Financial Management for Startups

Explore effective financial management for startups to optimize resources, reduce costs, and boost success with practical tips and tools.

Tax planning for individuals is a powerful tool to reduce your tax burden and keep more of your hard-earned money. At My CPA Advisory and Accounting Partners, we’ve seen firsthand how effective tax strategies can lead to significant savings.

This guide will walk you through key tax planning techniques, from maximizing deductions to leveraging retirement accounts. We’ll also explore how working with a tax professional can help you create a personalized plan for optimal results.

Tax planning is a strategic approach to manage your finances and reduce your tax liability. It involves analyzing your financial situation to minimize tax obligations within legal boundaries. This process doesn’t aim to evade taxes but to make smart decisions that align with tax regulations to your advantage. For example, contributing to a 401(k) can lower your taxable income while building your retirement savings.

The IRS allows certain deductions and credits that can provide more benefits if timed correctly. Self-employed individuals might consider purchasing necessary equipment in December rather than January to claim the deduction in the current tax year.

Knowledge of your tax bracket is essential. Restoring the 39.6% top tax rate and applying it to taxable incomes exceeding $400,000 could save at least $500 billion over a decade. If you’re near the next bracket, strategies such as income deferral or deduction acceleration could keep you in a lower tax bracket, potentially saving you substantial money.

According to Fox Business, tax brackets have shifted higher by 5.4% in 2024 for both single and joint filers. Standard deductions also took an increase. However, itemizing deductions might prove more beneficial if your qualifying expenses exceed these amounts. Common itemized deductions include mortgage interest, state and local taxes (up to $10,000), and charitable contributions.

Tax credits directly reduce your tax bill dollar-for-dollar, making them even more valuable than deductions. The Child Tax Credit can provide up to $2,000 per qualifying child. The Earned Income Tax Credit (EITC) is another powerful tool, especially for low to moderate-income earners.

Tax laws change frequently. The Tax Cuts and Jobs Act provisions will expire in 2026, which could increase top income tax rates and affect various exemptions. Staying informed about these changes is vital for effective tax planning.

As we move forward, let’s explore specific strategies to maximize your tax savings and minimize your tax burden. These techniques will help you take full advantage of the tax planning principles we’ve discussed.

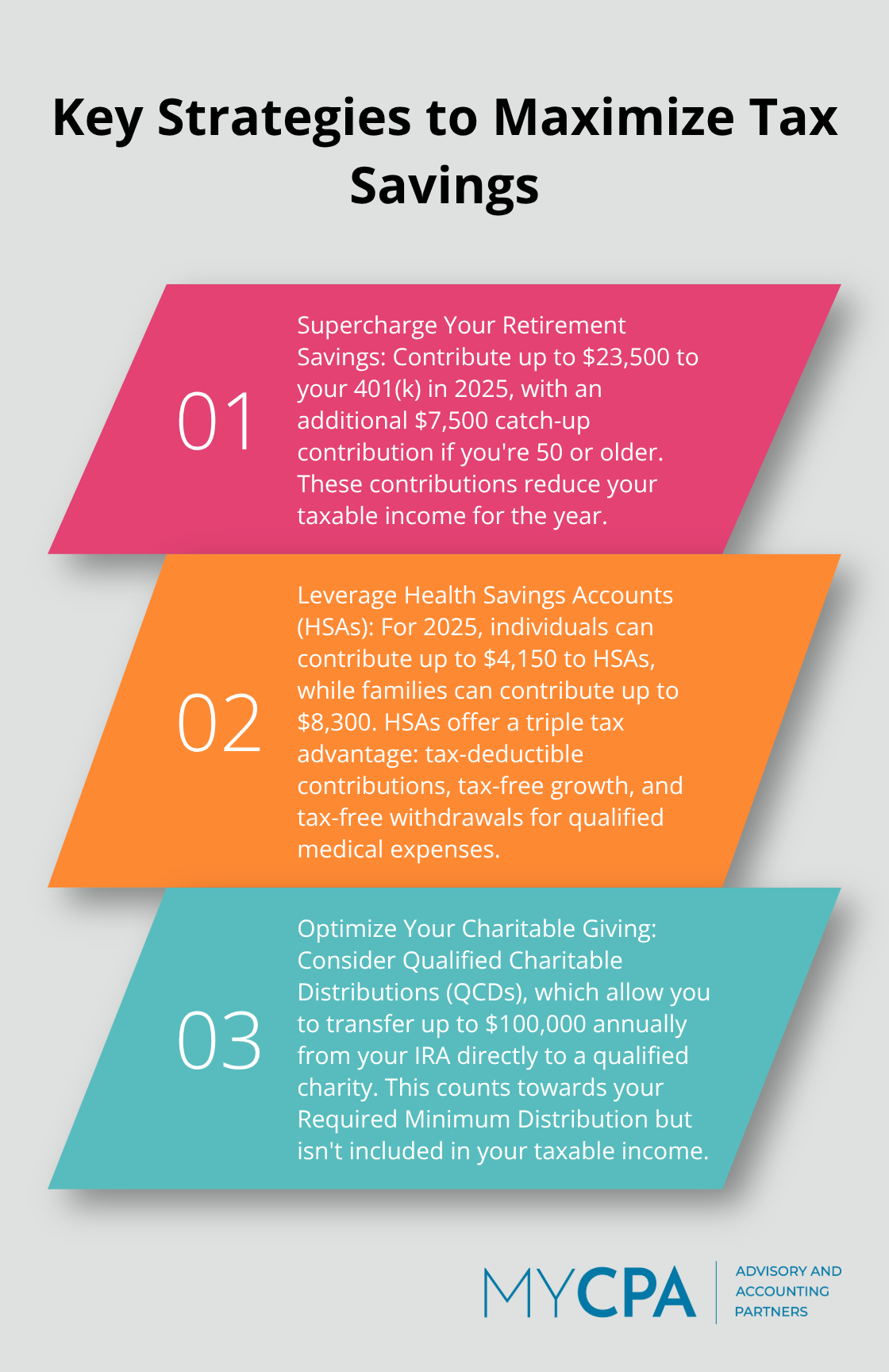

One of the most effective ways to lower your taxable income is to maximize contributions to retirement accounts. In 2025, you can contribute up to $23,500 to your 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older. These contributions are made with pre-tax dollars, which effectively reduces your taxable income for the year.

For Individual Retirement Accounts (IRAs), the contribution limit stands at $7,000 for 2025, with an extra $1,000 catch-up contribution for those 50 and above. Traditional IRA contributions may be tax-deductible (depending on your income and whether you’re covered by an employer-sponsored retirement plan), while Roth IRA contributions offer tax-free growth and withdrawals in retirement.

If you have a high-deductible health plan, an HSA can provide a triple tax advantage. Contributions are tax-deductible, the account grows tax-free, and withdrawals for qualified medical expenses are tax-free. For 2025, individuals can contribute up to $4,150, while families can contribute up to $8,300. Those 55 and older can add an extra $1,000 catch-up contribution.

The timing of your income and expenses can significantly impact your tax liability. If you’re self-employed or have control over when you receive income, consider deferring income to the following year if you expect to be in a lower tax bracket. Conversely, if you anticipate being in a higher bracket next year, accelerating income into the current year might benefit you.

For expenses, bunching deductions into a single year can be advantageous, especially if it pushes you over the threshold for itemizing deductions. This strategy works well for medical expenses, property taxes, and charitable contributions.

Charitable contributions not only support causes you care about but can also provide substantial tax benefits. Consider donating appreciated securities instead of cash. You’ll avoid capital gains tax on the appreciation and still receive a deduction for the full market value of the securities.

For those over 70½, Qualified Charitable Distributions (QCDs) allow you to transfer up to $100,000 annually from your IRA directly to a qualified charity. This counts towards your Required Minimum Distribution (RMD) but isn’t included in your taxable income.

These strategies can help you create a more tax-efficient financial plan. However, tax laws are complex and ever-changing. To ensure you make the most of available opportunities while staying compliant with current regulations, it’s important to work with experienced professionals. This brings us to our next topic: the benefits of working with a tax professional and how to choose the right advisor for your needs.

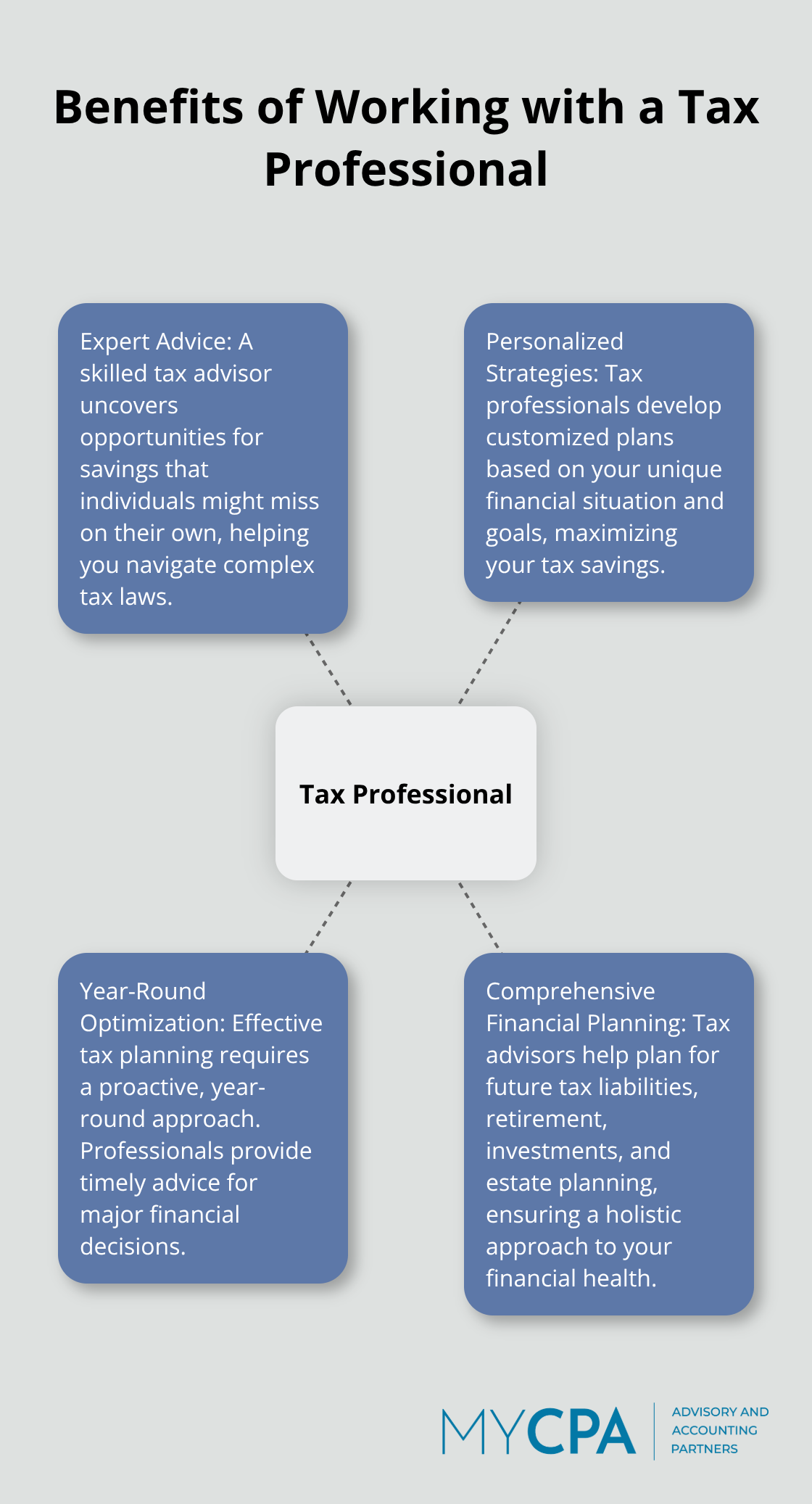

At My CPA Advisory and Accounting Partners, we observe clients who benefit significantly from professional tax advice. A skilled tax advisor uncovers opportunities for savings that individuals might miss on their own. They can help you plan for future tax liabilities, retirement, investments, and estate planning, ensuring a holistic approach to your financial health.

When you choose a tax professional, focus on relevant expertise and credentials. CPAs and Enrolled Agents are both excellent choices, but their specialties differ. CPAs often possess broader financial knowledge, while Enrolled Agents focus specifically on tax matters.

Ask potential advisors about their experience with situations similar to yours. If you own a small business, you need someone well-versed in business tax law. Inquire about their continuing education practices – tax laws change frequently, and your advisor should stay current.

A typical tax planning session involves a comprehensive review of your financial situation. Your advisor will examine your income sources, investments, and potential deductions. They will also discuss your financial goals and how tax strategies can support them.

For example, if you plan to sell a business, your advisor might suggest strategies to minimize capital gains tax. They could recommend spreading the sale over multiple years or using specific tax-deferral methods if you reinvest in similar property.

Effective tax planning requires a year-round approach (not just an annual event). We encourage clients to contact us whenever they consider major financial decisions. This proactive approach allows us to provide timely advice that can significantly impact your tax situation.

Year-round planning helps you anticipate and mitigate potential tax liabilities. For instance, if you think about converting a traditional IRA to a Roth IRA, consult your tax advisor first. They can help you understand the tax implications and choose the most advantageous timing for the conversion.

While tax software can handle basic returns, it cannot replace the personalized strategies and insights a professional provides. Expert guidance helps you navigate the complex tax landscape with confidence and potentially keep more of your hard-earned money.

Tax planning for individuals can significantly impact your financial well-being. You can save thousands of dollars each year and secure a more stable financial future through strategic implementation. Regular reviews of your tax strategy will ensure you take advantage of the latest savings opportunities and stay compliant with current regulations.

A personalized tax plan starts with an assessment of your current financial situation and goals. We recommend working with a professional tax advisor who can provide tailored advice and help you navigate complex tax laws. My CPA Advisory and Accounting Partners offers comprehensive tax services designed to minimize your tax liabilities and enhance your overall financial health.

Our team of experts can help you develop a customized tax strategy that aligns with your unique circumstances and long-term objectives. Don’t wait until tax season to start planning – the time to act is now (your financial future depends on it). Take a proactive approach to tax planning and position yourself for greater financial success.

Privacy Policy | Terms & Conditions | Powered by Cajabra