How to Implement Effective Tax Planning Strategies

Boost financial outcomes with effective tax planning strategies. Learn how to save more, reduce liabilities, and secure your financial future.

Most businesses and individuals leave thousands of dollars on the table each year by failing to implement proper tax planning strategies. The difference between reactive tax preparation and proactive planning can mean significant savings.

We at My CPA Advisory and Accounting Partners see clients reduce their tax burden by 15-30% through strategic planning. Smart timing and documentation make all the difference.

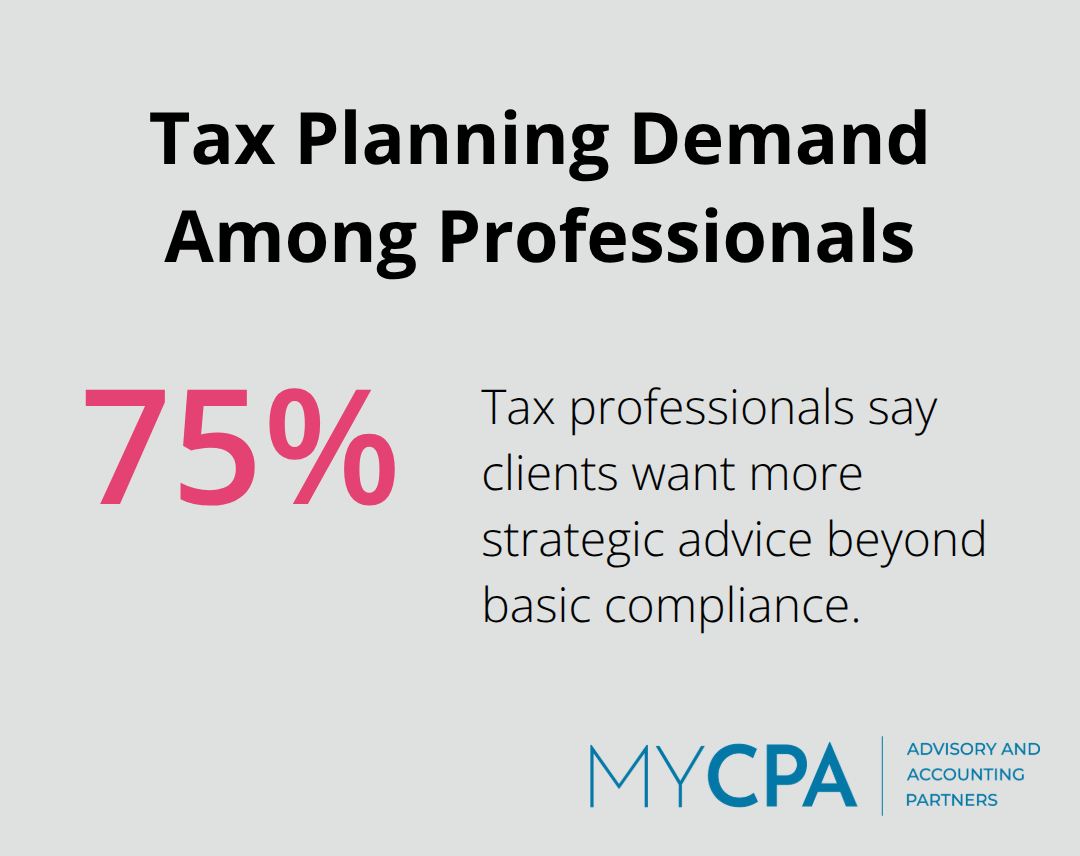

Tax preparation focuses on returns based on what already happened during the year. Tax planning shapes financial decisions throughout the year to minimize tax liability. 75% of tax professionals report clients want more strategic advice beyond basic compliance work.

Tax preparation looks backward and reacts to completed transactions. Planning looks forward and creates opportunities for tax savings. This proactive approach allows taxpayers to structure transactions before they occur rather than accept whatever tax consequences result.

Legal tax avoidance uses legitimate strategies within tax law to reduce liability. Tax evasion involves illegal methods to hide income or inflate deductions. The IRS applies a 7% interest rate on underpayment penalties in 2025, which makes compliance expensive for those who miscalculate.

Smart taxpayers maximize deductions through documented charitable contributions, retirement account contributions, and business expense coordination. The key difference lies in transparency – legitimate strategies withstand IRS scrutiny because they follow established rules. Proper documentation supports every deduction claimed.

Income and deduction coordination can save thousands annually. Self-employed individuals can defer invoices until January to push income into the following tax year when rates might be lower. Alternatively, income acceleration into the current year makes sense when expecting higher future tax rates.

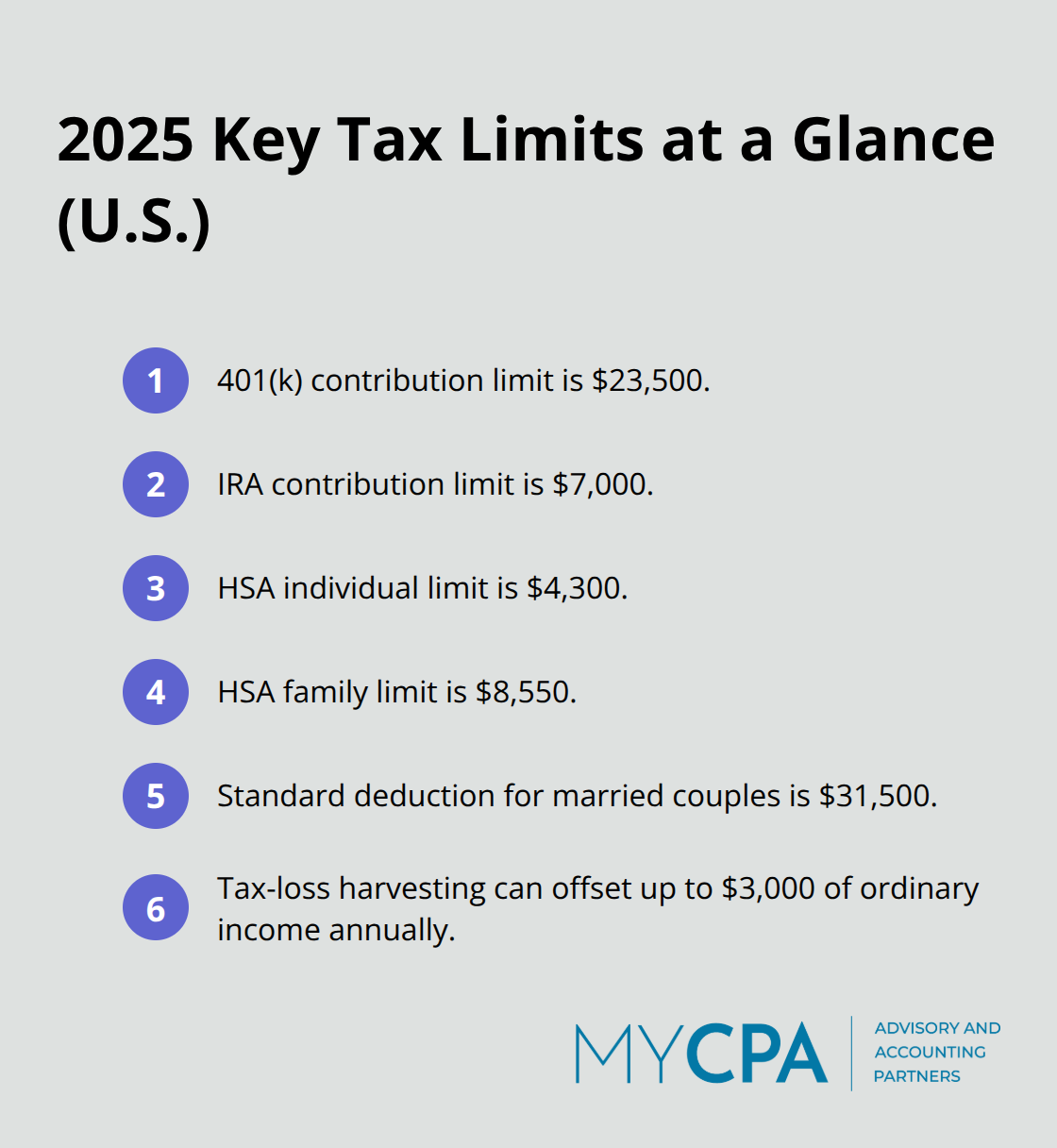

The potential sunset of the Tax Cuts and Jobs Act in 2025 makes these decisions particularly important. Charitable donation coordination (contributing two years’ worth in one year) helps exceed the high standard deduction threshold of $31,500 for married couples in 2025.

Retirement account contributions reduce current taxable income while building future wealth. The 2025 contribution limit for 401(k) plans reaches $23,500, with catch-up contributions available for those aged 50 and older. Health Savings Accounts offer triple tax benefits – deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Asset location strategies place tax-inefficient investments in tax-deferred accounts and tax-efficient investments in taxable accounts. This approach optimizes the overall tax burden across all investment accounts. These foundational strategies set the stage for more sophisticated business and individual tax planning strategies.

Self-employed individuals and business owners control when they receive income more than W-2 employees realize. December invoices deferred until January push income into the next tax year, potentially saving thousands when tax rates increase. The Tax Cuts and Jobs Act sunset provisions in 2025 make this timing particularly valuable.

Income acceleration into 2024 makes sense when you expect higher rates next year. Equity compensation holders can time stock option exercises and restricted stock vesting to optimize their tax brackets. The key lies in projecting total annual income across multiple years rather than focusing on single-year optimization.

Charitable donations bunched into alternate years help exceed the $31,500 standard deduction for married couples in 2025. Appreciated stock donated to charity allows deduction of fair market value without realized capital gains, effectively doubling the tax benefit.

Business owners should conduct cost segregation studies to recover the cost of business or income-producing property through deductions for depreciation. The 2025 contribution limits reach $23,500 for 401k plans and $7,000 for IRAs, with additional catch-up contributions for those over 50. Health Savings Accounts provide triple tax benefits with $4,300 individual and $8,550 family contribution limits.

Tax-loss harvesting in taxable investment accounts can offset up to $3,000 of ordinary income annually, with unused losses carried forward indefinitely.

Pass-through entities benefit from the section 199A qualified business income deduction, allowing eligible taxpayers to deduct up to 20 percent of their qualified business income, plus 20 percent of qualified real estate investment trust (REIT) dividends. Income limits and business type restrictions apply.

Full expensing of domestic research and development costs now reduces taxable income significantly for innovation-focused companies. The section 163j limitation threshold increase allows businesses to deduct higher interest expenses (benefiting leveraged operations). Asset location strategies place tax-inefficient investments in tax-deferred accounts while keeping tax-efficient investments in taxable accounts.

Investment portfolios require regular rebalancing for tax efficiency, identifying opportunities for strategic gains and losses coordination. High-net-worth individuals should explore valuation discounts when gifting business interests or real estate to family members, maximizing the annual $19,000 gift tax exclusion per recipient.

These strategies work best when implemented consistently throughout the year, but many taxpayers sabotage their efforts through common mistakes that cost thousands in unnecessary taxes.

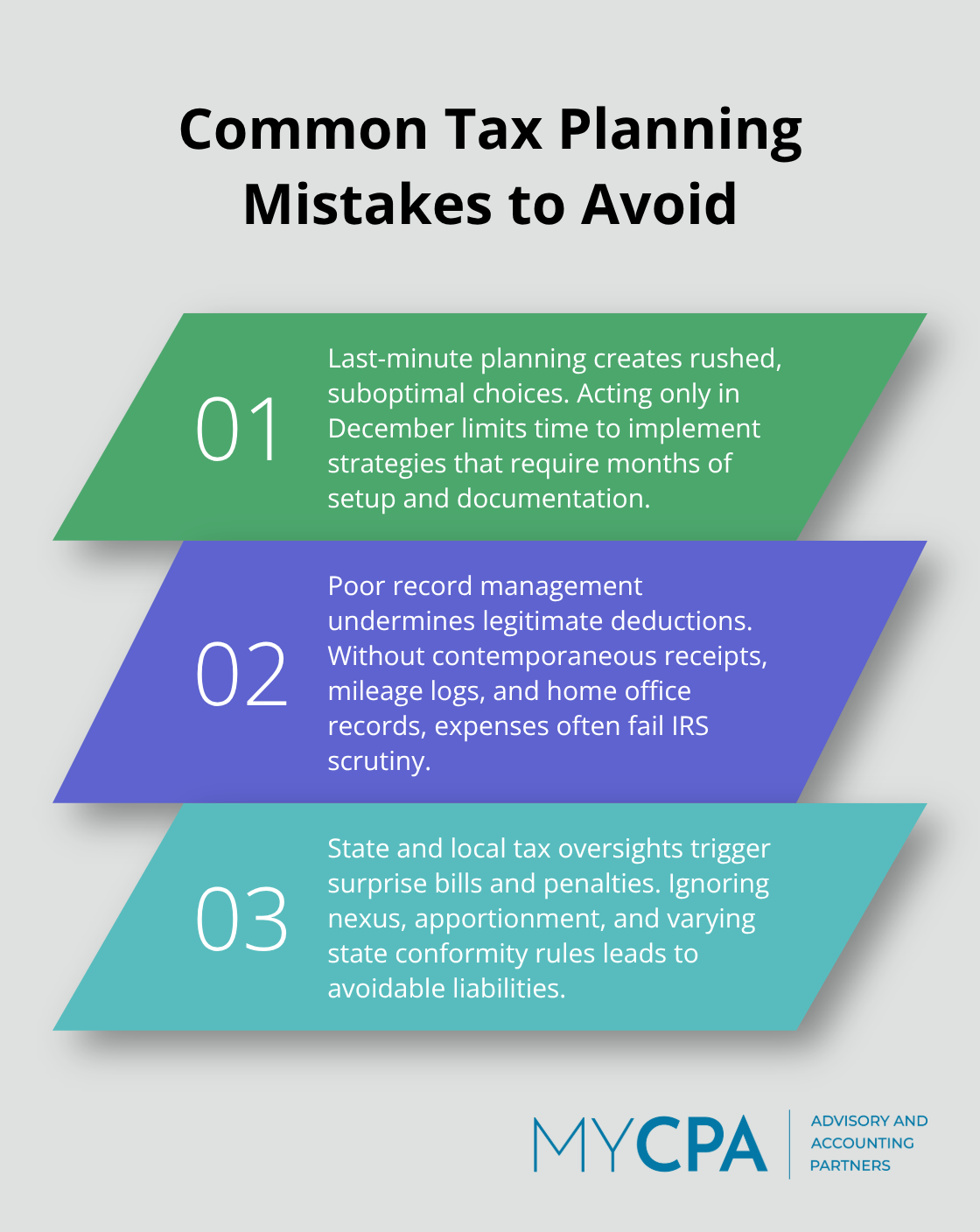

December panic drives most taxpayers into expensive mistakes that professional planning prevents throughout the year. Late preparation limits your options to surface-level adjustments when sophisticated strategies require months of preparation and documentation. The IRS processes over 161 million individual returns annually, and late filers consistently miss deductions worth thousands because rushed preparation overlooks eligible credits and strategic opportunities.

Year-end scrambles force taxpayers into suboptimal decisions that cost real money. Retirement account contributions made in December lack the compound growth potential of January contributions. Charitable donations bunched hastily in December miss the strategic coordination that maximizes deductions across multiple tax years.

Business owners who wait until December to purchase equipment miss depreciation benefits and face limited inventory availability. Year-round planning provides significant advantages over last-minute December preparation, allowing taxpayers to implement comprehensive strategies that maximize their tax savings potential.

Missing documentation costs taxpayers billions in legitimate deductions annually. Business meal receipts, mileage logs, and home office records require contemporaneous documentation that reconstruction cannot replace during IRS audits. The IRS disallows 78% of business deductions that lack proper documentation, even when the expenses were legitimate business costs.

State tax obligations compound these problems because multistate businesses often fail to track nexus requirements and apportionment factors throughout the year. This oversight leads to unexpected tax bills and penalties that average $12,000 per state (according to Council on State Taxation research).

Multistate operations face complex compliance requirements that catch unprepared businesses off guard. State conformity to federal tax reforms varies significantly, creating unexpected liabilities when businesses assume uniform treatment across jurisdictions. The reinstatement of 100% bonus depreciation creates opportunities in some states while others maintain different depreciation schedules.

Pass-Through Entity Tax elections can reduce state and local tax exposure, but these elections require advance planning and cannot be implemented retroactively. Payroll tax implications multiply when businesses expand geographically without proper preparation for varying state requirements.

Proactive tax planning strategies deliver measurable results that reactive preparation cannot match. Businesses and individuals who implement year-round planning reduce their tax burden by 15-30% compared to those who wait until December. The average taxpayer leaves $3,207 on the table annually through missed deductions and poor timing decisions.

Professional guidance becomes essential as tax laws grow increasingly complex. The potential sunset of Tax Cuts and Jobs Act provisions in 2025 creates planning opportunities that require expert navigation (state conformity variations and multistate compliance issues demand specialized knowledge that most taxpayers lack). We at My CPA Advisory and Accounting Partners help clients implement comprehensive tax planning strategies through personalized financial plans and proactive advice.

Start your tax planning journey now rather than wait for year-end pressure. Document expenses throughout the year, maximize retirement contributions early, and coordinate income timing with professional guidance. Strategic planning today prevents costly mistakes tomorrow.

Privacy Policy | Terms & Conditions | Powered by Cajabra