Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Most businesses close their books monthly, but few do it well. Delays, errors, and disconnected processes turn what should be a routine task into a monthly headache.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how a sloppy monthly accounting close creates blind spots in financial reporting and stalls decision-making when you need answers most. The good news: fixing your close process is entirely within your control.

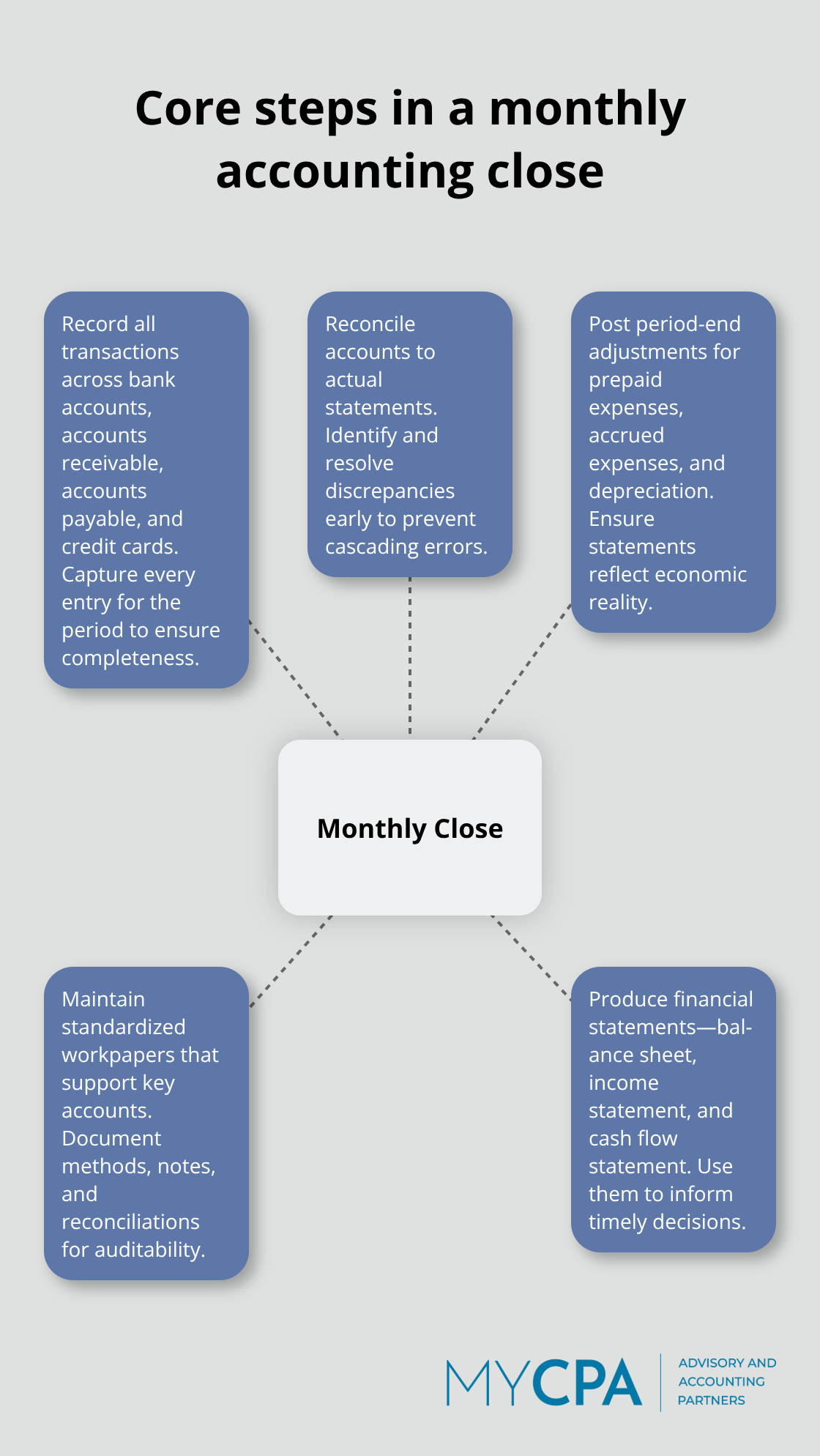

A monthly accounting close finalizes all financial transactions, reconciles accounts, and produces accurate financial statements for a specific period. The process sounds straightforward, but execution reveals complexity. Your close involves recording every transaction across bank accounts, accounts receivable, accounts payable, and credit cards. You reconcile those accounts to their actual statements. You post adjustments for prepaid expenses, accrued expenses, depreciation, and other items that don’t flow automatically from your accounting system. You update workpapers that support your key accounts. Then you generate your balance sheet, income statement, and cash flow statement.

The typical close takes three to five business days, but many businesses stretch this into weeks because they wrestle with manual processes and disconnected systems. The problem isn’t the tasks themselves-it’s how most companies execute them.

A delayed close cripples your ability to make informed decisions. If you wait ten days to know your true cash position, you make spending and investment decisions based on incomplete information. Finance leaders using technology-driven close processes report significantly faster closes and higher accuracy, which translates directly to better visibility into your actual financial health. Cash flow planning becomes impossible when you don’t know your real numbers until mid-month. A timely close tells you exactly where you stand on revenue, expenses, and cash reserves-information you need to adjust your strategy before problems compound. Companies that close within three to five days spot trends, identify cost overruns, and respond to cash flow issues while there’s still time to act. Those that drag the close into weeks operate essentially blind.

Most businesses treat workpapers as a compliance checkbox for audits. Workpapers serve a different purpose: they function as your documentation layer and capture the details, notes, and reconciliations that don’t live in your accounting system. They show how you arrived at each number on your financial statements. Consistent workpapers across months let you spot anomalies, track what changed month-to-month, and explain variances without scrambling. They also dramatically reduce friction during tax planning conversations because your accountant doesn’t need to reconstruct your thinking. When you standardize your workpapers and maintain them month after month, your close becomes faster because you build on a foundation rather than starting from scratch each time.

Bank reconciliations and credit card reconciliations form the backbone of a reliable close. You match your accounting records to actual bank and credit card statements, identifying discrepancies before they compound into larger problems. Many businesses skip this step or rush through it, which introduces errors that cascade through your financial statements. Reconciling these accounts early in your close window (rather than at the end) gives you time to investigate and resolve issues. When you reconcile consistently and document your findings in workpapers, you create an audit trail that supports both your financial reporting and tax compliance.

The tasks that make up your monthly close-reconciliations, journal entries, workpaper updates-are repetitive and predictable. That predictability is your opportunity. The next section covers how to standardize these tasks, assign clear ownership, and use tools that eliminate manual work so your team focuses on analysis instead of data entry.

Most businesses fail at the monthly close not because they lack discipline or intelligence, but because their close process was never designed to handle the complexity of modern business operations. Manual data entry remains the primary culprit. Your accounting team receives transaction data from bank feeds, credit card processors, payroll systems, and department spreadsheets-each in different formats, arriving at different times. Someone manually enters or reconciles these into your accounting system, introducing errors that compound through your financial statements. When your bank reconciliation depends on one person matching transactions by hand against a spreadsheet, you’re not just slow-you’re building fragility into your process. A single typo cascades into hours of investigation.

The second obstacle is information arriving in fragments. Your payroll team finalizes numbers on the 27th. Your accounts payable team still processes invoices on the 28th. Your field operations team submits expense reports whenever they remember. Finance sits waiting for complete data before reconciliation can begin, which means your close window shrinks and pressure mounts. Delayed financial information from disconnected departments isn’t a coordination problem-it’s a structural problem that kills your ability to close on schedule. When departments operate independently without aligned deadlines, your finance team cannot start critical reconciliations until all data arrives. This sequential dependency stretches your close timeline and forces your team to work under constant time pressure.

The third and most damaging obstacle is the absence of standardized procedures. Without a clear checklist of close tasks, assigned owners, and firm deadlines, work gets duplicated, skipped, or delayed. One person reconciles accounts payable while another person in the same department reconciles the same accounts using different methods. Workpapers exist in scattered formats across multiple files, making it impossible to know what was adjusted last month or why. Your team spends time hunting for information instead of analyzing it. The absence of standards means every close feels like the first close-your team rebuilds the process from memory rather than following a documented path.

This is why technology adoption matters less than you’d expect if your underlying process remains chaotic. QuickBooks Online or any other software amplifies your existing problems if you haven’t standardized how data flows into it and how tasks get executed. The fix requires addressing structure first, then layering in tools that support your standardized approach. Without structure, new software simply automates confusion faster. Your accounting system is only as reliable as the data and processes feeding into it. When you establish clear procedures, assign ownership, and enforce deadlines before implementing new tools, technology becomes a multiplier of good practices rather than a magnifier of bad ones. The next section shows you exactly how to build that structure and which tools support it most effectively.

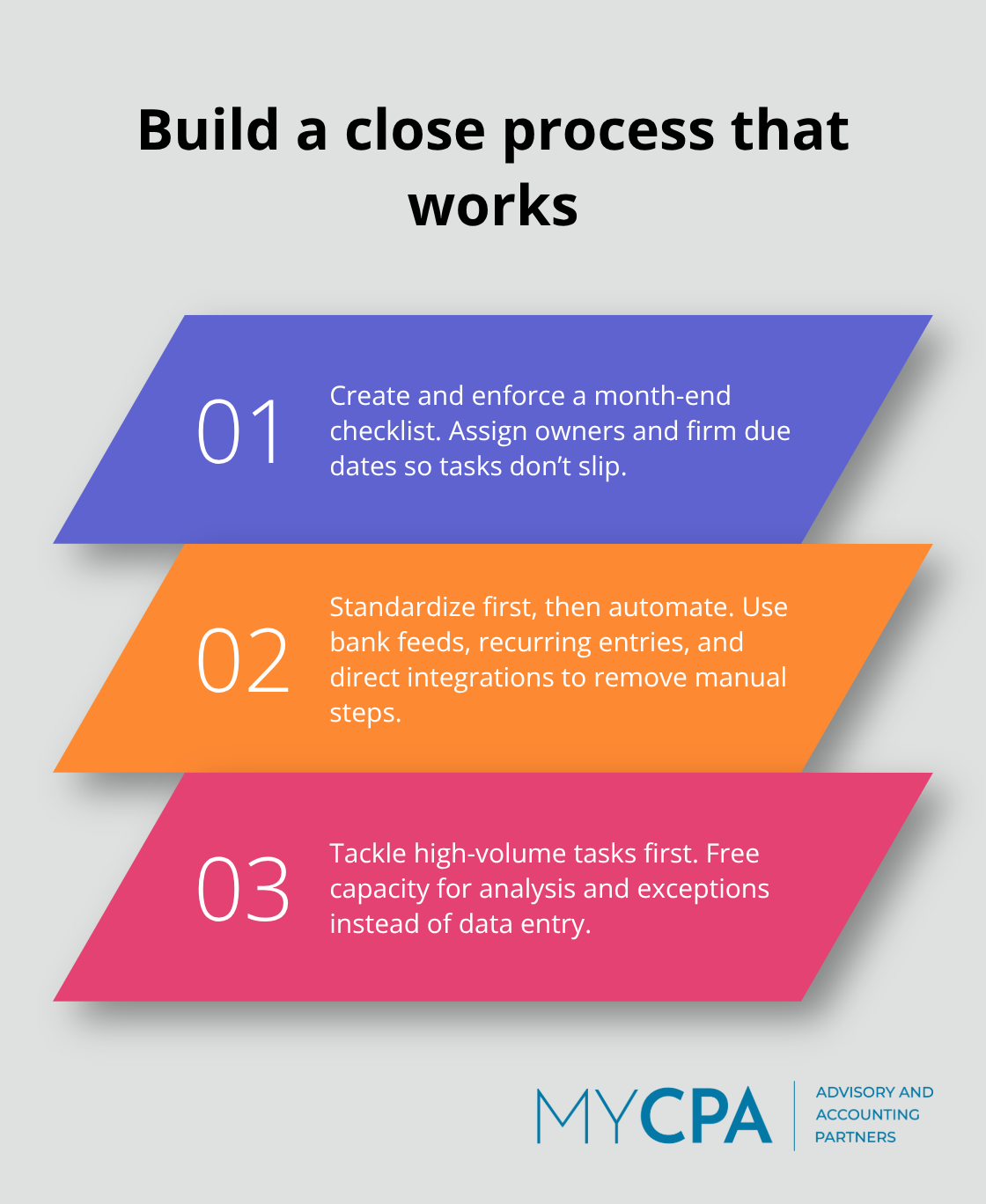

The structure of your close matters far more than which software you use. Businesses that invest in expensive accounting platforms often remain stuck at a three-week close because they never defined who does what, when, and how. The fix starts with a standardized month-end checklist that lists every task, assigns a clear owner, and sets a firm due date. This checklist becomes your enforcement mechanism. Without it, tasks slip, duplicate, or get skipped entirely.

Your checklist should live in a shared document or dashboard where team members mark tasks complete and flag blockers in real time. Elliott Davis research shows that standardized workflows with checklists and defined timelines reduce bottlenecks and improve coordination across teams significantly. Your checklist must include bank reconciliations, journal entry reviews, accounts payable and receivable verification, payroll reconciliation, fixed asset updates, and workpaper sign-offs. Assign each task to a specific person with a specific deadline-not a vague window, but an actual date. If your close typically takes five days, your bank reconciliations should be due on day two, not day four. This forces early completion and gives you time to investigate discrepancies before they cascade into larger problems.

Your checklist also prevents the scramble that happens when finance doesn’t know what operations completed or what still needs attention. Make it visible to everyone involved, not just your accounting team. When your payroll manager sees that payroll reconciliation is due on the 27th and owns that deadline, the close stops depending on someone following up repeatedly.

Automation must follow standardization, not precede it. Once you have a clear process, automation amplifies it. QuickBooks Online’s bank feed feature automatically imports transactions from your bank, which reduces manual data entry and speeds reconciliations substantially. Set up recurring journal entries for predictable adjustments like monthly depreciation, so those post automatically without manual intervention each month. QuickBooks can export internal financial statements directly, which eliminates the need to build them manually in spreadsheets. The key is knowing your system’s capabilities before you assume you need external tools. Many businesses pay for expensive add-ons when QuickBooks already handles their core needs.

According to Elliott Davis, automating data entry and reconciliation significantly reduces manual processing time and error rates. Real-time data validation across connected systems improves accuracy and reduces reconciliation time further. If your payroll system can feed directly into QuickBooks or your general ledger, that integration eliminates the manual step where errors most often creep in. Similarly, expense management platforms that auto-categorize transactions and sync to your accounting software cut the reconciliation workload dramatically.

Start with the highest-volume, most repetitive tasks-bank feeds, payroll posting, recurring accruals-and automate those first. This frees your team to focus on analysis and exception handling rather than data entry. The typical month-end close takes three to five business days when processes are standardized and automation is in place. If yours stretches longer, the gap is almost always manual work that could be eliminated through better process design or tool configuration, not a need for more staff or longer hours.

A reliable monthly accounting close transforms how your business operates. When your close runs on schedule and produces accurate numbers, your leadership team makes decisions based on reality rather than guesswork. You spot cash flow problems before they become crises, understand which departments perform well, and catch tax planning opportunities while time remains to act on them. This confidence ripples through your entire organization because decisions move faster and strategy shifts based on actual performance.

Proper close procedures also anchor your tax planning and compliance work. Your accountant cannot optimize your tax position if financial records arrive incomplete or late, and tax deadlines do not move. When you maintain consistent workpapers, reconcile accounts thoroughly, and document your adjustments clearly, your tax professional has the foundation needed to identify deductions, timing strategies, and entity structure improvements that save money. A sloppy close forces your tax team into reactive mode, scrambling to file returns rather than planning proactively.

The path forward requires one decision: commit to standardizing your monthly accounting close process before adding new tools. Start with a checklist that assigns clear ownership and firm deadlines, automate the repetitive tasks that consume the most time, and build workpapers that document your thinking. These steps cost nothing except discipline, yet they compress your close timeline and eliminate the errors that plague most businesses-and we at My CPA Advisory and Accounting Partners help business owners implement close processes that work.

Privacy Policy | Terms & Conditions | Powered by Cajabra