Tax Compliance Audits: Preparing with Confidence

Prepare for tax compliance audits with confidence using our expert strategies, common audit triggers, and practical steps to protect your business.

Tax compliance audits can feel overwhelming, but they don’t have to be. At My CPA Advisory and Accounting Partners, we’ve helped countless clients navigate audits with clarity and confidence.

This guide walks you through what to expect, how to organize your records, and the steps to take when an audit comes your way. You’ll learn practical strategies that turn audit anxiety into audit readiness.

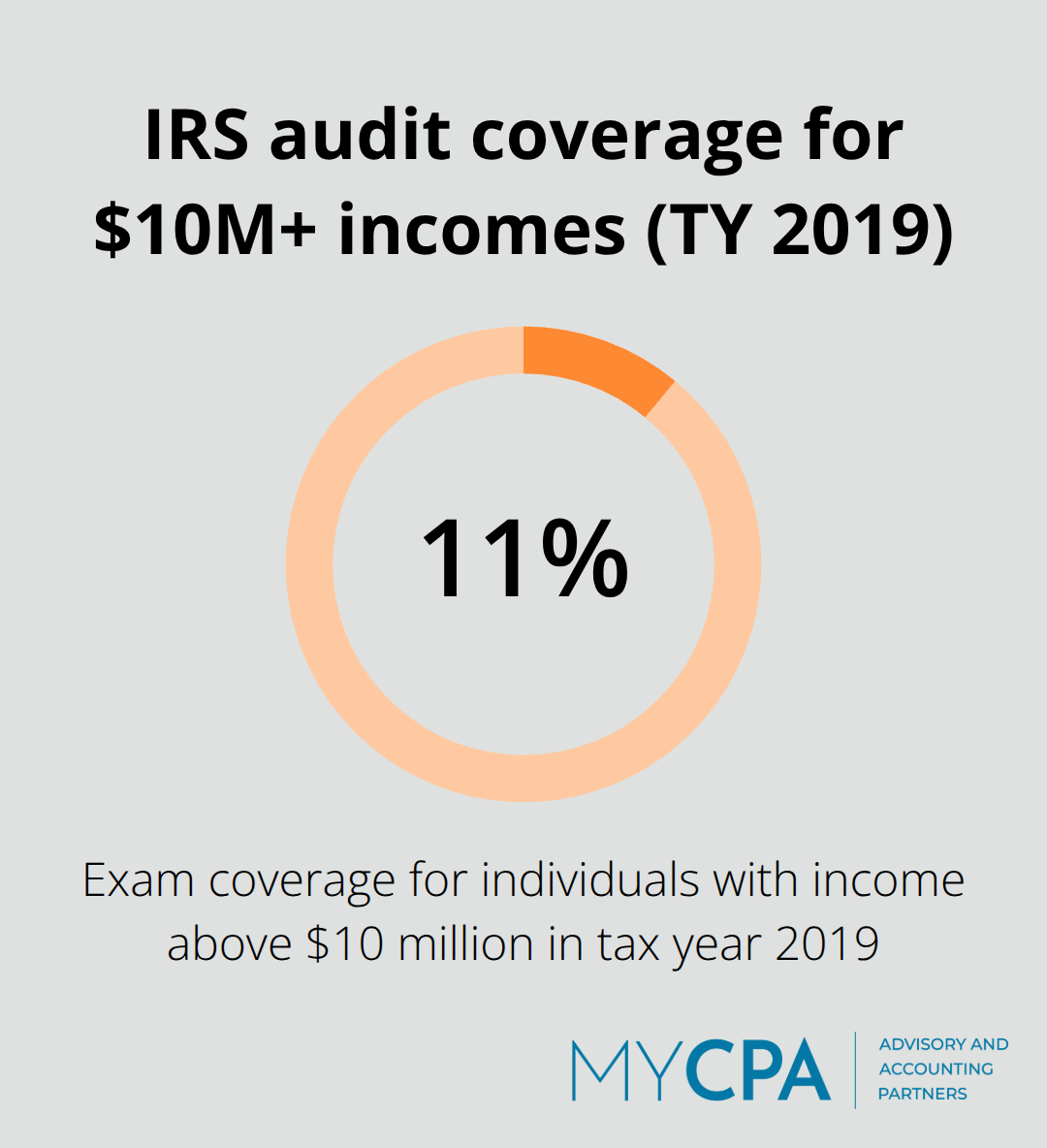

The IRS closed over 505,000 tax audits in fiscal year 2024, resulting in nearly $29 billion in recommended additional taxes according to the IRS Data Book audit statistics. This scale matters because it shows audits are real, but your actual risk remains low-less than 0.50% of individual returns faced audit selection between 2020 and 2023, the lowest rate since 1950. The IRS typically selects returns through random sampling, computerized screening that flags discrepancies, or information matching between what you reported and what employers or financial institutions reported on Forms W-2 and 1099. Correspondence audits, handled entirely by mail, represent the most common approach and often involve straightforward questions about specific deductions or income items. Field audits, where an IRS agent visits your business or meets with you in person, occur less frequently but carry more intensity-they typically target higher-income individuals or complex business structures. For very high-income earners above $10 million, exam coverage reached 11.0% in tax year 2019, meaning your audit probability increases significantly at that level.

The IRS can examine your last three years of returns under normal circumstances, but this window extends to six years if substantial errors surface.

The IRS employs multiple selection methods to identify returns for examination. Random sampling pulls returns without regard to specific characteristics, while computerized screening flags returns that contain patterns the agency associates with higher risk. Information matching compares your reported figures against third-party documents filed by employers, banks, and other institutions. This three-pronged approach means the IRS catches many discrepancies automatically before any human review occurs. Understanding these mechanics removes much of the mystery surrounding audits and positions you to respond strategically rather than reactively.

Unreported income ranks as the single most common audit trigger because the IRS compares your reported income directly against third-party documents like W-2s and 1099s through automated matching programs. The Automated Underreporter program closed 1.2 million cases in fiscal 2024, generating $7.7 billion in additional assessments. Schedule C filers face particular attention, especially those reporting losses or operating cash-intensive businesses-the IRS views these as higher-risk categories. Home office deductions, vehicle deductions claiming 100% business use, and excessive deductions relative to your income level draw scrutiny because they appear frequently on audited returns. Hobby losses also flag returns when you cannot demonstrate a profit motive, though the IRS generally accepts a business if you show profit in at least three of five years. Cryptocurrency transactions face intensified enforcement through a dedicated IRS compliance campaign, so any digital asset transactions require meticulous documentation.

The key insight here is that audits rarely happen randomly-they follow patterns the IRS has identified through decades of enforcement data. This means your preparation strategy should directly address these high-scrutiny areas with organized, contemporaneous documentation that proves your positions. When you organize your records before an audit notice arrives, you shift from a defensive posture to one of confidence. The next section walks you through exactly which documents and records you need to gather and how to organize them for maximum effectiveness.

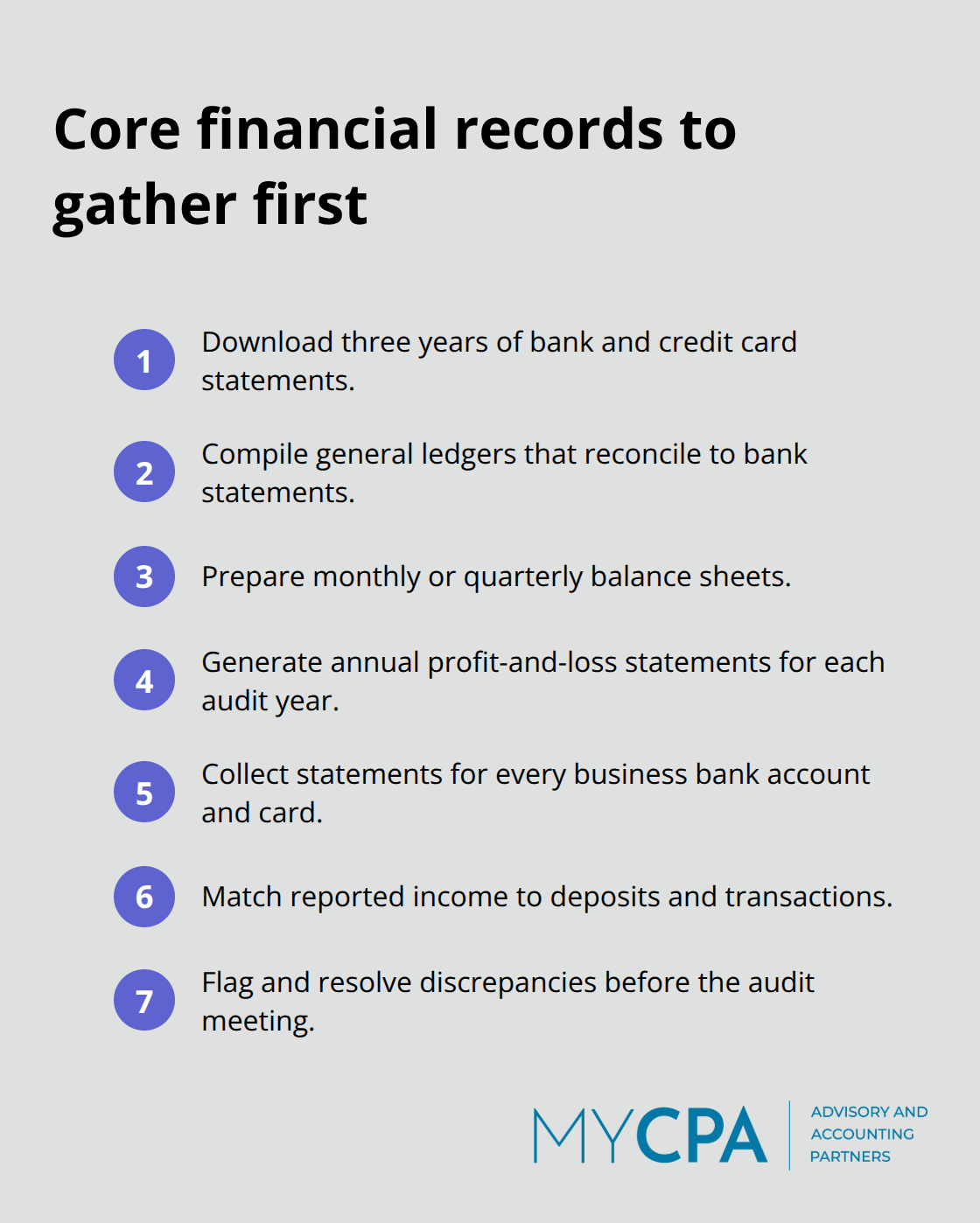

Organizing records before an audit notice arrives separates those who navigate audits smoothly from those who scramble. The foundation starts with your financial statements and bank records, which form the backbone of any audit defense. You need general ledgers that reconcile to your bank statements, monthly or quarterly balance sheets, and profit-and-loss statements for each year under examination. Pull statements from every business bank account and credit card for the full audit period, not just summaries. The IRS cross-references your reported income against deposits and transactions, so discrepancies between your tax return and actual bank activity invite additional questions.

Many business owners fail to align their records and discover mid-audit that their documentation doesn’t match, forcing them to reconstruct transactions or explain gaps. Start downloading three years of bank and credit card statements now, even if you haven’t received an audit notice.

Gather every receipt, invoice, and supporting document for expenses you claimed on your tax return. The IRS doesn’t randomly select deductions to challenge-it targets categories where documentation frequently falls short. Vehicle expenses demand mileage logs showing dates, destinations, and business purpose for every trip claimed; claiming 100% business use without detailed logs guarantees scrutiny. Home office deductions require documentation of the square footage used exclusively for business, utility bills showing the home’s total size, and records of renovations or furniture purchases related to that space. Meal and entertainment expenses need receipts showing the amount, date, attendees, and business purpose written on the receipt itself or in a contemporaneous log. Charitable contributions must include written acknowledgment from the charity confirming the donation amount. If you operate a cash-intensive business or reported significant losses on Schedule C, organize all income records alongside expense documentation to demonstrate your profit motive and legitimate business operations.

Payroll records demand equal attention because employment tax compliance directly affects audit outcomes. Maintain copies of all W-2s issued, Form 941 quarterly payroll tax returns, state payroll tax filings, and unemployment insurance documentation for the audit period. Reconcile your payroll records to your general ledger to confirm wages expense matches what you reported on your tax return and what you reported to the IRS on quarterly filings. Employee records should include I-9 verification forms, wage agreements, and timekeeping records that support the wages you paid. If you classified workers as independent contractors, retain the agreements and 1099 forms issued, along with documentation of why you treated them as contractors rather than employees-the IRS frequently challenges contractor classifications, particularly in construction and service industries.

Create a master file for each audit year containing these three document categories organized chronologically or by account. Use folders, spreadsheets, or dedicated software to index what you have and where it’s located; when an auditor requests specific records, you’ll retrieve them in minutes rather than hours. This level of preparation signals competence and reduces the likelihood that the auditor will expand the scope of the examination beyond initial items. With your documents organized and ready, you now face the critical question: how do you actually respond when the IRS contacts you, and what rights do you have during the process?

The moment an audit notice arrives, your instinct might be to panic or delay. That’s exactly wrong. The IRS expects a response within thirty days for correspondence audits, and missing this deadline signals non-cooperation that invites expanded scrutiny. Your first action should be to read the notice carefully and identify exactly which tax years and specific items the IRS questions. Many audit notices target only certain deductions or income categories, not your entire return.

Respond promptly and directly to what was asked, nothing more. Provide only the documents the auditor explicitly requested rather than flooding them with everything you have. This focused approach prevents you from volunteering information that raises additional questions. If the notice requests field examination, you have the right to conduct the audit at your CPA’s office instead of your business location, which gives you more control over the environment and allows your tax professional to manage the conversation. Schedule the appointment at least two weeks out to gather materials and prepare. Before the meeting, review your documentation thoroughly with your tax professional to identify weak areas and develop explanations for any questionable positions. Walking into an audit unprepared costs you credibility and often extends the examination timeline.

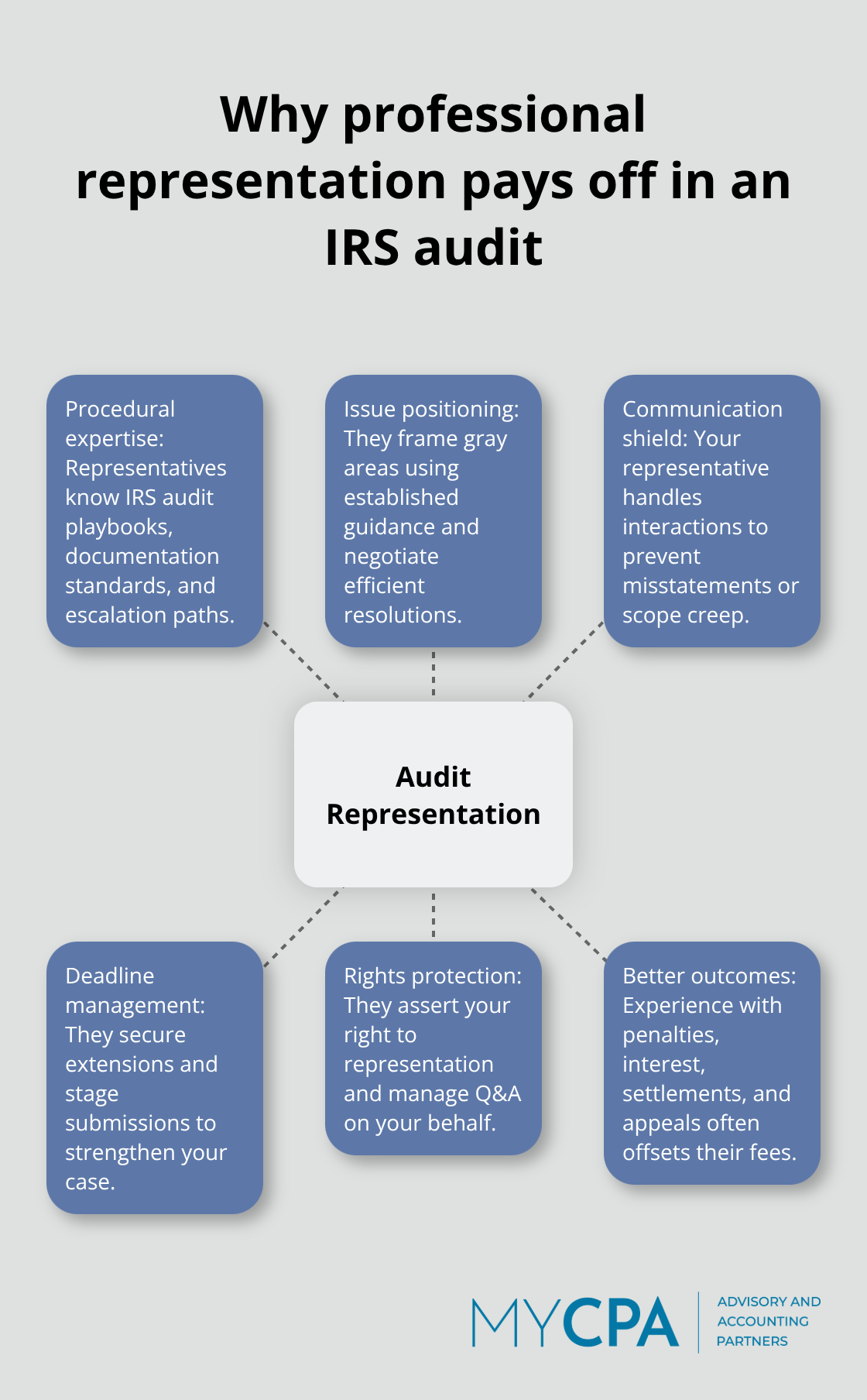

The second critical decision is whether to handle this alone or engage professional representation. Tax professionals understand audit procedures, IRS positions on common issues, and settlement strategies that individuals typically miss. The IRS conducts audits as adversarial proceedings, and an examination can assess additional taxes, penalties, and interest-so the cost of professional representation usually pays for itself through better outcomes. You have the legal right to representation throughout the audit process, including the right to have your representative answer questions on your behalf so you don’t inadvertently contradict your documentation or admit positions you didn’t intend.

During correspondence audits, your CPA or tax attorney handles all communication directly with the IRS, eliminating direct contact that often leads to misstatements. If the auditor requests documents you cannot locate, your representative can request reasonable time extensions rather than admitting the documents don’t exist. The IRS allows multiple submission deadlines during an audit, so professional representation ensures you maximize each opportunity to strengthen your position. When the examination concludes, your representative receives the audit report first, reviews it for errors, and determines whether to accept the findings or pursue appeals. This final layer of professional judgment protects your rights and prevents you from accepting unfavorable determinations you could have challenged successfully.

Tax compliance audits don’t have to derail your business or personal finances. The strategies outlined in this guide address the core challenge: preparation transforms uncertainty into control. Organizing your financial statements, bank records, expense documentation, and payroll records before an audit arrives eliminates the scramble that costs time and credibility, while understanding how the IRS selects returns through automated matching removes the mystery and helps you focus on high-scrutiny areas like unreported income, Schedule C losses, and vehicle deductions.

Professional guidance extends far beyond the audit itself. Tax professionals identify weak positions early, negotiate with the IRS on your behalf, and protect your rights throughout the examination process-they understand settlement strategies, appeal procedures, and the nuances of IRS positions that individuals typically overlook. This expertise often recovers more in favorable outcomes than the cost of representation, and responding promptly to audit notices while providing only requested documentation shifts the dynamic from defensive to strategic.

Treat tax compliance audits as an ongoing practice rather than a crisis response. Review your records quarterly, reconcile your tax positions annually, and maintain contemporaneous documentation for every significant deduction. Contact My CPA Advisory and Accounting Partners to create a tailored audit-prep plan that fits your specific situation and protects your financial interests.

Privacy Policy | Terms & Conditions | Powered by Cajabra