Financial Reporting Accuracy: How Precise Data Powers Confident Decisions

Improve financial reporting accuracy with precise data practices for confident decisions and stronger compliance.

Tax planning for businesses is a critical aspect of financial management that can significantly impact your bottom line. At My CPA Advisory and Accounting Partners, we’ve seen how effective tax strategies can lead to substantial savings and improved cash flow for our clients.

This guide will explore essential tax planning techniques that can help your business optimize its tax position and financial performance. From maximizing deductions to choosing the right business structure, we’ll cover key strategies that can make a real difference to your company’s financial health.

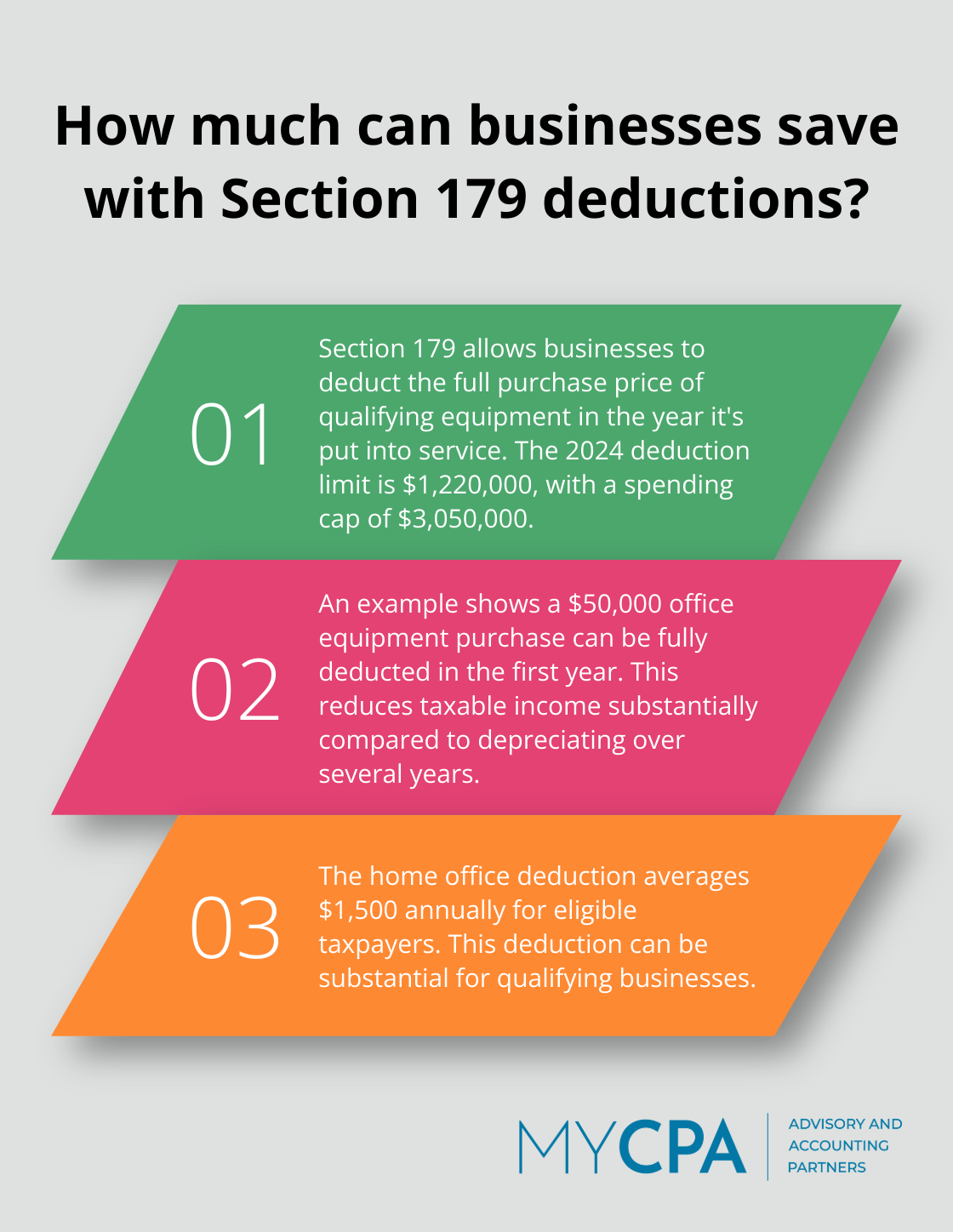

The IRS allows businesses to deduct ordinary and necessary expenses. These typically include office rent, employee wages, utilities, and business-related travel. Many businesses overlook less obvious deductions. The home office deduction can be substantial for those who qualify. The National Association for the Self-Employed reports this deduction averages $1,500 annually for eligible taxpayers.

Professional development costs, such as courses or certifications related to your industry, are also deductible. Even bank fees and interest on business loans can be written off. Businesses should track these expenses meticulously throughout the year to maximize deductions come tax time.

Depreciation allows businesses to deduct the cost of assets over time, but Section 179 offers an opportunity to deduct the full purchase price of qualifying equipment in the year it’s put into service. This can lead to significant tax savings. For 2024, the Section 179 deduction limit is $1,220,000, with a spending cap of $3,050,000.

Consider this example: You purchase $50,000 worth of office equipment. Instead of depreciating it over several years, you could potentially deduct the entire amount in the first year, reducing your taxable income substantially. However, it’s important to weigh the benefits of immediate deduction against potential future tax implications.

Accurate record-keeping is essential when it comes to tax deductions. The IRS requires clear documentation to support your claims. This means keeping detailed receipts, maintaining mileage logs for business travel, and clearly separating personal and business expenses.

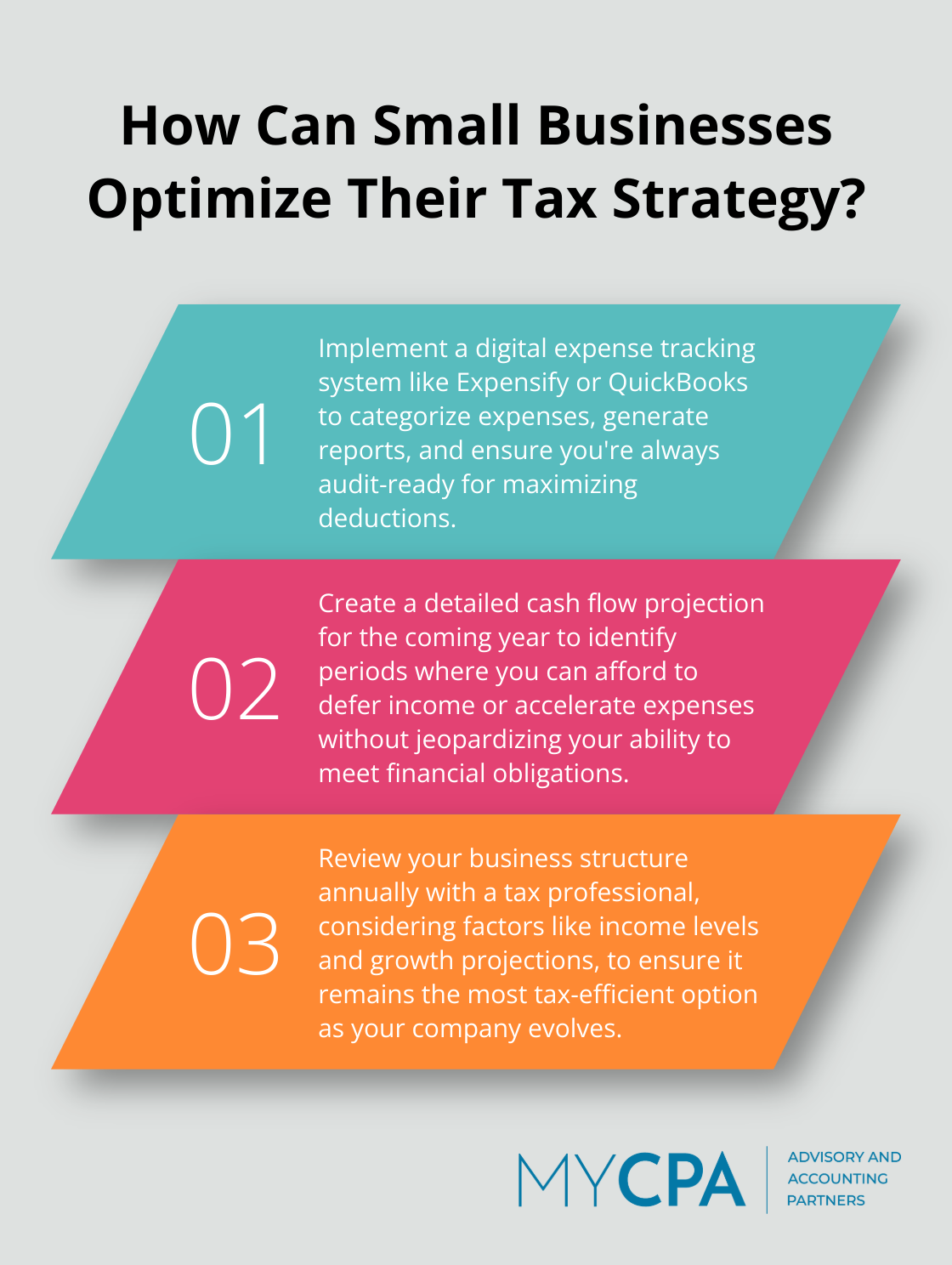

Implement a digital expense tracking system. Tools like Expensify or QuickBooks can streamline this process, making it easier to categorize expenses and generate reports. These solutions help ensure businesses are always audit-ready.

Businesses often miss out on valuable deductions. Some commonly overlooked items include:

Take time to review all business expenses with a tax professional. You might uncover additional deductions that can significantly reduce your tax liability.

Tax laws change frequently, and new deductions or credits may become available. Stay informed about these changes to take advantage of new opportunities. Subscribe to reputable tax news sources or consult regularly with a tax professional to ensure you’re not missing out on potential savings.

The key to maximizing deductions is to stay informed and organized throughout the year. Regular consultations with a tax professional can help identify new opportunities and ensure you’re taking advantage of all available deductions. These strategies to minimize taxes can significantly reduce your tax burden, allowing you to reinvest those savings back into your business’s growth. As we move forward, let’s explore how strategic timing of income and expenses can further optimize your tax position.

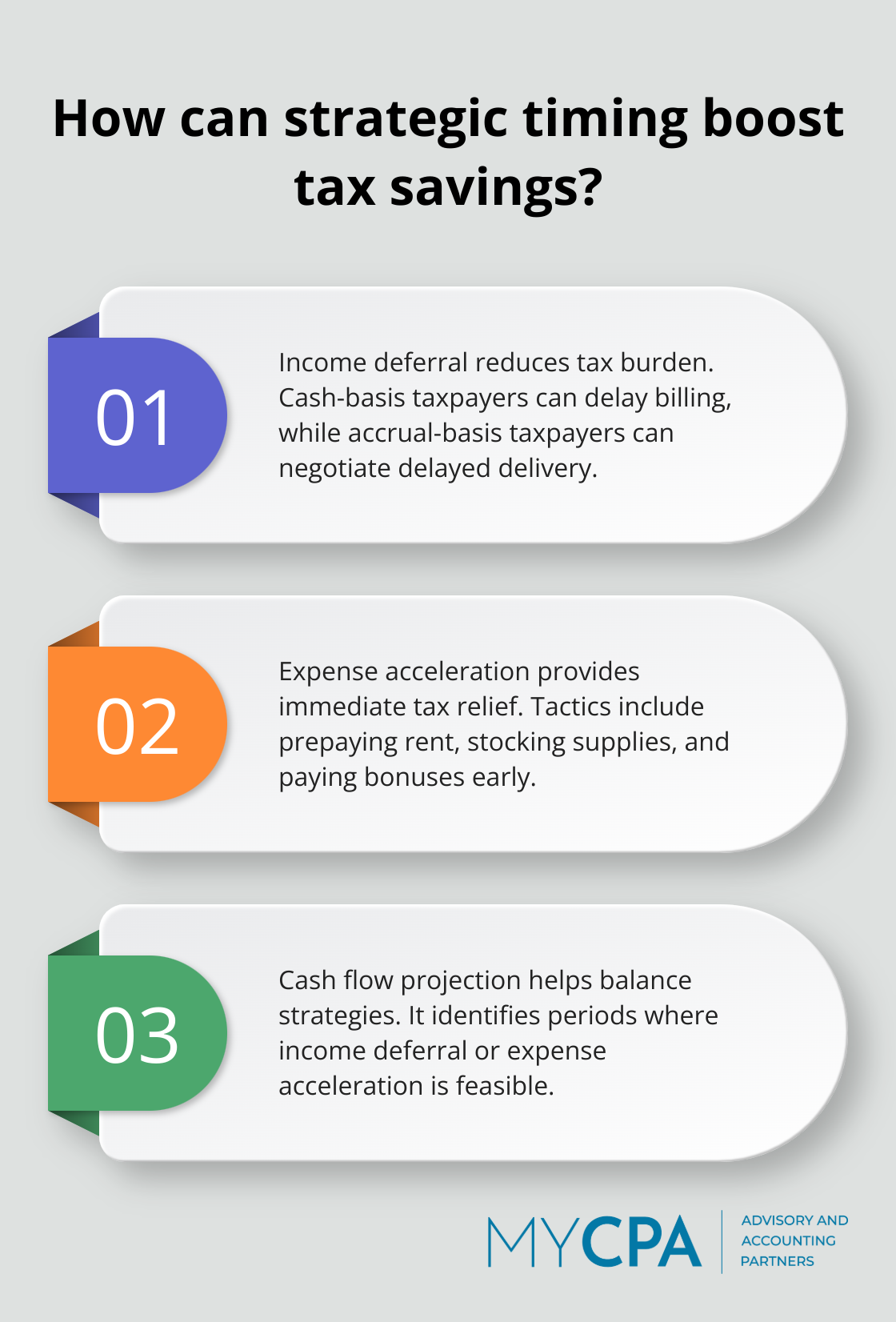

Income deferral stands as a potent strategy in tax planning. Businesses can reduce their tax burden by pushing income recognition to the next tax year, especially if they expect to fall into a lower tax bracket. Cash-basis taxpayers might delay billing for services until late December, ensuring payment arrives in January. Accrual-basis taxpayers have fewer options but can negotiate contracts to delay delivery or acceptance of goods or services until the new year.

While income deferral pushes tax liability into the future, expense acceleration provides immediate tax relief. This strategy involves paying for deductible business expenses before year-end. Common tactics include:

These strategies yield substantial tax savings, but businesses must balance them with cash flow needs. Deferring too much income or accelerating too many expenses could lead to a shortage in operating capital.

Create a detailed cash flow projection for the coming year. This will help identify periods where you can afford to defer income or accelerate expenses without jeopardizing your ability to meet financial obligations.

The Tax Cuts and Jobs Act of 2017 included significant changes to the tax code. Many of these changes were enacted on a temporary basis and are set to expire after 2025.

If you expect tax rates to rise, it might benefit you to accelerate income into years with lower rates and defer deductions to years with higher rates. Conversely, if you anticipate lower future rates, the opposite approach might prove more advantageous.

Stay informed about potential tax law changes and work with a professional who can help you model different scenarios. At My CPA Advisory and Accounting Partners, we continuously monitor tax legislation and help our clients adjust their strategies accordingly.

Proper timing also involves managing estimated tax payments. Underpayment can result in penalties, while overpayment ties up cash unnecessarily.

The IRS allows businesses to use the “annualized income installment method” for calculating estimated taxes. This method benefits businesses with fluctuating income throughout the year, as it allows lower estimated taxes during lean periods and higher amounts during more profitable times.

Strategic timing of income and expenses requires careful consideration of your business’s unique financial situation and future prospects. While the potential savings are substantial, implement these strategies thoughtfully and in consultation with experienced professionals. As we move forward, let’s explore how choosing the right business structure can further optimize your tax position and overall financial performance.

S Corporations offer a unique blend of benefits. Profits and losses pass through to shareholders’ personal tax returns, which avoids double taxation. This structure can benefit businesses with substantial profits. The IRS reports that the total number of returns filed by S corporations for Tax Year 2003 increased 5.9 percent to nearly 3.3 million, from nearly 3.2 million.

S Corporation owners can pay themselves a reasonable salary and take additional profits as distributions (which aren’t subject to self-employment tax). This arrangement can lead to significant tax savings. However, the IRS scrutinizes these salary-distribution splits closely, so owners must set justifiable salaries.

C Corporations face double taxation – the corporation pays taxes on profits, and shareholders pay taxes on dividends. Despite this drawback, C Corporations offer advantages for larger businesses or those planning to go public. They allow for multiple classes of stock and have no restrictions on the number or type of shareholders.

The Tax Cuts and Jobs Act of 2017 reduced the corporate tax rate. However, this rate will expire after 2025, which underscores the importance of long-term tax planning.

Limited Liability Companies (LLCs) offer flexibility in taxation. Single-member LLCs are taxed as sole proprietorships by default, and multi-member LLCs as partnerships. However, LLCs can elect to be taxed as S Corporations or C Corporations, which provides a unique level of adaptability.

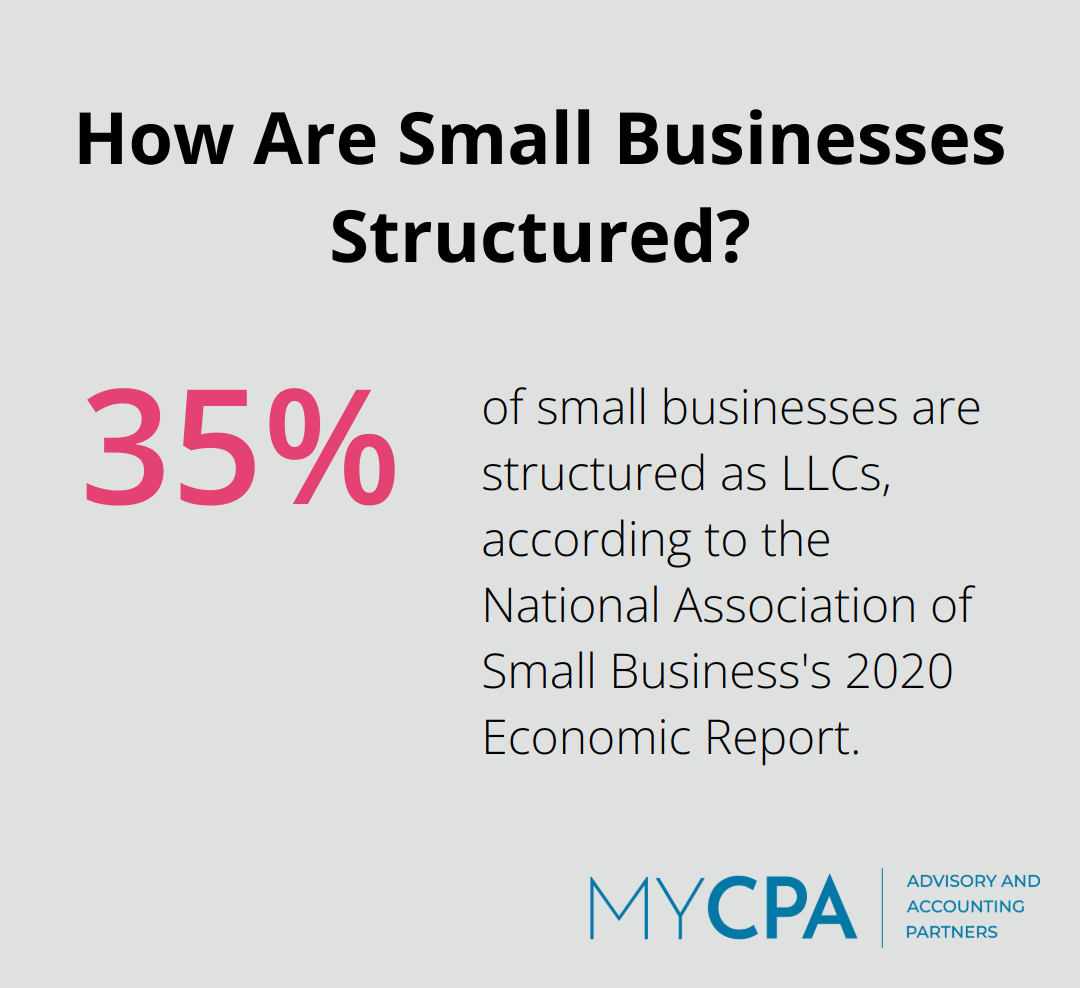

LLCs appeal to small business owners due to their simplicity and protection of personal assets. The National Association of Small Business’s 2020 Economic Report indicates that 35% of small businesses are structured as LLCs.

A business structure change can yield significant tax benefits, but it requires careful consideration. Try to change your business structure if:

Selecting the right business structure involves complex considerations (tax implications, liability protection, and operational flexibility). Professional guidance can prove invaluable in this decision-making process. Tax professionals can analyze your unique situation, consider factors like income levels and growth projections, and recommend the most tax-efficient structure.

The optimal business structure can change as your company evolves. Regular reviews with a tax professional (such as those at My CPA Advisory and Accounting Partners) can ensure your structure continues to serve your best interests.

Tax planning for businesses requires a multifaceted approach to optimize financial health. Companies can minimize tax burdens through strategic deduction maximization, income and expense timing, and appropriate business structure selection. Professional guidance proves invaluable in navigating complex tax regulations and developing tailored strategies that align with specific business goals.

Effective tax planning leads to improved cash flow, increased profitability, and better financial decision-making. It frees up resources for reinvestment and growth, potentially providing a competitive edge in the industry. Every business has unique needs, so a customized tax plan maximizes financial potential.

We at My CPA Advisory and Accounting Partners specialize in providing tailored tax strategies for businesses. Our team stays current with the latest tax regulations to help navigate complex financial decisions. Take the first step towards optimizing your tax strategy today and set your business on the path to greater financial prosperity.

Privacy Policy | Terms & Conditions | Powered by Cajabra