Monthly Close Process: Streamline Your Bookkeeping

Streamline your monthly close process with practical steps to organize bookkeeping, reduce errors, and close your books faster each month.

Your monthly close process makes or breaks your financial accuracy. Most businesses waste hours on manual reconciliations and miss errors that compound throughout the year.

We at My CPA Advisory and Accounting Partners have seen firsthand how poor closing practices create headaches during tax season and audits. This guide shows you the mistakes to avoid, the practices that work, and the tools that save you time.

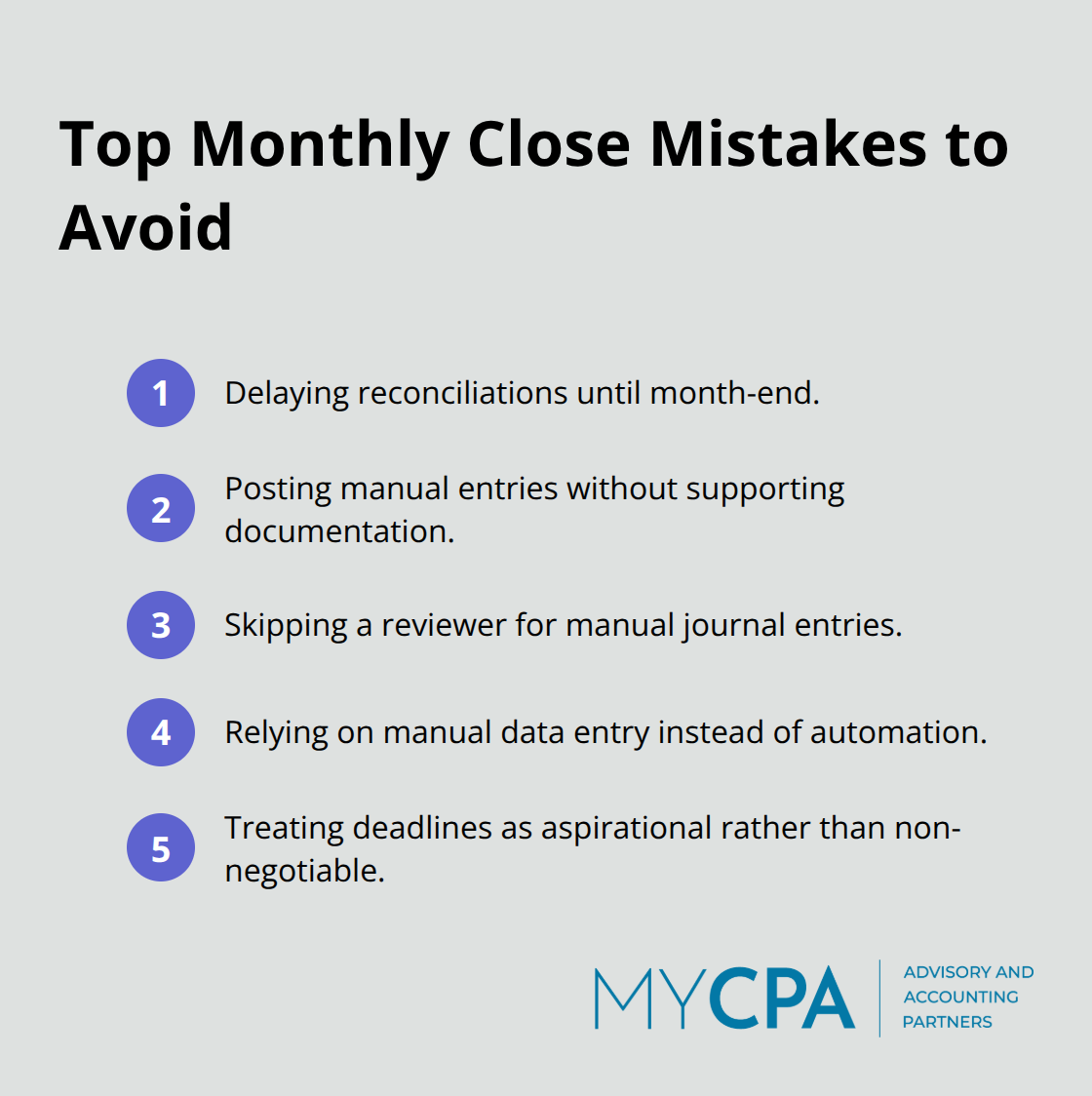

The biggest mistake businesses make is waiting until month-end to reconcile accounts. When you delay reconciliations, small discrepancies compound into massive headaches. A transaction posted to the wrong account in week one becomes harder to trace by week four. J.P. Morgan research shows that inefficient closes cost far more than staff time alone-they enable financial reporting errors that delay critical decisions on cash position and working capital. Reconcile bank and credit card accounts weekly instead of monthly. This transforms your month-end close from a scramble into a verification exercise. When you catch errors early, you eliminate the last-minute panic and the post-close adjustments that eat into your team’s time.

Failing to document transactions properly creates a paper trail that disappears when you need it most. Without clear notes on why a transaction happened or what it represents, your team spends hours hunting for context during close. Manual journal entries represent a significant source of month-end errors. Every adjusting entry requires a documented reason, approval, and date. Set a non-negotiable rule: no entry posts without supporting documentation attached in your accounting system. If you use QuickBooks, attach images of receipts and invoices directly to transactions. This practice alone cuts reconciliation time significantly because your team avoids wasting hours reconstructing what happened. During tax season or audits, solid documentation also protects you from questions about your numbers.

Journal entries that slip through without review act as silent killers. A single misclassified entry throws off your entire profit and loss statement. Assign one person to review all manual entries for accuracy, proper account coding, and supporting documentation before final sign-off each month. This review takes two to three hours for most businesses but catches errors that would otherwise surface weeks later. When you implement this discipline, you reduce post-close adjustments dramatically and build confidence in your financial statements. These three practices form the foundation of a reliable close-and they set the stage for the best practices that actually accelerate your process.

Speed matters because delays in your close ripple through your entire financial calendar. Most businesses close between 5 and 10 days after month-end, but faster closes are possible when you eliminate bottlenecks. The key is treating your close timeline as non-negotiable rather than aspirational.

You need a hard deadline-say, the 5th business day after month-end-and you work backward from there. Assign specific tasks to specific people with clear ownership. If reconciliation owns days one and two, journal entry review owns day three, and financial statement preparation owns day four, your team knows exactly what’s expected. A simple spreadsheet with task names, owners, and deadlines eliminates the status-chasing that wastes hours each month. Without this structure, close becomes reactive-people work overtime, skip steps, and introduce errors that surface later.

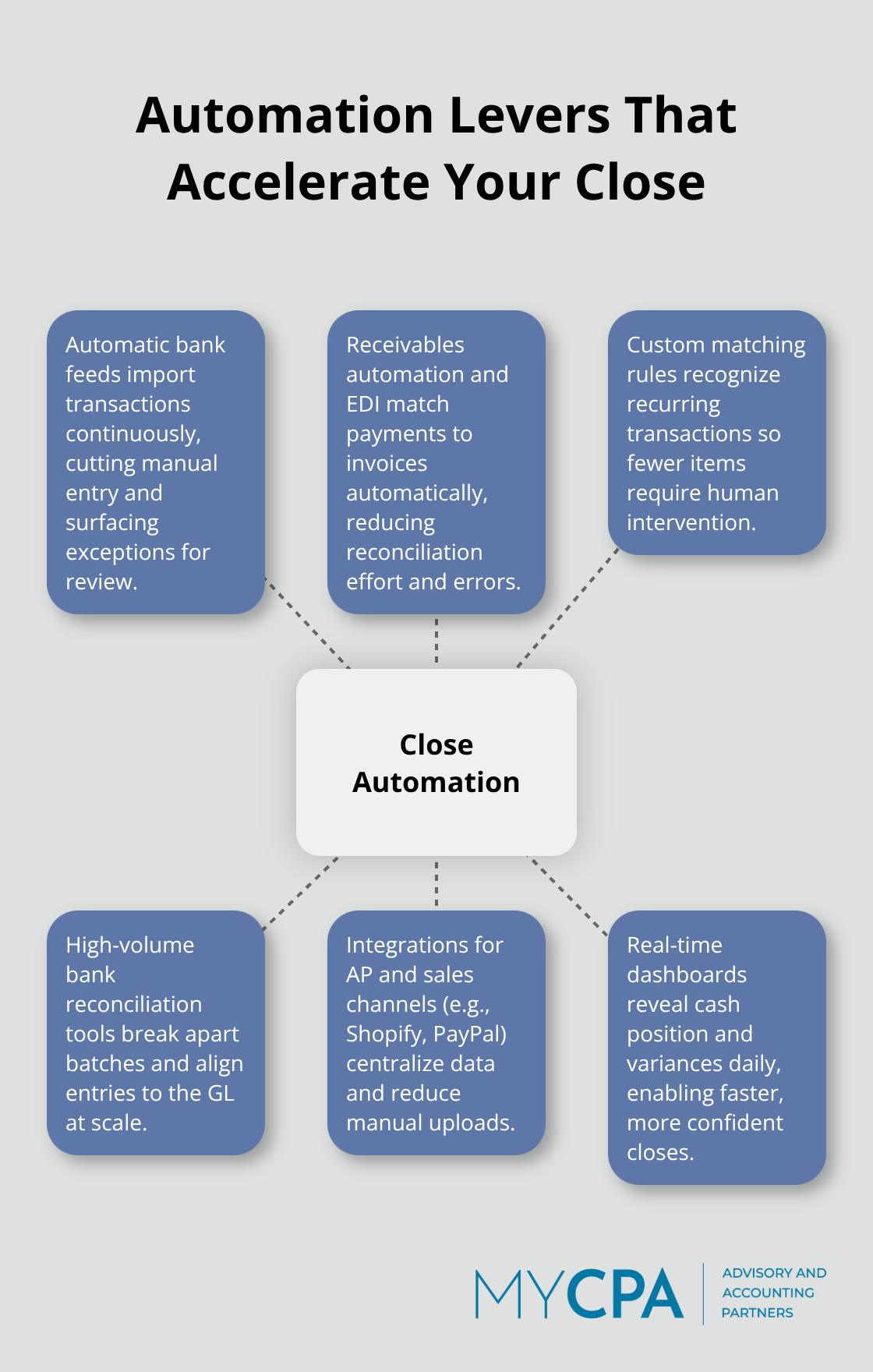

Manual data entry and reconciliation represent the biggest time sinks in most month-end closes. When you connect your bank accounts directly to QuickBooks or similar accounting software, transactions appear automatically without human intervention. This alone cuts reconciliation time substantially because your team spends less time typing and more time reviewing exceptions.

Electronic Data Interchange, or EDI, technology takes this further by sending payment details directly from customers to your accounting system, enabling automatic matching without manual lookup. J.P. Morgan data shows that organizations implementing end-to-end receivables automation have cut reconciliation time in half and reduced errors significantly. Start with your highest-volume accounts-typically cash, credit cards, and your primary bank account. Automate those first, then expand to accounts payable and sales channels like Shopify or PayPal. Most implementations take two months but deliver immediate efficiency gains that compound monthly. The investment pays for itself within the first quarter through staff time saved.

Weekly reconciliations of bank and credit card accounts keep discrepancies small and traceable. When you reconcile on a fixed schedule-say, every Friday morning-small errors surface before they tangle with dozens of other transactions. This practice transforms your month-end close from a hunt for problems into a final verification.

Assign one person to own each reconciliation and hold them accountable for completion by the deadline. If a transaction doesn’t match, they investigate immediately rather than deferring it. Over time, this discipline reveals patterns (duplicate entries, timing issues with transfers, or systematic miscoding) that you can fix permanently. Your team learns the system better, catches fraud faster, and builds confidence in the numbers they’re reporting.

Once you establish these operational foundations, the tools you select determine whether your team executes them consistently or struggles with manual workarounds.

The right accounting software eliminates hours of manual work each month, but only if you configure it correctly and actually use its automation features. QuickBooks remains the most widely adopted platform for small to mid-sized businesses, and its native reconciliation tools work well when you connect your bank feeds properly.

Connect automatic bank feeds for every account you own, not just your primary checking account. Credit cards, savings accounts, and merchant services accounts all feed transactions directly into QuickBooks without manual entry. The reconciliation window then shows you what posted automatically versus what still needs matching. Most businesses waste time reconciling transactions that QuickBooks already matched correctly but flagged as pending because of minor formatting differences. Spend 30 minutes customizing your matching rules so QuickBooks recognizes your recurring transactions automatically. Transactions from your payroll processor, regular vendor payments, and customer deposits should match without human intervention once you teach the system what to expect.

Bank reconciliation automation solutions go deeper than QuickBooks alone by breaking apart batched transactions and matching them to your general ledger with minimal manual intervention. Leading platforms include Airwallex, BlackLine, FloQast, and Trintech, which excel at handling high business processing volumes. If you process high volumes of checks or ACH payments, these services cut reconciliation time dramatically by automating what would otherwise consume hours of line-by-line verification. ACH Reconcilement Services break batched ACH entries into underlying transactions, giving your team clearer visibility and faster matching capabilities. Check Return Services alert you to returned deposits, improving your cash positioning and enabling quicker follow-up on receivables.

Financial reporting dashboards in QuickBooks, Xero, or specialized tools like Dext show your cash position, expense trends, and balance sheet health in real time rather than waiting until month-end to discover problems. These dashboards pull live data from your connected accounts and display profit-and-loss statements, cash flow forecasts, and aging reports automatically. When your team can see updated numbers daily, they spot anomalies immediately instead of discovering them during close. Real-time reporting keeps income statements and balance sheets current, enabling faster monthly close cycles. The combination of automatic data feeds, intelligent matching, and real-time visibility transforms your month-end close from a reactive scramble into a controlled process where surprises rarely occur.

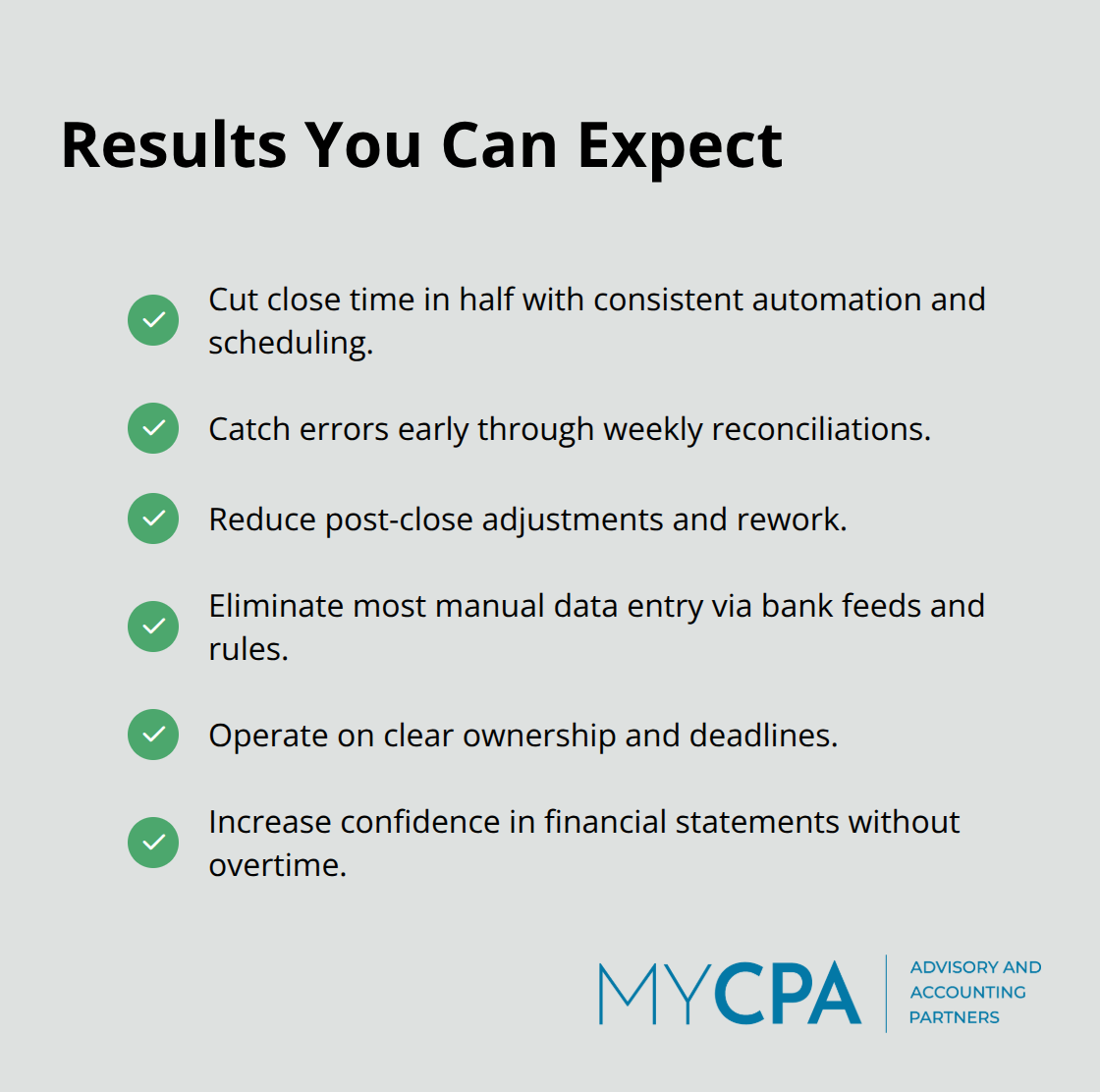

Your monthly close process transforms financial data into a strategic asset or leaves it buried under friction and errors. The mistakes we covered-delayed reconciliations, poor documentation, and unreviewed entries-all have straightforward fixes. Hard deadlines, clear ownership, and automation eliminate the scramble that most teams experience each month.

Most businesses that implement these changes cut their close time in half while catching errors before they spread. Weekly reconciliations replace month-end panic, automated bank feeds eliminate data entry, and real-time dashboards surface problems immediately. Your team executes a predictable, reliable process without overtime or stress.

We at My CPA Advisory and Accounting Partners work with business owners who understand that financial accuracy matters for growth and decision-making. Whether you need help configuring your accounting software, establishing a documented close process, or identifying gaps in your current procedures, contact My CPA Advisory and Accounting Partners to discuss your situation and discover the highest-impact improvements for your business.

Privacy Policy | Terms & Conditions | Powered by Cajabra