Tax Compliance Readiness 2026: A Practical Roadmap for Growing Businesses

Prepare your business for tax compliance readiness in 2026 with our practical roadmap designed for growing companies.

Owner’s equity is the financial stake you have in your business. It’s what remains after subtracting liabilities from assets, and it directly reflects your company’s financial health and value.

Many business owners overlook owner’s equity management until problems arise. We at My CPA Advisory and Accounting Partners see firsthand how poor equity decisions-from mixing personal and business finances to ignoring tax implications-can undermine long-term growth and profitability.

This guide covers the strategies and mistakes that matter most for managing your equity effectively.

Owner’s equity is the residual value left when you subtract total liabilities from total assets. The formula is straightforward: Assets minus Liabilities equals Owner’s Equity. For a mid-sized business with $2.5 million in assets and $1.2 million in liabilities, owner’s equity sits at $1.3 million. This number matters because it represents your actual financial stake in the business and signals whether the company is solvent or in trouble. Negative equity means liabilities exceed assets, which signals serious financial distress and limits your ability to borrow, attract investors, or weather downturns. A transportation company with $1.875 million in assets and $710,000 in liabilities has owner’s equity of $1.165 million, which translates to genuine financial strength. Most lenders and investors look at this figure first because it reveals whether your business can absorb losses or fund growth without external capital.

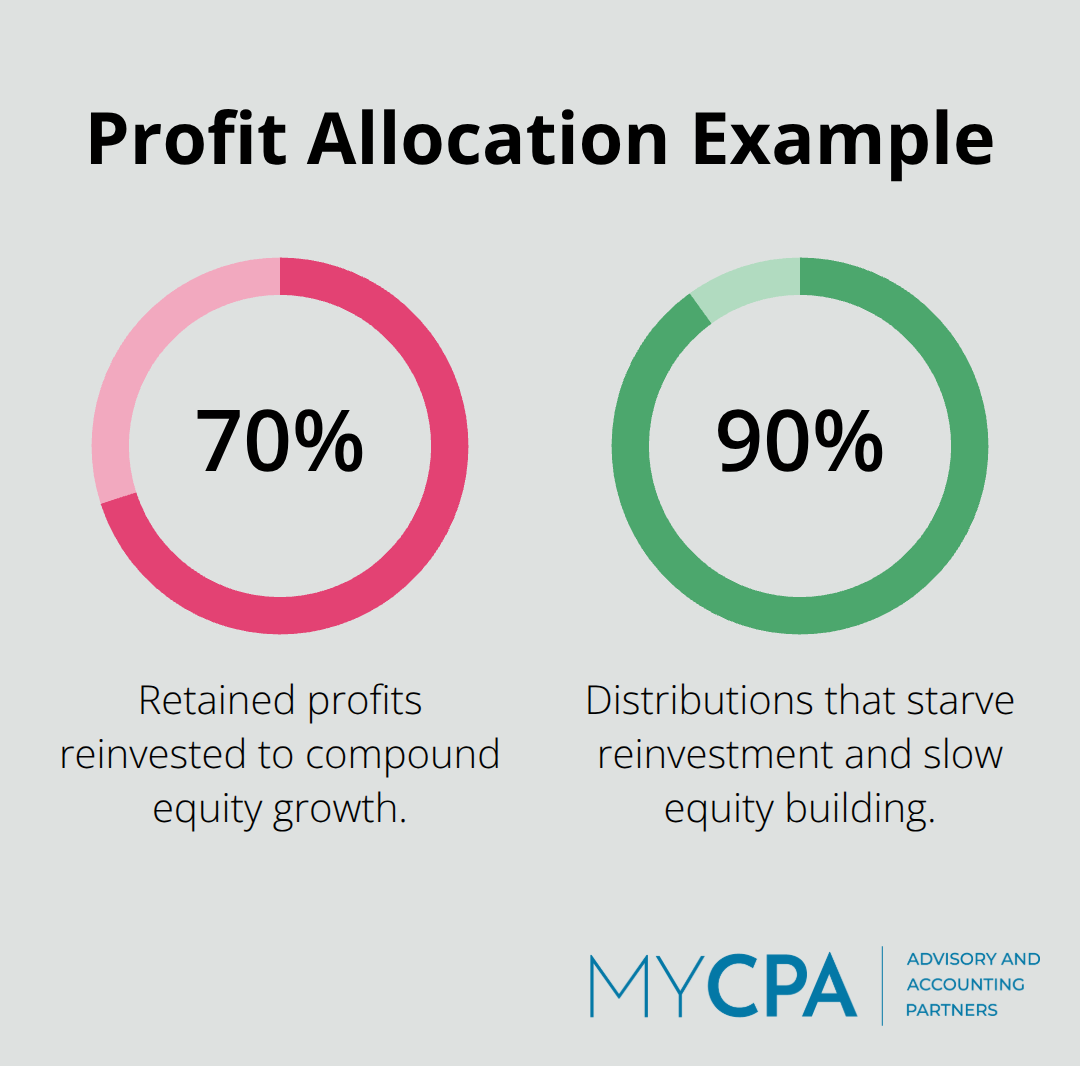

Owner’s equity changes through three primary mechanisms. Retained earnings-the profits you reinvest rather than withdraw-are the largest driver for most businesses. If you retain 70% of annual profits and distribute 30%, retained earnings compound over time and build real equity strength. Capital contributions from you or other owners increase equity immediately but only reflect cash injected into the business. Distributions and withdrawals reduce equity dollar-for-dollar, which is why excessive draws weaken your balance sheet and limit future borrowing capacity. Tax planning directly impacts how much equity you retain because minimizing tax obligations preserves cash. A business owner saving $25,000 through strategic deductions at a 25% tax rate retains that cash for reinvestment, which flows into retained earnings and strengthens equity. Most owners fail to connect tax efficiency to equity growth, treating them as separate concerns when they are fundamentally linked.

Book value-what your balance sheet shows-rarely matches market value. A wholesale distributor with $812,500 in assets and $335,000 in liabilities reports owner’s equity of $477,500 on paper. A buyer might value that same business at $600,000 or $800,000 depending on cash flow, customer concentration, and growth trajectory.

Lenders use equity ratios to set borrowing limits and interest rates. A [debt-to-equity ratio](https://www.investopedia.com/terms/d/debtequityratio.asp] above 2.0 signals financial risk and makes lending expensive or unavailable. A healthy ratio below 1.5 opens doors to favorable terms. Equity also determines how much you can reinvest without diluting ownership or taking on debt. A strong equity position lets you fund equipment purchases, inventory expansion, or market entry from retained earnings instead of borrowing at 6% or higher interest rates. Weak equity forces you into expensive debt or gives up ownership to investors, both of which reduce long-term returns to you as the owner.

The gap between book value and market value creates friction in capital decisions. You may think your equity position is stronger than lenders perceive it, which affects your ability to access favorable financing. Equity also constrains your strategic options. If your debt-to-equity ratio sits at 1.8, you cannot easily borrow for growth without jeopardizing financial stability. This constraint forces you to choose between slower organic growth, expensive equity financing that dilutes your ownership, or aggressive cost-cutting that may harm operations. Understanding your actual equity position-not just the number on your balance sheet-shapes every major decision you make about debt, investment, and distribution. The strategies that strengthen equity require you to understand which levers move the needle most in your specific situation.

The fastest way to strengthen your equity position is to retain profits instead of extracting them. Most business owners treat retained earnings as optional, but the math is unavoidable: a business that retains 70% of annual profit and reinvests it will compound equity growth far faster than one that distributes 90% and struggles to fund growth. If your business generates $200,000 in annual profit and you retain $140,000, that amount flows directly into retained earnings and strengthens your balance sheet.

Over five years at consistent profit levels, you accumulate $700,000 in additional equity without taking on debt or diluting ownership.

The alternative costs far more. Excessive distributions force you to fund growth through debt, which costs 6% or higher in interest and reduces your actual returns. A business owner who borrows $100,000 at 6% interest to fund what retained earnings could have covered loses $6,000 annually in interest alone. This is not a theoretical problem; it happens constantly when owners prioritize cash draws over balance sheet strength.

The second lever is managing how you inject and withdraw capital. Capital contributions increase equity immediately but you should track them separately from retained earnings so you understand what portion of your equity comes from reinvested profits versus fresh injections. Withdrawals and distributions work the opposite direction, reducing equity dollar-for-dollar. If your business has $1.3 million in equity and you withdraw $50,000, equity drops to $1.25 million instantly, which weakens your debt-to-equity ratio and borrowing capacity.

Many owners treat owner withdrawals as casual decisions when they should be strategic. The best practice is to set a withdrawal policy based on cash flow needs and equity targets. If you need $60,000 annually for personal expenses but your business generates $200,000 in profit, take the $60,000 and reinvest the remaining $140,000. This approach builds real wealth over time instead of extracting cash that could compound.

Tax planning amplifies profit retention significantly. A business that structures compensation to minimize tax obligations preserves additional cash available for reinvestment. These strategies and deductions are not bonuses; they are cash that stays in the business and strengthens your equity position when you reinvest them rather than distribute them.

The connection between tax efficiency and equity growth matters more than most owners realize. Strategic deductions preserve thousands of dollars annually that you can direct toward balance sheet strength instead of tax payments. This preserved cash compounds over time and creates genuine financial leverage without additional borrowing.

Understanding your specific tax situation requires professional guidance, which is why many business owners work with accounting professionals who can identify opportunities aligned with your equity and growth goals. The right tax strategy turns what feels like a compliance obligation into a tool that directly strengthens your financial position.

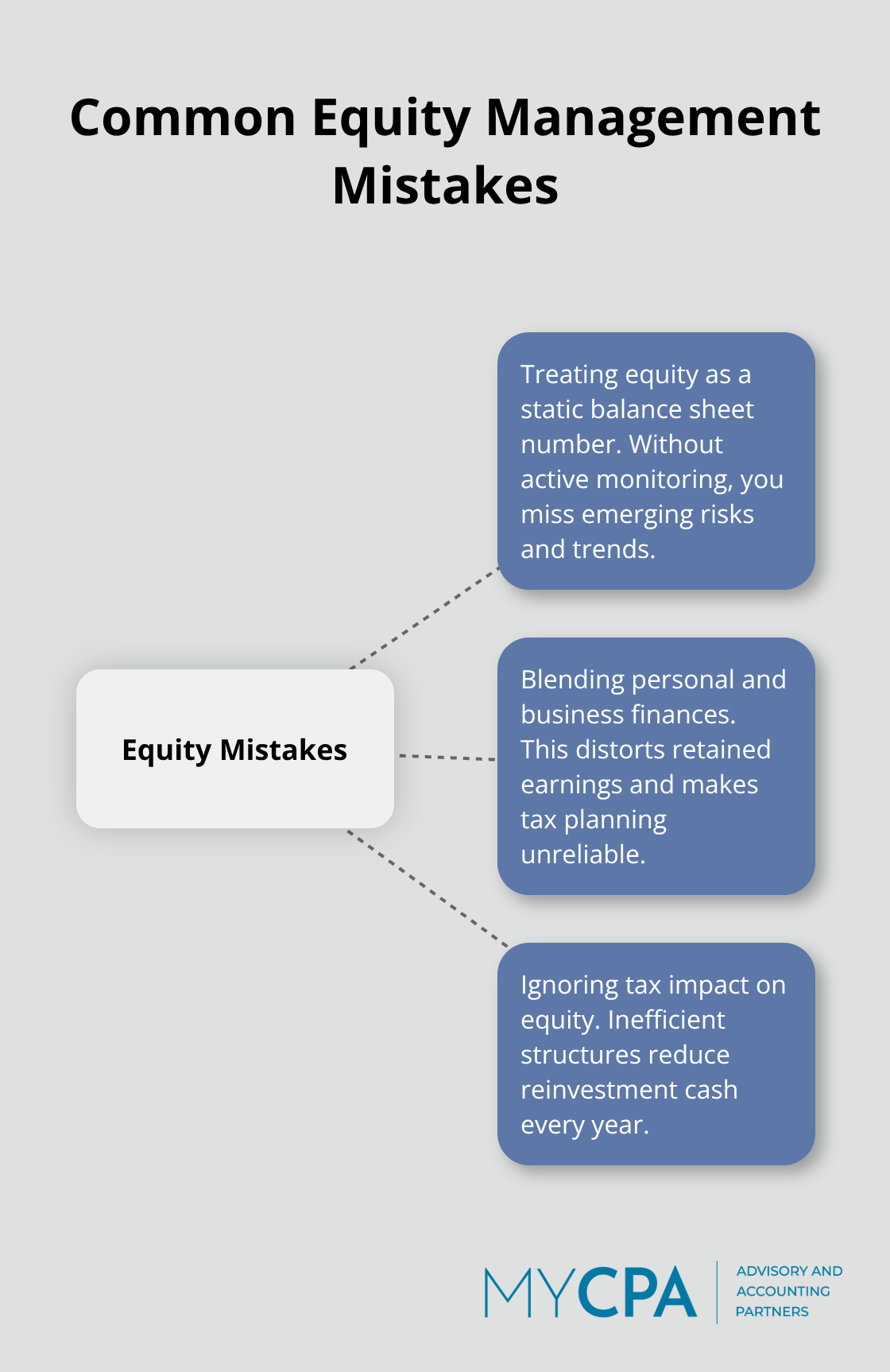

Most business owners fail at equity management not because they lack ambition but because they ignore three preventable mistakes that compound over years. The first mistake is treating equity as a number that appears on the balance sheet rather than a metric you actively monitor and influence. Without quarterly tracking, you cannot see whether retained earnings are growing, whether distributions are sustainable, or whether your debt-to-equity ratio is drifting toward risky territory.

A business owner who checks equity annually is already six months behind on spotting problems. The second mistake is blending personal and business finances, which destroys your ability to calculate accurate equity and makes tax planning nearly impossible. When you pay personal expenses from the business account or deposit personal income into the business, your retained earnings figure becomes meaningless because you cannot separate what the business actually earned from what you extracted. The third mistake is ignoring how tax decisions affect equity retention. Many owners focus on minimizing their current-year tax bill without recognizing that inefficient tax structures cost them thousands in reinvestment capital annually. These three mistakes interact and amplify each other, turning what should be a straightforward financial picture into a murky mess that prevents you from making confident capital decisions.

Quarterly equity reviews serve as your early warning system for financial stress. When you track equity quarterly, you see immediately whether retained earnings are accumulating as expected or whether excessive distributions are eroding your balance sheet strength. A business that generates $50,000 in quarterly profit but withdraws $45,000 is barely building equity, which means within two years it will lack the cash reserves to fund growth or weather a revenue dip. Quarterly tracking also reveals whether your debt-to-equity ratio is creeping upward, which signals that you are borrowing faster than you are building equity. If your ratio climbs from 1.2 to 1.6 over two quarters, you have concrete data to adjust either your borrowing or your profit retention strategy before the ratio reaches dangerous levels above 2.0. Pull a balance sheet and calculate owner’s equity every quarter using your accounting software, then compare it to the previous quarter and the same quarter last year. This takes 30 minutes and eliminates the surprise of discovering months later that your equity position has weakened. Most businesses that struggle with debt-to-equity ratios above 2.0 never saw the problem coming because they checked equity once a year or not at all.

Mixing personal and business finances destroys equity visibility and creates tax complications that cost money. When you pay a personal credit card from the business account, you reduce retained earnings on the books even though that cash left the business for personal use. When you deposit a personal bonus or investment into the business account, you inflate retained earnings when you should record a capital contribution instead. Over time, these transactions create a retained earnings figure that bears no relationship to actual profit the business earned. The solution is absolute separation: use a dedicated business bank account for all business transactions, use a personal account for all personal expenses, and pay yourself through documented owner withdrawals or salary that appear on your tax return. This separation makes equity calculations accurate and tax planning straightforward. It also protects you legally if the business faces disputes or litigation, because your personal and business assets remain clearly distinct. Many owners resist this discipline because it feels bureaucratic, but the cost of not doing it appears in inflated tax bills, weak equity reporting, and an inability to refinance debt at favorable rates because lenders cannot trust your financial statements.

A business owner who ignores tax planning voluntarily reduces the cash available for equity reinvestment. Strategic deductions, retirement plan contributions, and compensation structure decisions preserve thousands annually that flow into retained earnings instead of tax payments. A sole proprietor earning $200,000 who maximizes deductions and retirement contributions might reduce taxable income to $150,000, saving roughly $12,500 at a 25% tax rate. That $12,500 stays in the business and compounds as retained earnings, which strengthens equity without requiring additional borrowing or owner contributions. Most owners know they should optimize taxes but treat it as a year-end scramble with an accountant rather than a strategic decision integrated into equity planning. The better approach is to work with accounting professionals who understand your equity goals and can identify which deductions, entity structures, and timing strategies align with your goal to retain profits and build balance sheet strength. These professionals help business owners connect tax efficiency directly to equity growth by showing how specific decisions preserve reinvestment capital.

Owner’s equity management shapes your ability to fund growth, access favorable financing, and build genuine wealth from your business. Pull your most recent balance sheet and calculate your current owner’s equity using the formula Assets minus Liabilities, then calculate your debt-to-equity ratio by dividing total liabilities by owner’s equity. If that ratio sits above 1.5, your priority is increasing retained earnings or reducing debt over the next 12 months; if it sits below 1.0, you have capacity to invest in growth or equipment without jeopardizing financial stability.

Audit how personal and business finances overlap immediately. If you pay personal expenses from the business account or deposit personal income into business accounts, open a separate personal account and establish a documented owner withdrawal policy that reflects your actual cash needs (this separation takes one afternoon to implement and eliminates years of financial confusion). Set a quarterly review schedule on your calendar and commit to checking these numbers every three months to prevent the drift that turns manageable equity positions into financial stress.

Connect tax efficiency to your equity goals by identifying which deductions, entity structures, and timing strategies align with your objectives. We at My CPA Advisory and Accounting Partners help business owners move from guessing about their equity position to making confident capital decisions through integrated tax and accounting services tailored to your situation. Reach out to discuss how we can build a financial plan that strengthens your balance sheet and supports your long-term growth.

Privacy Policy | Terms & Conditions | Powered by Cajabra