Strategic Financial Advisory: Insightful Guidance for Growth

Gain strategic financial advisory insights to drive business growth, improve profitability, and make smarter decisions for long-term success.

Most business owners leave thousands of dollars on the table each year through tax inefficiencies. Whether it’s missed deductions, poor timing, or disorganized records, these gaps compound quickly.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how tax efficiency practices transform a company’s bottom line. This guide walks you through the strategies that actually work.

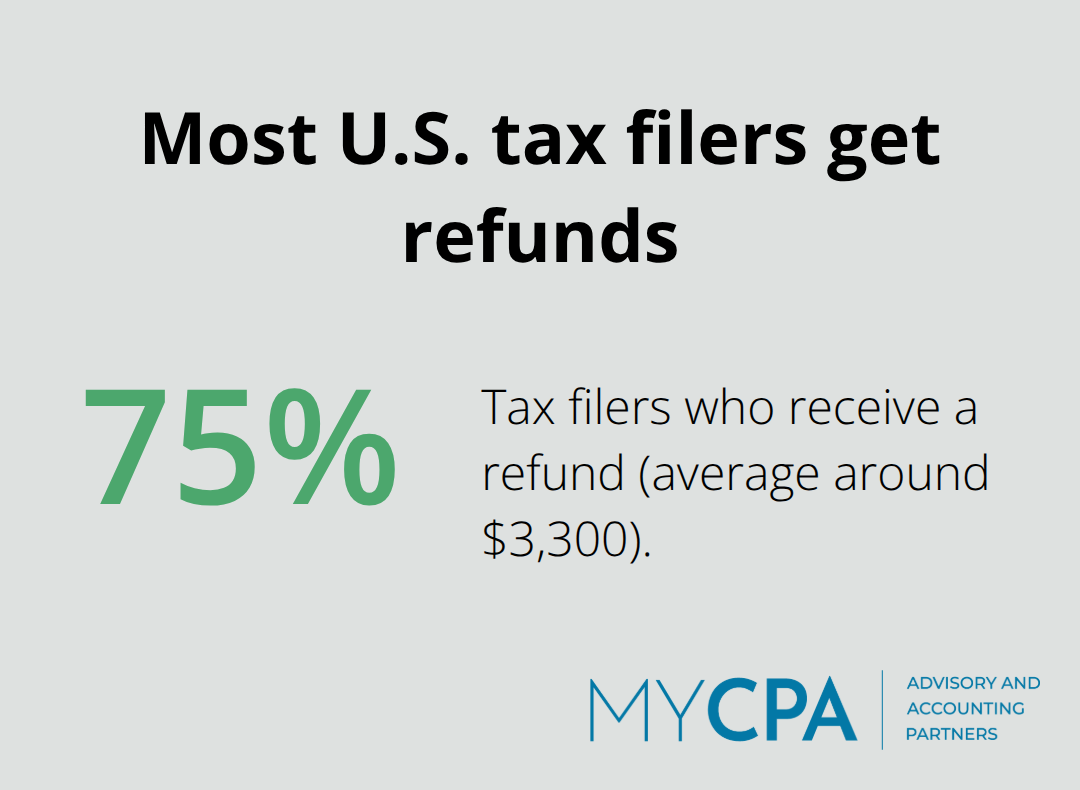

Most business owners don’t realize how much money leaks away through preventable tax mistakes. Roughly three-quarters of all tax filers receive refunds, averaging nearly $3,300 annually. But refunds tell only part of the story.

The real damage comes from deductions you never claimed, credits you didn’t know existed, and timing decisions made without tax consequences in mind. A business owner might write off $50,000 in legitimate expenses but miss $15,000 in available credits simply because no one flagged them. Another owner might recognize income in December when deferring it to January would have saved thousands in taxes. These aren’t exotic strategies. They’re foundational tax management practices that separate owners who pay what they owe from owners who pay far more than necessary.

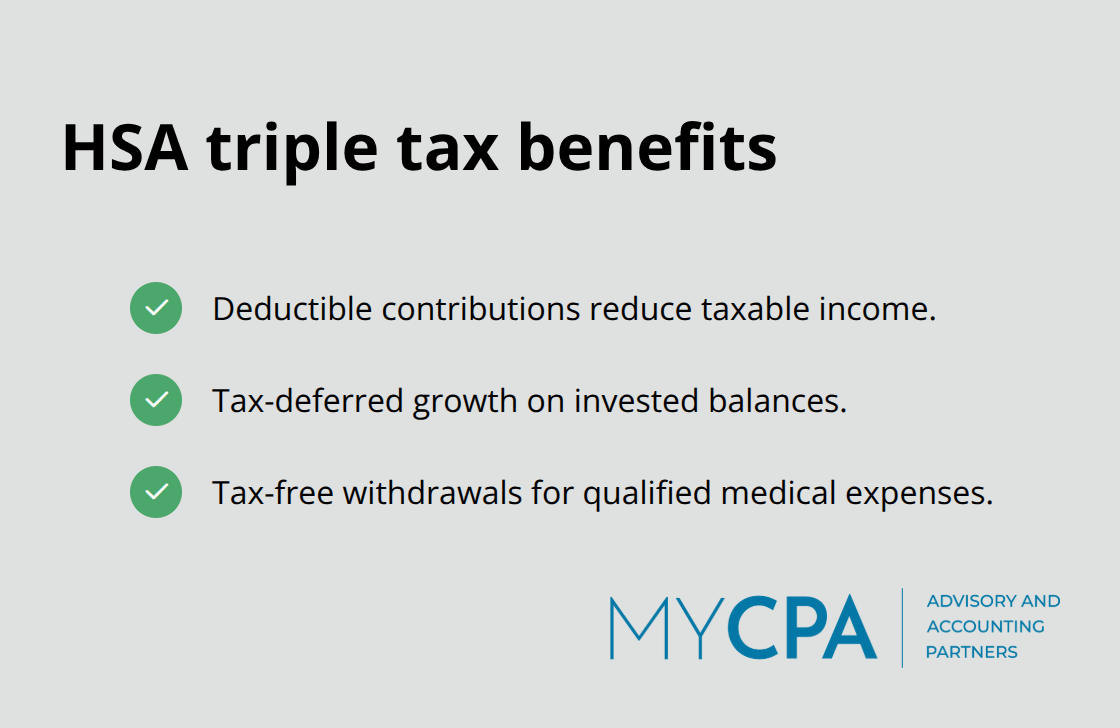

The gap between what you can deduct and what you actually deduct often runs into five figures. Many business owners claim the obvious expenses-rent, payroll, supplies-but miss the secondary deductions that compound annually. Health Savings Accounts offer triple tax benefits: deductible contributions, tax-deferred growth, and tax-free withdrawals for qualified medical expenses. If you have a high-deductible health plan, you can max out an HSA at no tax cost while building a tax-free medical fund.

Similarly, if you’re self-employed or a business owner with employees, you might qualify for the Saver’s Credit, which directly reduces your tax bill for retirement contributions. The IRS also offers credits for clean vehicles, home energy improvements, and childcare expenses-yet many business owners never investigate whether they qualify. The problem isn’t complexity; it’s visibility. Without a systematic review of your specific situation, credits sit unclaimed year after year.

Income and expense timing determines whether you pay tax this year or next. A client who invoices a large contract in December instead of January might push themselves into a higher tax bracket unnecessarily. Another who defers equipment purchases until January misses the Section 179 deduction available only in the year of acquisition. The Section 179 deduction allows up to $2.5 million in immediate write-offs for qualified property, with the phase-out threshold at $4 million. Bonus depreciation complements this by allowing immediate deductions for new or used property, and both can work together for larger first-year write-offs. Missing this window means spreading the deduction over years instead of capturing the full tax benefit immediately. Capital gains timing matters equally. Long-term gains taxed at rates up to 23.8% are vastly preferable to short-term gains taxed as high as 40.8%. Yet many owners sell investments without considering the holding period, turning favorable long-term gains into unfavorable short-term ones. Quarterly estimated tax payments also expose timing mistakes. Owners who pay too much quarterly lose the use of that cash; those who pay too little face penalties and interest.

Disorganized records don’t just create compliance headaches-they cost money directly. An owner without clear documentation of business expenses cannot claim them, regardless of legitimacy. Another with commingled personal and business expenses cannot confidently allocate costs to the business. When mutual fund distributions arrive, many owners don’t track the tax date, missing opportunities to manage the tax impact strategically. If you purchase a mutual fund shortly before a large distribution, you inherit a taxable liability without the corresponding gain. Knowing distribution dates lets you time purchases to minimize this exposure. Similarly, tracking cost basis methodically matters enormously. Specific identification lets you choose which shares to sell, and using a method like the MinTax approach suggests which lots minimize taxes. Without this information, you default to FIFO (first-in, first-out), which often produces suboptimal tax outcomes. Real-time record systems transform tax planning from guesswork into precision. These systems also prepare you for the advanced strategies that multiply your tax savings.

Your choice of business entity-sole proprietorship, S-corp, C-corp, LLC, or partnership-determines how much tax you actually owe. Most business owners never optimize this decision, treating it as a one-time legal question rather than an ongoing tax lever. An S-corp election lets you split income between W-2 wages (subject to payroll tax) and distributions (not subject to self-employment tax). A self-employed consultant earning $150,000 might pay roughly $21,000 in self-employment tax on the full amount. Restructuring as an S-corp and taking $90,000 in W-2 wages plus $60,000 in distributions could reduce self-employment tax to approximately $12,700, saving nearly $8,300 annually. That money stays in your business instead of flowing to the IRS. The tradeoff involves additional accounting and filing complexity, but the math works decisively in favor of S-corp status for many business owners earning above $60,000.

Entity structure also affects retirement plan options available to you. A C-corp can sponsor a defined-benefit pension plan, allowing you to shelter substantially more income than traditional 401(k) limits allow. For 2026, standard 401(k) contributions cap at $24,500, but catch-up contributions for those 60–63 reach $11,250, bringing the employee limit to $35,750. Add employer contributions, and the combined limit hits $72,000 annually. A defined-benefit pension plan can exceed these amounts significantly if structured correctly. The IRS data shows that owners who fail to evaluate their entity structure annually leave five-figure tax savings uncaptured. We recommend reviewing your entity structure every two to three years as your business scales, particularly when income crosses $80,000 to $100,000 thresholds where structural changes typically generate the strongest returns.

Retirement savings accomplish two goals simultaneously: they fund your future while reducing your current tax bill. Most business owners contribute to retirement accounts sporadically rather than strategically, missing the compounding effect of consistent, maximum contributions. A Solo 401(k) for self-employed individuals allows you to contribute up to $72,000 combined in 2026 if structured properly, with employee deferrals reaching $35,750 and employer contributions filling the remainder. A SEP IRA caps contributions at the lesser of 25% of net earnings or $70,000, making it ideal for high-income self-employed owners who want simplicity without the administrative burden of a 401(k). The decision between these options hinges on your income level and administrative tolerance.

Health Savings Accounts deserve separate emphasis because they offer triple tax benefits that few business owners exploit fully. Contributions reduce your taxable income, growth occurs tax-free, and withdrawals for qualified medical expenses trigger no tax whatsoever. For 2026, individual coverage maxes at $4,300 annually with a $1,000 catch-up for those 55 and older. Over a 20-year career, maxing an HSA at 7% annual growth and modest medical withdrawals creates a tax-free medical fund exceeding $150,000. Yet many business owners with high-deductible health plans never open an HSA, leaving this opportunity dormant.

Roth conversions represent another underused lever. Converting pre-tax retirement funds to a Roth account locks in taxes at your current rate but creates tax-free withdrawals later. If you expect tax rates to rise-a reasonable assumption given current federal debt levels-converting during lower-income years makes mathematical sense. Model multiple scenarios with actual numbers rather than guessing about future tax rates.

Equipment purchases represent the largest tax-deductible blind spot for business owners. Many claim standard depreciation over five to seven years when immediate deductions are available. Section 179 allows up to $1.25 million in immediate deductions for qualified property in 2025, with the phase-out beginning at $3.15 million of purchases. Bonus depreciation complements this by allowing first-year deductions for both new and used equipment, and using both strategies together multiplies your write-offs substantially. A business that purchases $200,000 in equipment in December can deduct the entire amount immediately rather than spreading it across years, creating a six-figure tax reduction in a single year.

Home office deductions also carry substantial value that gets overlooked. The simplified method allows $5 per square foot up to 300 square feet, generating deductions up to $1,500 annually with minimal documentation. The actual expense method requires tracking utilities, insurance, and depreciation but often generates larger deductions for owners with dedicated office space.

Vehicle deductions follow similar logic to equipment purchases. Heavy vehicles exceeding 14,000 pounds qualify for full Section 179 treatment, while trucks and SUVs between 6,000 and 14,000 pounds face annual limits. Knowing these thresholds prevents purchasing the wrong vehicle and forfeiting deductions. Professional services, continuing education, software subscriptions, and business insurance round out the deductible landscape. Most business owners claim these reactively when paying bills rather than proactively planning to maximize them. A quarterly review of business expenses-identifying what you spent, what you can deduct, and what you missed-typically uncovers $3,000 to $8,000 in overlooked deductions annually. These gaps in deduction capture compound year after year, making systematic expense tracking the foundation for the advanced tax planning techniques that follow.

Income timing determines whether you pay tax this year or defer it to next year, and the difference compounds substantially over a career. A business owner who recognizes $50,000 in revenue in December versus January shifts that income into a different tax year with potentially different bracket implications. The strategy works both directions: defer income when you’re in a high bracket, accelerate deductions when you’re in a low bracket. If you anticipate a lower-income year due to business slowdown or planned sabbatical, pull forward deductible expenses into that year. Conversely, if you know next year will be higher-income, defer revenue recognition through careful invoicing timing or contract structuring.

Long-term capital gains receive preferential treatment at rates up to 23.8% compared to short-term gains taxed as ordinary income, making the holding period a tax lever you control directly. A business owner who sells an appreciated investment after 12 months and one day saves substantially compared to selling one day earlier. This distinction alone justifies calendar-based planning for investment sales.

Investment losses deserve equal attention to gains. Tax-loss harvesting offsets realized gains with losses, and you can deduct up to $3,000 of net losses against ordinary income annually, with excess losses carrying forward indefinitely. The mechanics matter: if you realize $30,000 in capital gains and harvest $25,000 in losses, you offset the gains entirely, deduct $3,000 against ordinary income, and carry forward $2,000 to future years. At typical tax rates, this strategy generates substantial simulated savings.

The wash-sale rule blocks claiming a loss if you repurchase the same or substantially identical investment within 30 days before or after the sale, so harvesting requires reinvesting in a similar but different security. This rule applies across all your accounts including IRAs and 401(k)s, so coordination matters. Trades must settle by year-end to count for the current year, typically December 31 unless that date falls on a weekend. Specific identification of which shares you sell lets you choose which lots to harvest, and using projection tools suggests which shares minimize taxes in many cases.

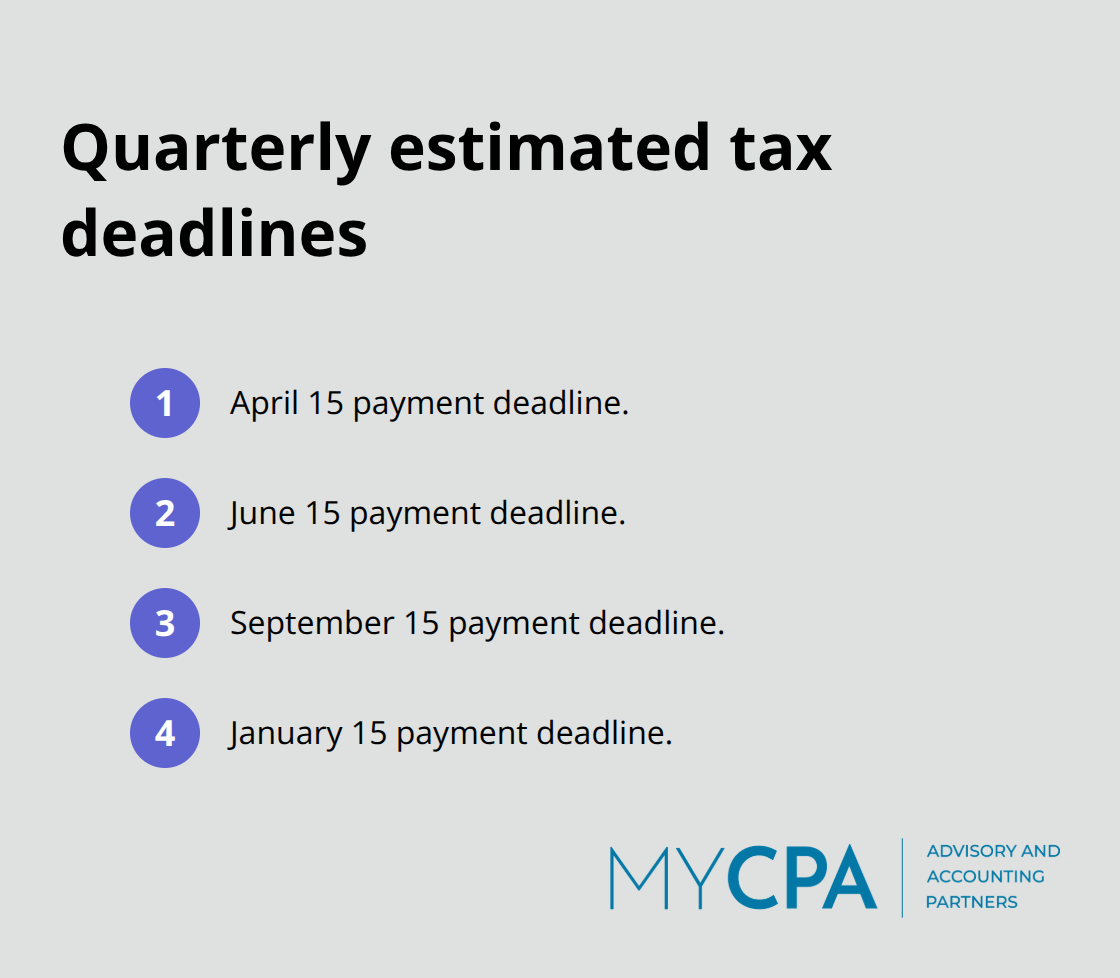

Quarterly estimated tax payments expose a critical timing mistake that costs many owners thousands annually. Underpayment triggers penalties and interest, while overpayment locks your cash with the IRS interest-free until refund. The IRS requires estimated payments if you expect to owe $1,000 or more after withholding, with payments due April 15, June 15, September 15, and January 15.

Many business owners guess at these amounts rather than calculating them precisely. A more effective approach divides your projected annual tax liability by four, adjusting the calculation quarterly as actual results emerge. If your first quarter income exceeds projections, increase subsequent payments; if it falls short, decrease them. This prevents both penalties and unnecessary overpayment.

Self-employed owners face an additional layer: self-employment tax on net earnings at 15.3% on 92.35% of net profit. A consultant earning $100,000 in profit pays roughly $14,130 in self-employment tax alone, separate from income tax. Quarterly estimates must account for both components. Owners structuring as S-corps gain leverage here because distributions escape self-employment tax entirely. A $150,000 income split into $90,000 W-2 wages and $60,000 distributions reduces self-employment tax from $21,000 to approximately $12,700, an $8,300 annual swing that flows directly to your bottom line. The complexity of calculating estimated taxes correctly makes this area ripe for error, yet the financial stakes justify precise quarterly planning rather than year-end scrambling.

Tax efficiency practices separate business owners who keep more money from those who leave it behind. The strategies outlined here-from capturing overlooked deductions and credits to timing income strategically and harvesting losses-compound into five-figure annual savings for most business owners. These aren’t theoretical concepts; they’re concrete actions that directly reduce what you owe.

Building a leaner tax strategy requires you to organize your records systematically so deductions and credits become visible rather than invisible. You must also review your business structure and retirement plan options annually to confirm you’re using the most tax-efficient vehicles available. Implement quarterly planning rather than year-end scrambling, adjusting estimated payments and income timing as your business evolves.

We at My CPA Advisory and Accounting Partners help business owners move from reactive tax filing to proactive tax planning. Our team minimizes your liabilities while our accounting expertise creates the organized records that make tax efficiency possible. Contact us to discuss how tax efficiency practices can strengthen your bottom line.

Privacy Policy | Terms & Conditions | Powered by Cajabra