How to Choose the Best Accounting Services for Small Business

Find the best accounting services for small business. Explore factors, benefits, and tips to simplify your choice and enhance financial management.

High income tax planning is a complex yet essential task for those in upper tax brackets. The stakes are high, with significant portions of earnings at risk without proper strategies in place.

At My CPA Advisory and Accounting Partners, we’ve seen firsthand how effective tax planning can save our high-earning clients substantial sums. This post will explore key strategies to minimize tax liabilities and maximize wealth retention for high-income individuals.

High income earners face unique challenges in tax planning. The IRS uses various thresholds for different tax provisions, rather than a single definition of “high income.”

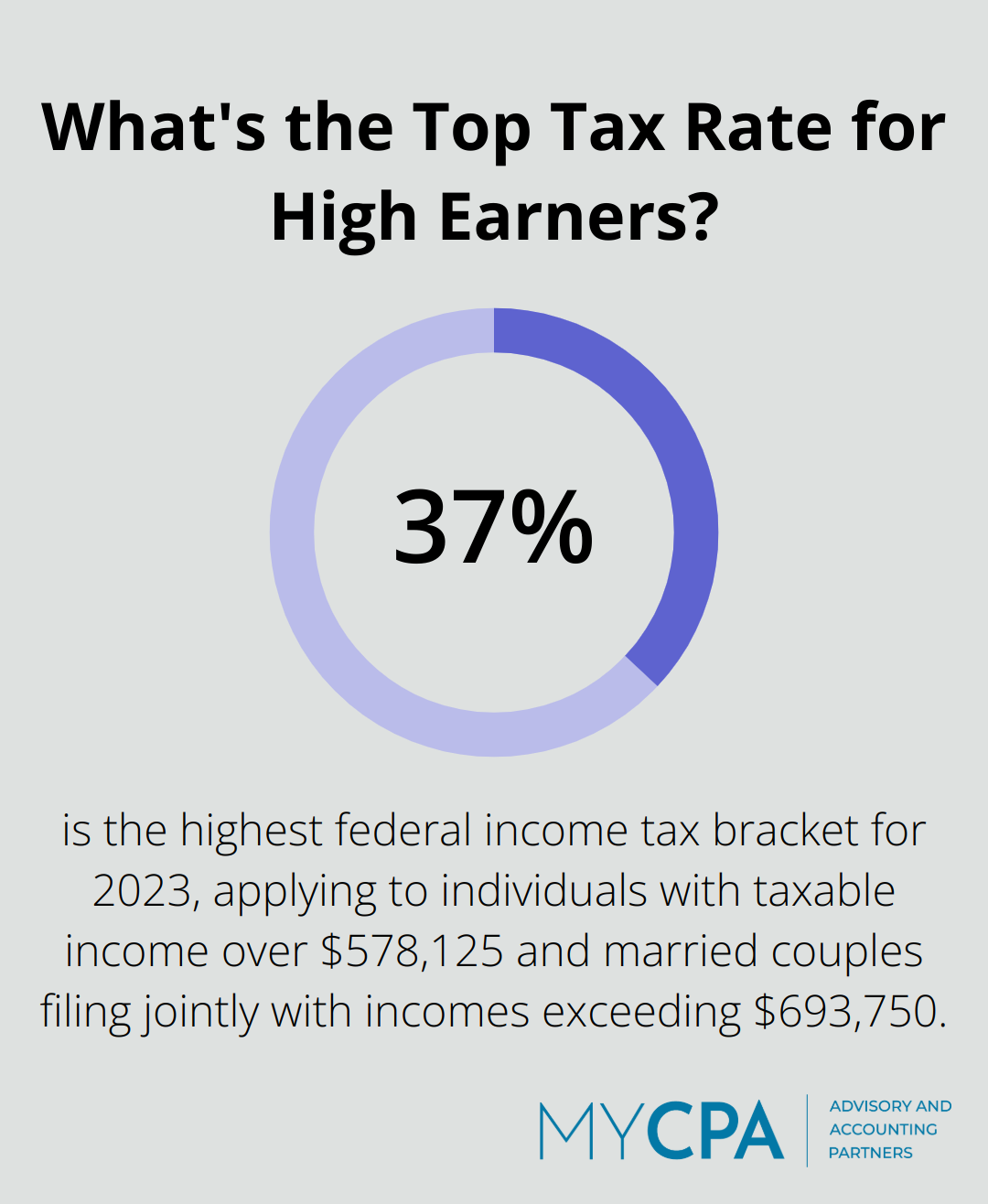

For 2023, the highest federal income tax bracket (37%) applies to individuals with taxable income over $578,125 and married couples filing jointly with incomes exceeding $693,750. This top rate marks a significant increase from the 35% bracket, which starts at $231,250 for single filers and $462,500 for married couples filing jointly.

High income doesn’t just mean higher income tax rates. Earners above certain thresholds face additional taxes:

The progressive nature of the U.S. tax system increases the effective tax rate as income rises. For example, a single filer with $600,000 in taxable income would pay about $186,000 in federal income tax (an effective rate of 31%). This calculation excludes state taxes, which can add significantly to the total tax burden, especially in high-tax states like California or New York.

High income earners should also consider the Alternative Minimum Tax (AMT). While less commonly discussed than regular tax obligations, it’s crucial to understand how the AMT can impact your financial well-being.

Understanding these thresholds and their implications proves essential for effective tax planning. High income earners need to take a proactive approach to manage their tax liabilities. This often requires sophisticated strategies that extend beyond basic tax preparation.

As we move forward, we’ll explore specific strategies that high-income earners can employ to optimize their tax situation and preserve more of their hard-earned wealth.

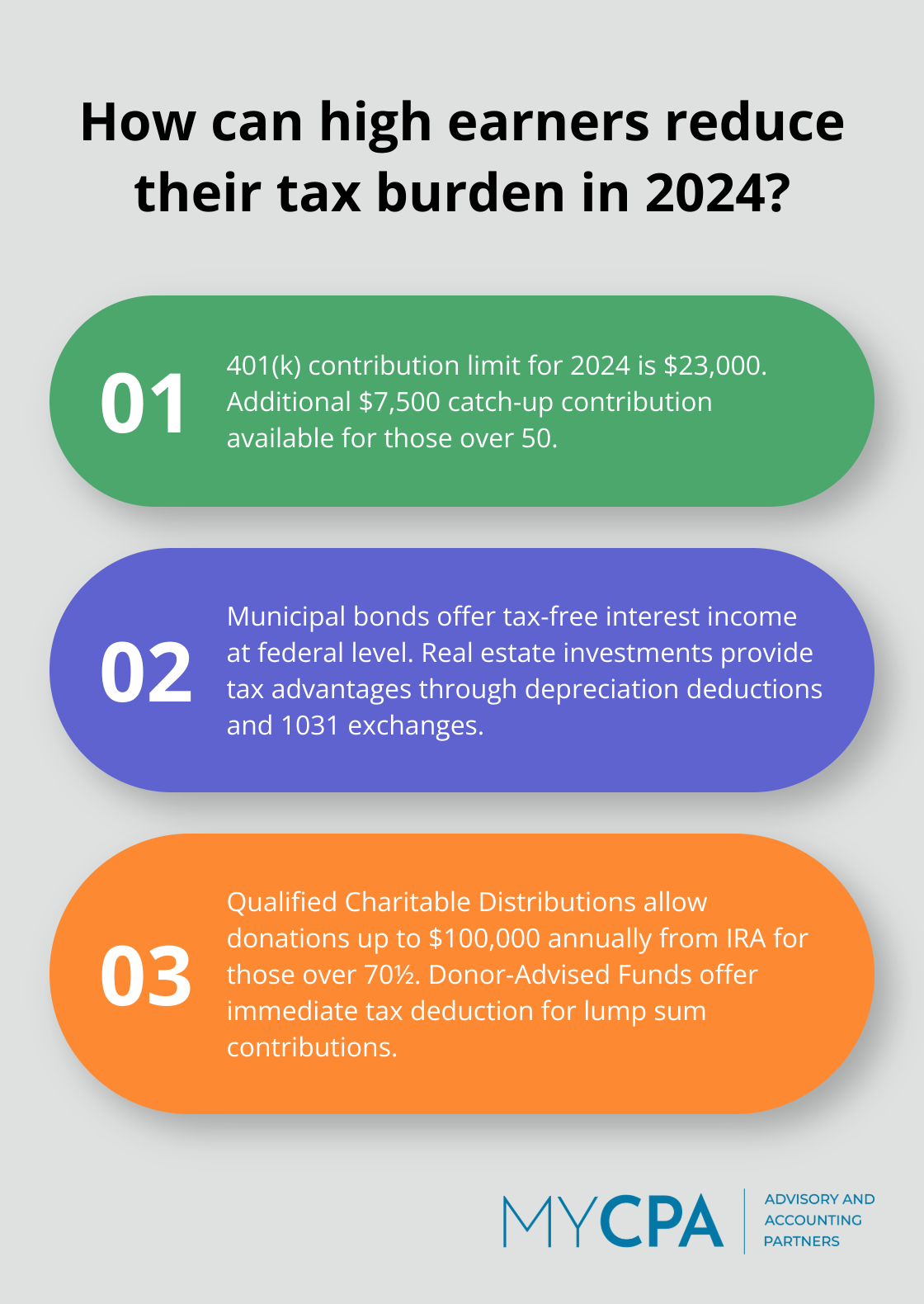

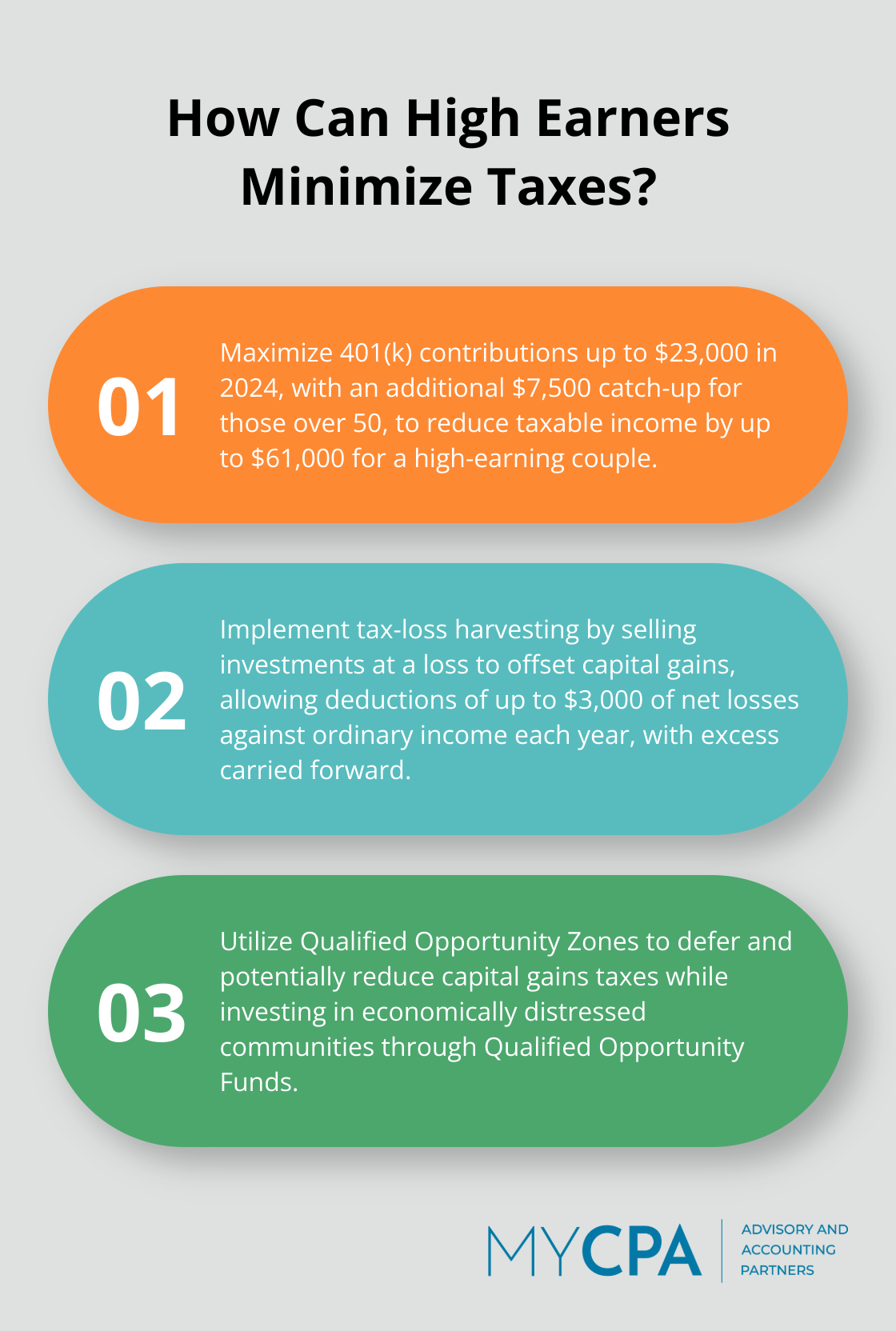

High-income earners can significantly reduce their taxable income by maximizing contributions to tax-advantaged retirement accounts. For 2024, the contribution limit for a 401(k) is $23,000, with an additional $7,500 catch-up contribution for those over 50. A high-earning couple over 50 could potentially reduce their taxable income by up to $61,000 through 401(k) contributions alone.

For those with even higher incomes, a backdoor Roth IRA strategy proves effective. This involves making non-deductible contributions to a traditional IRA and then converting them to a Roth IRA, allowing for tax-free growth and withdrawals in retirement.

Municipal bonds offer tax-free interest income at the federal level (and often at the state level for residents). While the yields might be lower than taxable bonds, the tax benefits can result in a higher after-tax return for high-income individuals.

Real estate investments also provide tax advantages through depreciation deductions and the potential for 1031 exchanges, which allow for the deferral of capital gains taxes when reinvesting in similar properties.

Charitable contributions not only support causes you care about but can also significantly reduce your tax burden. For those over 70½, Qualified Charitable Distributions (QCDs) allow you to donate up to $100,000 annually from your IRA directly to charities without incurring taxable income.

Donor-Advised Funds (DAFs) offer another powerful tool. You can contribute a lump sum in a high-income year, receive an immediate tax deduction, and then distribute the funds to charities over time.

For high-income business owners, the choice of business structure can have a substantial impact on tax liabilities. S-Corporations, for instance, can help reduce self-employment taxes by allowing owners to pay themselves a reasonable salary and take additional income as distributions.

Additionally, the Qualified Business Income (QBI) deduction allows eligible pass-through business owners to deduct up to 20% of their qualified business income (subject to certain limitations).

The implementation of these strategies requires careful planning and expertise. A qualified tax professional (such as those at MyCPA Advisory and Accounting Partners) can help develop comprehensive tax planning strategies tailored to your unique financial situation. They can also keep you informed about changes in tax laws that may affect your planning.

As we move forward, we’ll explore more advanced tax planning techniques that high-income earners can use to further optimize their tax situation and preserve their wealth.

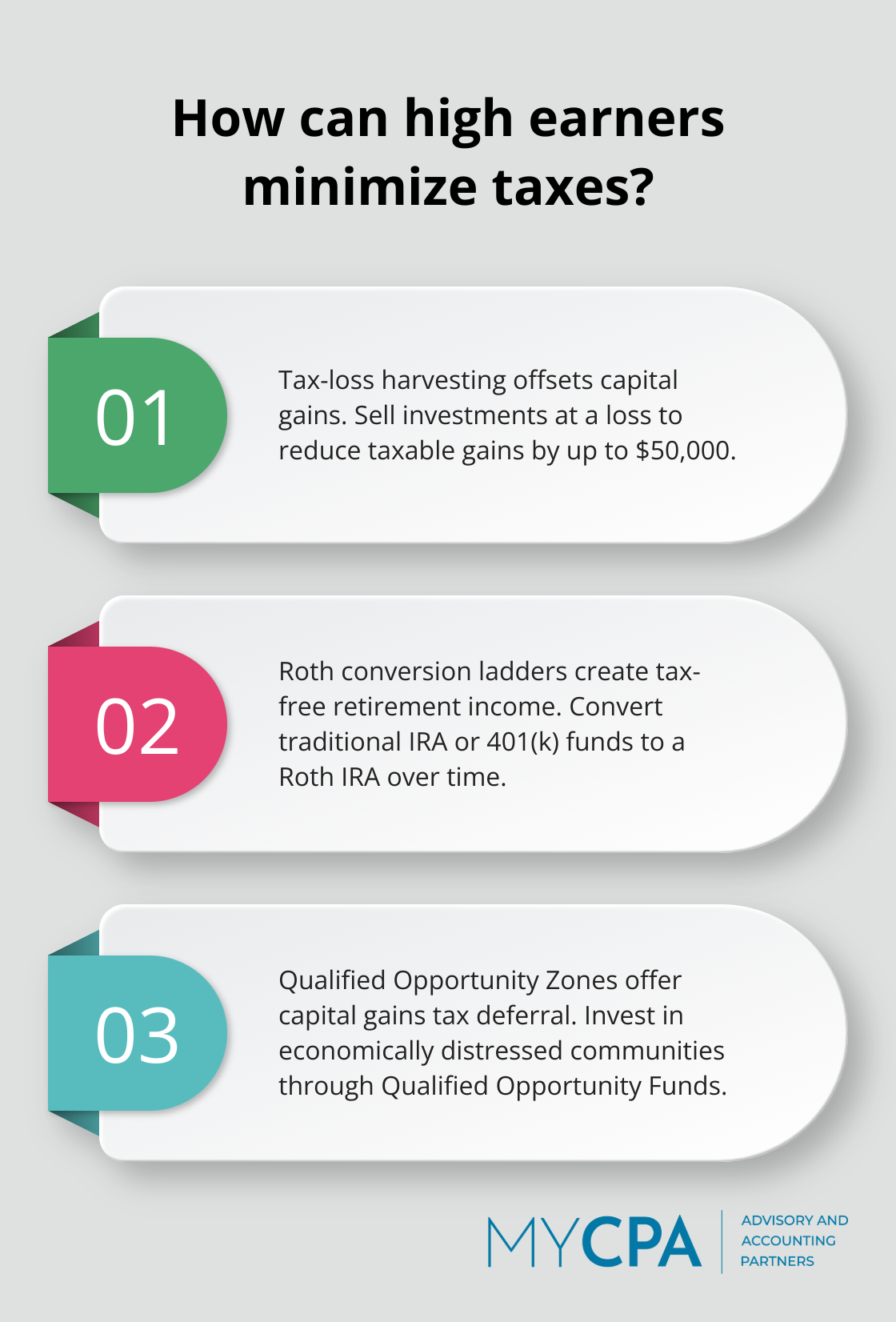

High-income earners can use tax-loss harvesting to minimize their tax burden. This strategy involves selling investments at a loss to offset capital gains. For instance, if you have $50,000 in long-term capital gains and sell investments with $30,000 in losses, you’ll only owe taxes on $20,000 of gains. The IRS allows deductions of up to $3,000 of net losses against ordinary income each year (with excess carried forward).

Be aware of the wash-sale rule, which prohibits claiming a loss on a security if you buy the same or a “substantially identical” security within 30 days before or after the sale. A knowledgeable advisor can help you navigate these rules effectively.

High earners who exceed income limits for direct Roth IRA contributions can benefit from Roth conversion ladders. This strategy converts traditional IRA or 401(k) funds to a Roth IRA over several years. You pay taxes on the converted amount each year, but this creates a substantial pool of tax-free retirement income.

The key is to time these conversions strategically. You might convert larger amounts in years when your income is lower or when you have significant deductions to offset the additional taxable income from the conversion.

Qualified Opportunity Zones (QOZs) offer a way to defer and potentially reduce capital gains taxes while investing in economically distressed communities. Taxpayers can invest in these zones through Qualified Opportunity Funds. You can support economic development in Qualified Opportunity Zones and temporarily defer tax on eligible gains.

Carefully evaluate the underlying investments in QOZs. Not all QOZ projects are created equal, and the tax advantages shouldn’t overshadow the need for sound investment fundamentals.

High-net-worth individuals should prioritize estate planning to minimize estate taxes and ensure efficient wealth transfer. High-net-worth families have time to take advantage of higher estate and gift tax exemptions before they’re significantly reduced if TCJA provisions sunset.

Strategies like establishing irrevocable trusts, leveraging annual gift tax exclusions, and using valuation discounts for closely-held business interests can help reduce potential estate tax liabilities. A Grantor Retained Annuity Trust (GRAT) can allow you to transfer appreciation on assets to heirs with minimal gift tax consequences.

Estate planning isn’t just about tax minimization; it ensures your assets are distributed according to your wishes and provides for your loved ones. Regular reviews and updates to your estate plan are essential as your financial situation and tax planning strategies change.

High income tax planning requires a multifaceted approach to manage tax liabilities and preserve wealth effectively. The strategies we discussed can significantly reduce your tax burden and enhance your long-term financial well-being. However, the complexity of tax laws and the ever-changing financial landscape make professional guidance invaluable.

A skilled tax advisor can help you navigate intricate regulations, identify opportunities specific to your situation, and develop a comprehensive plan that aligns with your financial goals. They can also keep you informed about legislative changes that may impact your tax strategy (ensuring you’re always prepared to make informed decisions). At My CPA Advisory and Accounting Partners, we specialize in providing tailored financial services for high-income individuals and business owners.

Our team of experts can help you implement effective tax planning strategies, manage your accounting needs, and offer valuable business advisory services. We take a proactive approach to your financial management, working closely with you to minimize tax liabilities and maximize your financial health. Contact My CPA Advisory and Accounting Partners today to start optimizing your tax strategy and securing your financial success.

Privacy Policy | Terms & Conditions | Powered by Cajabra