Financial Reporting Accuracy: How Precise Data Powers Confident Decisions

Improve financial reporting accuracy with precise data practices for confident decisions and stronger compliance.

Startups fail not because of bad ideas, but because they run out of money. We at My CPA Advisory and Accounting Partners have seen countless founders make preventable mistakes with their funding strategies for startups.

This guide walks you through the real decisions you need to make: where to get capital, how much you actually need, and how to spend it wisely.

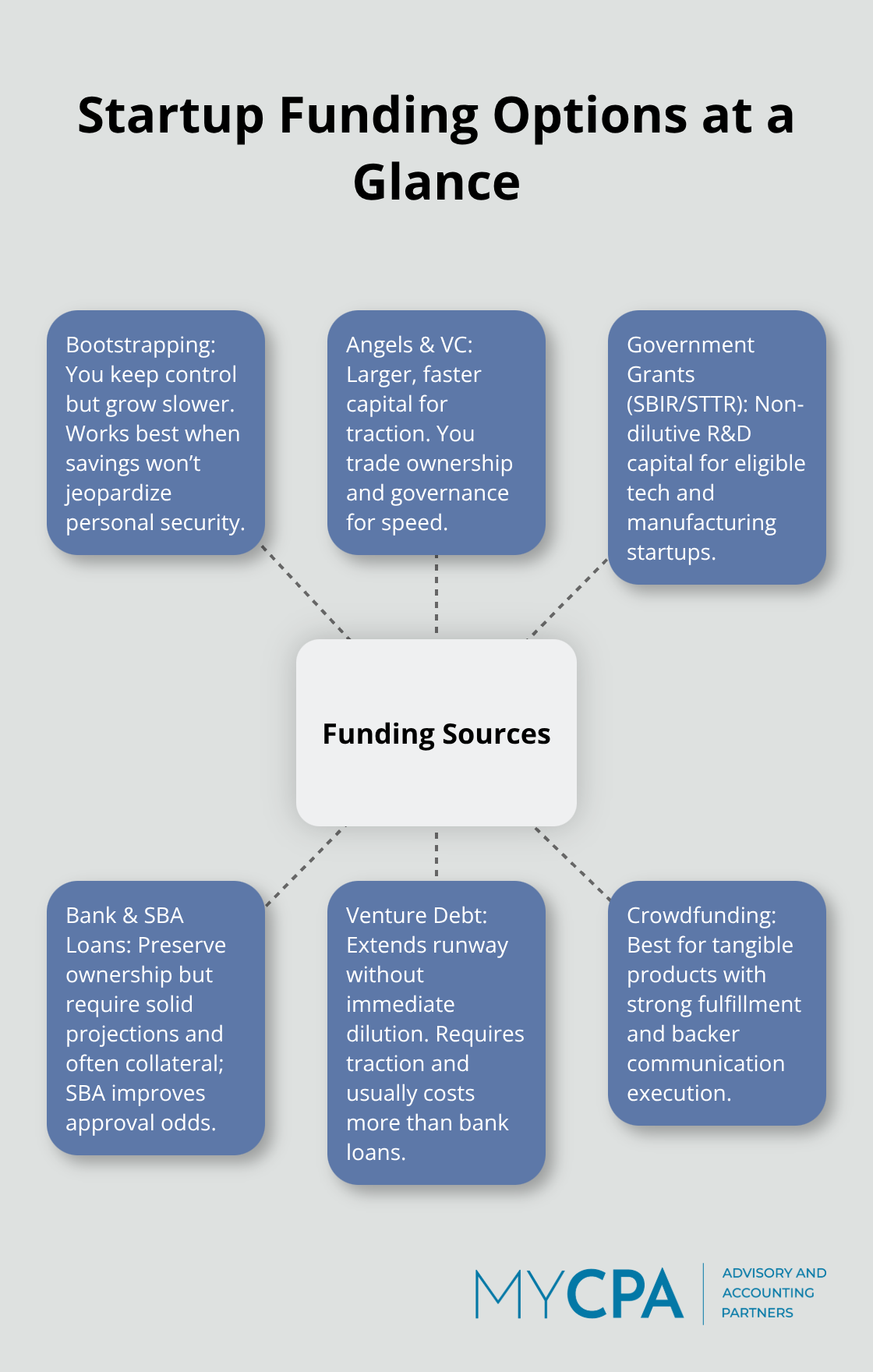

Startups access far more capital sources than most founders realize, but not all fit your situation. The funding landscape splits into two camps: equity-based options where you trade ownership, and debt or non-dilutive options where you keep control. Bootstrapping keeps you independent but limits growth speed. Self-funding works best when you have personal savings to allocate without jeopardizing your financial security, and founders often underestimate how long their runway lasts. Angel investors and venture capital provide substantial checks, but angel funding typically ranges from $25,000 to $500,000 per investor for early-stage companies, while Series A rounds averaged $7.9 million in Q1 2025 according to Carta data. Government programs like SBIR and STTR offer non-dilutive capital specifically for tech and manufacturing startups conducting research and development. Traditional bank loans preserve ownership but require solid financial projections and often collateral. Crowdfunding works if you have a tangible product and can execute fulfillment at scale.

Most successful startups don’t pick one source; they layer multiple options together to balance control, speed, and capital availability.

The harsh reality is that cash flow problems remain one of the leading causes of startup failure. Calculate your monthly burn rate by totaling all expenses: salaries, rent, software subscriptions, payment processing fees, taxes, insurance, and shipping. A startup burning $10,000 monthly with $100,000 in the bank has a 10-month runway. Plan for 24 to 30 months between funding rounds because actual fundraising takes longer than founders expect. Your capital target should stretch far enough to reach fundable milestones that prove traction to the next investor. Early-stage startups try for a path to break-even by year two or three, with gross margins around 50% or higher. Track your numbers obsessively using tools like QuickBooks to understand what you actually spend versus what you forecast. Most founders overestimate revenue and underestimate expenses by 40% or more, so double your early cost estimates and build in a buffer.

Many startup founders avoid looking at their finances until money runs out, which eliminates any chance to adjust course. Running a business without an income statement, cash flow statement, and balance sheet is like driving blind. Mixing personal and business finances creates a nightmare for taxes and makes it impossible to see what your company actually costs. Taking venture capital when you should bootstrap, or bootstrapping when you should raise, are both common missteps that slow growth unnecessarily. Founders often chase funding before validating that customers actually want their product, burning capital on features nobody needs. Raising too much money too early creates pressure for growth that may not be sustainable, while raising too little forces constant firefighting instead of building. Some founders neglect to model dilution across funding rounds, only to discover later that their ownership drops from 100% at seed to 23% by Series B. The cap table becomes messy when SAFEs and convertible notes convert without proper tracking, making future rounds difficult. Spending aggressively on hiring and marketing before proving unit economics works is toxic; focus on customers who generate revenue first, then scale the team.

The best founders treat their financial model as a living document that updates monthly, not a one-time exercise. Your model should show realistic revenue projections, itemized expenses, and clear paths to profitability. When you update your model monthly, you spot cash flow problems weeks or months before they become crises. This discipline also prepares you for investor conversations-institutional investors expect founders to know their numbers cold. Your financial projections become the foundation for every capital decision you make next.

Bootstrapping remains the most common path for early-stage founders, and for good reason. When you self-fund, you maintain complete control over decisions, avoid dilution, and stay focused on building a product customers actually want rather than chasing growth metrics for investors. The downside is obvious: you move slower and risk your personal finances. If you have savings, the critical decision is how much you can deploy without jeopardizing your personal security. Most founders underestimate their runway because they forget to account for taxes, insurance, and the reality that development takes longer than planned.

If you bootstrap, treat your burn rate like a countdown timer and prioritize revenue generation immediately. You cannot afford to spend months perfecting a product nobody will pay for. The math is brutal: a founder with $50,000 in savings burning $5,000 monthly has ten months before the bank account hits zero.

Angel investors and venture capital offer speed but demand ownership in return. Angel investors typically write checks between $25,000 and $500,000 per round and often provide mentorship alongside capital, making them valuable for founders who need strategic guidance. Series A funding averaged $7.9 million in Q1 2025, a jump that signals institutional investors expect you to have proven traction with real customers and recurring revenue.

The tradeoff is stark: founders often retain ownership after a seed round, then drop further after Series A, and fall further by Series B. Understand this dilution curve before you sign anything. Venture capitalists take board seats, expect quarterly results, and push for exits within seven to ten years. If you want to build a sustainable business over decades, VC funding may not fit your vision. Angels, by contrast, often accept longer timelines and more flexible terms because they invest their own money rather than managing other people’s capital.

Government programs like SBIR and STTR provide non-dilutive capital for startups conducting research and development in tech, manufacturing, and life sciences. These grants are competitive but worth pursuing if your startup qualifies. Traditional bank loans preserve ownership entirely but require solid financial projections, often collateral, and a track record of revenue. SBA-backed loans reduce lender risk and improve approval odds for riskier ventures.

Venture debt is another option: you borrow money that converts to equity only if you fail to repay, giving you runway without immediate dilution. The catch is that venture debt requires existing traction and typically costs more than traditional loans.

Crowdfunding works only if you have a tangible product ready to ship and the marketing bandwidth to execute a campaign. Most crowdfunding campaigns fail because founders underestimate fulfillment complexity and overestimate their ability to manage backer communications. The winners are founders who treat the campaign like a business sprint, not a passive fundraising event.

Most successful startups layer three to four funding sources together. A founder might bootstrap for six months to build an MVP, raise angel capital to fund the first team, apply for SBIR grants for R&D, and then approach Series A investors with real revenue and customer traction. This approach reduces risk and preserves more ownership than chasing VC immediately. The specific mix depends on your industry, growth timeline, and how much control you want to retain-which brings us to the financial management discipline required to make any funding strategy work.

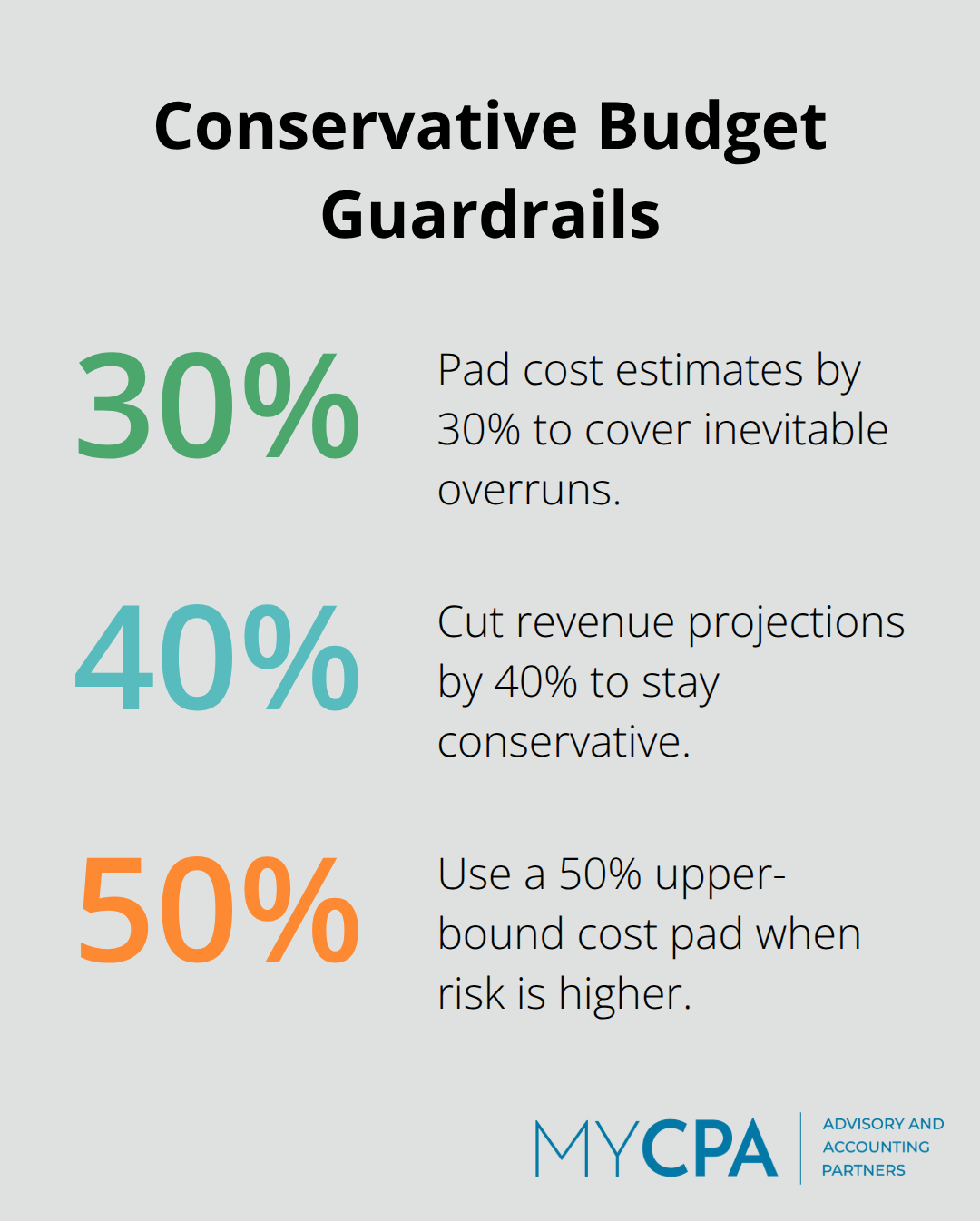

Your budget is not a guess about the future. It’s a weapon against cash flow collapse. Most founders fail because they budget like accountants who’ve never run a business: they forecast revenue conservatively but treat expenses as flexible variables that can shrink when money gets tight. This is backwards. Founders who document every line item for their pitch deck often ignore their own numbers once the money arrives. Your budget must reflect reality, which means padding costs by 30 to 50 percent above your initial estimates and cutting revenue projections by 40 percent. If you think you’ll spend $5,000 monthly on salaries, software, and infrastructure, budget for $7,000 to $7,500. If you forecast $20,000 in monthly revenue, plan operationally for $12,000. This conservative approach sounds pessimistic until month four when an unexpected server outage costs $3,000 and your payment processor raises fees by 0.5 percent, cutting into margins you didn’t know were that thin.

Your financial model must include every cost that actually exists: employee payroll taxes, accounting fees, insurance premiums, payment processing fees, bank charges, and the software subscriptions that accumulate silently. Most founders forget that QuickBooks, Slack, GitHub, and AWS each cost money, and stacked together they eat 5 to 10 percent of early revenue. Your budget should separate fixed costs (rent, salaries, subscriptions) from variable costs (shipping, payment processing, advertising) so you understand what you must pay regardless of sales and what scales with growth. Update this budget monthly without fail. When actual spending diverges from forecast by more than 10 percent, investigate why immediately rather than waiting for the next quarterly review.

Spend aggressively on customer acquisition only after you’ve proven unit economics work. This means running small tests first: if you spend $1,000 acquiring customers and they generate $3,000 in lifetime value, scale that channel. If you spend $1,000 and get $500 back, stop immediately and find a different approach. Too many founders reverse this logic: they raise capital, hire a VP of Sales, launch an expensive marketing campaign, and then discover nobody wants the product at the price they need to charge. The root cause of startup failure is almost always spending on growth before validating that growth is profitable.

Your first hires should be someone who can write code or build your core product, not a salesperson. Revenue-generating talent compounds; hiring overhead talent early just accelerates your burn without proving demand exists. Once you have paying customers, your next hire should address your biggest constraint. If you’re losing deals because you can’t deliver fast enough, hire for delivery. If customers are churning because the product lacks features, hire for product development. Hiring because you’re growing is a trap that turns temporary success into permanent cash drain. Your budget should reflect this priority ruthlessly: allocate 50 to 60 percent of early spending to product and operations, 20 to 30 percent to customer acquisition once validated, and the remainder to overhead. This forces difficult conversations about whether you actually need that office space, that additional contractor, or that management layer.

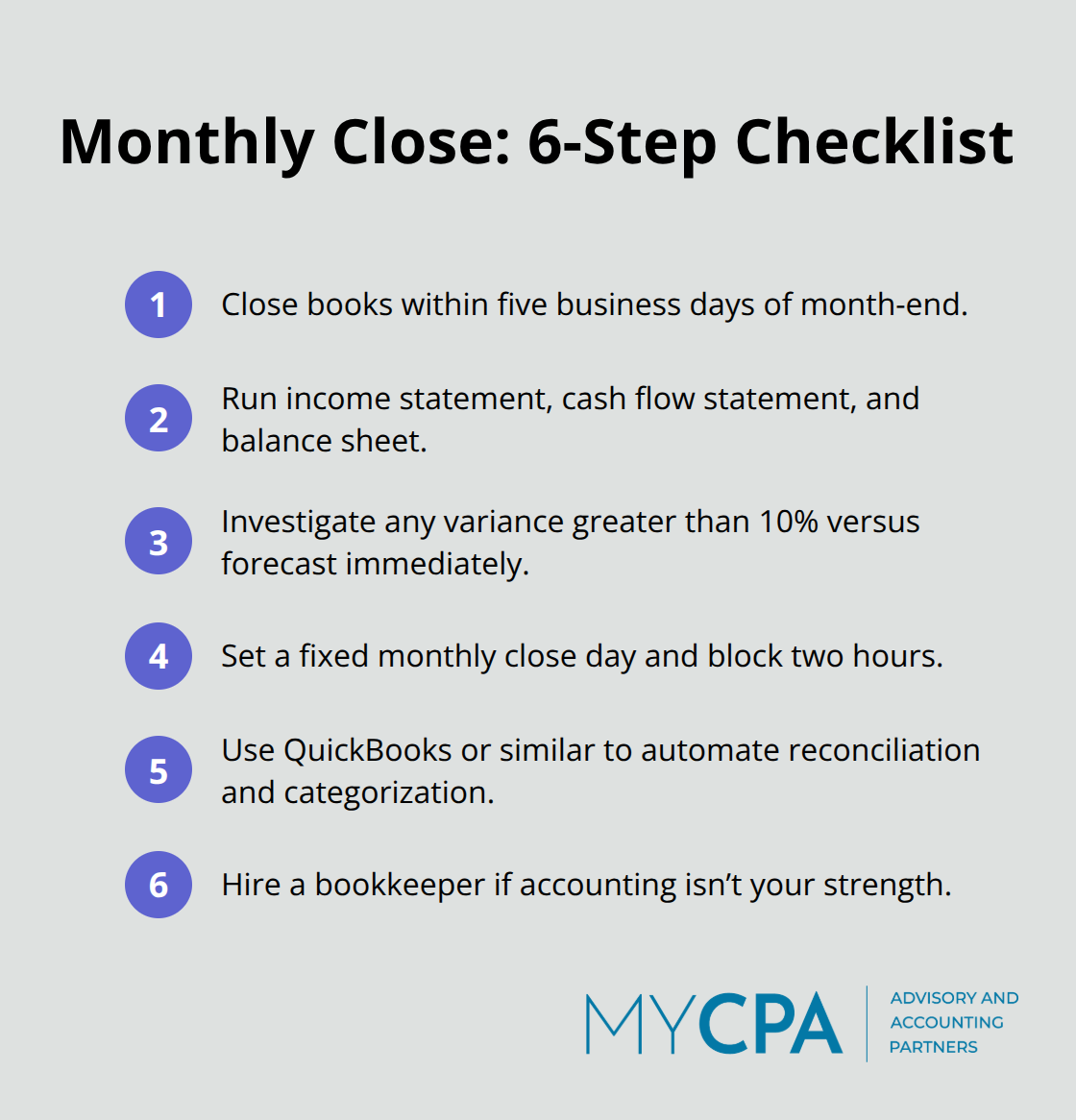

Close your books every month without exception. Run your income statement, cash flow statement, and balance sheet within five business days of month-end. Most founders treat accounting as a quarterly or annual exercise, which means they discover cash problems months after they started. Your cash flow statement is the one document that tells you how much money you actually have and when it runs out. If your income statement shows $50,000 in revenue but your cash flow statement shows you spent $55,000 in the same month, you have a problem that an income statement alone would hide.

This happens constantly when customers pay on net-30 or net-60 terms: you recognize revenue but don’t see the cash for weeks or months. A founder with strong revenue on the income statement can still run out of cash in week three of the month if payment timing doesn’t align with payroll. Your balance sheet tells you what you own and what you owe, which reveals liabilities that can sneak up on you. If you’ve accrued payroll taxes, sales taxes, or contractor invoices that haven’t been paid yet, they appear on the balance sheet but might not have registered in your head as immediate obligations.

Set a specific day each month (the 5th or the 10th) and spend two hours closing your books completely. Use QuickBooks or similar software to automate reconciliation and categorization so the work doesn’t consume your entire week. If accounting is not your strength, hire a bookkeeper or work with a firm that can handle monthly close for a flat fee rather than hourly rates. The cost is worth it because clean monthly financials give you the visibility to adjust spending before you hit a wall.

The difference between startups that survive and those that fail comes down to discipline with your funding strategies for startups. You now understand how to layer multiple capital sources, calculate your burn rate ruthlessly, and spend only on what generates revenue. The founders who win are not the ones with the biggest checks or the best pitch decks-they are the ones who treat their finances like a competitive advantage rather than an administrative burden.

Your funding strategy must match your stage and your vision. If you want to build a sustainable business over decades, bootstrapping or angel capital with non-dilutive grants keeps you in control. If you want to scale aggressively and exit within seven years, venture capital accelerates that path but demands ownership and governance tradeoffs. Close your books monthly without exception, update your financial model when reality diverges from forecast, and spend on customer acquisition only after you prove unit economics work.

Most founders underestimate how much accounting and financial management matter until they face a crisis. We at My CPA Advisory and Accounting Partners help business owners build the financial systems that prevent those crises through bookkeeping, tax strategy, QuickBooks setup, and business advisory. Contact us today to build the financial foundation that supports your funding strategy and keeps your startup alive.

Privacy Policy | Terms & Conditions | Powered by Cajabra