Tax Compliance Audits: Preparing with Confidence

Prepare for tax compliance audits with confidence using our expert strategies, common audit triggers, and practical steps to protect your business.

A simple accounting services agreement protects both you and your clients by setting clear expectations from day one. Without one, misunderstandings about fees, deliverables, and responsibilities can damage client relationships and expose your firm to legal risk.

We at My CPA Advisory and Accounting Partners have seen too many accounting firms operate without proper agreements, only to face disputes later. This guide walks you through the essential components, common mistakes to avoid, and best practices for creating an agreement that works for your business.

Your accounting services agreement needs four foundational elements that directly prevent disputes and protect your firm’s revenue. The scope of services section must list exactly what you will and will not do. Specify whether you handle accounts payable, accounts receivable, bank reconciliations, payroll processing, tax preparation, or financial statement preparation. The more specific you are here, the less room clients have to request work outside your agreed deliverables.

Many accounting firms lose money because scope creep-clients ask for extra tasks that weren’t quoted, and the firm absorbs the cost. Your agreement should state that additional services beyond this list require a separate change order with new pricing. This single clause protects your profitability and forces honest conversations about what clients actually need.

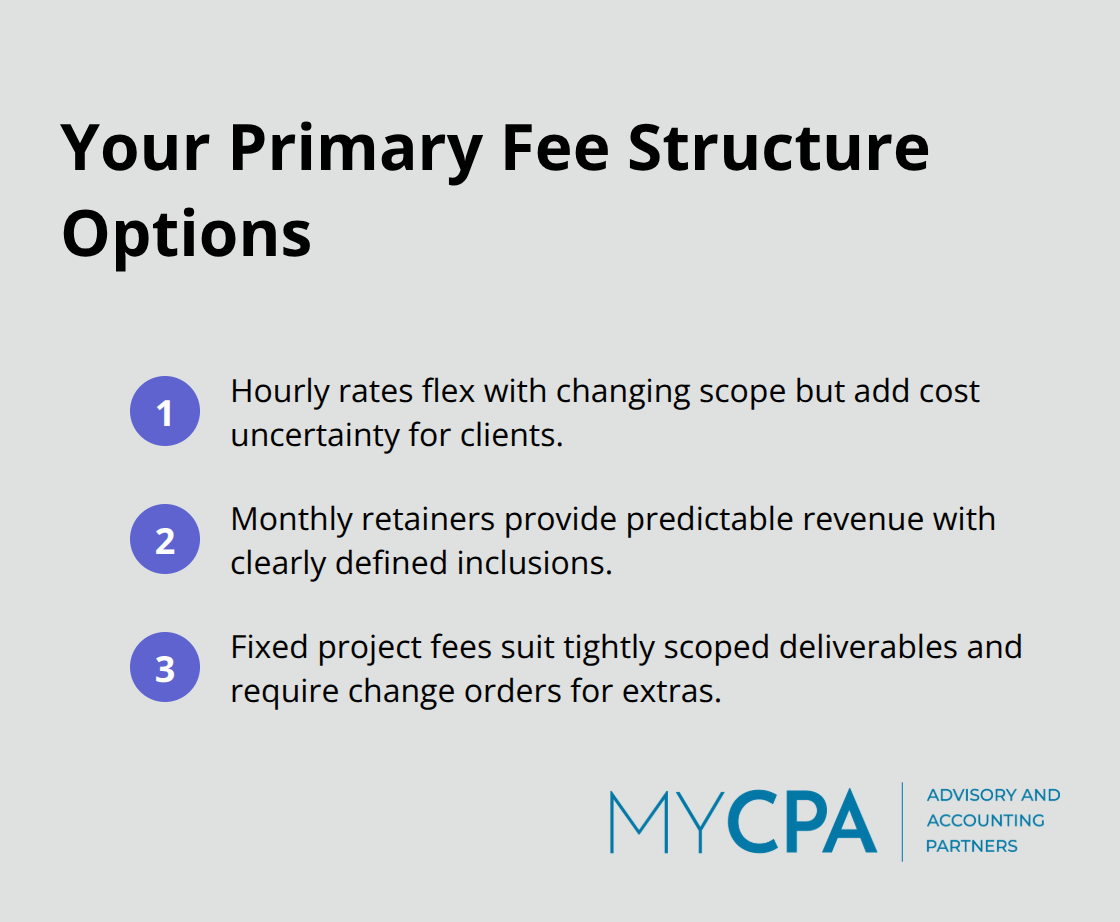

Fee structure demands absolute clarity on how much clients pay and when. You have three primary options: hourly rates, monthly retainers, or fixed project fees. Hourly rates work best for variable engagements where scope fluctuates, but they create uncertainty for clients who prefer predictable costs. Monthly retainers suit ongoing bookkeeping relationships and give your firm stable revenue.

Fixed project fees work for tax returns or year-end closes, though you must define scope tightly to avoid working unpaid hours.

Your agreement should specify payment terms (net 30 is standard), accepted payment methods, and late fees. Include a clause stating what happens if a client doesn’t pay-does work stop immediately, or do you allow a grace period? This clarity prevents revenue leaks and sets firm boundaries around payment expectations.

Confidentiality and data protection standards protect sensitive financial information and demonstrate compliance with professional standards. Your agreement should detail how you store client data, who has access, how you handle data breaches, and what happens if a client terminates the relationship. This section builds trust and sets expectations around security practices your firm actually uses.

Address data ownership explicitly-specify that you maintain backup copies at separate locations and that clients retain ownership of their records. These provisions show clients you take their information seriously and operate with professional standards.

Term and termination conditions define how long the relationship lasts and how either party can end it. Most ongoing bookkeeping relationships run month-to-month or year-to-year with 30 days’ notice to terminate. Your agreement should address what happens when a client leaves-do you provide data within a specific timeframe, and who pays transfer costs? This section also clarifies immediate termination rights if a client breaches the agreement (such as nonpayment) versus standard notice periods.

Include a final invoice clause requiring clients to pay all outstanding amounts within 15 days of termination. These provisions protect your cash flow and establish clear exit procedures that prevent disputes during transitions.

With these four elements in place, you eliminate ambiguity and reduce the likelihood of disputes that drain management time. The next step involves identifying common mistakes that accounting firms make when drafting these agreements-mistakes that can undermine even well-intentioned language.

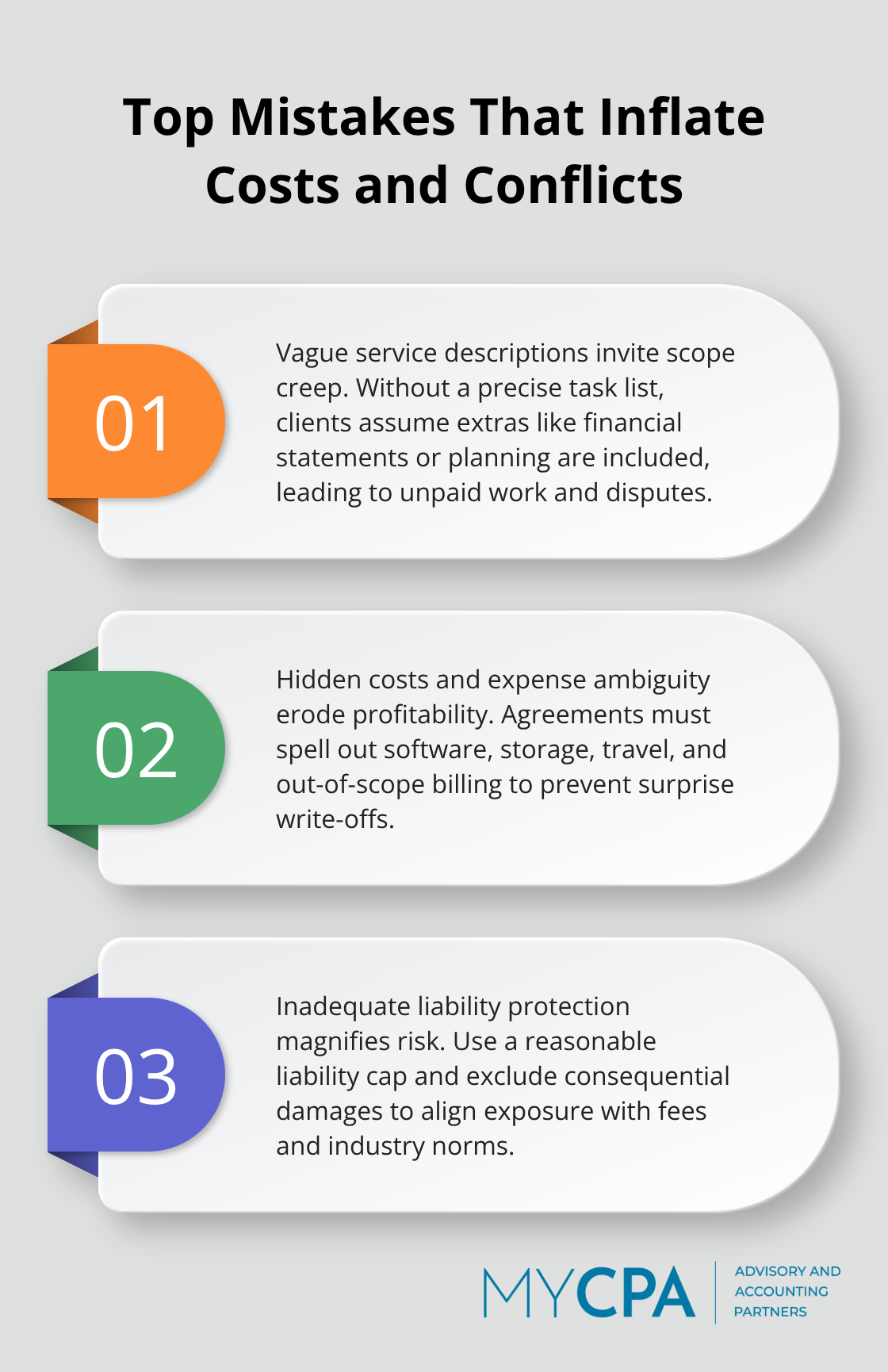

Vague service descriptions sit at the top of the list for agreements that fail. When you write something like “we handle bookkeeping and tax services” without specifying what bookkeeping actually means, clients interpret this differently than you do. One client thinks bookkeeping includes monthly financial statements and tax planning conversations. Another thinks it means data entry only. Six months later, you’re providing unpaid services or arguing about what was promised.

The fix is brutally simple: list the exact tasks you perform. Write “accounts payable processing, accounts receivable management, monthly bank reconciliations, payroll entry, and financial statement preparation” if those are your services. Then write what you do not do. You do not provide tax strategy, audit support, or CFO consulting unless separately contracted. This specificity costs you thirty minutes to write but saves you dozens of hours in client disputes.

Fee arrangements create the second major problem, and this one directly hits your profitability. Hidden costs emerge when agreements don’t specify what expenses clients pay. Does your fee include accounting software subscriptions, or does the client pay separately? Who covers document storage services or cloud backup? Does the client reimburse travel time for site visits? Many accounting firms absorb these costs because the agreement never addressed them, turning a profitable engagement into a money loser.

Your agreement must state clearly whether fees are all-inclusive or whether specific expenses get reimbursed. If you charge monthly retainers, specify exactly what happens when a client requests work outside the standard scope. Do you bill hourly for extra tasks, or do you absorb it? Write this down. Undocumented assumptions about extra work are how firms leave thousands on the table each year.

Inadequate liability protection creates exposure that keeps business owners awake at night. Your agreement should include a liability cap tied to either the fees paid over a defined period or your professional liability insurance limits, whichever is lower. Without this cap, a client can sue you for damages far exceeding what you earned from the engagement.

Also exclude certain damages from recovery, such as business interruption losses or consequential damages, since you cannot control or predict these outcomes. This protection is standard in professional service agreements and demonstrates that you operate with industry norms.

Missing dispute resolution procedures force expensive litigation when disagreements arise. Include a binding arbitration clause that requires both parties to pursue arbitration before filing lawsuits. Arbitration typically costs far less than court proceedings and resolves disputes in weeks rather than months or years.

This single clause transforms how you handle conflicts with clients. Instead of escalating to lawyers and courtrooms, you settle matters through a neutral third party who understands accounting and business disputes. The cost difference is substantial-arbitration often runs one-tenth the expense of litigation-and the timeline matters equally. You move forward with your business instead of managing legal proceedings that consume management attention and drain resources.

These four mistakes appear repeatedly in agreements that fail to protect accounting firms. The next section shows you how to customize your agreement so it actually reflects your business model and protects your interests.

Your agreement must reflect what clients actually need, not what you think they should want. Many accounting firms write one-size-fits-all agreements and wonder why clients push back or negotiate heavily. The real issue is that a bookkeeping client needs different protections and reporting schedules than a tax preparation client. A manufacturing company with complex inventory tracking needs different services than a service-based business.

Start by asking clients what problems they face with their current accounting setup and what outcomes matter most to them. Does the restaurant owner care about daily cash flow reporting? Does the nonprofit need monthly compliance documentation? This conversation happens before you write the agreement, not after. Once you understand client priorities, your agreement becomes a document they recognize as solving their specific problems rather than imposing generic requirements. This approach dramatically reduces negotiation cycles and gets signatures faster.

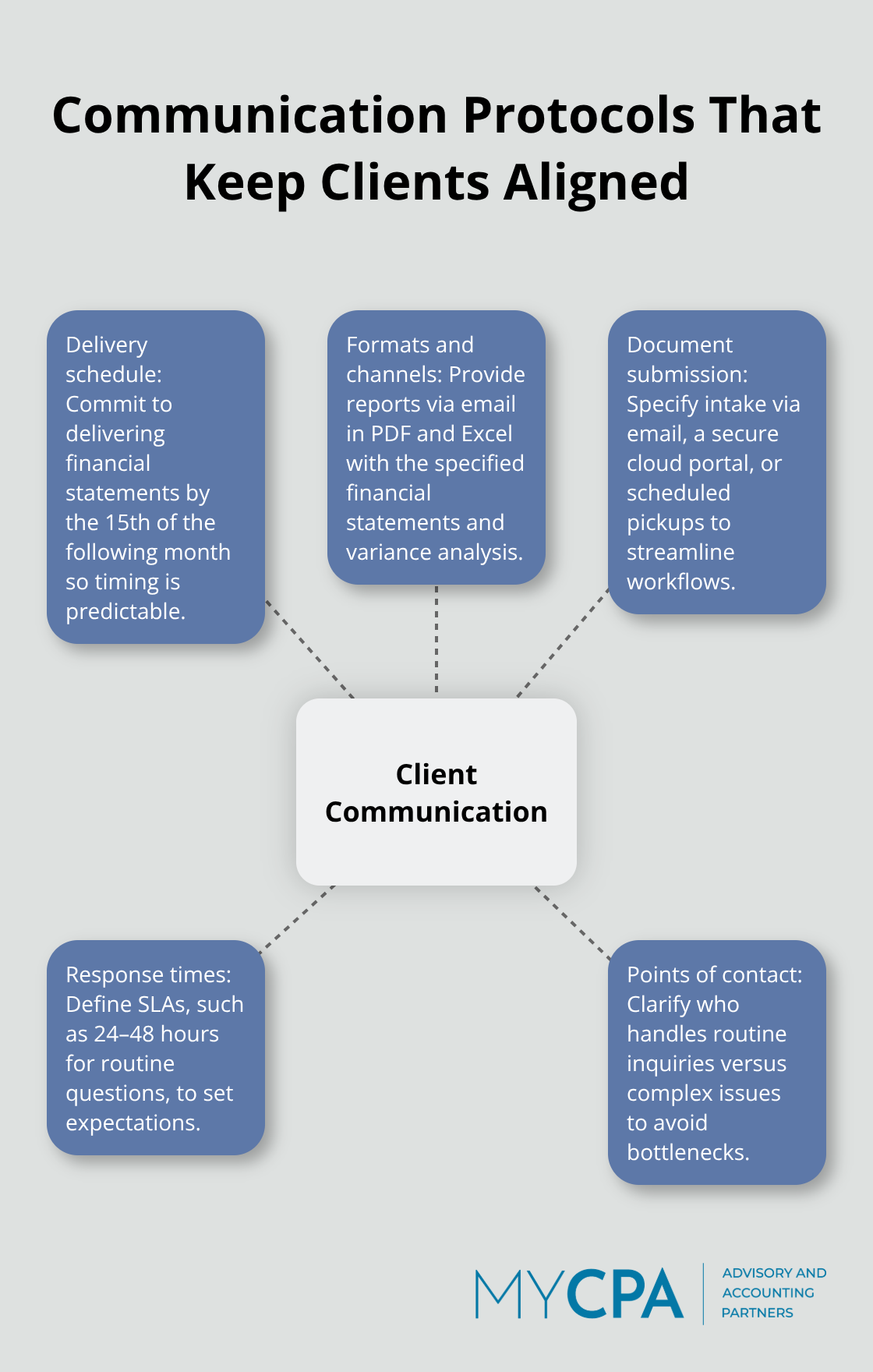

Communication protocols and reporting schedules must be specific enough that clients know exactly what to expect. Instead of writing “we provide monthly financial statements,” write “we deliver financial statements by the 15th of the following month, via email, in PDF and Excel formats, showing income statement and balance sheet with a variance analysis from the prior month.” Specify how clients submit documents to you, whether through email, a cloud portal, or scheduled pickups.

State your response time for client questions: do you answer within 24 hours or 48 hours? Define who at your firm clients contact for routine questions versus complex issues. Many firms lose clients because communication expectations were never set, leading to frustrated clients who feel ignored. This clarity prevents misalignment and keeps relationships strong throughout the engagement.

Define roles and responsibilities with brutal honesty about what clients must do. Your agreement should require clients to provide accurate and timely documentation, grant you access to their accounting software, notify you of significant transactions, and respond to your questions within three business days. When clients understand these obligations upfront, they either commit to meeting them or find another firm.

This self-selection prevents engagements with clients who cannot or will not provide necessary information. Clients who meet these standards tend to be satisfied with your work because they understand their role in the process. Those who cannot commit to these requirements would likely become problem clients anyway, so filtering them out early protects your firm’s profitability and sanity.

Include a straightforward change order process in your agreement. As client businesses grow, their accounting needs change. Your agreement should state that either party can request service modifications with 30 days’ notice, and pricing adjusts accordingly. This clause prevents resentment when clients ask for new services and keeps your engagement profitable as their needs evolve.

A change order process also protects you from scope creep (the silent killer of accounting firm profitability). Instead of absorbing new requests, you document them, price them, and get client approval before proceeding. Clients respect this approach because it shows you take their needs seriously while protecting your business model. The process itself becomes a conversation starter about whether new services align with their budget and priorities.

A simple accounting services agreement forms the foundation that separates profitable client relationships from ones that drain your time and money. The four core elements-scope of services, fee structure, confidentiality standards, and termination conditions-protect your firm’s revenue and reputation directly. Without them, you operate in ambiguity where clients interpret promises differently than you intended, and disputes consume management attention that should fuel business growth.

The mistakes we outlined appear across the accounting industry and cost firms thousands annually. Vague descriptions, hidden expenses, weak liability protection, and missing dispute resolution procedures transform straightforward engagements into complicated conflicts. You avoid these pitfalls through specificity, stating what you will and will not do, and establishing clear boundaries around payment and communication.

Your agreement requires updates as your business evolves, your service offerings change, and market conditions shift. Review it annually and adjust terms based on what you learn from client engagements (if you consistently add services beyond your scope, your agreement needs revision). We at My CPA Advisory and Accounting Partners help accounting firms build sustainable practices through comprehensive support in tax services, accounting, and business advisory-contact us today to strengthen your client relationships while protecting your firm’s profitability.

Privacy Policy | Terms & Conditions | Powered by Cajabra