Growth Funding Options: Financing Paths for Startups

Explore growth funding options for startups, from bootstrapping to venture capital. Find the right financing path for your business expansion.

Tax minimization strategies are a hot topic for individuals and businesses alike. At My CPA Advisory and Accounting Partners, we often field questions about how to legally reduce tax burdens.

This post will explore effective methods to minimize your tax liability while staying within the bounds of the law. We’ll cover key strategies and highlight the importance of professional guidance in navigating the complex world of tax planning.

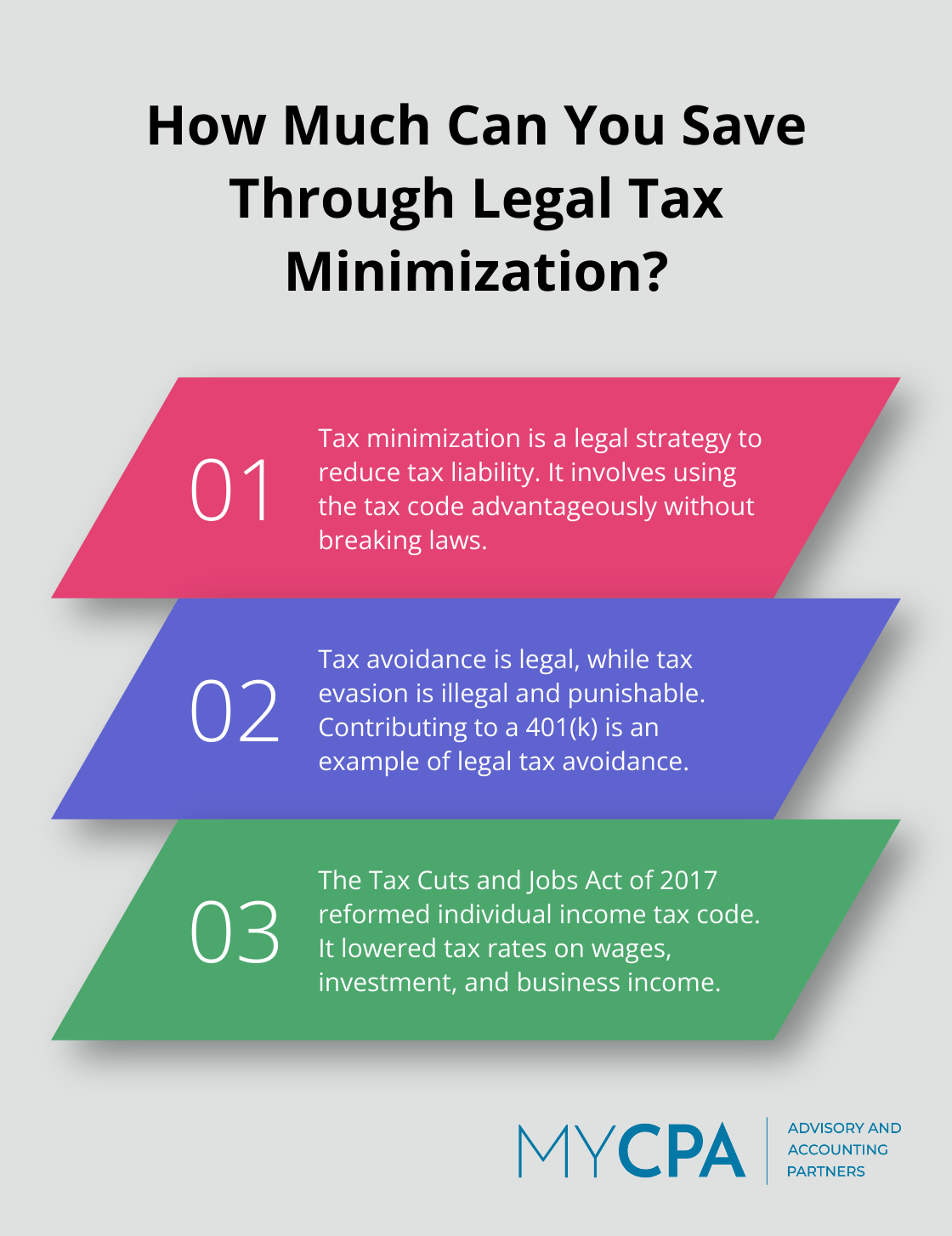

Tax minimization is a legal strategy to reduce your tax liability. It involves using the tax code to your advantage without breaking it. The goal is to pay the least amount of tax required by law.

Tax avoidance is legal. It involves structuring your finances to minimize tax obligations within the law. Tax evasion, however, is illegal. It refers to the deliberate underpayment or non-payment of taxes. The IRS imposes severe penalties for evasion, including fines and potential jail time.

A common example of tax avoidance is contributing to a 401(k), which reduces your taxable income legally. Tax evasion might involve hiding income or overstating deductions. The key difference lies in intent and legality.

Ethical tax planning matters for several reasons:

Legal Compliance: It keeps you on the right side of the law.

Trust Building: For business owners, ethical practices build trust with customers and partners.

Peace of Mind: You’ll sleep better knowing you’re not at risk of an audit or legal trouble.

Know the Tax Code: Stay updated on changes. The Tax Cuts and Jobs Act of 2017 reformed the individual income tax code by lowering tax rates on wages, investment, and business income.

Maximize Deductions: Decide whether to itemize or take the standard deduction.

Use Tax-Advantaged Accounts: Contribute to IRAs, 401(k)s, and HSAs.

Time Income and Expenses: If you’re self-employed, consider deferring income to the next tax year or accelerating expenses into the current year.

Seek Professional Help: Tax laws are complex. A professional can help you navigate them effectively.

Tax minimization requires a strategic approach to managing your finances. While individual efforts can yield results, professional guidance often leads to more significant savings. Certified Public Accountants (CPAs) possess the expertise to navigate complex tax laws and identify opportunities you might overlook.

As we move forward, we’ll explore specific strategies to maximize your tax savings while maintaining full compliance with the law.

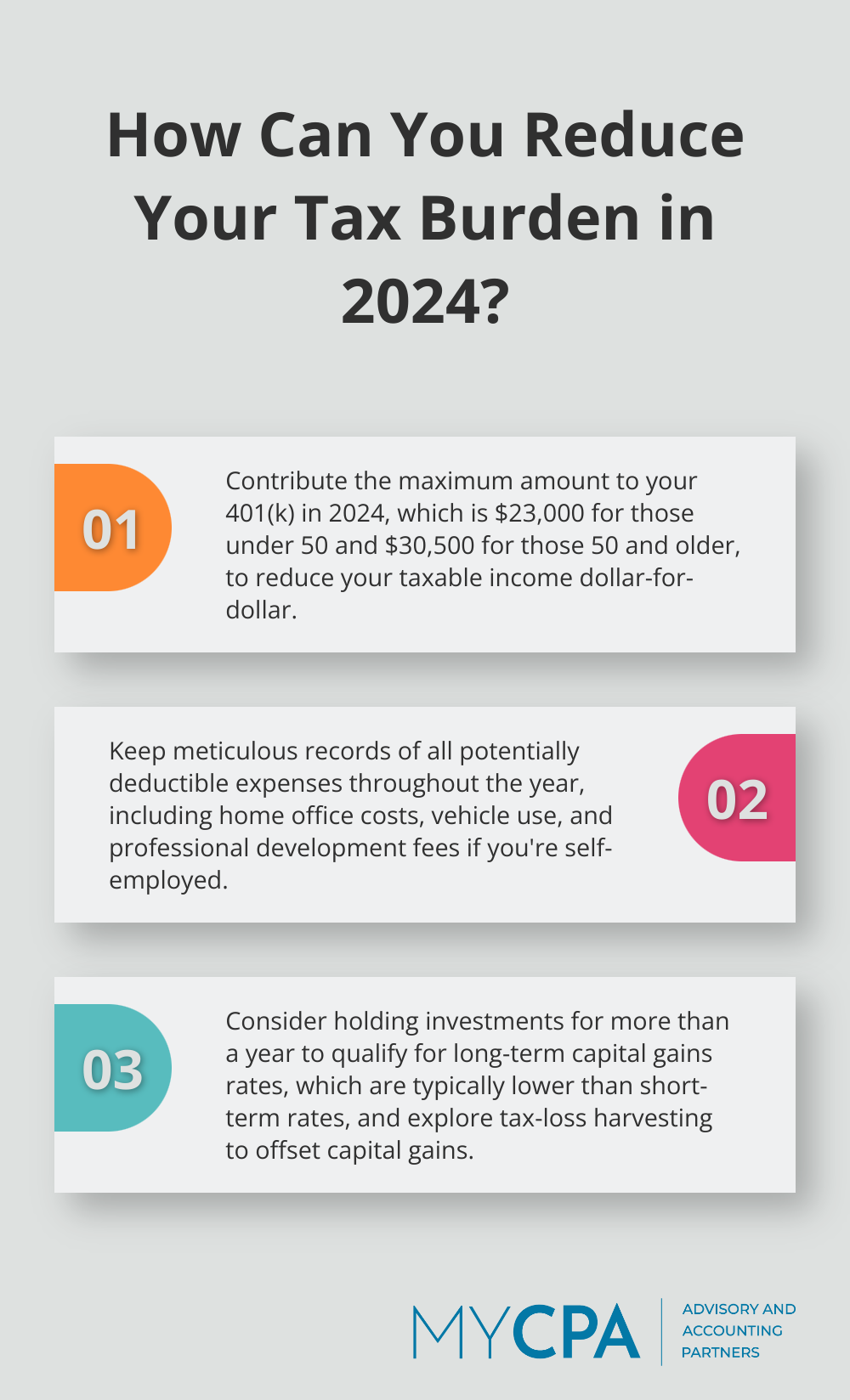

Tax minimization requires careful planning and execution. One of the most effective ways to reduce your tax burden involves taking full advantage of available deductions and credits. Keep meticulous records of all potentially deductible expenses throughout the year. Self-employed individuals should track all business-related expenses, including home office costs, vehicle use, and professional development fees.

The IRS provides information on returns filed, taxes collected, enforcement, taxpayer assistance, the IRS budget and workforce, and other selected activities. This comprehensive data can help taxpayers understand the broader context of tax collection and potentially identify areas for deductions and credits.

The timing of your income and expenses can significantly impact your tax liability. Self-employed individuals or those with control over income receipt should consider deferring some income to the following year if they expect to be in a lower tax bracket. Conversely, accelerating income into the current year might benefit those anticipating a higher bracket next year.

Midyear tax planning for small businesses and individuals in 2024 includes considerations for income timing and generous depreciation breaks. This strategy can be particularly effective for those near the threshold of a higher tax bracket.

Contributions to retirement accounts like 401(k)s and IRAs not only secure your financial future but also offer immediate tax benefits. In 2024, you can contribute up to $23,000 to a 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older. These contributions reduce your taxable income dollar-for-dollar.

For those without access to employer-sponsored plans, Traditional IRAs offer similar benefits. In 2024, you can contribute up to $7,000 (or $8,000 if you’re 50 or older). The tax benefits of Traditional IRA contributions may phase out at higher income levels, so understanding your specific situation is essential.

The structure of your business can significantly impact your tax liability. Different business entities (such as sole proprietorships, partnerships, S corporations, and C corporations) have varying tax implications. Choosing the right structure for your business can lead to substantial tax savings.

For instance, S corporations can provide tax advantages through the ability to split income between salary and distributions, potentially reducing self-employment taxes. However, the optimal structure depends on various factors specific to your business and personal financial situation.

Smart investment strategies can also contribute to tax minimization. Consider holding investments for more than a year to qualify for long-term capital gains rates, which are typically lower than short-term rates. Additionally, tax-loss harvesting (selling investments at a loss to offset capital gains) can help reduce your overall tax burden.

Municipal bonds offer another tax-efficient investment option, as the interest earned is often exempt from federal taxes and sometimes state and local taxes as well.

The complexity of these strategies underscores the value of professional guidance in developing a comprehensive tax minimization plan. A qualified tax professional can help you navigate these options and tailor a strategy to your unique financial situation.

CPAs maintain current knowledge of the latest tax laws and regulations. The tax code’s complexity and frequent changes make a CPA’s up-to-date expertise invaluable. This knowledge allows you to take advantage of new deductions or credits you might otherwise overlook.

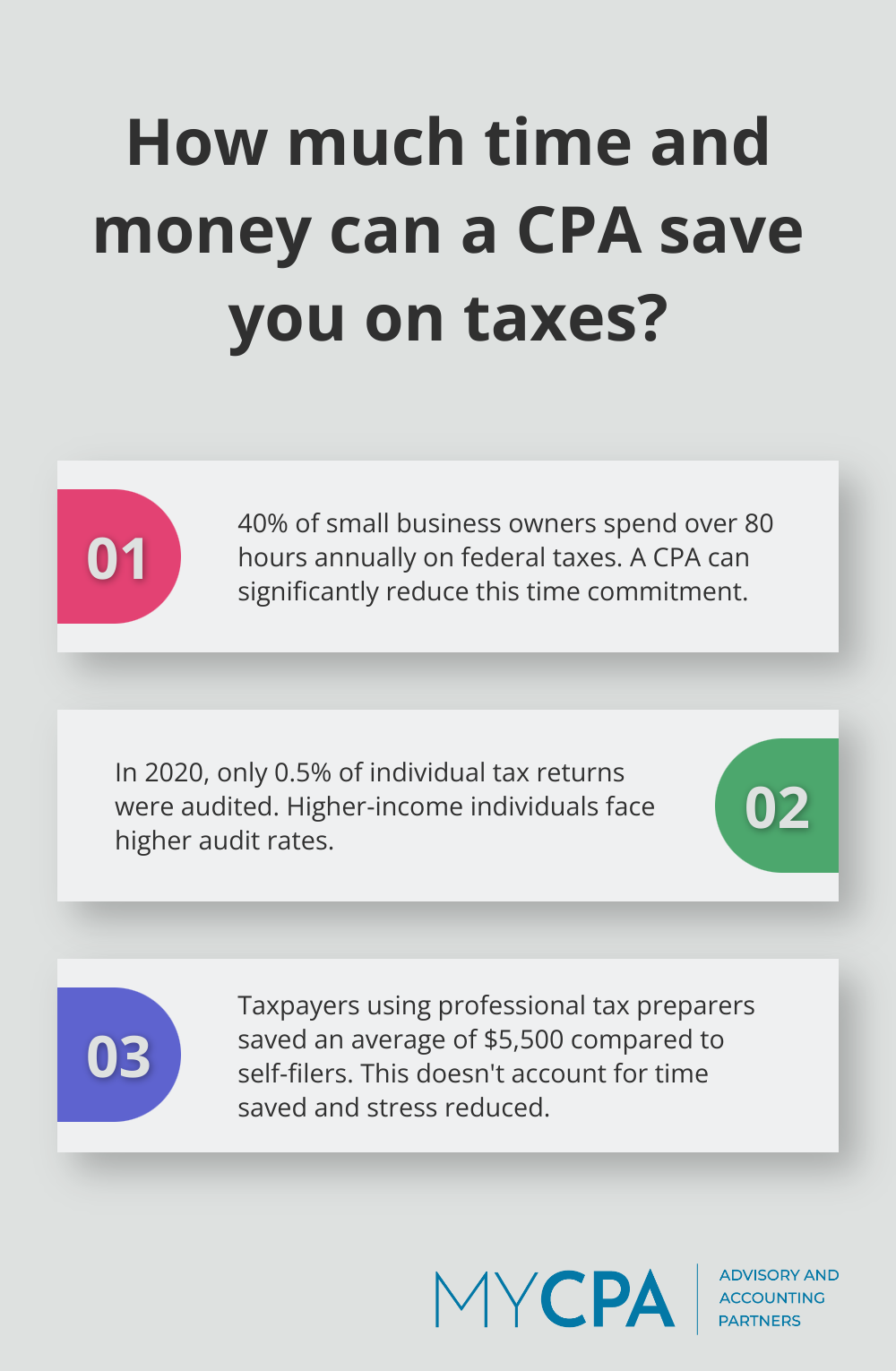

Every financial situation requires a unique approach. A CPA develops a personalized tax strategy tailored to your specific circumstances. For small business owners, a CPA might suggest strategies such as income and expense timing or selecting the most tax-efficient business structure. The National Federation of Independent Business reports that 40% of small business owners spend over 80 hours per year on federal taxes. A CPA can significantly reduce this time commitment.

Effective tax planning requires ongoing attention and adjustments. A CPA provides year-round support, helping you make informed financial decisions that impact your tax liability. They advise on the tax implications of major purchases, investments, or business decisions throughout the year.

In the event of an IRS audit, a CPA becomes an invaluable asset. CPAs represent you before the IRS, handling communications and negotiations on your behalf. Overall, just 0.5% of individual tax returns were audited in 2020, with higher-income individuals being audited at higher rates.

While hiring a CPA incurs a cost, the potential tax savings often outweigh this expense. A study by the National Society of Accountants found that taxpayers who used a professional tax preparer saved an average of $5,500 compared to those who filed on their own. This figure doesn’t account for the time saved and stress reduced by having a professional handle your taxes. Business advisory & consulting services can empower you to make the best choices for minimizing tax liability and maximizing wealth.

Tax minimization strategies form a critical part of financial planning for individuals and businesses. These methods can lead to substantial savings when applied correctly, from maximizing deductions to optimizing retirement contributions. Professional guidance proves invaluable in navigating the complex and ever-changing landscape of tax laws.

Proactive tax planning offers benefits beyond reducing your annual tax bill. It helps build wealth more efficiently, secures a more comfortable retirement, and provides peace of mind. A strategic approach to tax minimization sets the foundation for a more financially secure future.

My CPA Advisory and Accounting Partners specializes in implementing effective tax minimization strategies. Our team of experts can provide tailored solutions to optimize your tax position while ensuring full compliance with tax regulations. Take control of your financial future with proactive tax planning today.

Privacy Policy | Terms & Conditions | Powered by Cajabra