Complex Accounting Solutions: Navigating Intricate Finances

Manage complex accounting solutions with practical strategies to reduce errors and strengthen your financial foundation.

Most startups fail because of cash flow problems, not bad ideas. At My CPA Advisory and Accounting Partners, we’ve seen firsthand how poor financial management derails promising businesses before they gain traction.

Getting startup bookkeeping basics right from day one separates companies that thrive from those that struggle. This guide walks you through the systems, tools, and practices that build a solid financial foundation.

Cash flow problems kill nearly half of startups within five years, according to failure rate research. This statistic isn’t about bad business models or weak demand-it’s about founders who didn’t track where their money went until it was too late. Bookkeeping acts as an early warning system that tells you whether your business is actually profitable or just burning through cash. Without accurate records, you’re flying blind. You won’t know if a customer payment landed in your account, whether that supplier invoice was paid, or if you have enough cash to cover next month’s payroll. The difference between startups that survive and those that fail often comes down to one thing: founders who knew their numbers from day one.

Your income statement shows profit or loss, but it doesn’t tell the whole story. A startup can show profit on paper while having zero cash in the bank because of timing mismatches between when you invoice customers and when they pay. Cash flow is what keeps the lights on. Bookkeeping gives you visibility into this gap. You’ll see exactly when customer payments arrive, when bills are due, and whether you have enough liquid cash to meet obligations. This isn’t theoretical-it’s the difference between making payroll and missing it.

Track your spending patterns monthly, not quarterly or annually. Monthly reconciliation catches fraud, errors, and spending leaks before they compound. Most startups that fail financially didn’t lack revenue; they lacked cash management discipline. The moment you understand your cash conversion cycle, you can make smarter decisions about extending payment terms to customers, negotiating better terms with suppliers, or timing major purchases.

The IRS expects organized records. If you can’t document your deductions, you lose them. Startups that mix personal and business expenses face audits, penalties, and disqualification of legitimate deductions. Federal guidance emphasizes paying business expenses by check and maintaining organized documentation to support deductions. Separate business and personal finances immediately. Open a dedicated business bank account and use a business credit card for all company expenses. This single step eliminates the most common compliance nightmare and makes tax preparation straightforward instead of chaotic.

Your tax obligation depends on your business structure-sole proprietor, LLC, S corporation, or C corporation each have different rules-and choosing the wrong structure costs thousands in unnecessary taxes. Quarterly estimated tax payments are required once profits appear, and missing these deadlines triggers penalties. Startups with multiple revenue streams, international transactions, or those seeking investor funding need accrual accounting instead of cash accounting because investors and lenders demand GAAP-compliant financial statements. A skilled tax professional can help you navigate these requirements and maximize available credits and deductions.

Founders who guess about their finances make expensive mistakes. Cutting the wrong expense, overinvesting in the wrong channel, or hiring too early happens when you don’t know your unit economics. Bookkeeping reveals gross margin-the percentage of revenue left after production costs-and this number determines whether your pricing strategy works. If your gross margin is 30 percent, you have limited room for operating costs, taxes, and cash reserves. A 60 percent gross margin gives you breathing room to scale.

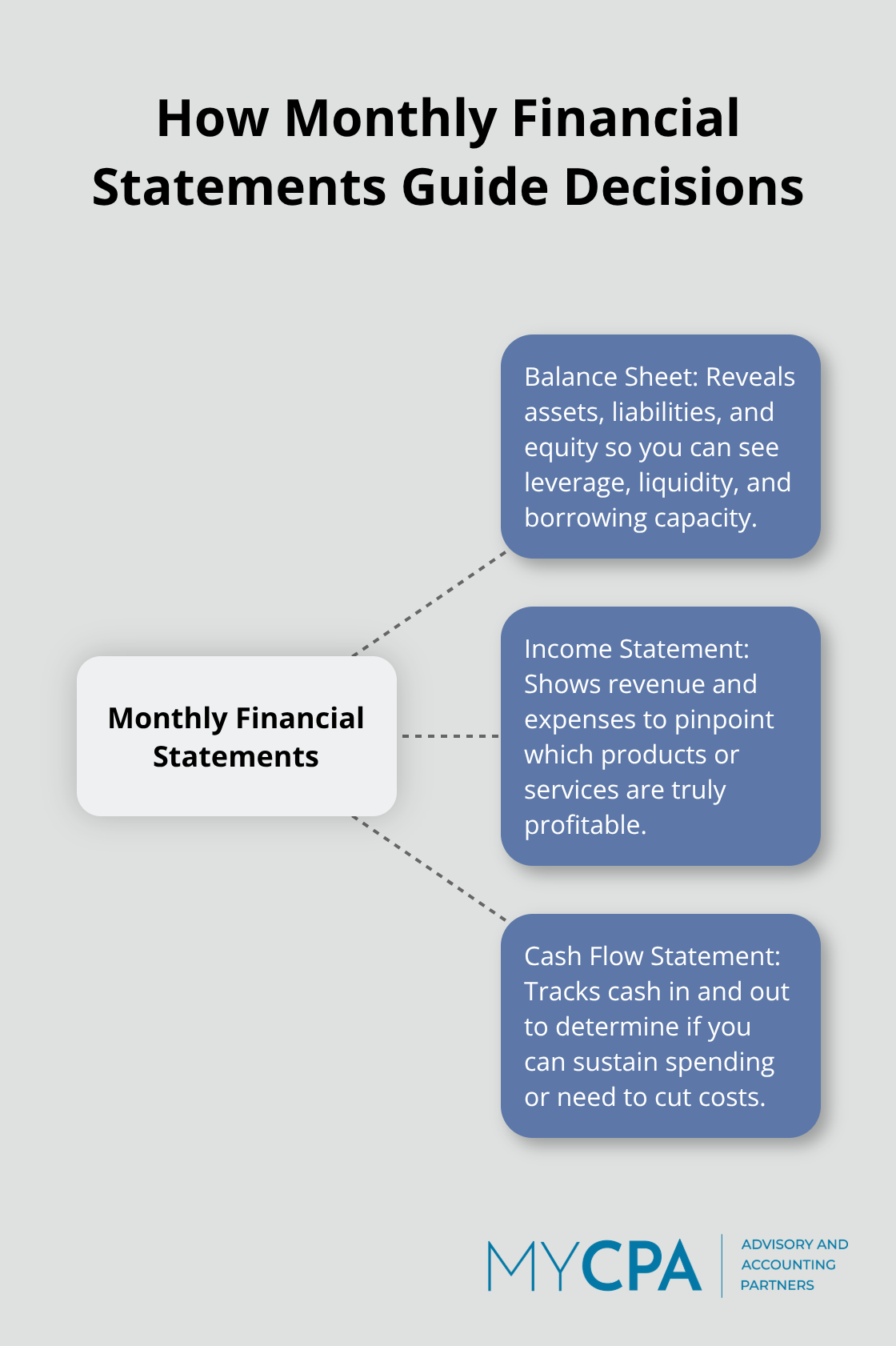

Customer acquisition cost and lifetime value come from accurate expense tracking. If you spend $500 to acquire a customer who generates $400 in lifetime revenue, that’s a losing equation that bookkeeping will expose immediately. Monthly financial statements (balance sheet, income statement, and cash flow statement) aren’t bureaucratic overhead. They’re decision-making tools. The balance sheet shows whether you’re overleveraged or have room to borrow.

The income statement reveals which products or services are actually profitable. The cash flow statement shows whether you can sustain current spending or need to cut costs. Startups that review these reports monthly catch problems early and adjust strategy before they become crises.

Getting these systems in place now positions you to handle the operational complexity that comes with growth. The next section walks you through the specific tools and structures that make bookkeeping manageable and scalable.

The right accounting software matters far more than most founders realize. QuickBooks Online costs around $30 per month for the Essentials plan and handles invoicing, expense tracking, and basic reporting-enough for startups with straightforward operations. Xero offers unlimited users across all plans, starting at $13 monthly, making it ideal if you’re collaborating with a bookkeeper or accountant from day one. Wave Accounting provides genuine free invoicing and expense tracking, though payroll processing incurs extra costs. The catch with Wave is scalability-as transaction volume grows and reporting needs become more complex, you’ll outgrow its capabilities. Zoho Books sits between these options with strong inventory and project management features at $10–$40 monthly, but the pricing structure becomes confusing as you add modules.

The decision hinges on one question: will your accountant or bookkeeper need access to your software? If yes, Xero wins because unlimited users mean no per-seat fees. If you manage books solo initially, QuickBooks Online offers the strongest integration ecosystem with third-party apps and the easiest handoff to a professional later. Test your choice for two weeks before committing. Most platforms offer free trials, and 14 days reveals whether the interface matches how your brain works.

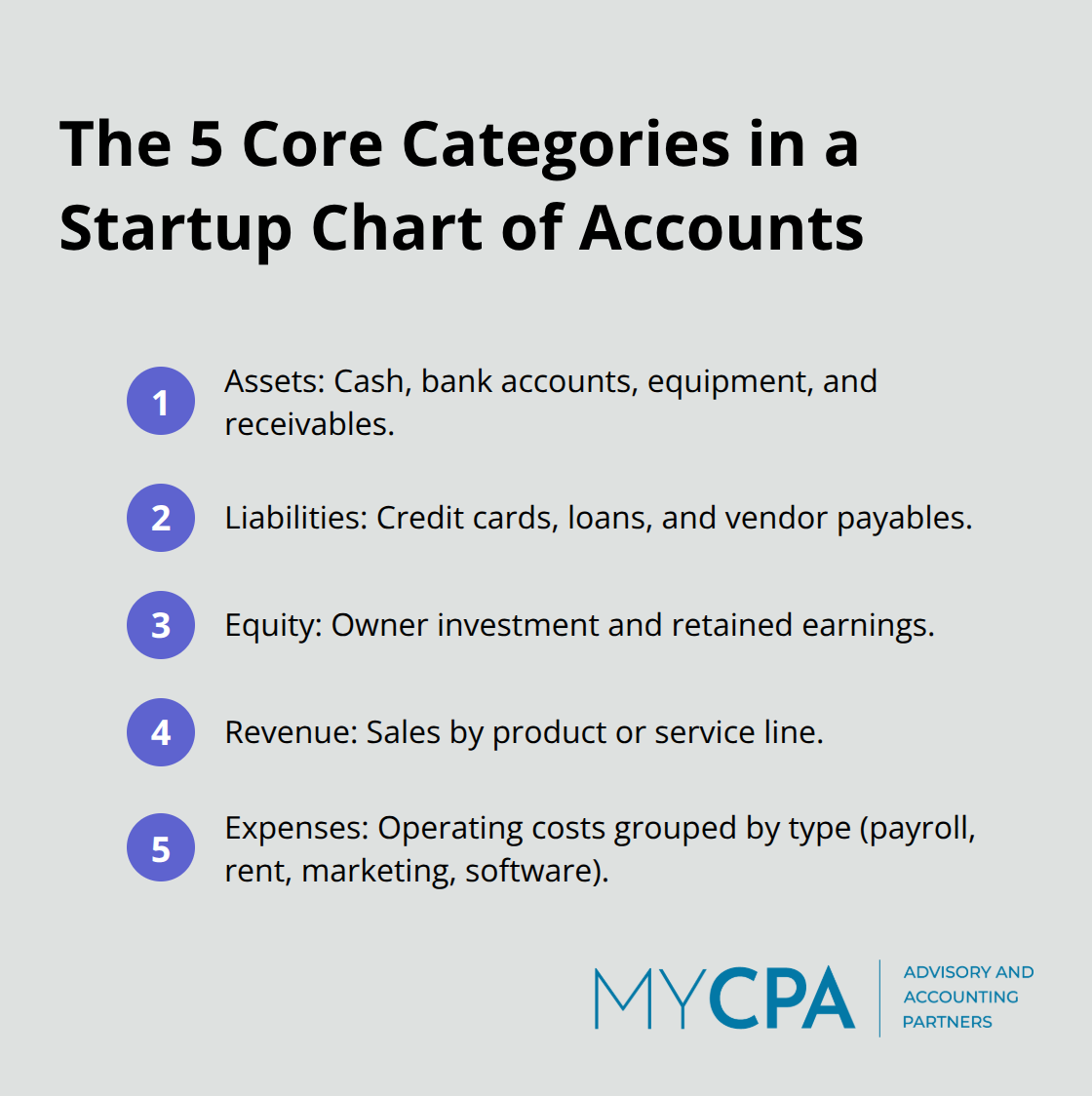

Your chart of accounts acts as the skeleton of your financial system. Organize it into five categories: assets (bank accounts, equipment), liabilities (credit cards, loans), equity (owner investment), revenue (sales by product line), and expenses (broken down by type).

Use a four-digit numbering system-assets start at 1000, liabilities at 2000, equity at 3000, revenue at 4000, and expenses at 5000. Within expenses, create subcategories: 5100 for payroll, 5200 for rent, 5300 for marketing, 5400 for software subscriptions.

Start simple and add detail as you grow; a bloated chart of accounts with 200 line items wastes time and creates reconciliation headaches. Your industry and growth stage should shape the structure. A SaaS startup needs different expense categories than a product-based business, and your chart should reflect where money actually flows in your operation. Many founders benefit from financial and accounting outsourcing services to design a chart tailored to their specific business model.

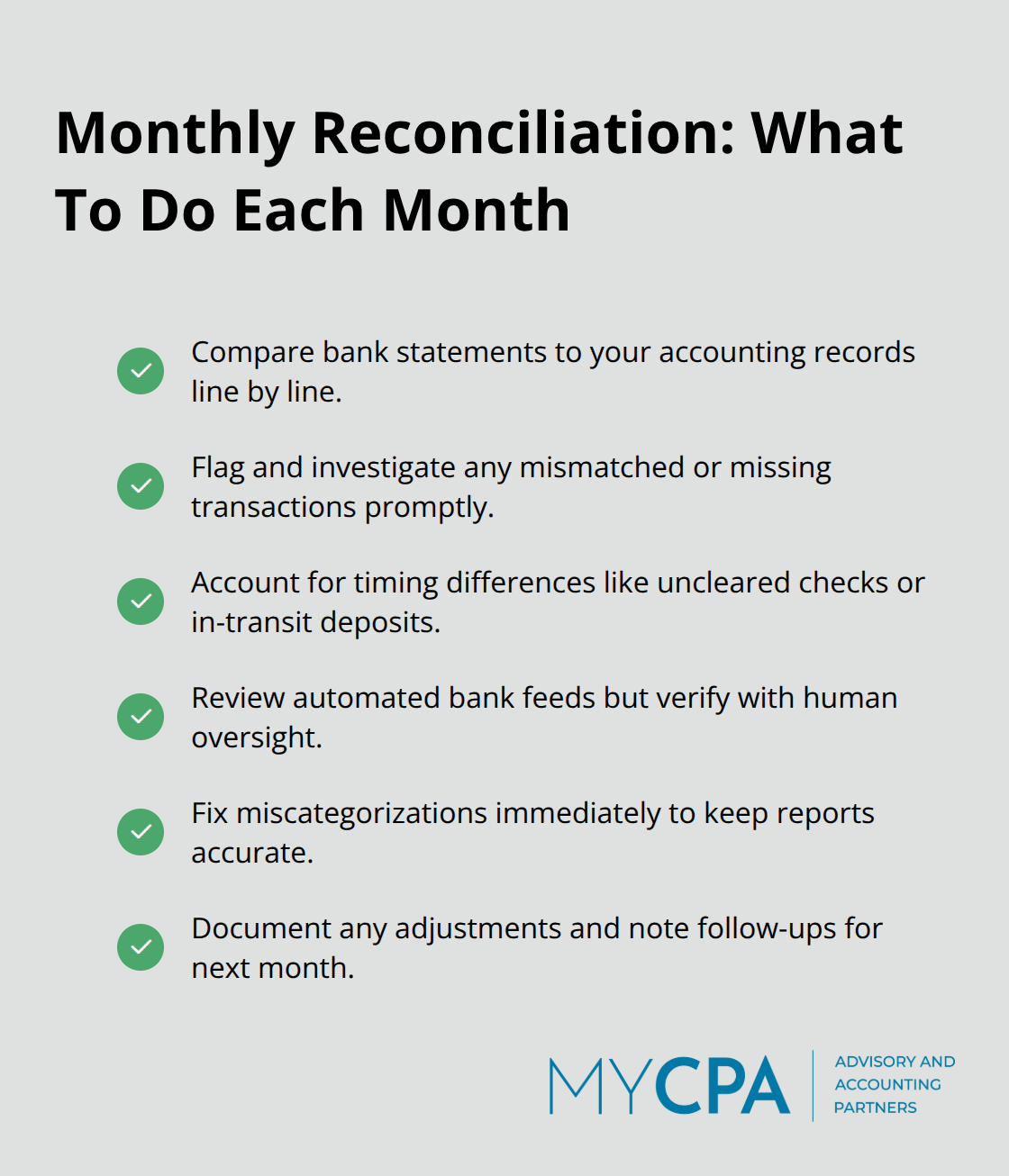

Monthly reconciliation is non-negotiable. Spend 30 minutes each month comparing your bank statement to your accounting software. Flag transactions that don’t match, investigate timing differences (checks that haven’t cleared), and catch unauthorized charges immediately. Most accounting software includes bank feeds that automatically import transactions, but automation isn’t a substitute for human review.

Categorization errors slip through constantly-a marketing expense gets coded as office supplies, a personal charge lands in the business account.

Monthly review catches these mistakes before they distort your financial statements. Set a calendar reminder for the same day each month, ideally within three days of month-end when transactions are fresh and memories are sharp. This discipline prevents small errors from compounding into major financial statement problems that take weeks to untangle later.

The three biggest bookkeeping failures follow a predictable pattern. Founders set up accounting software, get busy, and then abandon the discipline that makes the system work. The software itself isn’t the problem-it’s the habits and boundaries that surround it. A startup with QuickBooks and sloppy practices will fail financially faster than one using Wave Accounting with strict protocols. The infrastructure only matters if you actually use it correctly.

This mistake costs startups more money than founders realize. When personal and business expenses mixed in the same bank account, three problems emerge immediately. First, tax deductions disappear because the IRS won’t accept a deduction for an expense you can’t clearly document as business-related. A $50 coffee shop transaction that includes both a client meeting and a personal breakfast becomes impossible to categorize. Second, financial statements become unreliable. Your profit calculation is wrong because it includes personal spending that has nothing to do with business operations. Third, lenders and investors reject your financial statements outright. Every serious investor asks to see three years of bank statements, and mixed personal and business spending signals either incompetence or fraud.

Open a dedicated business bank account immediately and use it exclusively for business transactions. The moment a personal expense hits the business account, you’ve created a reconciliation problem that wastes hours to untangle. Use your personal account for everything personal, period. A business credit card for recurring expenses like software subscriptions, office supplies, and marketing costs takes 15 minutes to set up and eliminates the largest source of categorization errors in early-stage startups.

Most startups lose receipts because they lack a system, not because they don’t care. A receipt gets snapped on a phone, forwarded to email, maybe stored in a folder, and then forgotten when tax season arrives. The IRS requires documentation for every deduction you claim, and a missing receipt for a $2,000 software purchase means losing that deduction entirely. Create a single central repository for all receipts and invoices-either a physical folder organized by month or a cloud folder with consistent naming conventions. Timestamp every receipt with the transaction date and category. When you receive an invoice from a vendor, attach it to the corresponding transaction in your accounting software rather than storing it separately.

Startups that implement this discipline spend five minutes per week on document organization instead of 20 hours searching for receipts during tax preparation. Digital tools like Expensify or receipt scanners built into accounting software cut this time further (they automatically capture receipt data and match it to transactions). The payoff is immediate: you’ll have what you need when the IRS asks questions, and tax preparation becomes a straightforward process instead of a scramble.

This is the costliest mistake because it compounds. A transaction coded incorrectly in January remains wrong through December, distorting every monthly financial statement you produce. When you finally reconcile at year-end, you discover unexplained discrepancies, duplicate payments, or unauthorized charges that happened months earlier and are now harder to investigate. Monthly reconciliation helps identify errors or fraudulent activities and takes 30 minutes to complete. You’ll spot that duplicate vendor payment immediately, notice the software subscription that auto-renewed at a higher rate, and catch any fraudulent charges before they accumulate.

Startups that reconcile monthly have accurate financial statements every month, not just one accurate statement at year-end. This matters because monthly statements guide decisions. If you don’t reconcile until December, you’ve been making business decisions based on potentially inaccurate numbers for 11 months. You might overspend on inventory, delay necessary equipment upgrades, or miss seasonal cash flow patterns that could derail payroll. Set a calendar reminder for the same day each month, ideally within three days of month-end when transactions are fresh and memories are sharp. This discipline prevents small errors from compounding into major financial statement problems that take weeks to untangle later.

Startup bookkeeping basics form the foundation that separates businesses that survive from those that fail. The systems you build now determine whether you’ll have accurate financial statements next quarter, whether the IRS will accept your deductions, and whether you can make decisions based on facts instead of guesses. A dedicated business bank account, organized receipts, monthly reconciliation, and the right accounting software take weeks to implement but save hundreds of hours and thousands of dollars later.

Monthly financial statements reveal which products generate profit and which drain cash, while accurate records attract investors and lenders who demand GAAP-compliant statements. Clean books eliminate the scramble during tax season and reduce the risk of penalties or disqualified deductions. Most importantly, you’ll know whether your business is actually profitable or just moving money around.

If you’re uncertain about your chart of accounts structure, which accounting software fits your business, or how to navigate tax obligations as you scale, professional guidance accelerates the process. We at My CPA Advisory and Accounting Partners offer accounting services, QuickBooks setup and management, and business advisory tailored to early-stage companies. Visit My CPA Advisory and Accounting Partners to explore how we can help you establish a bookkeeping foundation that works.

Privacy Policy | Terms & Conditions | Powered by Cajabra