Tax Compliance Audits: Preparing with Confidence

Prepare for tax compliance audits with confidence using our expert strategies, common audit triggers, and practical steps to protect your business.

Tax planning and strategy can make a significant difference in your financial well-being. At My CPA Advisory and Accounting Partners, we’ve seen how effective tax planning can lead to substantial savings and improved financial outcomes for our clients.

Creating a solid tax strategy isn’t just about filing your returns on time; it’s about making informed decisions throughout the year that can positively impact your tax situation. In this post, we’ll guide you through the process of developing a tax planning strategy that works for your unique circumstances.

Start by listing all your income sources. This includes wages, self-employment income, investments, rental properties, and any other money you receive. Each type of income is taxed differently. For example, long-term capital gains typically face lower tax rates than ordinary income. This knowledge can help you make smarter investment decisions.

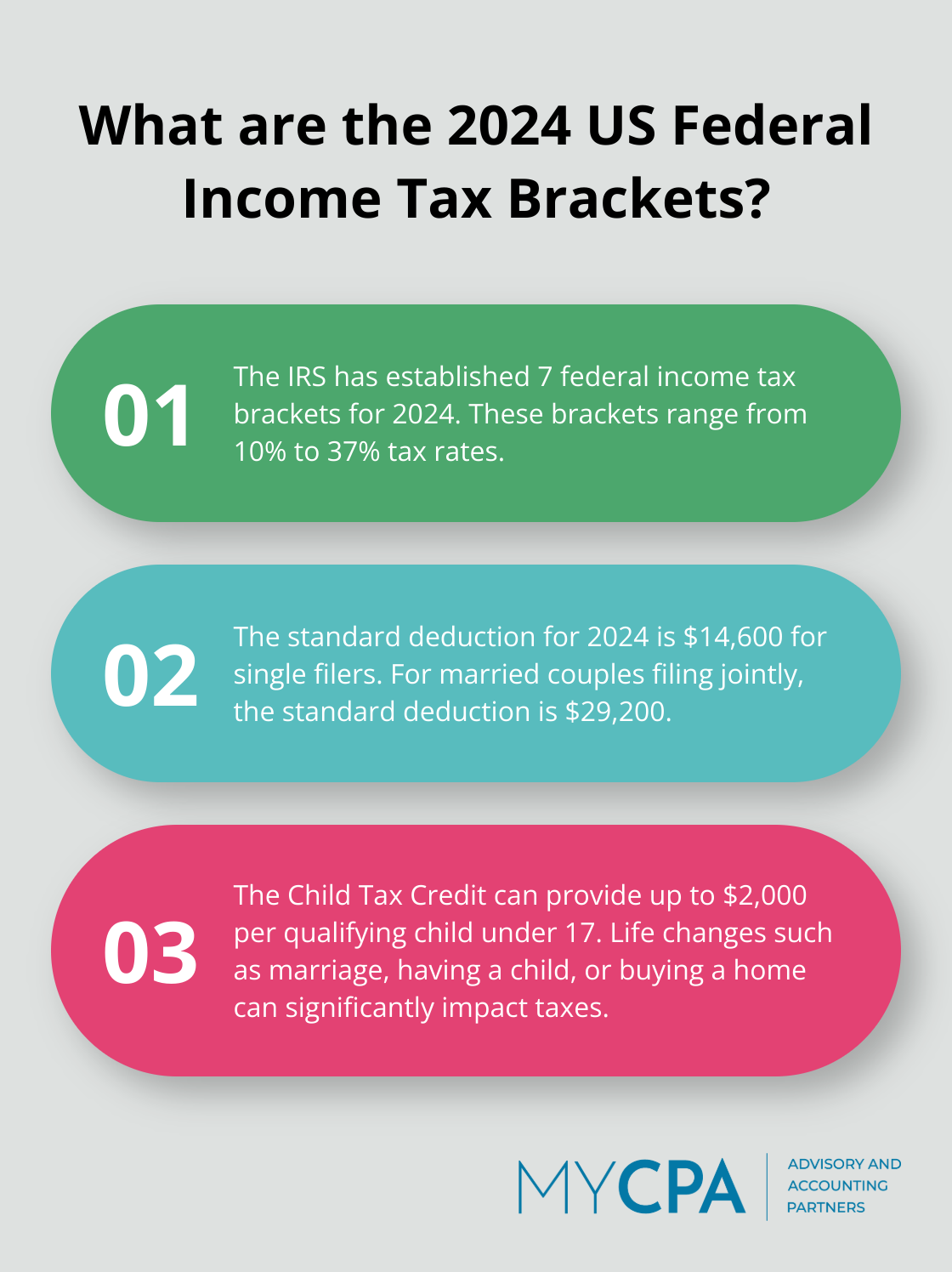

In 2024, the IRS has seven federal income tax brackets (ranging from 10% to 37%). Your total income determines which bracket you fall into. If you’re close to the edge of a bracket, even small changes in income can significantly impact your tax bill.

Next, examine your expenses. Many people miss out on deductions simply because they don’t know what qualifies. Common deductible expenses include mortgage interest, property taxes, and charitable donations. If you’re self-employed, you might deduct home office expenses, travel costs, and health insurance premiums.

Keep in mind that for 2024, the standard deduction is $14,600 for single filers and $29,200 for married couples filing jointly. If your itemized deductions exceed these amounts, you’ll save more by itemizing.

Your past tax returns provide valuable information. They show patterns in your income and deductions that can help you plan for the future. Look for areas where you might have overpaid in the past. Did you miss any deductions? Did you fail to claim any credits?

Reviewing past returns can uncover opportunities for future tax savings. For instance, you might spot a trend of increasing business income that suggests it’s time to consider changing your business structure for tax purposes.

Life changes can significantly impact your taxes. Getting married, having a child, buying a home, or starting a business can all affect your tax situation. For example, the Child Tax Credit can provide up to $2,000 per qualifying child under 17.

If you plan any major life changes, talk to a tax professional about the potential tax implications. A qualified advisor can help you understand how these changes might affect your taxes and adjust your strategy accordingly.

With a clear understanding of your tax situation, you can now move on to the key components of an effective tax planning strategy. These components will help you maximize your tax savings and achieve your financial goals.

An effective tax strategy starts with full utilization of available deductions and credits. The IRS offers numerous opportunities to lower your taxable income, yet many taxpayers miss out due to lack of awareness.

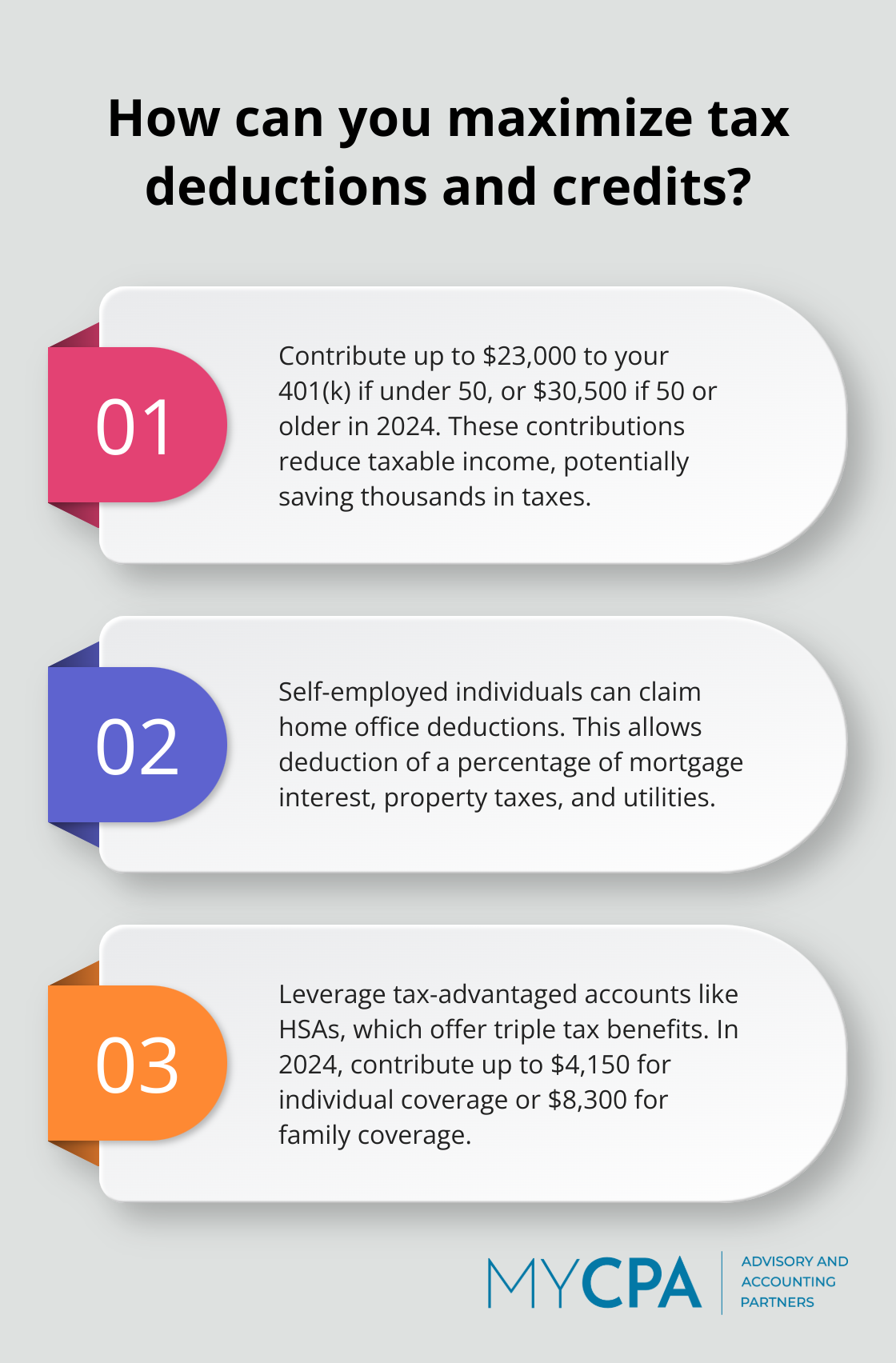

For example, in 2024, you can contribute up to $23,000 to your 401(k) if you’re under 50 (or $30,500 if you’re 50 or older). These contributions reduce your taxable income, potentially saving you thousands in taxes.

Self-employed individuals should not overlook the home office deduction. If you use a portion of your home exclusively for business, you may deduct a percentage of your mortgage interest, property taxes, and utilities.

The timing of income and expenses plays a critical role in tax planning. Strategic timing can potentially lower your tax bill.

Self-employed individuals who expect to be in a lower tax bracket next year might consider deferring some income. Conversely, those anticipating a higher bracket might accelerate income into the current year.

This principle applies to expenses as well. When planning a large business purchase, consider whether it makes more sense to make it this year or next, based on your projected income and tax situation.

Tax-advantaged accounts serve as powerful tools in tax planning. These include retirement accounts like 401(k)s and IRAs, as well as Health Savings Accounts (HSAs) and 529 college savings plans.

HSAs offer a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. In 2024, you can contribute up to $4,150 for individual coverage (or $8,300 for family coverage).

For self-employed individuals and small business owners, the choice of business structure significantly impacts tax obligations. Each entity type (sole proprietorship, partnership, LLC, S corporation, or C corporation) carries different tax implications.

An S corporation can help save on self-employment taxes. Owners of S corporations can use various strategies to lower their taxes, including deductions and credits.

However, the optimal structure depends on various factors, including income level, growth plans, and personal financial situation. This complex decision warrants professional advice.

As you move forward with implementing your tax strategy, it’s important to set clear financial goals and create a year-round plan. The next section will guide you through these crucial steps and highlight the value of professional assistance in navigating the ever-changing landscape of tax laws.

Define clear, measurable financial goals. Try to set specific targets such as “reduce taxable income by $10,000 this year” or “increase retirement contributions by 5%.” These concrete goals provide a framework for your tax planning efforts and make it easier to track progress.

Create a monthly tax planning checklist to ensure you consistently work towards your goals. This might include reviewing business expenses, updating income projections, or scheduling quarterly meetings with your tax advisor. A monthly approach to tax strategy helps you avoid last-minute scrambles that often lead to missed opportunities.

The complexities of tax law often require professional guidance. A qualified tax advisor can provide personalized strategies tailored to your unique financial situation. They can also help you navigate complex issues like business structure optimization or international tax considerations.

Tax laws constantly evolve, and staying informed is essential for effective planning. The Tax Cuts and Jobs Act reduced statutory tax rates at almost all levels of taxable income and shifted the thresholds for several income tax brackets. Subscribe to reputable tax news sources, attend workshops, or follow tax professionals on social media to stay current.

Don’t wait until tax season to assess your financial situation. Conduct quarterly reviews of your income, expenses, and tax projections. This regular check-in allows you to make timely adjustments to your strategy. If you’re self-employed or have variable income, these reviews are particularly important for managing estimated tax payments and avoiding penalties.

Effective tax planning relies on accurate and organized financial records. Invest time in setting up a robust record-keeping system (whether it’s a digital solution like QuickBooks or a well-organized physical filing system). Proper documentation not only makes tax preparation easier but also provides valuable insights for ongoing financial decision-making.

Tax planning and strategy forms the foundation of financial success. You can reduce your tax burden significantly through understanding your tax situation, maximizing deductions and credits, and timing income and expenses strategically. Regular reviews and adjustments ensure your strategy remains effective as your financial situation evolves.

Proactive tax planning offers benefits beyond reducing your tax bill. It improves cash flow, supports long-term financial goals, and provides peace of mind. Taking control of your tax situation positions you to make informed financial decisions and seize opportunities for growth and wealth creation.

At My CPA Advisory and Accounting Partners, we provide personalized strategies tailored to your unique financial situation. Our team of experts guides you through the complexities of tax planning. Visit our website to learn more about how we can help you create and implement an effective tax planning strategy that aligns with your financial goals.

Privacy Policy | Terms & Conditions | Powered by Cajabra