Financial Reporting Best Practices: Elevate Your Financial Story

Master financial reporting best practices to transform how stakeholders perceive your business's financial health and growth potential.

At My CPA Advisory and Accounting Partners, we often encounter questions about comprehensive income in accounting. This financial reporting concept goes beyond traditional net income to provide a more complete picture of a company’s financial performance.

Comprehensive income includes both realized and unrealized gains and losses, offering valuable insights into a company’s long-term financial health. In this post, we’ll explore the components of comprehensive income, its importance in financial reporting, and how it impacts financial analysis and decision-making.

Comprehensive income represents a broader measure of a company’s financial performance than traditional net income. It includes both realized and unrealized gains and losses, providing a more complete picture of a company’s financial health.

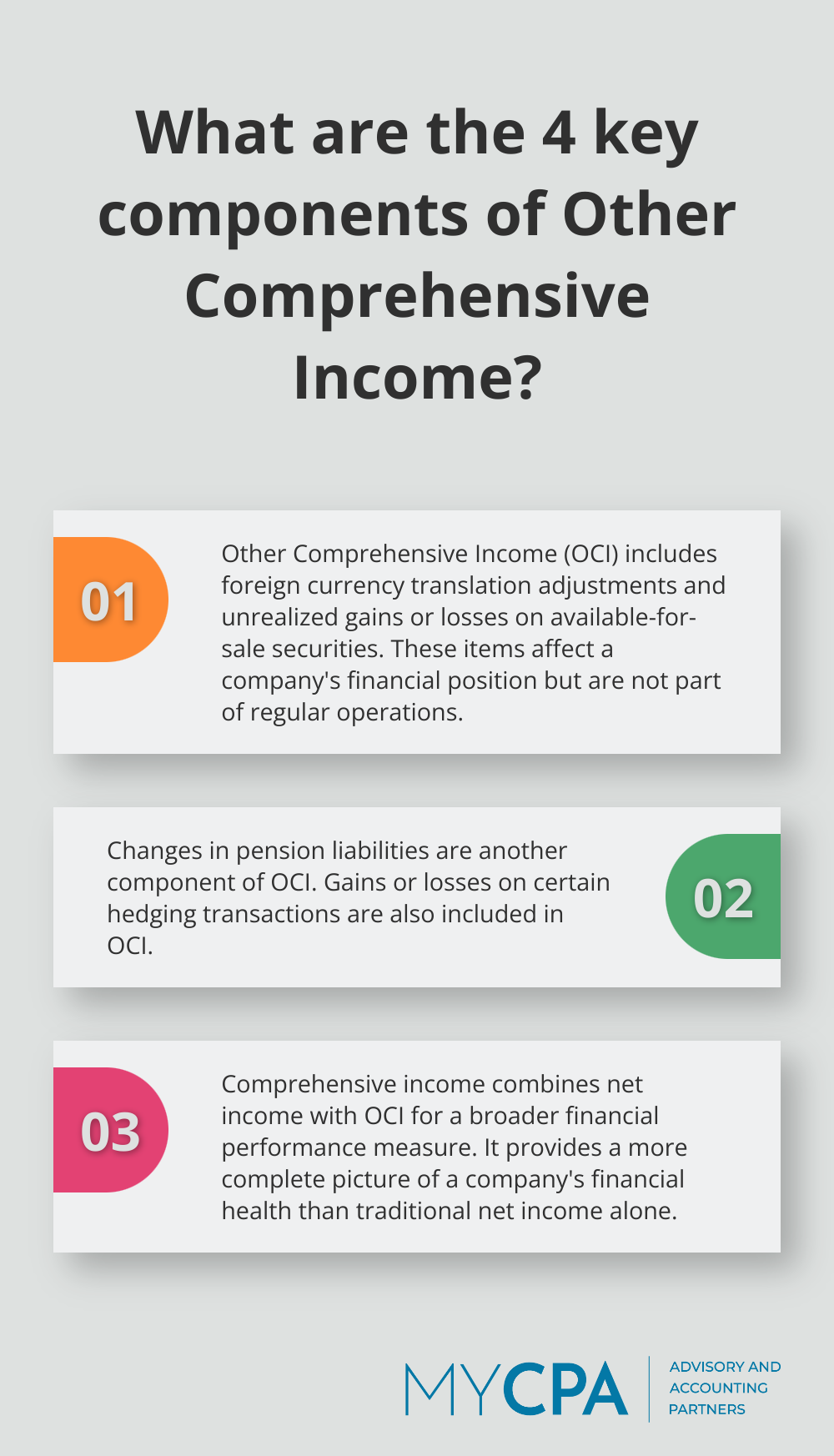

Net income, the bottom line on a typical income statement, includes realized gains and losses from a company’s primary operations. Comprehensive income expands on this by incorporating net income and adding other comprehensive income (OCI), which consists of unrealized gains and losses not reflected in the income statement.

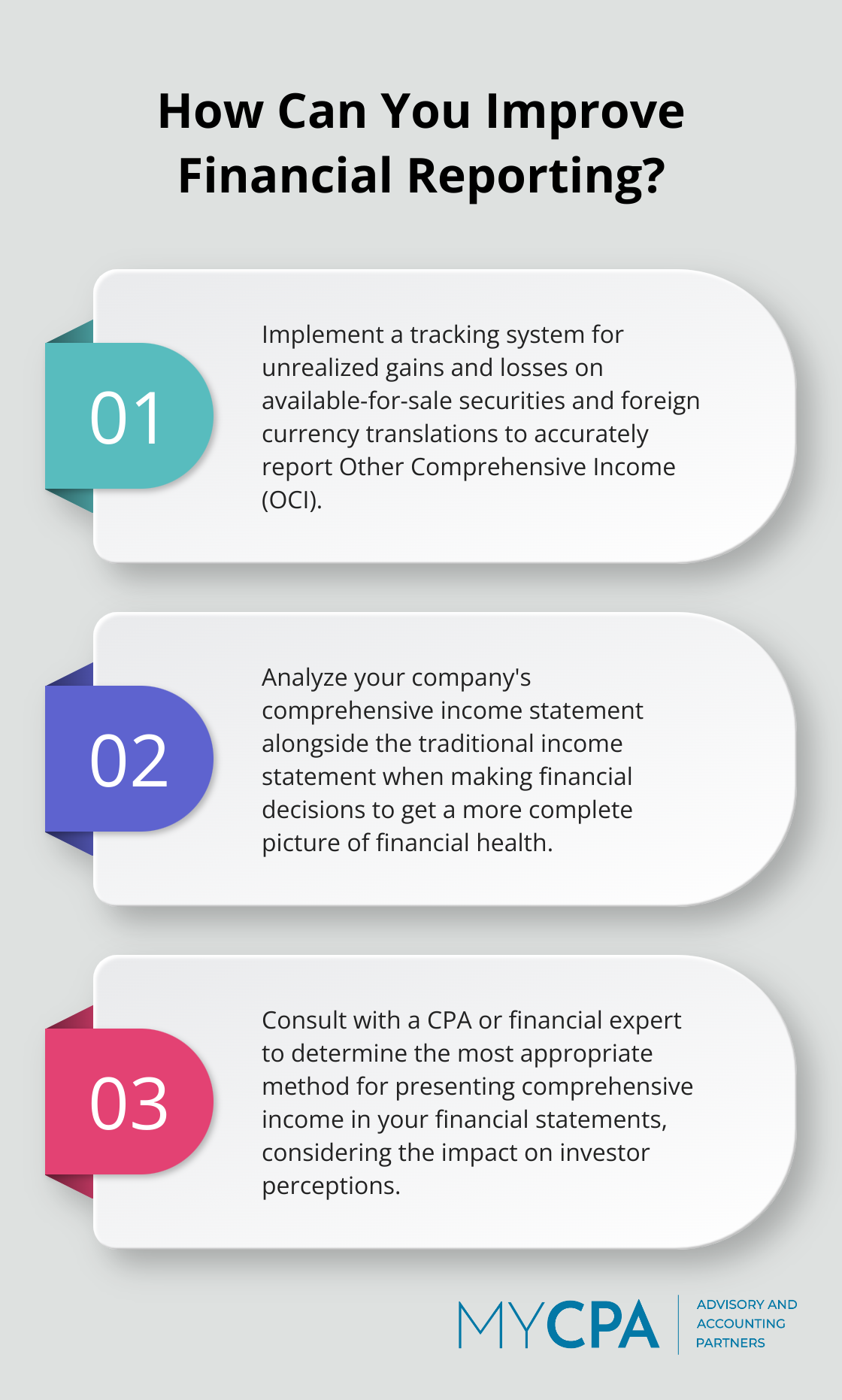

OCI typically includes several key elements:

These items can significantly affect a company’s financial position but are not part of regular operations.

Understanding comprehensive income is essential for accurate financial analysis. A company might report a healthy net income but show substantial losses in OCI due to currency fluctuations or market value changes in investments. This could signal potential future risks or opportunities that are not immediately apparent from net income alone.

Under both U.S. GAAP and IFRS, companies must report comprehensive income. They can choose to present it in a single statement of comprehensive income or in two separate but consecutive statements. This flexibility allows companies to highlight their operational performance while still providing a complete picture of their financial health.

As we move forward to explore the importance of comprehensive income in financial reporting, it becomes clear that this concept offers valuable insights beyond traditional financial statements. The next section will examine how comprehensive income enhances our understanding of a company’s overall financial performance and its implications for investors and stakeholders.

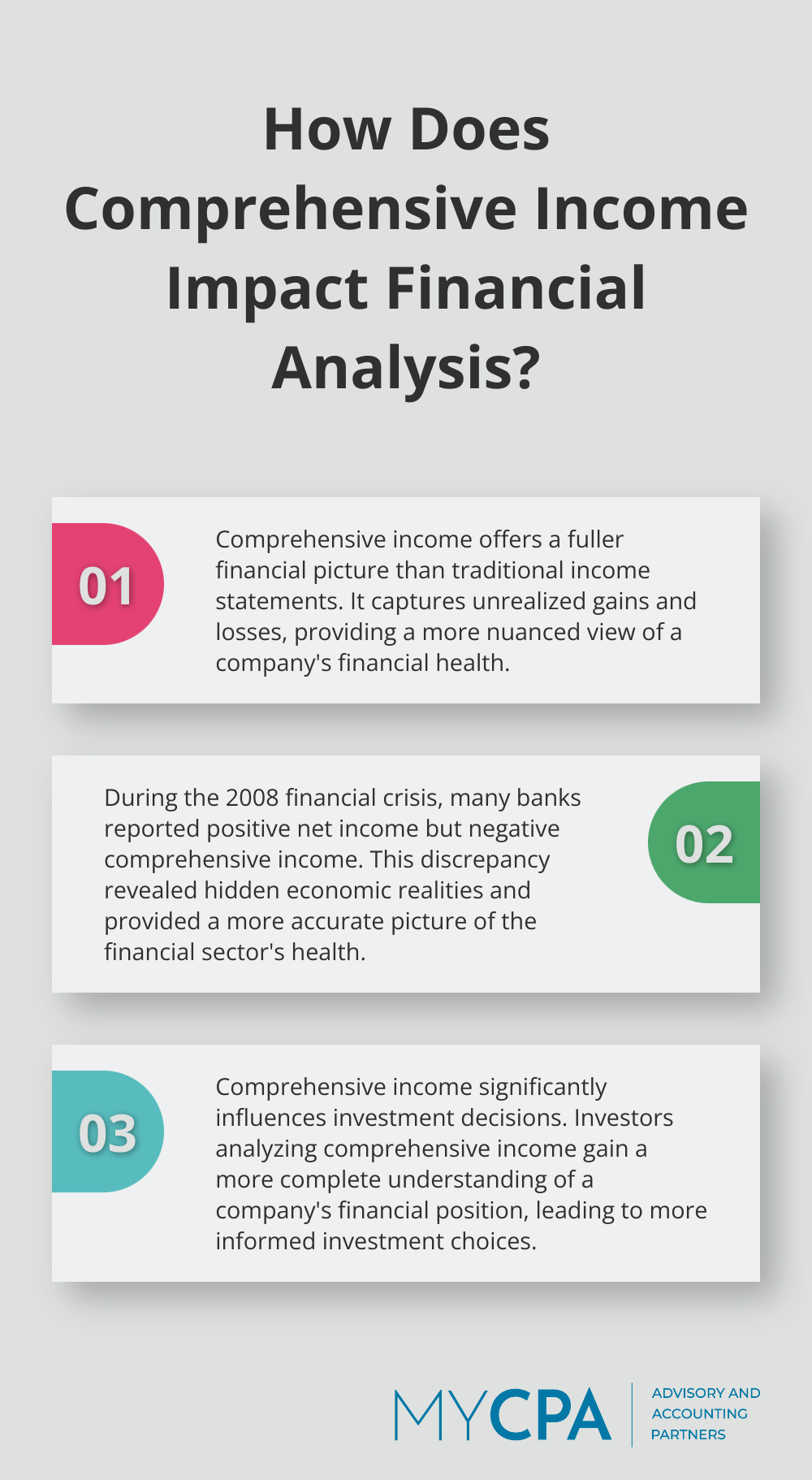

Comprehensive income provides stakeholders with a more nuanced view of a company’s financial health. Traditional income statements often fail to capture the full scope of financial performance. This substantial figure underscores OCI’s potential to materially affect a company’s financial position.

Comprehensive income serves as a critical indicator of long-term financial health. This highlights the importance of looking beyond net income to gauge a company’s true financial trajectory.

The inclusion of unrealized gains and losses in comprehensive income reflects economic realities that might otherwise remain hidden. During the 2008 financial crisis, many banks reported positive net income but significant negative comprehensive income due to unrealized losses on securities. This discrepancy provided a more accurate picture of the financial sector’s health during that turbulent period.

Comprehensive income significantly influences investment decisions. Investors who analyze comprehensive income gain a more complete understanding of a company’s financial position, which can lead to more informed investment choices. For example, a company with consistently positive net income but negative comprehensive income (due to factors such as currency translation losses) might signal potential long-term risks that aren’t immediately apparent from the income statement alone.

The reporting of comprehensive income enhances financial transparency. It allows stakeholders to see how external economic factors (such as changes in currency exchange rates or market values of investments) affect a company’s overall financial position. This transparency can foster greater trust between companies and their stakeholders, as it provides a more holistic view of financial performance.

As we move forward, we’ll explore how companies account for and present comprehensive income in their financial statements, shedding light on the practical aspects of this important financial concept.

Both GAAP and IFRS require companies to report comprehensive income. The Financial Accounting Standards Board (FASB) mandates that companies display the components of other comprehensive income (OCI) under GAAP, including foreign currency transactions and translations, available-for-sale securities adjustments, and cash flow hedges. IFRS, set by the International Accounting Standards Board (IASB), has similar requirements with some differences.

A notable distinction lies in the treatment of actuarial gains and losses related to defined benefit pension plans. GAAP allows recognition in OCI, while IFRS requires immediate recognition in profit or loss. This difference can result in significant variations in reported comprehensive income between companies following different standards.

Companies can choose between two primary options for presenting comprehensive income:

The choice of presentation can influence how investors and analysts perceive a company’s financial performance. A single statement might emphasize the relationship between net income and OCI, while separate statements could highlight operational performance more clearly.

Reclassification adjustments (also known as recycling) occur when items previously recognized in OCI are subsequently included in net income. These adjustments prevent double-counting of income and provide transparency about the timing of recognition in net income.

For example, when a company sells an available-for-sale security, it must reclassify any unrealized gains or losses previously recorded in OCI to net income. This process can significantly affect a company’s reported earnings in a given period.

The impact of reclassification adjustments can be substantial. In 2020, General Electric reported $1.5 billion in reclassification adjustments related to currency translation, demonstrating the material effect these adjustments can have on financial statements.

Companies must understand these accounting intricacies to ensure accurate financial reporting and analysis. Proper accounting for comprehensive income provides stakeholders with a clear and comprehensive view of a company’s financial position and performance.

Navigating the complexities of comprehensive income reporting requires expertise. Companies often seek professional assistance to ensure compliance with accounting standards and to present their financial information in the most effective manner.

Comprehensive income in accounting provides a holistic view of a company’s financial health. It encompasses realized and unrealized gains and losses, offering stakeholders a clearer picture of an organization’s economic reality. This broader perspective allows for a more nuanced evaluation of long-term financial stability, revealing potential risks and opportunities.

The importance of understanding and accurately reporting comprehensive income will grow as global markets become increasingly interconnected. We expect to see further refinements in accounting standards to address emerging financial instruments and economic complexities. There might also be a push for greater standardization in how companies present comprehensive income, facilitating easier comparisons across different industries.

Expert guidance proves invaluable for businesses navigating the complexities of comprehensive income reporting. My CPA Advisory and Accounting Partners specializes in helping companies understand and effectively report comprehensive income. Our team of experienced professionals can assist with ensuring compliance with accounting standards, optimizing financial reporting practices, and providing insights that drive informed decision-making.

Privacy Policy | Terms & Conditions | Powered by Cajabra