Monthly Business Advisory: Ongoing Guidance to Keep You on Track

Get ongoing guidance with monthly business advisory services to stay aligned with your goals and make informed decisions

Mutual fund tax efficiency can significantly impact your investment returns. At My CPA Advisory and Accounting Partners, we often see investors overlook this crucial aspect of their portfolio management.

This guide will show you practical strategies to minimize your tax burden while maximizing your mutual fund investments. We’ll explore key concepts and provide actionable tips to help you keep more of your hard-earned money.

Mutual fund taxation significantly impacts investment returns. Understanding the tax implications is essential for maximizing after-tax profits.

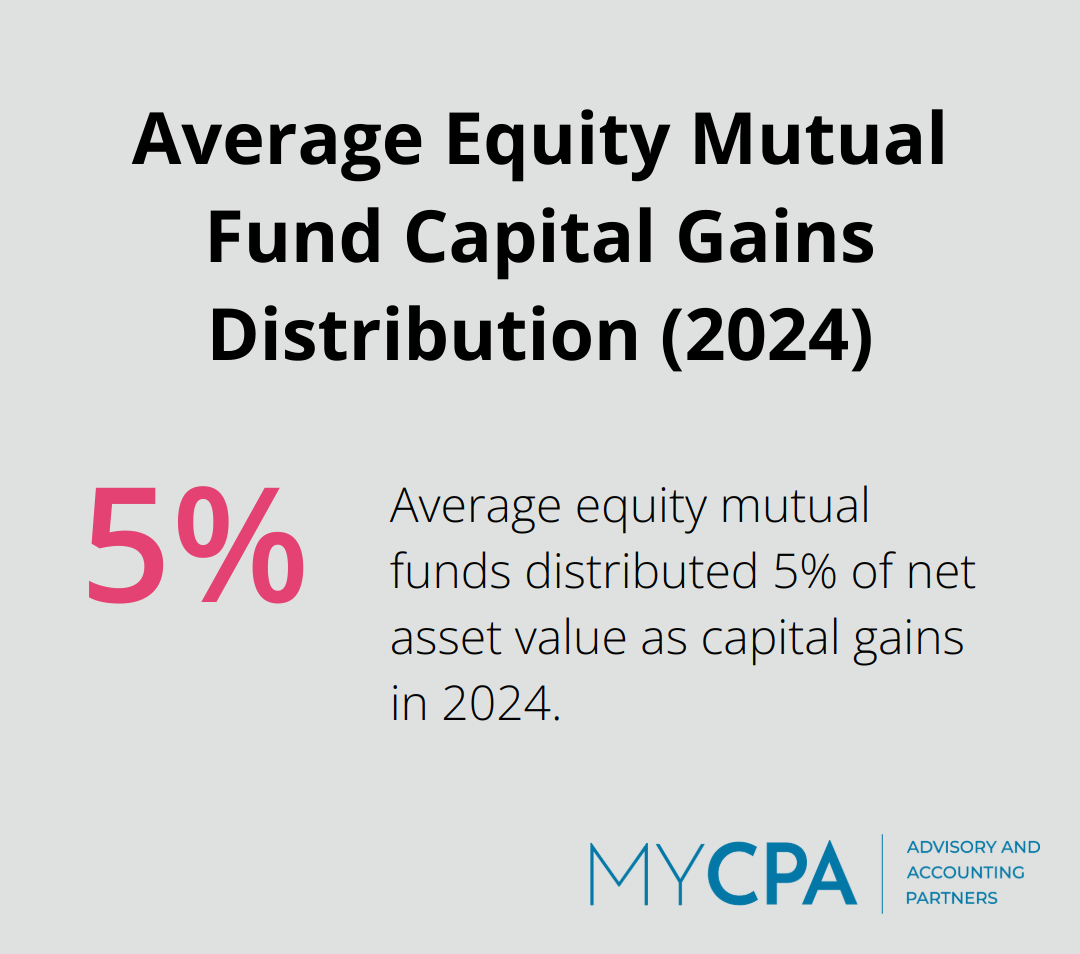

Mutual funds generate two primary types of taxable distributions: capital gains and dividends. Capital gains occur when a fund sells securities at a profit. These gains pass on to shareholders and are taxable, even if reinvested. Morningstar reports that in 2024, the average equity mutual fund distributed capital gains equal to 5% of its net asset value.

Dividends are payments made by companies to their shareholders. Mutual funds holding dividend-paying stocks pass these payments to fund investors. The tax treatment of dividends depends on their classification as qualified or non-qualified. Qualified dividends are taxed at the lower long-term capital gains rate, while non-qualified dividends are taxed as ordinary income.

A fund’s turnover ratio plays a key role in its tax efficiency. This ratio represents how frequently a fund buys and sells its holdings. A high turnover ratio often results in more frequent capital gains distributions, potentially increasing your tax bill.

ETFs can be more tax-efficient compared to traditional mutual funds. Generally, holding an ETF in a taxable account will generate less tax liabilities. Index funds and ETFs typically have lower turnover ratios, making them more tax-efficient options. These funds often have fewer taxable events, leading to better tax efficiency. For instance, the S&P 500 index fund from Vanguard has a turnover ratio of just 4%, compared to the average actively managed large-cap fund’s turnover ratio of 63%.

While tax efficiency is important, it shouldn’t be the sole factor in your investment decisions. Your overall financial goals and risk tolerance should always be considered when selecting investment strategies. This holistic approach ensures a well-rounded portfolio that aligns with your long-term objectives.

As we move forward, let’s explore specific strategies you can employ to maximize the tax efficiency of your mutual fund investments.

Maximizing the tax efficiency of your mutual fund investments can enhance your overall returns. Strategic tax management significantly impacts investment outcomes. Here are practical strategies to minimize your tax burden and optimize your mutual fund portfolio.

One of the most effective ways to boost tax efficiency is to hold mutual funds in tax-advantaged accounts. These include 401(k)s, traditional IRAs, and Roth IRAs. This approach allows you to defer or even eliminate taxes on your investment gains and income.

For example, a Roth IRA allows you to contribute after-tax dollars, but your investments grow tax-free, and you pay no taxes on qualified withdrawals in retirement. This proves particularly beneficial for high-growth or high-income-producing funds.

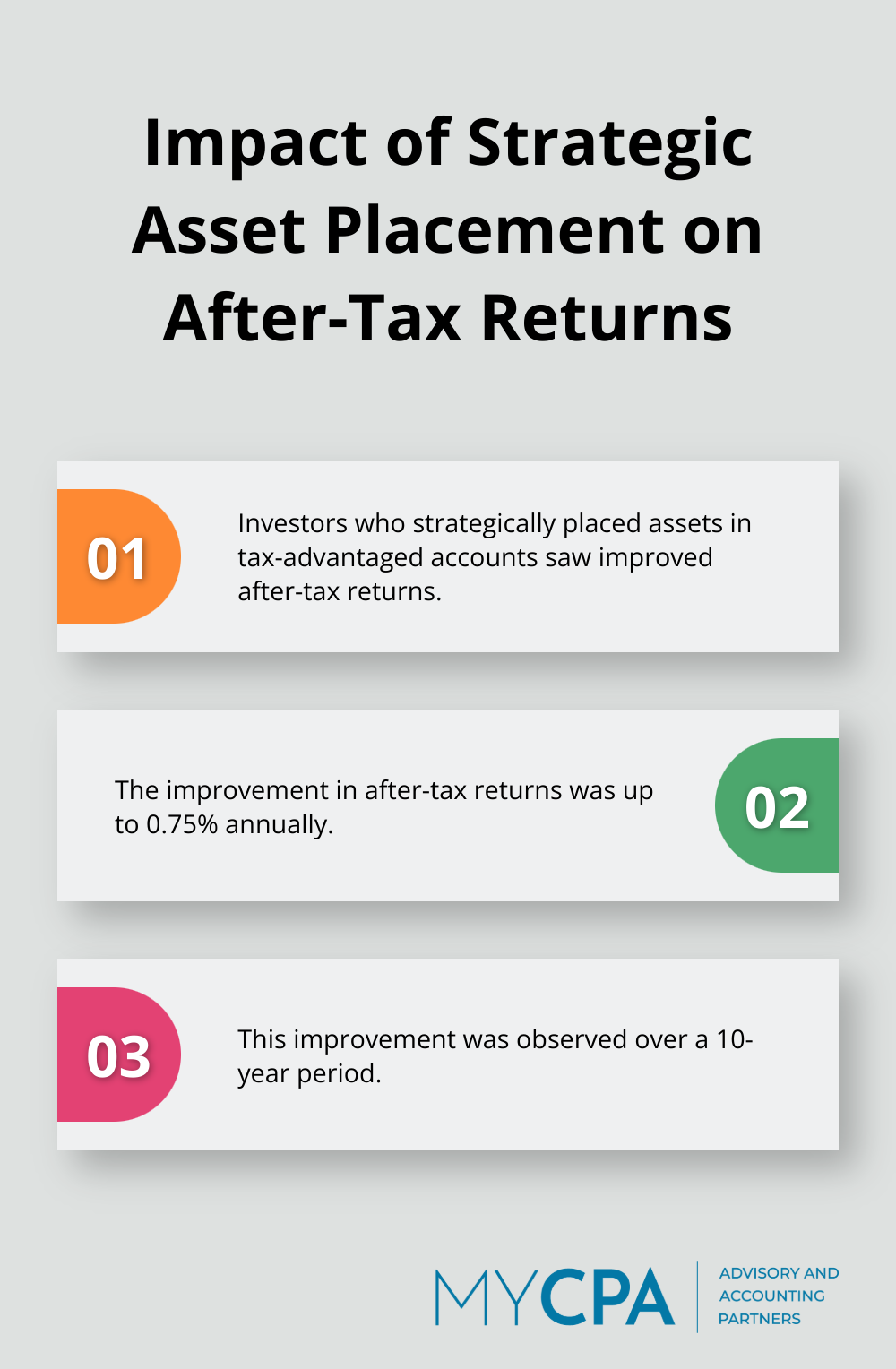

A study by Vanguard found that investors who strategically placed their assets in tax-advantaged accounts improved their after-tax returns by up to 0.75% annually over a 10-year period.

When you invest in taxable accounts, focus on funds designed for tax efficiency. Index funds and ETFs can be more tax efficient compared to traditional mutual funds. The Vanguard Total Stock Market Index Fund (VTSAX) has a turnover rate of just 3%, compared to the average actively managed fund’s rate of 63%.

Municipal bond funds can also serve as tax-efficient options, especially for high-income investors. The interest from these funds is often exempt from federal taxes (and sometimes state taxes as well).

The timing of your mutual fund transactions can significantly impact your tax bill. Avoid buying mutual funds just before they make distributions, as you’ll become liable for taxes on gains you didn’t benefit from.

Consider selling underperforming funds to harvest tax losses, which can offset capital gains. A study by Parametric found that systematic tax-loss harvesting can add up to 2% in after-tax returns annually.

Stay informed about your funds’ distribution schedules. Many mutual funds make significant distributions in December. Check these dates to plan your purchases and sales to minimize tax impact.

A financial advisor can help you navigate complex tax considerations. They can analyze fund distribution histories and work with you to create a tax-efficient investment strategy tailored to your unique financial situation.

Tax efficiency is important, but it shouldn’t be the sole factor in your investment decisions. Your overall financial goals, risk tolerance, and investment timeline should always guide your strategy. The next section will explore how to balance tax efficiency with your broader investment objectives.

Tax-aware investing considers the tax implications of investment decisions. A little investor education on tax treatment can go a long way toward generating better after-tax portfolio returns. It involves careful selection of investments, strategic placement in the right accounts, and optimal timing of transactions to minimize tax liabilities.

Financial advisors work closely with clients to optimize mutual fund strategies. They start with an analysis of your current portfolio, income situation, and long-term financial objectives. This comprehensive assessment identifies opportunities to improve tax efficiency without compromising overall investment goals.

For instance, an advisor might recommend moving high-yield bond funds to tax-advantaged accounts while keeping tax-efficient index funds in taxable accounts. They also help implement tax-loss harvesting strategies, which can offset capital gains and potentially reduce taxable income (up to $3,000 per year).

Tax efficiency is important, but it’s just one piece of the puzzle. A good financial advisor helps strike the right balance between tax minimization and achievement of broader financial objectives. This balance often involves:

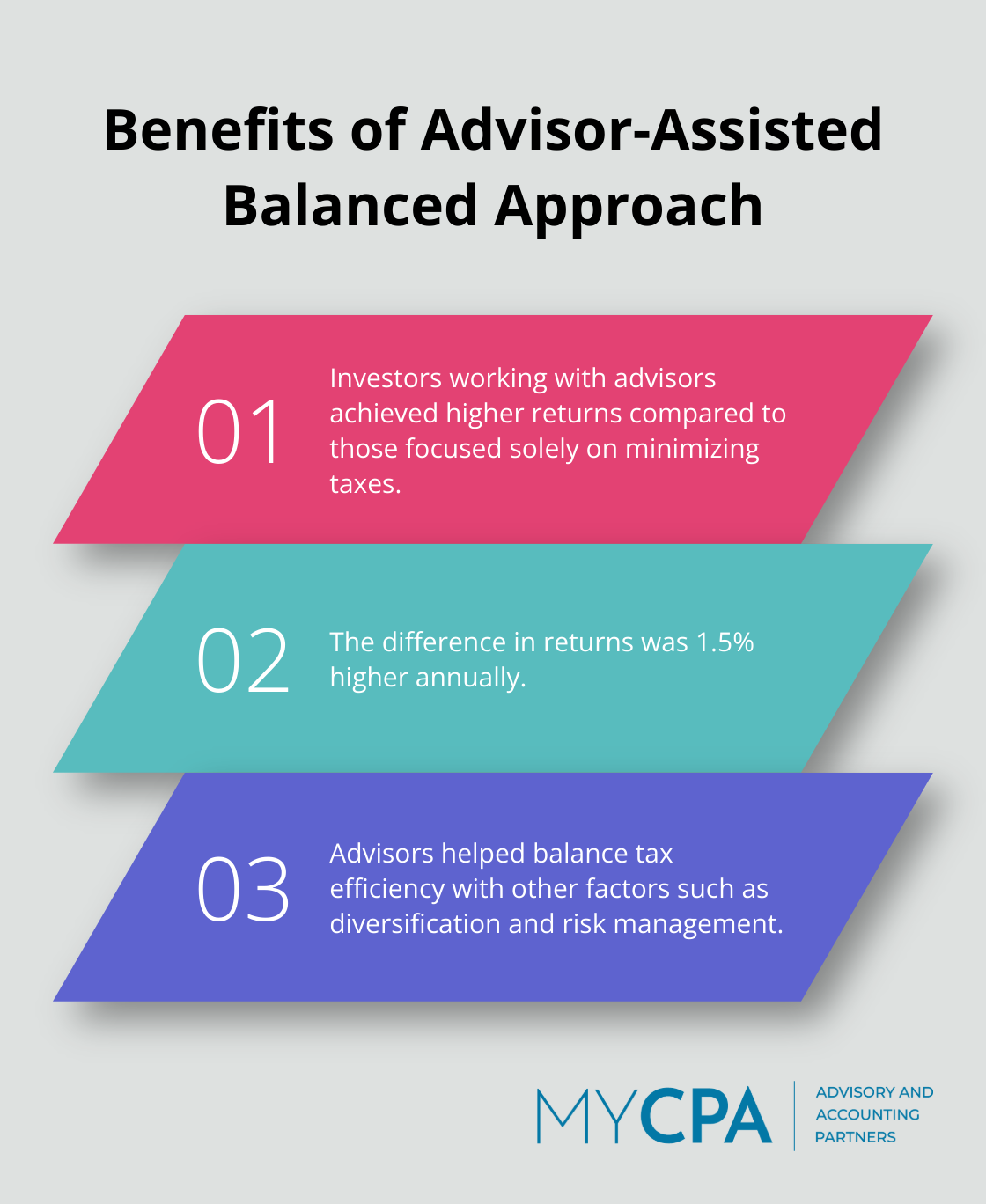

A Morningstar study found that investors who worked with advisors to balance tax efficiency with other factors achieved 1.5% higher returns annually compared to those who focused solely on minimizing taxes.

Financial advisors provide valuable expertise in navigating complex tax situations. They stay updated on tax laws and regulations, which change frequently. This knowledge allows them to adapt strategies quickly to new tax environments, ensuring your investment approach remains optimized.

A key benefit of working with a financial advisor is regular portfolio review and rebalancing. They monitor your investments continuously, making adjustments as needed to maintain tax efficiency and alignment with your goals. This proactive approach helps prevent tax inefficiencies from creeping into your portfolio over time.

For example, long-term investment strategies can significantly improve tax efficiency for certain funds. Advisors can help you implement and maintain such strategies effectively.

Mutual fund tax efficiency plays a vital role in successful investing. Investors can reduce their tax burden and enhance returns through strategic fund selection, timing, and account placement. We recommend a personalized approach that balances tax minimization with risk management, diversification, and income needs for long-term success.

At My CPA Advisory and Accounting Partners, we help clients navigate the complexities of mutual fund tax efficiency. Our team provides tailored strategies to optimize investments, minimize tax liabilities, and align portfolios with unique financial situations and goals. We offer comprehensive tax services designed to enhance financial health and provide peace of mind.

Mutual funds can build wealth, but they require careful planning and management to maximize returns while minimizing tax impact. Implementing effective strategies and seeking professional guidance will help you take control of your investments. Contact us today to learn how we can help you create a more tax-efficient and prosperous financial future.

Privacy Policy | Terms & Conditions | Powered by Cajabra