Month-End Close Process: Best Practices for Accurate Reporting

Streamline your month-end close process with best practices for accurate financial reporting and stronger accounting controls

Strategic tax planning is more than just a yearly chore-it’s a powerful tool for financial success. At My CPA Advisory and Accounting Partners, we’ve seen firsthand how effective tax strategies can significantly boost savings for both businesses and individuals.

This comprehensive guide will explore proven techniques to minimize your tax burden and maximize your financial resources. From business entity optimization to personal investment strategies, we’ll cover essential tactics that can transform your approach to taxes.

Strategic tax planning is a proactive approach to manage financial obligations. It involves the analysis of your financial situation and the making of informed decisions to minimize tax liabilities while maximizing savings. At its core, strategic tax planning uses the tax code to your advantage.

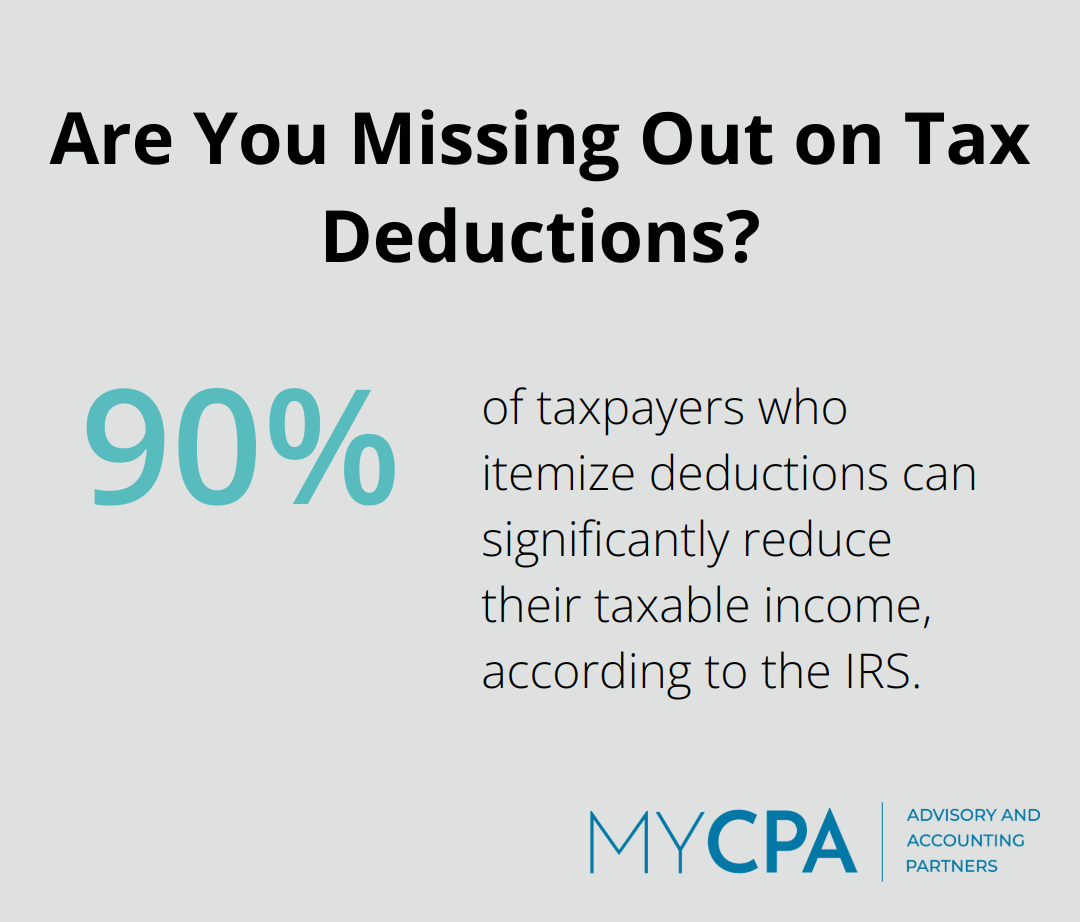

Effective tax planning requires a look beyond the current tax year. The IRS reports that over 90% of taxpayers who itemize deductions can significantly reduce their taxable income. This statistic underscores the importance of a forward-thinking approach. Anticipation of future financial changes and tax law updates allows for decisions today that will benefit you in the years to come.

A solid tax strategy encompasses several critical components:

Many people believe tax planning is only for the wealthy or that it’s too complex for the average person. These misconceptions can lead to missed opportunities. In reality, tax planning benefits individuals at all income levels. For example, maximization of contributions to retirement accounts like 401(k)s can lower your taxable income, which means a lower tax bill in the near term.

Another common myth states that tax planning is only necessary during tax season. In fact, year-round planning is essential. Tax-loss harvesting, for instance, can offset gains and lower taxable income throughout the year, as endorsed by financial experts at Fidelity.

Professional guidance can make a significant difference in the effectiveness of your tax planning strategy. Certified Public Accountants (CPAs) and tax professionals possess in-depth knowledge of tax laws and can provide personalized advice tailored to your specific financial situation.

At MyCPA Advisory and Accounting Partners, we emphasize the importance of ongoing tax planning. Our approach ensures that our clients prepare for tax season well in advance, which avoids last-minute scrambles and potential oversights. The integration of tax planning into your regular financial routine can lead to more informed decisions and potential annual savings of thousands of dollars.

As we move forward, let’s explore specific strategies that businesses can employ to optimize their tax positions and maximize savings.

Businesses have numerous opportunities to reduce their tax liabilities through strategic planning. This chapter explores effective methods to optimize tax positions and maximize savings.

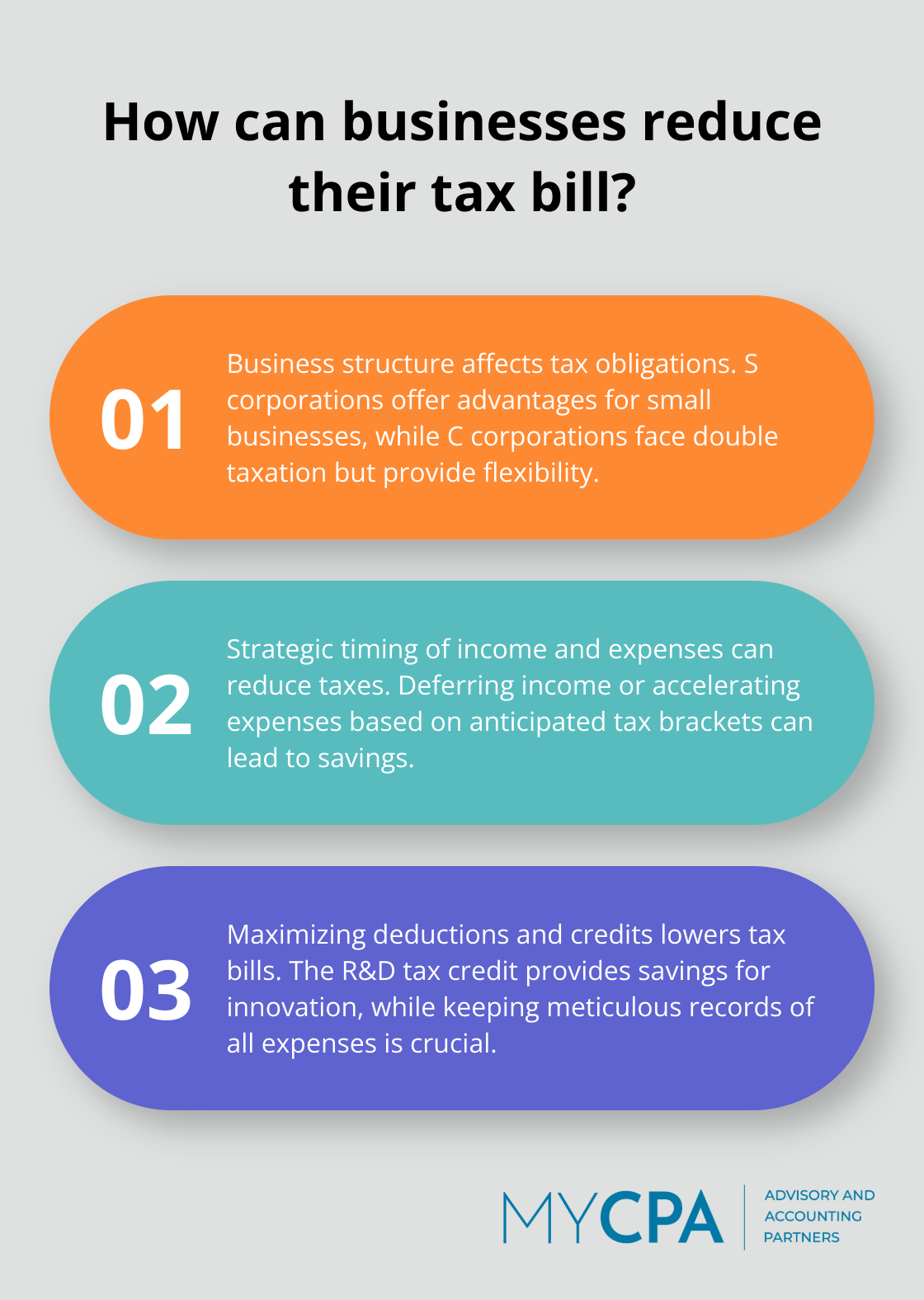

The structure of your business significantly affects your tax obligations. S corporations appeal to small businesses and sole proprietors, offering enticing tax advantages. C corporations face double taxation but offer more flexibility for reinvesting profits. Limited Liability Companies (LLCs) provide tax flexibility and personal asset protection. The optimal structure aligns with your business goals and financial situation.

Strategic timing of income and expenses can substantially reduce your tax bill. If you expect to be in a lower tax bracket next year, consider deferring income to the following year. If you anticipate being in a higher bracket, accelerate income into the current year. The same principle applies to expenses – prepay deductible expenses if you’re in a high tax bracket this year.

The tax code offers numerous deductions and credits that can lower your tax bill. The Research and Development (R&D) tax credit provides substantial savings for businesses investing in innovation. Don’t overlook smaller deductions either – they can add up quickly. Keep meticulous records of all business expenses (from office supplies to mileage).

Offering comprehensive employee benefits and retirement plans not only attracts talent but also serves as a powerful tax-saving strategy. Contributions to employee health insurance premiums are tax-deductible for employers. Setting up a 401(k) plan allows your business to deduct contributions made on behalf of employees. For 2024, the 401(k) contribution limit is $76,500 if you include catch-up contributions.

Tax laws evolve constantly, and staying informed about these changes is essential for effective tax planning. The Tax Cuts and Jobs Act (TCJA) introduced significant changes to the corporate tax rate, affecting many businesses. Regularly review your tax strategies to ensure they align with current legislation and maximize available benefits.

As we transition to personal tax planning techniques, it’s important to note that many of these business strategies can also apply to individual taxpayers. The next chapter will explore how individuals can optimize their tax positions and increase their savings through strategic planning.

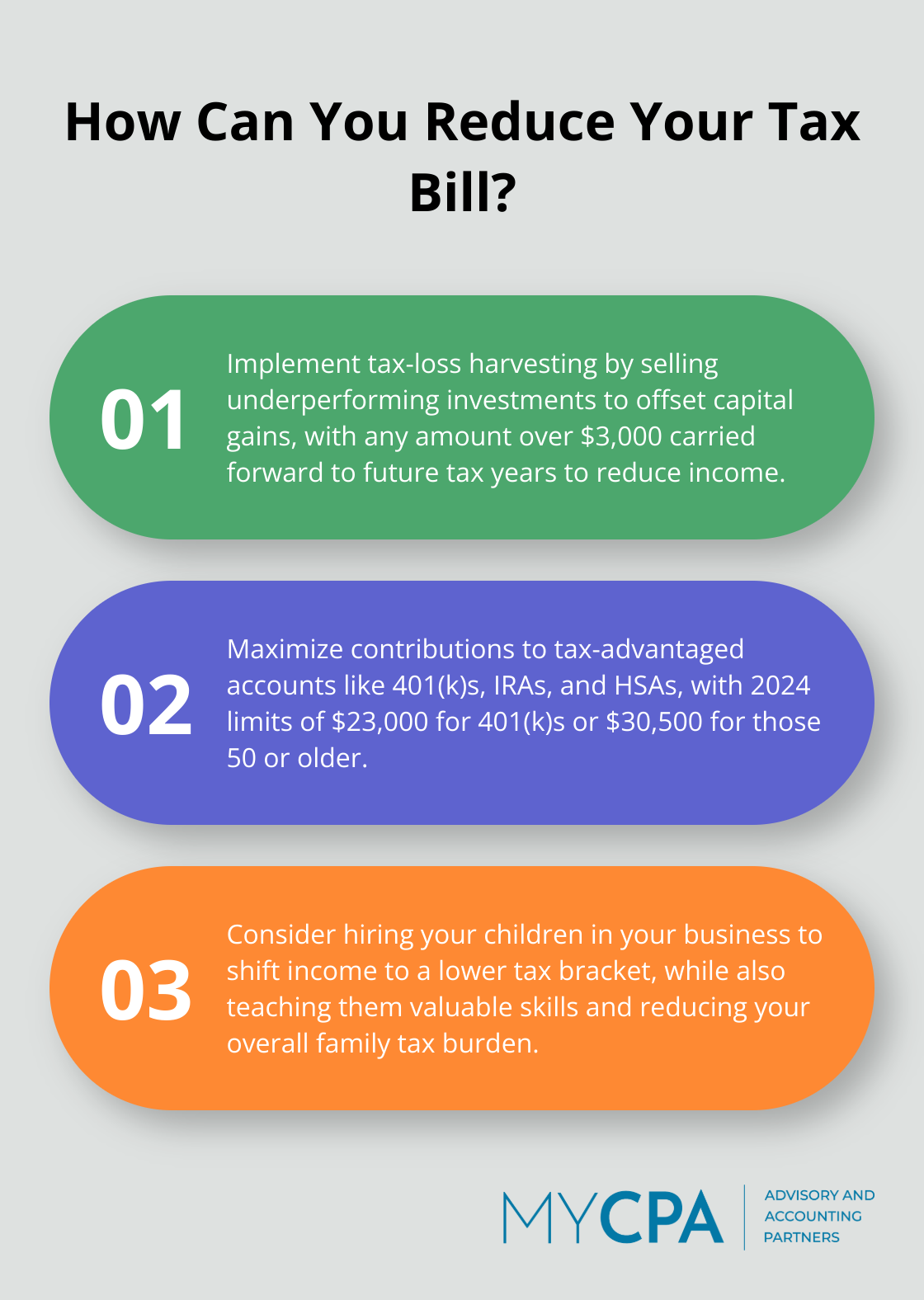

Family tax planning can reduce your tax burden significantly. Income splitting is a tax reduction strategy employed by families living in areas that are subject to bracketed tax regulations. For example, you can hire your children in your business to shift income to a lower tax bracket while teaching them valuable skills.

Family trusts offer another effective strategy. These trusts distribute income among family members, potentially lowering the overall tax burden. However, you must consider the kiddie tax rules, which can limit the tax benefits of transferring investment income to children under 19 (or 24 for full-time students).

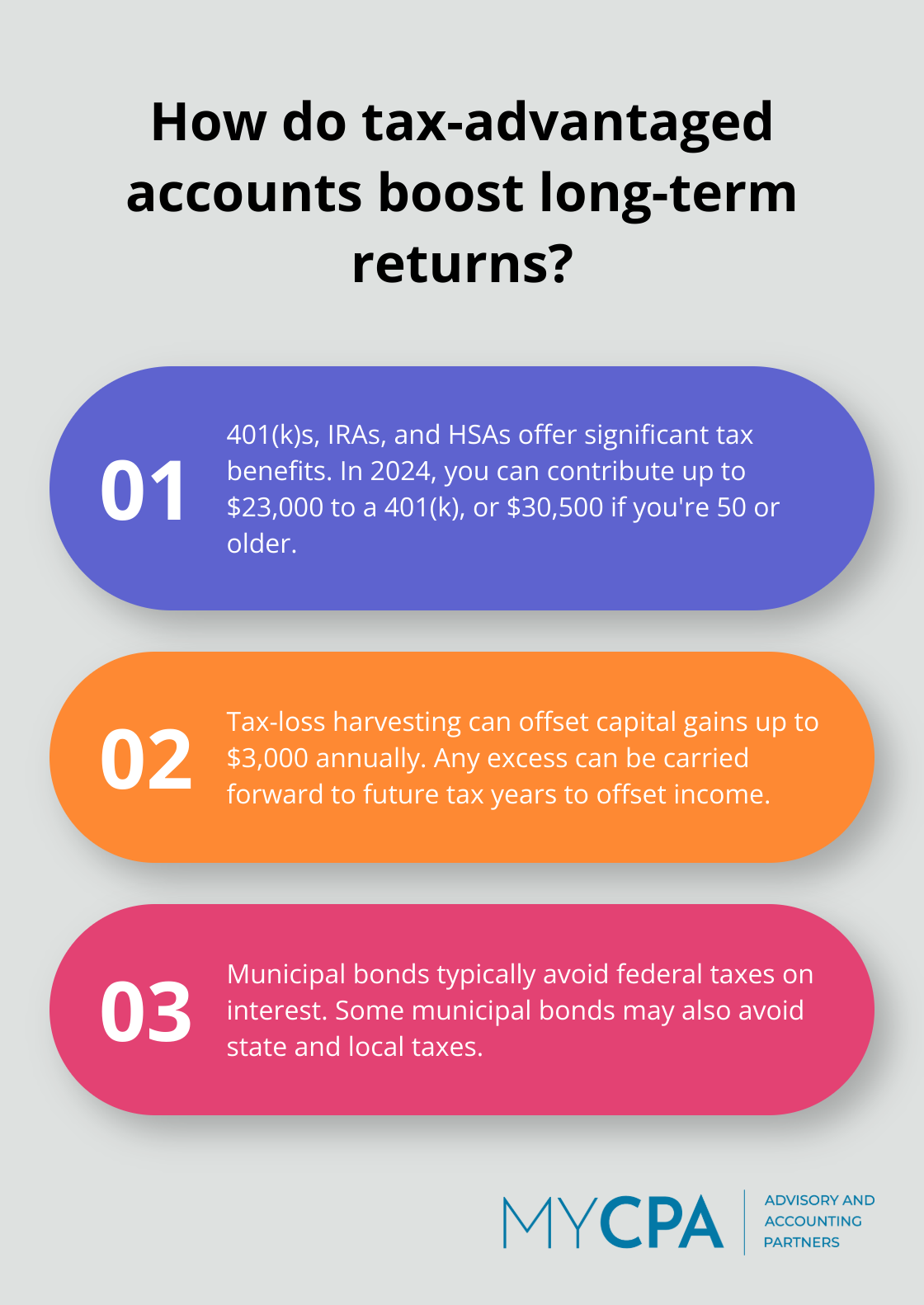

Your investment strategy impacts your tax bill. Tax-loss harvesting involves selling underperforming investments to offset capital gains. Any amount over $3,000 can be carried forward to future tax years to offset income down the road.

Tax-advantaged accounts like 401(k)s, IRAs, and Health Savings Accounts (HSAs) offer significant benefits. These accounts can boost your long-term returns through tax advantages. For 2024, you can contribute up to $23,000 to a 401(k), or $30,500 if you’re 50 or older.

Municipal bonds provide another tax-efficient investment option. The interest from these bonds typically avoids federal taxes (and sometimes state and local taxes as well).

Real estate investments offer numerous tax advantages. The mortgage interest deduction allows you to deduct the interest paid on your home loan (up to certain limits). Property tax deductions can also provide significant savings, though they’re now capped at $10,000 per year under the Tax Cuts and Jobs Act.

Rental property owners benefit from depreciation. This allows you to deduct a portion of your property’s value each year, even as the property potentially appreciates. You can also deduct expenses related to managing and maintaining the property.

Charitable giving supports causes you care about and can lower your tax bill. Donating appreciated assets, such as stocks, proves particularly tax-efficient. You avoid paying capital gains tax on the appreciation and can deduct the full market value of the asset.

For those over 70½, Qualified Charitable Distributions (QCDs) from IRAs can satisfy Required Minimum Distributions (RMDs) without increasing taxable income. This strategy benefits those who don’t itemize deductions especially.

Try bunching charitable donations in alternating years to exceed the standard deduction threshold. This allows you to itemize deductions in some years while taking the standard deduction in others, maximizing your tax benefits over time.

Strategic tax planning offers significant benefits for businesses and individuals. It reduces tax burdens and maximizes savings through careful entity structure selection, strategic timing, and deduction maximization. Tax-efficient investing, real estate strategies, and charitable giving also play key roles in effective tax planning.

Professional guidance proves invaluable in navigating complex tax laws and regulations. My CPA Advisory and Accounting Partners specializes in tailored financial services to help you optimize your tax strategies. We ensure you make informed decisions that align with your financial goals and maximize tax savings.

The implementation of an effective strategic tax plan starts with an assessment of your current financial situation and future goals. It requires the application of discussed strategies and regular review to ensure optimal results. A proactive approach to tax planning will transform your financial outlook and pave the way for long-term success.

Privacy Policy | Terms & Conditions | Powered by Cajabra