Tax Compliance Reporting Basics: Understand Your Requirements

Learn tax compliance reporting basics and understand your filing requirements to avoid penalties and stay audit-ready.

Tax compliance reporting basics aren’t optional-they’re a legal requirement that affects every business and individual who earns income. Missing deadlines or filing incorrectly can result in penalties, audits, and unnecessary stress.

We at My CPA Advisory and Accounting Partners help clients navigate these requirements with clarity and confidence. This guide breaks down what you need to know to stay compliant and avoid costly mistakes.

Tax compliance reporting is the formal process of documenting your income, expenses, and tax obligations to federal, state, and sometimes local authorities. It extends far beyond filing a tax return once yearly. The IRS receives over 266.6 million tax returns annually, with roughly 174.4 million representing individual and corporate income tax returns. Each one constitutes a legal declaration of financial activity.

The core components include accurate income reporting from all sources-wages, self-employment, investments, rental properties-along with legitimate deductions and credits you qualify for. You also must file information returns like 1099s and W-2s if you operate a business or employ staff, maintain detailed records for at least three years (longer for certain situations), and meet specific deadlines that vary by entity type and jurisdiction. The compliance burden is substantial: Americans spend roughly 7.1 billion hours annually on tax filing and reporting, according to the Office of Information and Regulatory Affairs. For individual filers, the average time commitment is 12 hours in 2025, down slightly from 13 hours in 2024, but out-of-pocket costs remain around $290. If you operate a business using Schedule C or other business provisions, expect roughly 21 hours and $610 to $620 in costs. This isn’t theoretical-it represents real time and real money that directly impacts your bottom line.

The consequences of non-compliance are severe and expensive. The IRS tax gap-the difference between taxes owed and taxes actually paid-reached $606 billion in Tax Year 2022, with underreporting of income accounting for roughly $539 billion of that shortfall. While IRS audit rates have dropped significantly due to budget constraints, falling from around 1 percent in 2011 to 0.3 percent in 2018, the agency actively invests in enforcement for high-income taxpayers and businesses. Penalties for late filing reach 5 percent of unpaid taxes per month, and accuracy-related penalties add 20 percent to underpaid amounts.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. Businesses face even steeper consequences: failing to file payroll tax returns on time triggers penalties starting at 2 to 10 percent depending on how late the filing occurs. Beyond penalties, non-compliance creates audit risk, damages credibility with lenders and investors, and can result in personal liability for business owners. For self-employed individuals, rental property owners, and those with pass-through business income, the stakes are higher because third-party reporting doesn’t catch everything-the IRS relies partly on your honesty and accuracy.

The specific reports you file depend entirely on your situation. Individual filers submit Form 1040, which generates about 2.129 billion hours of compliance burden across the country annually. Business owners file Form 1120 for C corporations or Schedule C for sole proprietorships. Employers must file Form 941 quarterly, which accounts for roughly 470 million hours of burden nationally. If you have employees, you also file W-2s and W-3s. Investment income triggers 1099 forms: 1099-INT for interest, 1099-DIV for dividends, 1099-B for brokerage transactions, and 1099-NEC for non-employee compensation. Self-employed individuals report quarterly estimated taxes using Form 1040-ES. Form 1099-B reporting creates a significant compliance burden, particularly for businesses handling brokerage transactions.

State and local requirements add another layer: sales tax returns, state income tax returns, property tax filings, and industry-specific reports. Multi-state businesses face compounding complexity because rates, rules, and deadlines differ across jurisdictions. This is where most business owners stumble-they understand federal requirements but miss state deadlines or file incorrectly, triggering penalties they didn’t anticipate. Understanding your specific filing obligations across all applicable jurisdictions determines whether you stay compliant or face costly mistakes.

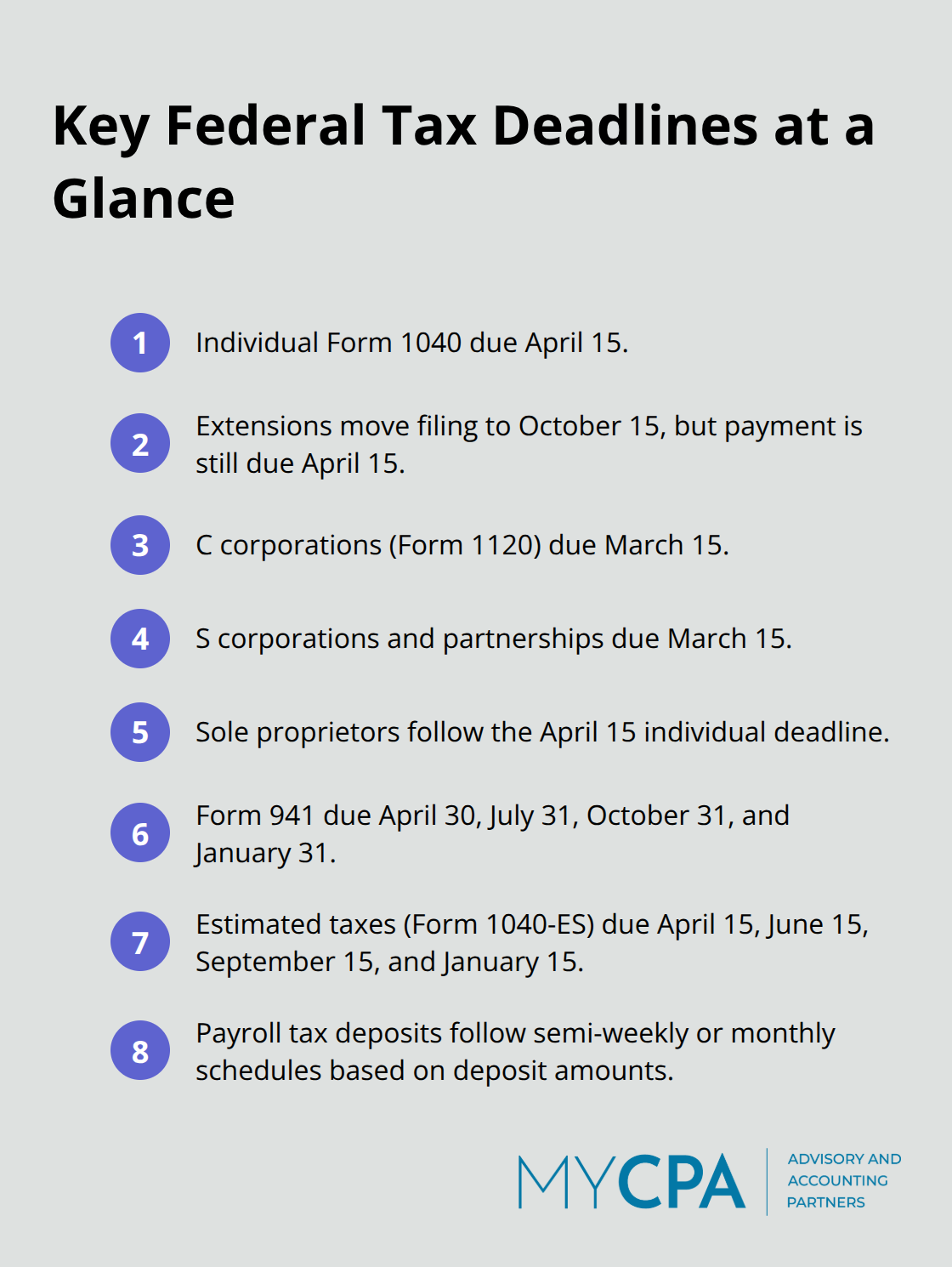

Federal tax deadlines are fixed and unforgiving. Individual income tax returns must reach the IRS by April 15 each year, with extensions pushing the deadline to October 15-though extensions only delay filing, not payment. If you owe taxes, you must pay by April 15 regardless of extension status. Businesses face different schedules: C corporations file Form 1120 by March 15, S corporations and partnerships file by March 15, and sole proprietors follow the April 15 individual deadline. Employers must file Form 941 quarterly by April 30, July 31, October 31, and January 31, with payroll taxes deposited on semi-weekly or monthly schedules depending on deposit amounts. Self-employed individuals owe quarterly estimated taxes on Form 1040-ES, due April 15, June 15, September 15, and January 15.

Missing these deadlines triggers failure-to-file penalties of 5 percent per month up to 25 percent of unpaid taxes, plus interest that compounds daily. The IRS processes roughly 266.6 million returns annually, and their systems flag late filings automatically, so extensions don’t hide missed deadlines from federal records.

State and local requirements add significant complexity to your compliance calendar. Most states require income tax returns aligned with federal deadlines, but some impose earlier or separate deadlines that catch business owners off guard. Sales tax returns vary wildly across jurisdictions: some states demand monthly filings, others quarterly, and a few annually, with penalties ranging from 2 to 10 percent for late submission depending on location. Property tax deadlines typically fall in December or early spring, varying by county. Payroll withholding reports must match federal schedules, but some states add their own state unemployment insurance filings on top of federal requirements.

Multi-state businesses face compounding complexity because compliance calendars differ across jurisdictions, and missing a single state deadline creates penalties that accumulate quickly. A business operating in three states might track nine different sales tax deadlines alone, each with its own rate and reporting format.

Documentation standards are non-negotiable and often overlooked by business owners. The IRS requires you to maintain records for at least three years, though six years applies if you underreport income by more than 25 percent, and indefinitely for fraud cases.

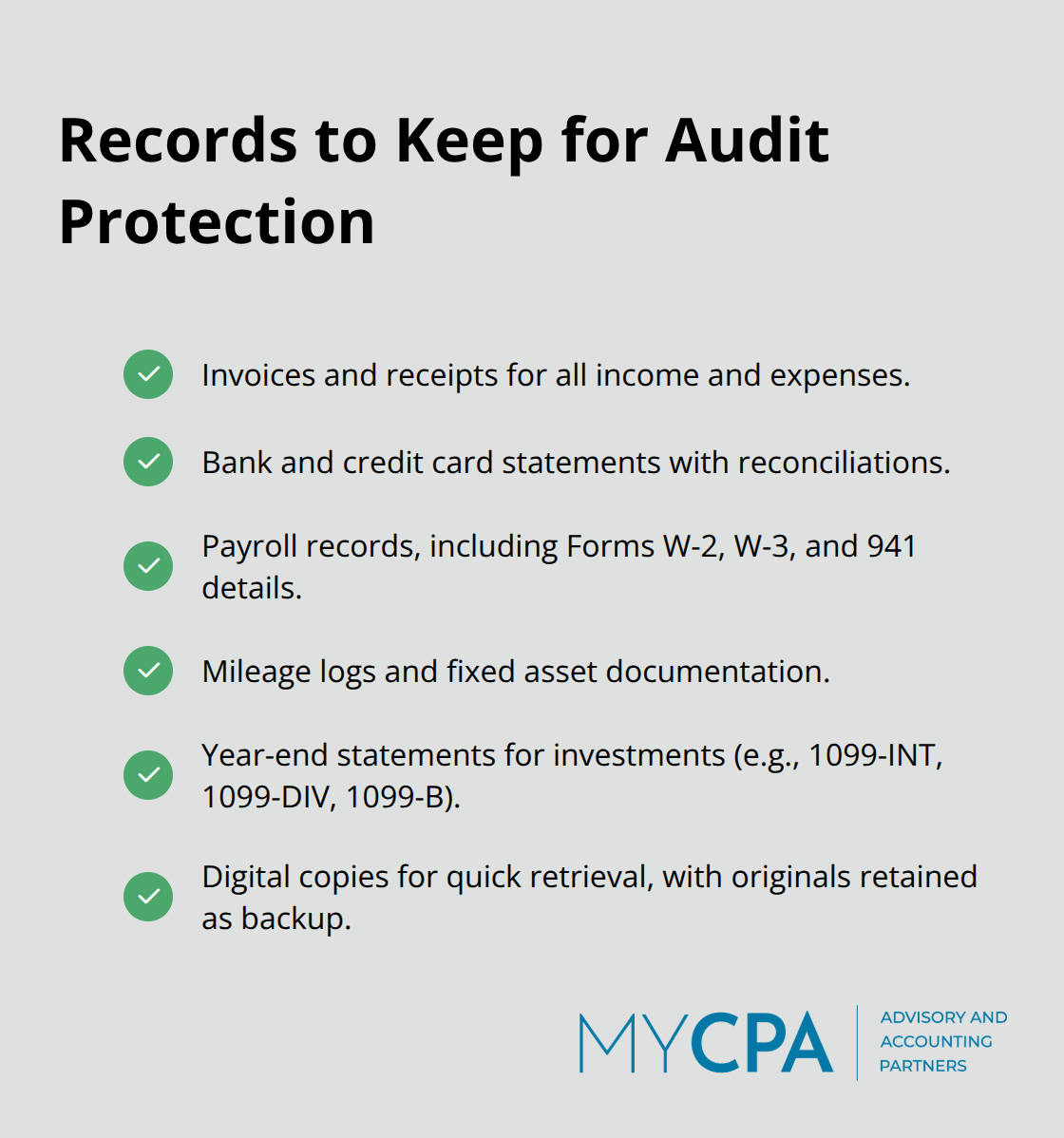

Records must include invoices, receipts, bank statements, payroll records, mileage logs for vehicle deductions, and supporting documentation for all claimed deductions. Digitizing records saves space and improves retrieval speed during audits, but you should retain original documents as backup.

The compliance burden across all tax forms totals roughly 7.1 billion hours annually in the United States, with out-of-pocket costs around $148 billion. Business owners spend substantially more than individual filers: roughly 21 hours and $610 to $620 in costs annually compared to 12 hours and $290 for non-business filers. Organizing records before tax season reduces preparation time significantly and protects you if the IRS questions your return.

Create a centralized system that separates folders for income documents, expense receipts, payroll records, and investment statements. Timestamp everything and cross-reference documents to corresponding tax line items. This preparation transforms a chaotic scramble into a manageable process and makes audits far less painful if they occur. Many business owners find that setting up these systems early in the year-rather than scrambling in March or April-saves weeks of stress and reduces the risk of missing critical documentation.

The complexity of multi-jurisdictional compliance, combined with the volume of records you must maintain, makes professional guidance valuable for most business owners. We at My CPA Advisory and Accounting Partners help clients establish these systems and stay on top of deadlines across all applicable jurisdictions, so you can focus on running your business rather than chasing filing dates.

Organization separates businesses that glide through tax season from those that scramble in April. The compliance burden for individual filers averages 12 hours annually, but business owners spend roughly 21 hours managing tax obligations. That gap widens dramatically when you lack systems. Most business owners fail at organization not because they’re careless, but because they treat tax compliance as a once-yearly event rather than an ongoing process.

Penalties compound quickly when you miss deadlines. Failure-to-file penalties start at 5 percent of unpaid taxes per month, accuracy-related penalties add 20 percent to underpaid amounts, and payroll tax penalties range from 2 to 10 percent depending on how late you file. One missed state sales tax deadline in a multi-state operation costs far more than setting up a proper system upfront. The IRS processes 266.6 million returns annually, and their systems flag late filings automatically-there’s no hiding from missed deadlines.

Start with a digital calendar that lists every federal, state, and local deadline applicable to your business-not just April 15, but quarterly estimated tax payments, monthly payroll deposits, state unemployment insurance filings, and sales tax returns specific to each jurisdiction you operate in. Use a spreadsheet or accounting software to track which documents you need for each filing: invoices, receipts, bank statements, payroll records, and mileage logs. Assign responsibility to a specific person or team member, not a vague hope that it gets done.

Digital organization saves time during preparation. Business owners who maintain organized records reduce their annual compliance time significantly compared to those who scramble to gather documents in March. Set up separate folders for income documents, expense receipts, and supporting documentation. Timestamp everything and cross-reference documents to corresponding tax line items. This preparation transforms a chaotic scramble into a manageable process and makes audits far less painful if they occur.

The most common mistake business owners make is assuming their accountant or bookkeeper will catch everything without clear communication about what they’re responsible for. Establish explicit expectations: who tracks deadlines, who gathers documents, who communicates with the IRS or state agencies. The second mistake is underestimating the cost of non-compliance. Missing a single quarterly estimated tax payment can trigger underpayment penalties that compound across the year. Failing to file a state payroll tax return on time creates penalties that start immediately and grow monthly.

The third mistake is treating documentation carelessly. The IRS requires records for at least three years, but six years applies if you underreport income by more than 25 percent. Digitizing records saves space and improves retrieval speed during audits, but you should retain original documents as backup. Many business owners discover too late that they lack the documentation to support their deductions when audited.

Professional guidance prevents these mistakes from happening in the first place. A qualified advisor who understands your business structure, income sources, and multi-state operations can flag compliance gaps you’d otherwise miss until penalties arrive. The complexity that most business owners underestimate-managing multi-jurisdictional compliance alone-creates substantial risk. A business operating in three states faces nine different sales tax deadlines alone, each with its own rate and reporting format. Payroll tax complexity multiplies when you add state unemployment insurance requirements on top of federal deposits. Working with experienced professionals addresses these layers of complexity and protects your bottom line from preventable penalties.

Tax compliance reporting basics come down to three hard truths: deadlines never move, penalties cost real money, and organization prevents both. The IRS processes 266.6 million returns annually and flags late filings automatically, so missing even one deadline triggers penalties that compound monthly. Business owners spend roughly 21 hours annually managing tax obligations, but that time shrinks dramatically when you establish systems from the start.

Staying on top of requirements protects your bottom line far beyond avoiding penalties. Organized records reduce audit friction if the IRS questions your return, and clear documentation of income, expenses, and deductions strengthens your position if disputes arise. Timely filings maintain credibility with lenders, investors, and business partners who review your tax history, while multi-jurisdictional compliance becomes manageable rather than chaotic when you track deadlines across all applicable jurisdictions upfront.

We at My CPA Advisory and Accounting Partners help business owners and individuals navigate these requirements with clarity and confidence. Our team provides tax services, accounting services, and business advisory to create personalized financial plans tailored to your situation. Contact us to discuss how we can transform tax compliance from a source of stress into a managed process that protects your financial health.

Privacy Policy | Terms & Conditions | Powered by Cajabra