Growth Funding Options: Financing Paths for Startups

Explore growth funding options for startups, from bootstrapping to venture capital. Find the right financing path for your business expansion.

Tax planning is a powerful tool for managing your financial future. At My CPA Advisory and Accounting Partners, we’ve seen how effective tax strategies can significantly impact our clients’ bottom lines.

This guide will walk you through the essentials of tax planning, from basic concepts to advanced techniques. We’ll also explore how working with tax professionals can optimize your financial outcomes.

Tax planning is the analysis of a financial situation or plan to ensure that all elements work together to allow you to pay the lowest taxes possible. It involves understanding the tax code and using it to your advantage. Effective tax planning requires year-round attention, not just during tax season.

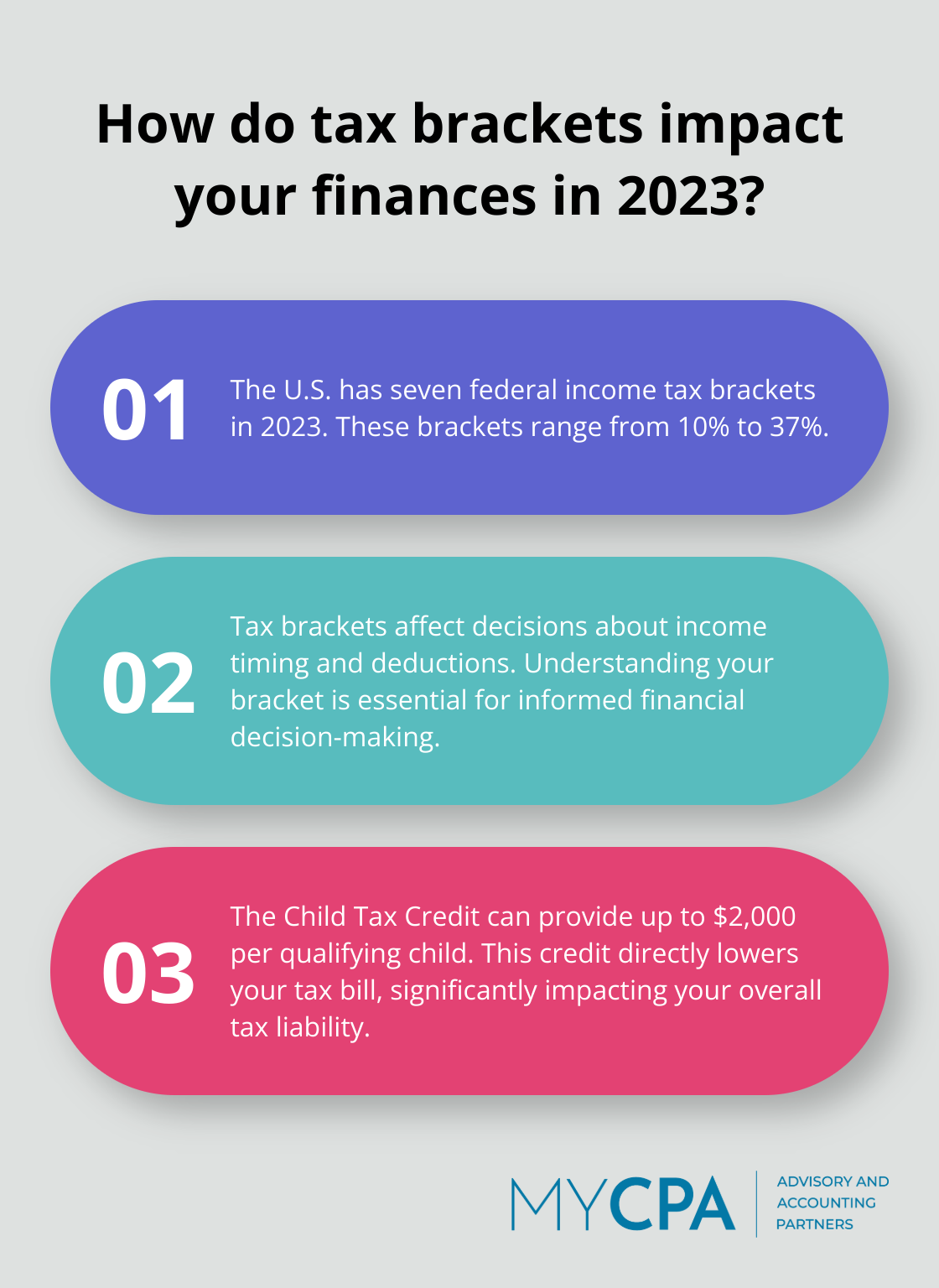

Understanding tax brackets is essential for informed decision-making. In 2023, the U.S. has seven federal income tax brackets (ranging from 10% to 37%). Your bracket affects decisions about income timing and deductions.

Tax deductions reduce your taxable income, while credits directly lower your tax bill. For example, the Child Tax Credit can provide up to $2,000 per qualifying child, significantly impacting your overall tax liability.

It’s critical to distinguish between tax avoidance and tax evasion:

At MyCPA Advisory and Accounting Partners, we strictly adhere to legal tax reduction strategies. We help our clients navigate complex tax laws to minimize their tax burden while staying compliant with IRS regulations.

Proper tax planning can lead to significant savings. For instance, contributing to a 401(k) can lower your taxable income. In 2024, you can contribute up to $76,500 if you include catch-up contributions, potentially saving thousands in taxes.

The tax landscape evolves constantly. What worked last year might not be the best approach this year. Staying informed about tax law changes and adjusting your strategy accordingly is crucial for effective tax planning.

As we move forward, let’s explore specific strategies that can help you plan your taxes more effectively and maximize your financial outcomes.

At My CPA Advisory and Accounting Partners, we recommend several effective tax planning strategies that can help optimize your financial outcomes. Let’s explore some of these approaches:

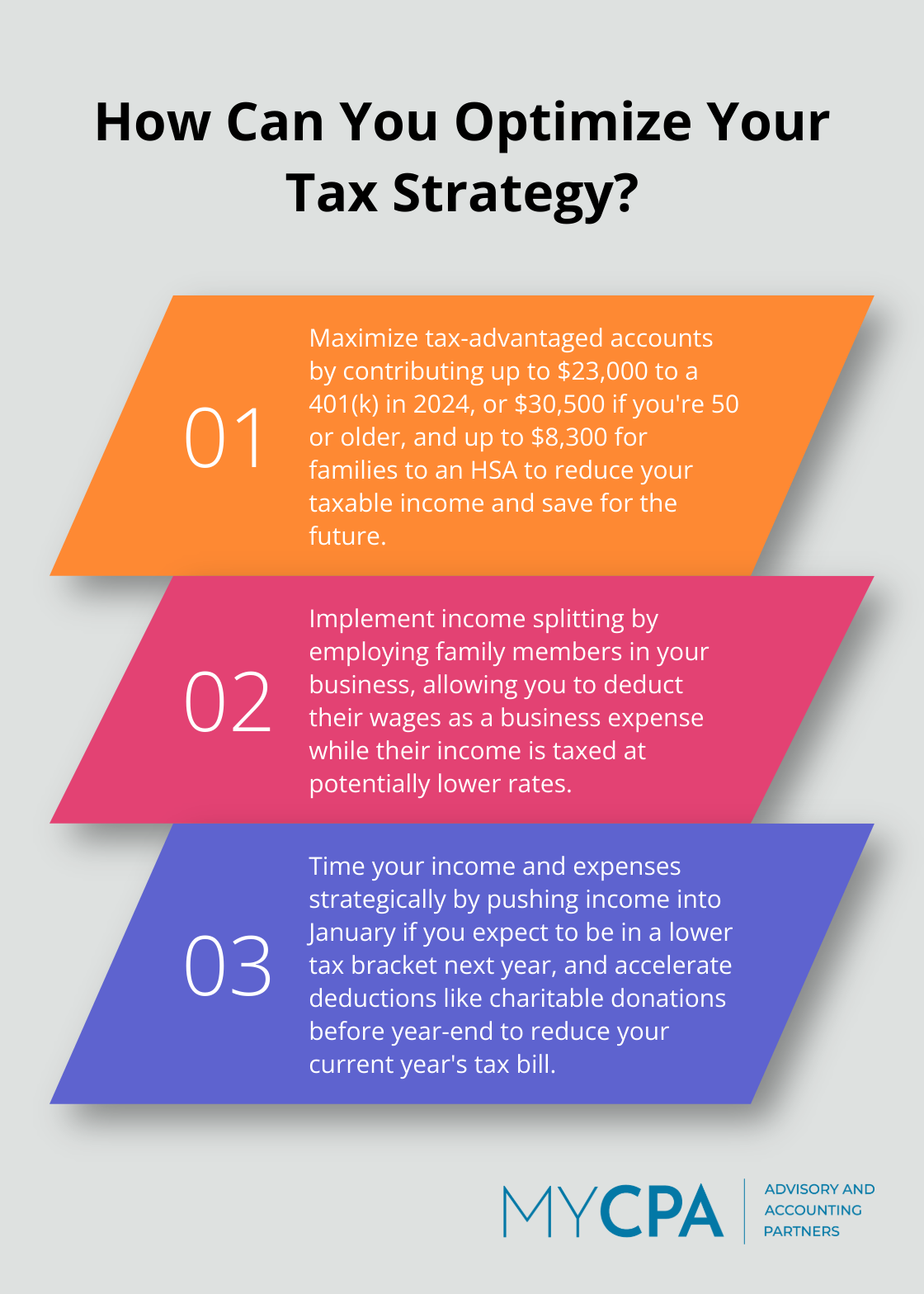

Income splitting is a powerful technique that distributes income among family members or business entities to take advantage of lower tax brackets. For example, business owners might employ their children. This strategy provides a tax deduction for the business while the children’s wages are taxed at their lower rates.

Income shifting moves income from high-tax years to lower-tax years. If your taxable income is going to be lower next year, deferring your income until next year could reduce your tax burden by transferring the income to a lower tax bracket.

Deductions and credits play a crucial role in reducing your tax bill. The key is to identify which ones apply to your situation and claim them correctly.

Self-employed individuals can benefit significantly from the home office deduction. If you use a portion of your home exclusively for business, you may deduct a percentage of your mortgage interest, property taxes, utilities, and maintenance costs.

Credits directly reduce your tax bill dollar-for-dollar. Explore popular tax credits and deductions available to help you save money during tax season in 2024.

The timing of income and expenses can significantly impact your tax liability. Self-employed individuals or those with control over income receipt should consider pushing some income into January if they expect to be in a lower tax bracket next year.

On the expense side, accelerating deductions into the current year can be beneficial. Making charitable donations before year-end, for instance, could reduce your current year’s tax bill.

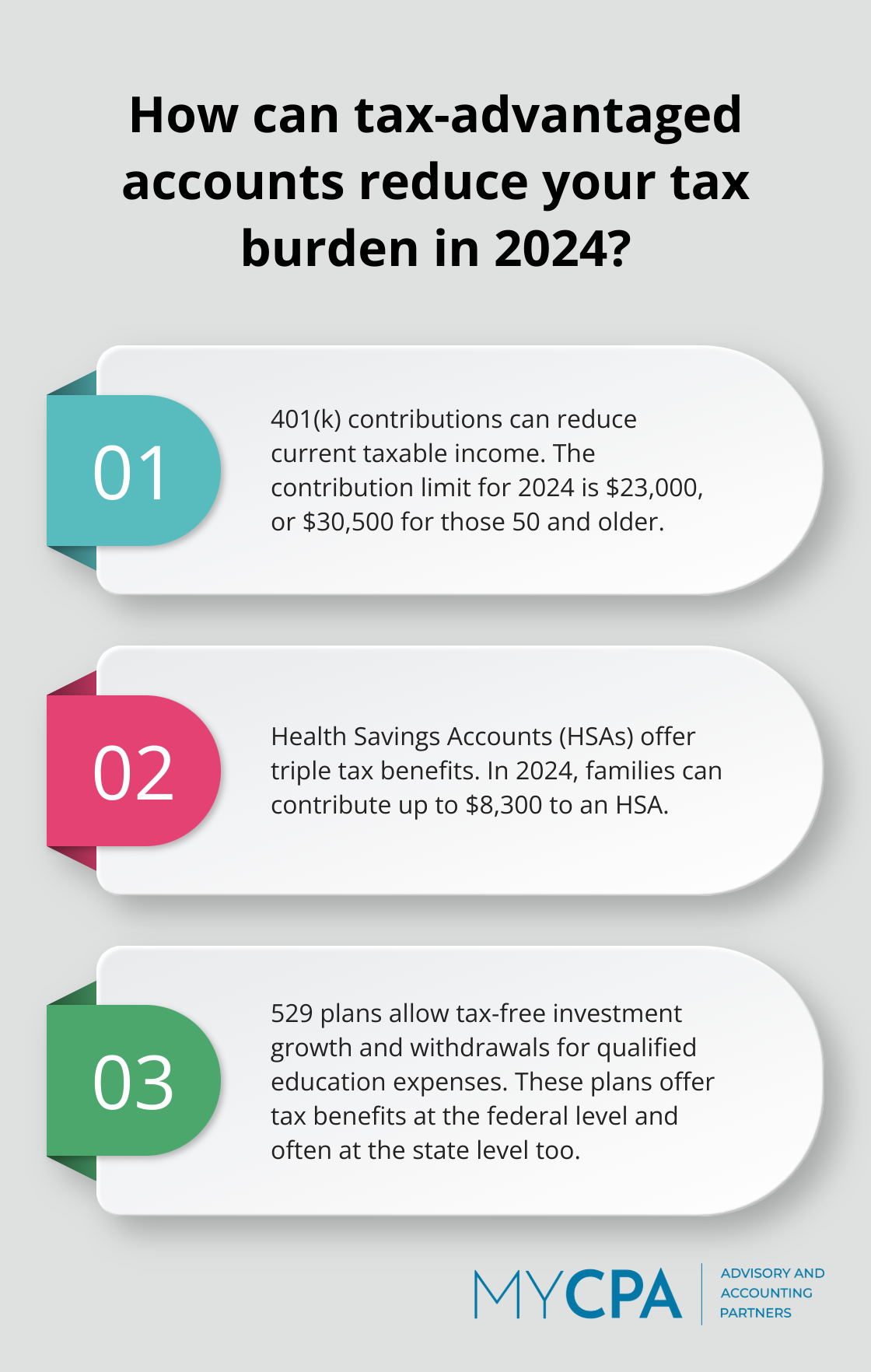

Tax-advantaged accounts are powerful tools for reducing your tax burden while saving for the future. Traditional 401(k)s and IRAs allow pre-tax dollar contributions, reducing your current taxable income. For 2024, you can contribute up to $23,000 to a 401(k), or $30,500 if you’re 50 or older.

Health Savings Accounts (HSAs) offer triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. In 2024, families can contribute up to $8,300 to an HSA.

For education savings, 529 plans allow tax-free investment growth and withdrawals for qualified education expenses (at the federal level and often at the state level too).

While these strategies can make a real difference in your financial life, tax planning is complex and highly individual. What works for one person may not be optimal for another. This complexity underscores the importance of working with qualified tax professionals who can develop personalized strategies tailored to your unique financial situation and goals.

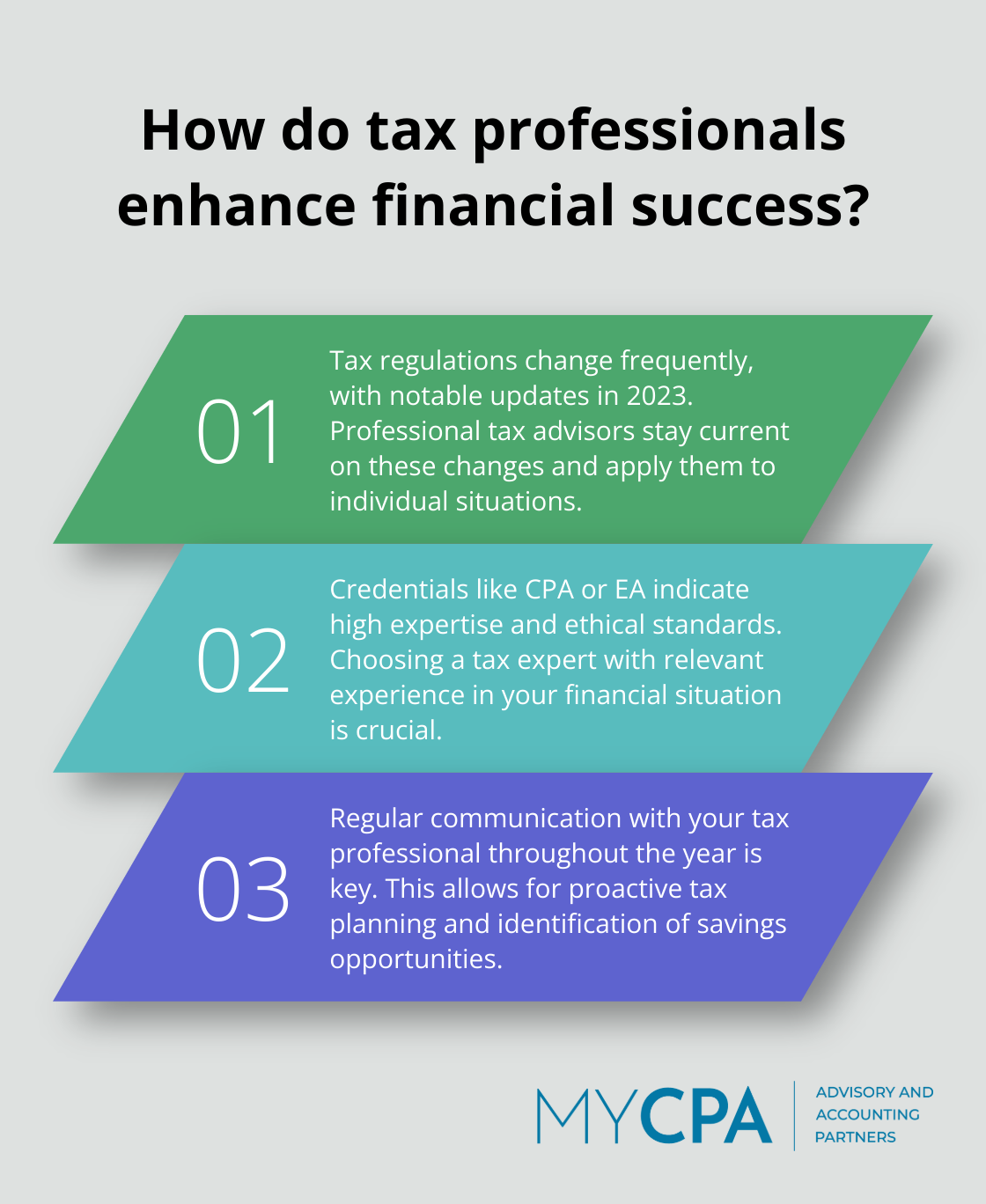

Tax planning involves complex strategies and ever-changing regulations. In 2023, numerous changes affected retirement contributions and electric vehicle credits. A skilled tax professional keeps up with these changes and applies them to your specific situation.

Selecting an appropriate tax professional is a critical decision. Look for credentials such as Certified Public Accountant (CPA) or Enrolled Agent (EA). These designations indicate high levels of expertise and adherence to ethical standards.

Experience in your specific financial situation matters. Small business owners should seek professionals with strong track records in business taxation. Those with complex investments should find advisors well-versed in investment tax strategies.

Interview potential tax advisors. Ask about their experience, approach to tax planning, and methods for staying updated on tax law changes. A competent tax professional should explain complex concepts in understandable terms.

After selecting a tax professional, work together effectively. Provide complete and organized financial information. The more thorough you are, the better your tax professional can work on your behalf.

Communicate proactively. Don’t wait until tax season to contact your advisor. Regular check-ins throughout the year can identify opportunities for tax savings and allow for strategic planning.

Your tax professional serves as a valuable resource. Take advantage of their knowledge by asking questions and seeking explanations. A deeper understanding of your tax situation equips you to make informed financial decisions.

At My CPA Advisory and Accounting Partners, we encourage clients to bring us their financial questions and plans year-round. This ongoing dialogue allows us to provide timely advice that can significantly impact their tax situation.

Modern tax professionals use advanced software and tools to analyze financial data and identify tax-saving opportunities. These technological advancements (combined with human expertise) can lead to more accurate and efficient tax planning strategies.

Effective tax planning requires a year-round approach to optimize your financial position. Strategic income management, maximizing deductions and credits, and leveraging tax-advantaged accounts can lead to substantial savings. The tax landscape evolves constantly, so you must review and adjust your strategies regularly to take advantage of all available opportunities.

Professional guidance often proves invaluable in navigating the complexities of tax laws. At My CPA Advisory and Accounting Partners, we offer personalized tax planning services to help you achieve your financial goals. Our team stays current with the latest regulations to position you for success.

Tax planning involves understanding the tax code and using it legally and ethically to your advantage. A proactive approach to tax planning can minimize your tax burden and maximize your savings (without resorting to risky behavior). You can secure a stronger financial future through informed decision-making and expert advice.

Privacy Policy | Terms & Conditions | Powered by Cajabra