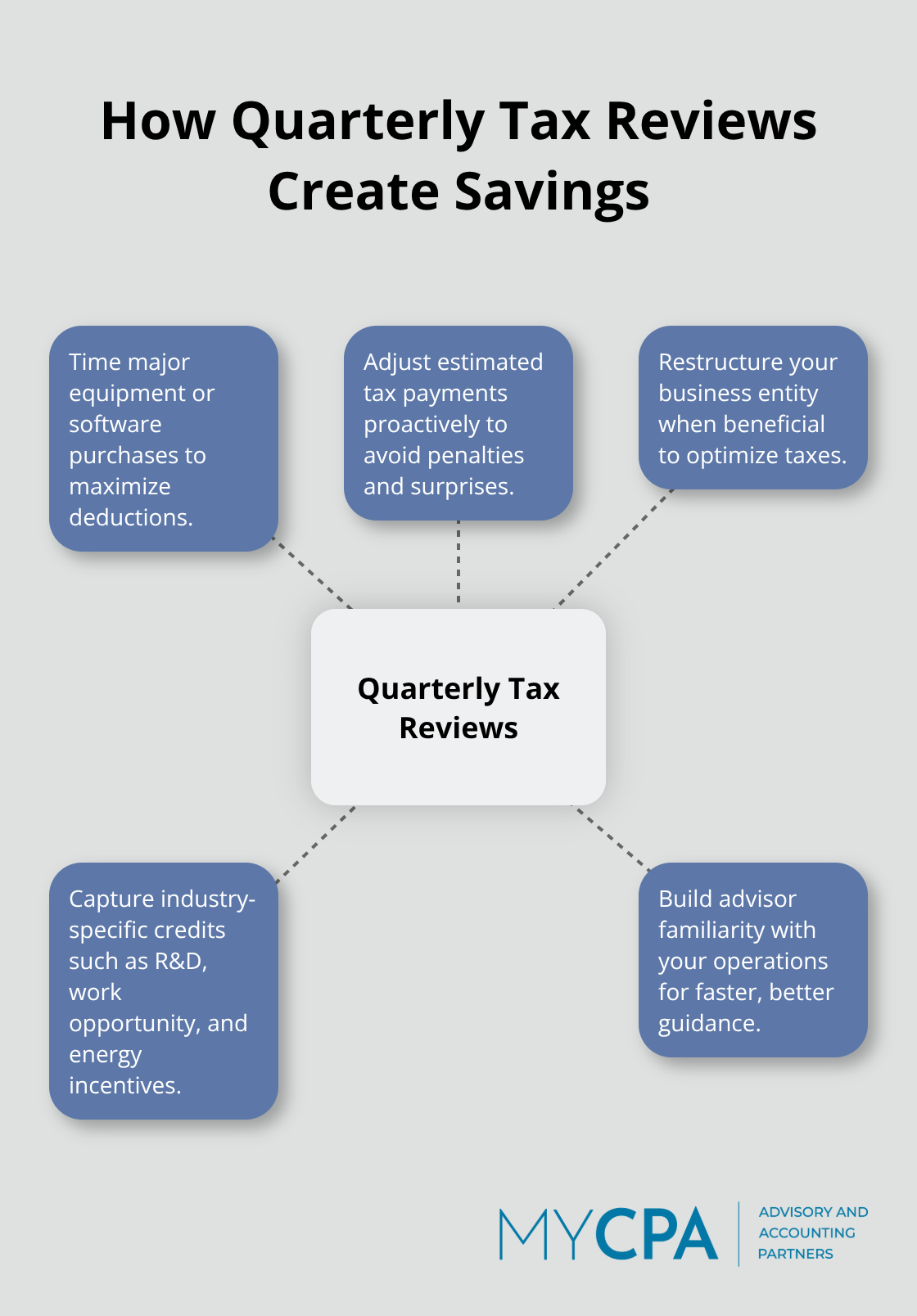

Working with a tax professional early in the process, ideally quarterly rather than in March, prevents expensive mistakes. A quarterly review identifies strategic opportunities like timing large equipment purchases, adjusting estimated tax payments, or restructuring your business to capture additional deductions. Early engagement also means your accountant understands your business operations and industry-specific credits you might qualify for, whether that’s research and development credits, work opportunity credits, or energy-related deductions for equipment upgrades. The cost of quarterly planning typically pays for itself through deductions your accountant identifies before year-end, giving you time to execute them.

Treating your accountant as a strategic partner, not a once-a-year expense, consistently delivers better results than waiting until April with incomplete records. This proactive approach positions you to maximize deductions and minimize your tax liability before the filing deadline arrives.

Your business structure determines how much you pay in taxes more than almost any other factor. A sole proprietorship files differently than an S-corp, and the tax burden can differ by thousands annually on identical income. The IRS allows business owners to choose between structures, and this choice should rest on your specific income level and business type, not habit or convenience. If you earn over $60,000 annually, an S-corp election often saves substantially on self-employment taxes because you can split income between W-2 wages and distributions, paying self-employment tax only on the W-2 portion. An S corp structure results in roughly $5,400 in annual tax savings for many business owners.

The administrative burden concerns many owners, but accounting software and payroll services handle most compliance automatically now. S-corps require payroll processing, quarterly filings, and accurate wage documentation-tasks that no longer demand significant manual effort. The decision hinges on one calculation: compare your current self-employment tax bill against what you’d pay with an S-corp structure. If the difference exceeds $1,500 annually, the structure change pays for itself immediately. This isn’t theoretical-it’s the single most impactful tax decision most business owners never evaluate seriously.

Equipment purchases placed into service before December 31st qualify for full-year depreciation or bonus depreciation under current rules, while purchases made January 2nd lose an entire year of deductions. If you plan equipment upgrades, software investments, or vehicle purchases, complete them by year-end to capture maximum tax benefits. One business owner delayed a $40,000 equipment purchase until January and unnecessarily paid higher taxes that year as a result.

The IRS allows deduction for bonus depreciation rules for business equipment, meaning you can deduct qualifying costs immediately rather than spreading deductions across years. This accelerates your tax benefit significantly. Conversely, deferring income into the next year reduces your current-year tax liability when you anticipate higher income this year than next. If you’re a consultant with discretionary invoicing, delaying client billing until January when you expect slower business makes mathematical sense.

Your industry likely qualifies for credits most owners never claim. Energy equipment upgrades for your office, research and development activities in technology or manufacturing, and hiring from specific demographics all trigger credits worth hundreds or thousands annually. The Energy Efficient Home Improvement Credit provides a 30 percent credit for qualifying improvements, capped at $1,200 annually, while the Residential Clean Energy Credit covers solar and geothermal installations at 30 percent. Many owners skip these entirely because they assume credits only apply to massive corporations. That assumption costs them thousands in unclaimed benefits. A tax planning strategy that includes a thorough review of available credits ensures you capture every dollar you’re entitled to claim.

Tax filing improvements happen when you stop treating taxes as an annual crisis and start treating them as an ongoing business operation. The mistakes outlined earlier-misclassified expenses, missed deductions, and disorganized finances-aren’t inevitable. They’re preventable through systems and strategy, and the financial impact of prevention far exceeds the cost of implementation.

Proactive tax planning delivers concrete results that compound over time. Business owners who organize finances continuously, review taxes quarterly, and time major purchases strategically reduce their tax bills by thousands annually (the S-corp structure alone saves many owners $5,400 per year). When your bookkeeping runs automatically through cloud-based software, your accountant spends less time reconstructing transactions and more time identifying deductions. When you maintain organized records throughout the year, tax season becomes manageable instead of overwhelming.

We at My CPA Advisory and Accounting Partners have watched business owners transform their tax outcomes by implementing these approaches. The difference between filing taxes yourself and working with professionals who understand your industry, your business structure, and your specific situation is substantial. Contact our team to build a personalized tax strategy that delivers real savings.

Privacy Policy | Terms & Conditions | Powered by Cajabra