Monthly Close Checklist: Tighten Your Month-End Close

Streamline your month-end accounting with our monthly close checklist. Reduce errors and close faster with proven best practices.

At My CPA Advisory and Accounting Partners, we know that smart tax planning can significantly reduce your income tax burden. Many taxpayers overlook valuable opportunities to keep more money in their pockets.

This guide will show you how to save income tax through tax planning, with strategies you can implement right away. We’ll cover everything from basic tax concepts to advanced investment tactics, helping you make informed decisions about your finances.

Income tax is a financial obligation that affects nearly every working individual and business in the United States. It represents a percentage of your earnings that you pay to the government. This money funds various public services and programs.

The IRS recognizes several types of taxable income. These include railroad retirement annuities, rewards, income from the sale of a home, and proceeds from selling personal items. Additionally, some scholarships and fellowships may be taxable, especially if they involve payment for services. However, there are exceptions to these rules, and it’s important to consult the IRS guidelines or a tax professional for specific situations.

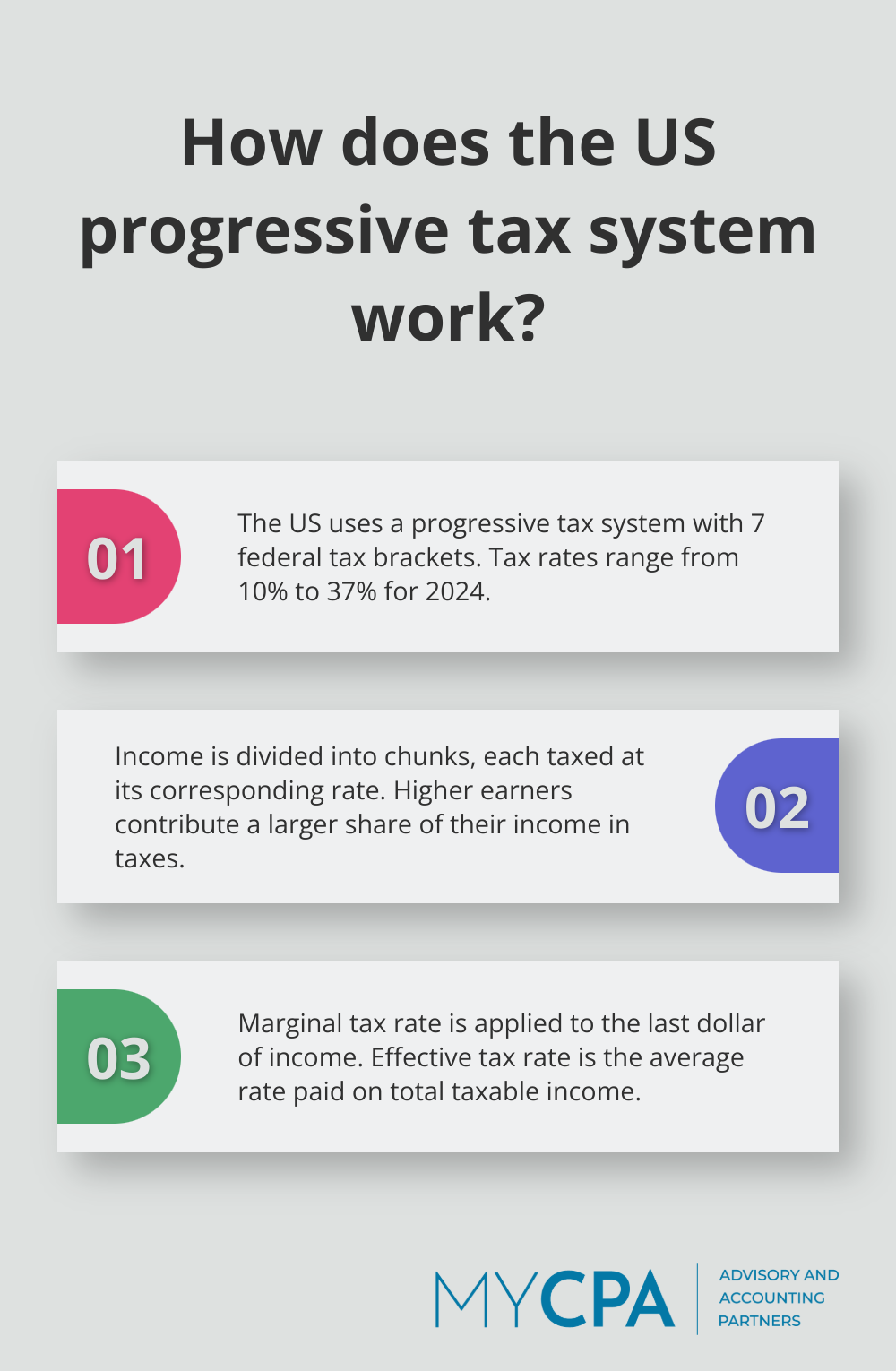

The U.S. uses a progressive tax system, which means tax rates increase as your income grows. For 2024, there are seven federal tax brackets ranging from 10% to 37%. Your income doesn’t all get taxed at one rate. Instead, it’s divided into chunks (each taxed at its corresponding rate). This system ensures that higher earners contribute a larger share of their income in taxes.

A common misconception exists about tax brackets. Moving into a higher tax bracket doesn’t mean all your income is taxed at that higher rate. Your marginal tax rate is the rate applied to your last dollar of income, while your effective tax rate is the average rate you pay on your total taxable income. Understanding this difference is key for effective tax planning.

The U.S. tax code is complex and changes frequently. Staying informed about current tax laws and working with professionals can help you navigate these complexities and identify opportunities for tax savings. This knowledge of tax basics forms the foundation for developing a comprehensive tax strategy.

As we move forward, we’ll explore effective strategies to maximize your tax savings and minimize your tax burden. These techniques will build upon the fundamental concepts we’ve just covered, allowing you to make more informed decisions about your finances.

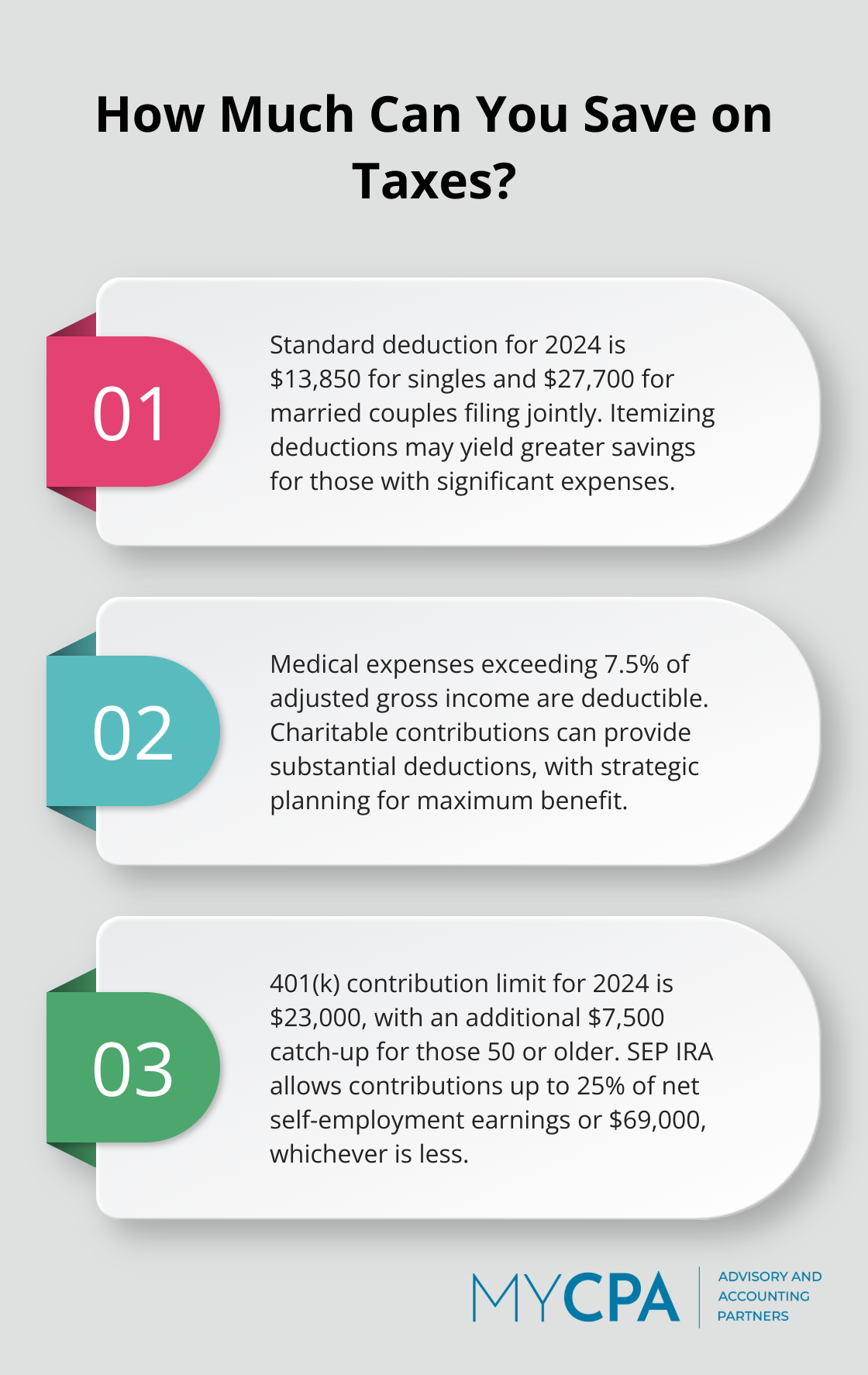

Lowering your taxable income requires claiming every deduction you’re entitled to. For 2024, the standard deduction stands at $13,850 for single filers and $27,700 for married couples filing jointly. However, itemizing deductions might yield greater savings if you have significant expenses in certain categories.

Medical expenses exceeding 7.5% of your adjusted gross income are deductible. This includes costs for doctors, dentists, hospitals, and even health insurance premiums. Keep detailed records of all health-related expenses throughout the year.

Charitable contributions can also provide substantial deductions. Consider concentrating your donations into a single tax year to exceed the standard deduction threshold. For instance, if you typically donate $5,000 annually, you could donate $10,000 every other year to maximize your tax benefit.

Contributing to retirement accounts is one of the most effective ways to reduce your taxable income. For 2024, you can contribute up to $23,000 to a 401(k) plan (with an additional $7,500 catch-up contribution if you’re 50 or older).

If you’re self-employed or run a small business, consider setting up a Simplified Employee Pension (SEP) IRA. These accounts allow contributions of up to 25% of your net earnings from self-employment, or $69,000, whichever is less.

For those with high incomes, a backdoor Roth IRA conversion can be a smart move. While you won’t get an immediate tax deduction, your money will grow tax-free, and you won’t pay taxes on withdrawals in retirement.

Timing plays a critical role in tax planning. If you’re self-employed or have control over when you receive income, consider deferring income to the following year if you expect to be in a lower tax bracket.

Conversely, if you anticipate being in a higher tax bracket next year, you might want to accelerate income into the current year. This strategy can be particularly effective if you’re close to the threshold of a higher tax bracket.

For business owners, consider making major purchases before the end of the tax year to increase your deductions. Section 179 of the tax code allows you to deduct the full purchase price of qualifying equipment and software in the year it’s put into service.

Tax laws are complex and constantly changing. While these strategies can be powerful tools for reducing your tax bill, it’s crucial to work with a qualified tax professional to ensure you’re making the most of every opportunity while staying compliant with tax laws. In the next section, we’ll explore tax-efficient investment strategies that can further optimize your financial position.

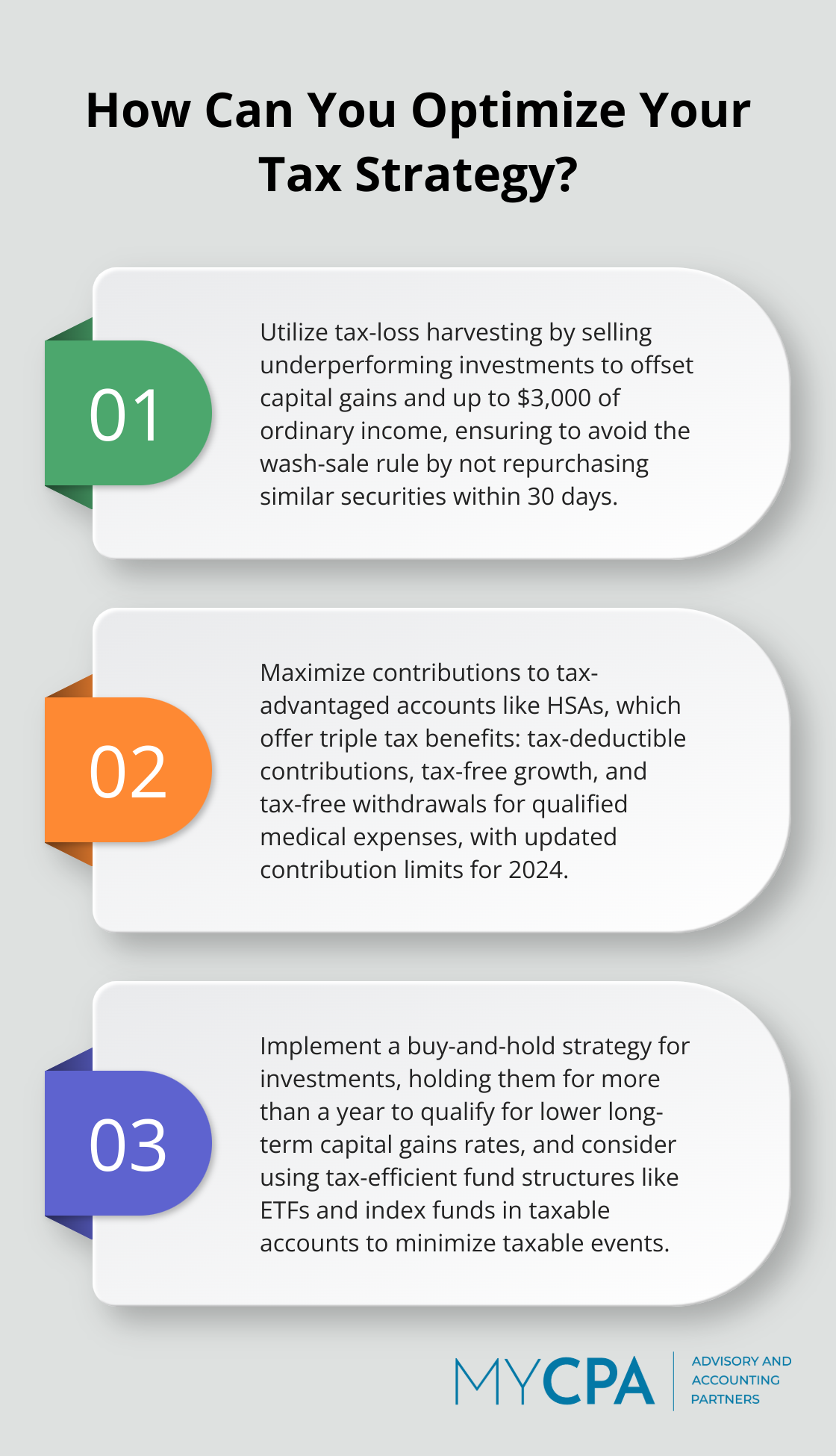

Tax-loss harvesting stands out as a powerful strategy to offset capital gains. This technique involves selling underperforming investments that are losing money. You can then use that loss to reduce your taxable capital gains and potentially offset up to $3,000 of ordinary income if your capital losses exceed your capital gains.

The strategy requires careful timing and selection of assets to sell. You must avoid the wash-sale rule, which prohibits buying a substantially identical security within 30 days before or after the sale. Many investors use this strategy to reduce tax liabilities while rebalancing their portfolios.

Tax-advantaged accounts offer another effective way to minimize your tax burden. Traditional IRAs and 401(k)s provide immediate tax deductions on contributions, while Roth accounts offer tax-free growth and withdrawals in retirement.

High-income earners might benefit from backdoor Roth IRA conversions. This involves contributing to a traditional IRA and then converting it to a Roth IRA. While you pay taxes on the conversion, your money grows tax-free thereafter.

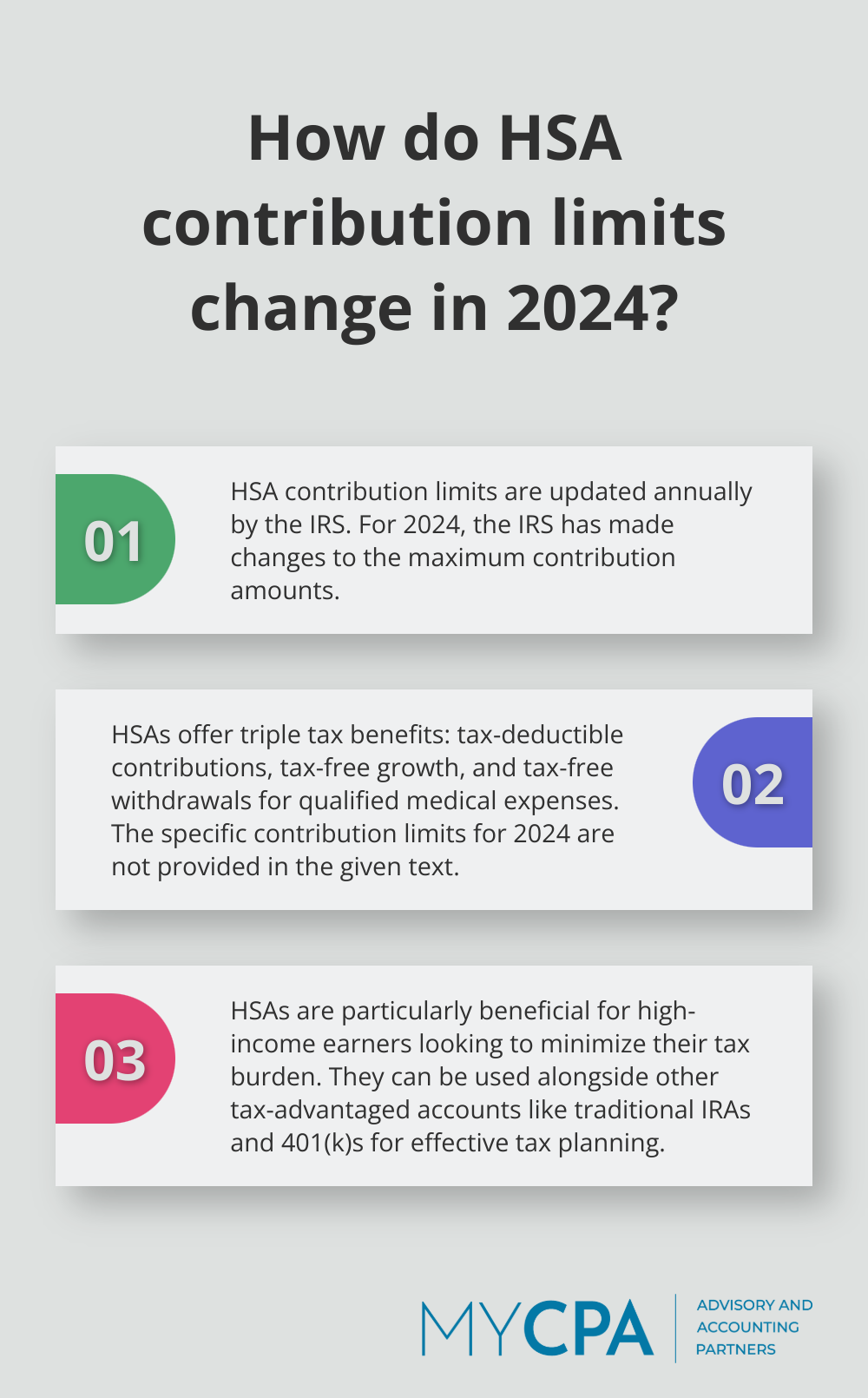

Health Savings Accounts (HSAs) provide triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. The IRS makes changes to the HSA contribution limits each year. For 2024, the maximum contributions and other HSA rules have been updated.

Municipal bonds present an excellent choice for investors in high tax brackets. The interest from these bonds typically remains exempt from federal taxes (and often from state and local taxes if you live in the issuing state).

For example, if you fall in the 35% tax bracket and invest in a municipal bond yielding 3%, your tax-equivalent yield would approximate 4.6%. This means you’d need to find a taxable bond yielding 4.6% to match the after-tax return of the municipal bond.

However, municipal bonds often have lower yields than comparable taxable bonds. A financial advisor can help determine if municipal bonds fit your investment strategy and tax situation.

A buy-and-hold strategy can significantly reduce your tax burden. When you hold investments for more than a year, you qualify for long-term capital gains rates, which are lower than short-term rates. For many investors, this means paying 15% instead of their ordinary income tax rate on gains.

This approach also minimizes the frequency of taxable events. By reducing portfolio turnover, you defer capital gains taxes and allow your investments to compound more efficiently over time.

Certain investment vehicles offer inherent tax advantages. Exchange-Traded Funds (ETFs), for instance, often generate fewer capital gains distributions than traditional mutual funds due to their unique structure. This can result in lower tax bills for investors, especially in taxable accounts.

Index funds also tend to be more tax-efficient than actively managed funds. Their lower turnover rates typically result in fewer taxable events. Try to place tax-efficient investments in taxable accounts and less tax-efficient ones in tax-advantaged accounts to optimize your overall tax situation.

Smart tax planning reduces your income tax burden and keeps more of your hard-earned money. You can lower your tax bill through understanding income tax basics, maximizing deductions, and using retirement accounts effectively. Many people search for “how to save income tax through tax planning PDF” resources, but professional guidance often yields better results than general guides.

At My CPA Advisory and Accounting Partners, we help business owners and individuals minimize tax liabilities and improve financial health. Our tailored financial services include tax planning, accounting, QuickBooks management, and business advisory. We provide personalized strategies that exceed generic advice, offering a proactive partnership in your financial journey.

Effective tax planning requires consistent effort and professional expertise. You can achieve significant tax savings year after year with the right strategies and guidance. Take control of your financial future and start implementing these tax-saving strategies today.

Privacy Policy | Terms & Conditions | Powered by Cajabra